ASHTY - Ashtead: Still A Long-Term Buy

Summary

- Ashtead has seen a strong price rise in 2023 so far, far outpacing the S&P 500 index. Its upcoming results could bolster it further.

- The construction equipment rental provider has already seen robust growth, and its outlook is healthy too. It also has a record of beating expectations.

- Moderation in construction activity in the US and its own P/E ratio could be seen as deterrents, but its long-term story is still strong.

The construction equipment rental provider Ashtead (ASHTF) has had a great run so far in 2023. The price of its ADRs has risen by 16.3% year-to-date [YTD]. By comparison, the S&P 500 ( SP500 ) is up by 6.7% YTD. ASHTF has now more than wiped out the price losses incurred last year and is in fact trading at 1.65% higher than it was a year ago. This is good progress.

The fact that it was due to rise was evident last year itself, which prompted me to give it a Buy rating on two occasions. Since the first time in September 2022, it's up by almost 31%. The next was in December 2022 , and it has risen 9.5% since then.

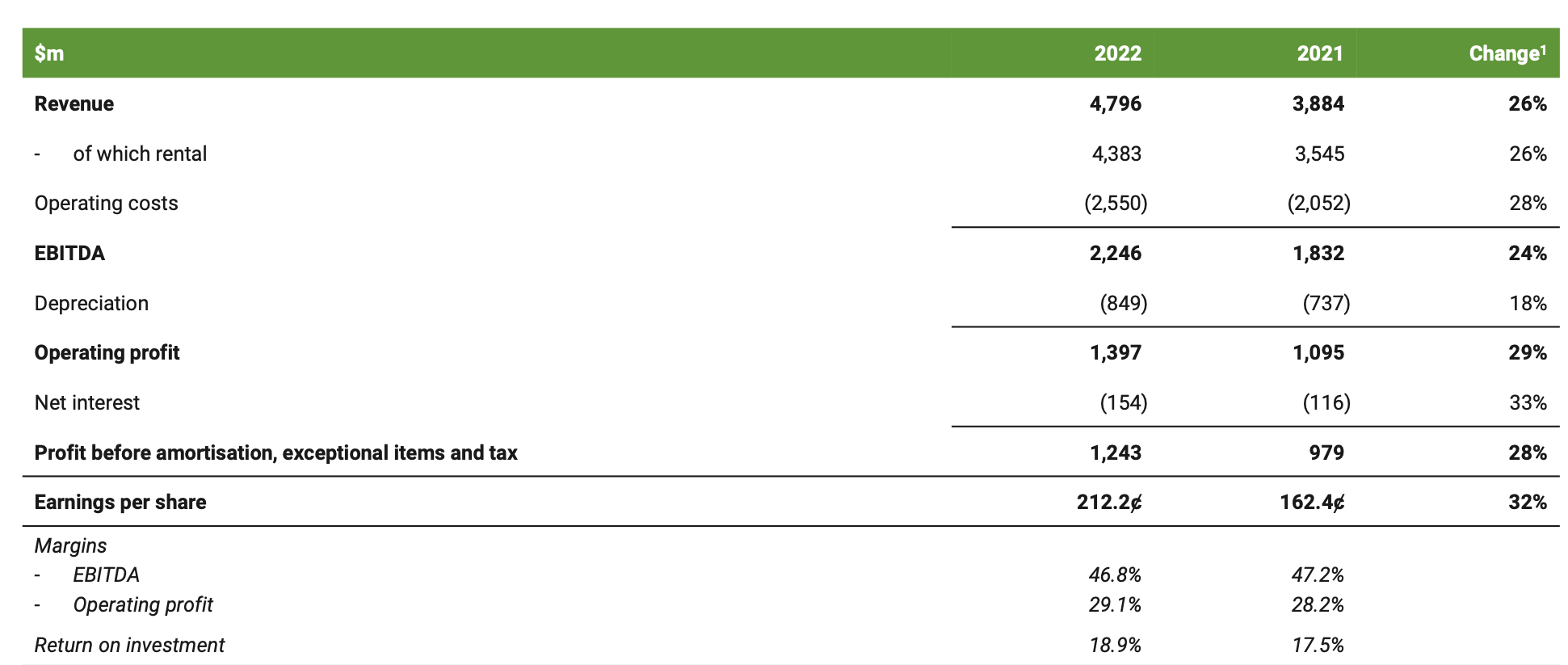

Its upcoming results could further bolster Ashtead's performance. To provide a quick recap, the company has turned in impressive results so far. For the first half of its financial year 2023 (H1 FY23), its revenue grew by 26% year-on-year (YoY) and its earnings per share [EPS] rose by 38%. Its operating profit margin is also strong at 29.1% (see table below).

{kind=link}

Upcoming results could support Ashtead's price

The company estimates a full-year increase in rental revenue, which accounts for over 91% of total revenues between 18% and 21%. According to my calculations, this can translate into an increase of at least 20% for the first nine months of the year (9M FY23), for which the numbers are due in early March.

This calculation is a straightforward one based on the forecasted estimates for the full-year rental revenue by the company, at between 18% to 21% and the numbers already available for the first half of the year. The average revenue forecast from the range provided is divided equally between the third and fourth quarters, the assumption being that they will be similar. This yields the 9M FY23 revenue figures.

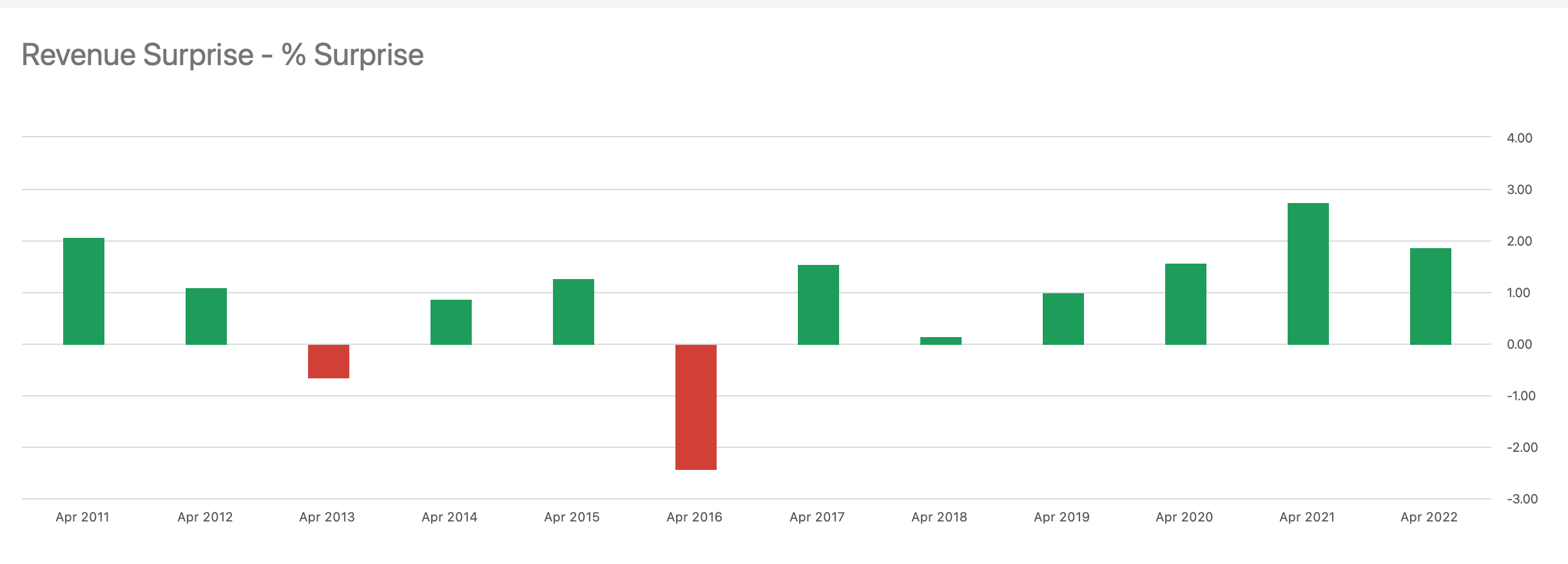

I wouldn't rule out an upside surprise to these. At the start of the year, the company's rental revenue guidance was of 12%-14% growth. It has increased quite a bit from there. Analysts expect the full-year revenue figures to increase by 19.8%, which is in the range provided. But Ashtead has a track record of exceeding expectations. It has done so every year for the past six years. On average, it has surprised by 1.47% in the last five years. If this happens again, we would see revenue growth of 21.6% for FY23, which exceeds even the company's own estimates.

{kind=link}

Leading construction index weakens

However, there is also a downside to consider. The current state of the US construction industry is mixed. Even though the company's UK headquartered, much of its business comes from the US. It has also shown the most robust revenue growth of 30% in H1 FY23 from the US, compared to its other markets Canada (25%) and the UK (-2%).

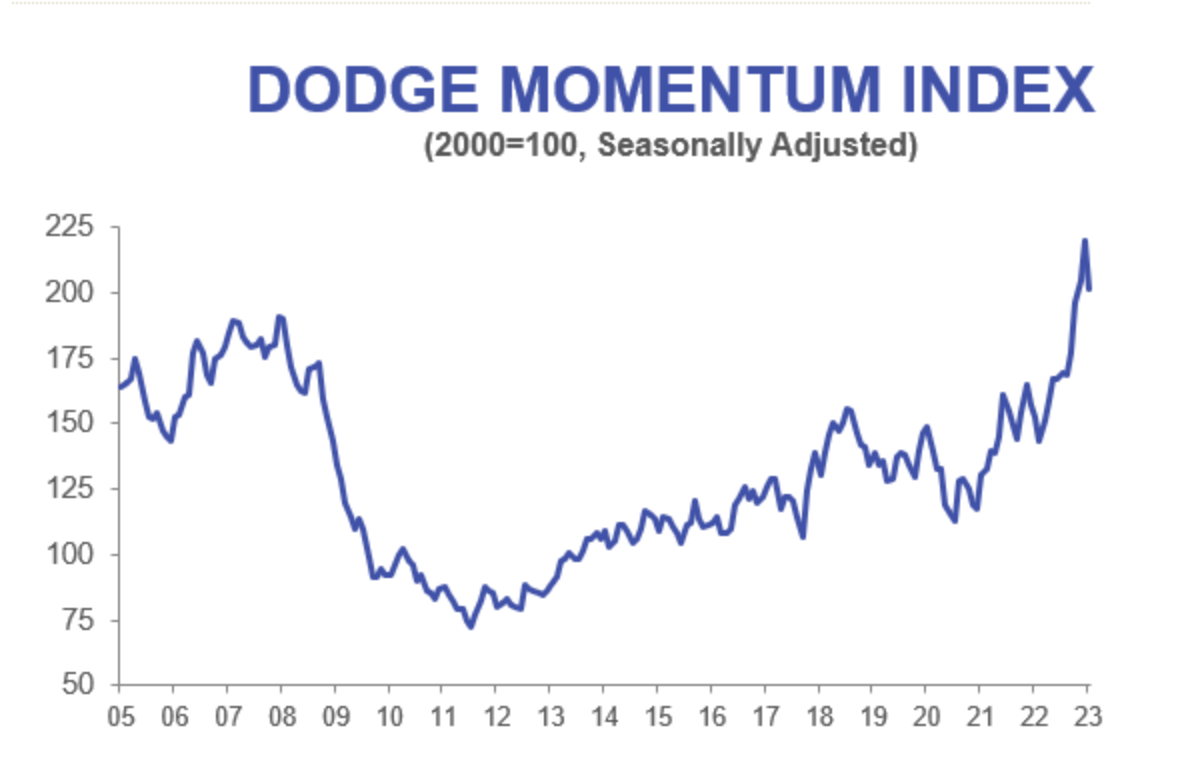

The Dodge Momentum Index, a leading indicator of the US construction industry, which is also referenced in Ashtead's results presentations, declined by 8.4% month-on-month [MOM] in January 2023. It's worth noting that the index was at its all-time high during Ashtead's last earnings release. Dodge Data and Analytics, the provider of the index, has cautioned about slow economic growth in its release. Construction GDP has already been a big drag on US growth in the recent past, which adds to the possibility that the construction industry can sag further.

{kind=link}

Nevertheless, two points are worth considering. First, the index is meant to be a leading indicator of construction activity by a year, which implies that the company shouldn't be affected by a slowdown in the sector in 2023. Second, the release is still positive about the construction industry's future.

Strong construction starts

Moreover, construction starts, also referenced by Ashtead, are however doing quite well. They jumped by a huge 27% MoM in December 2022. According to Richard Branch, Chief Economist at the Dodge Construction Network, "December starts revealed where the current strength in the construction lies: manufacturing and infrastructure… It is those segments that will provide insulation for the sector as the economy softens in 2023."

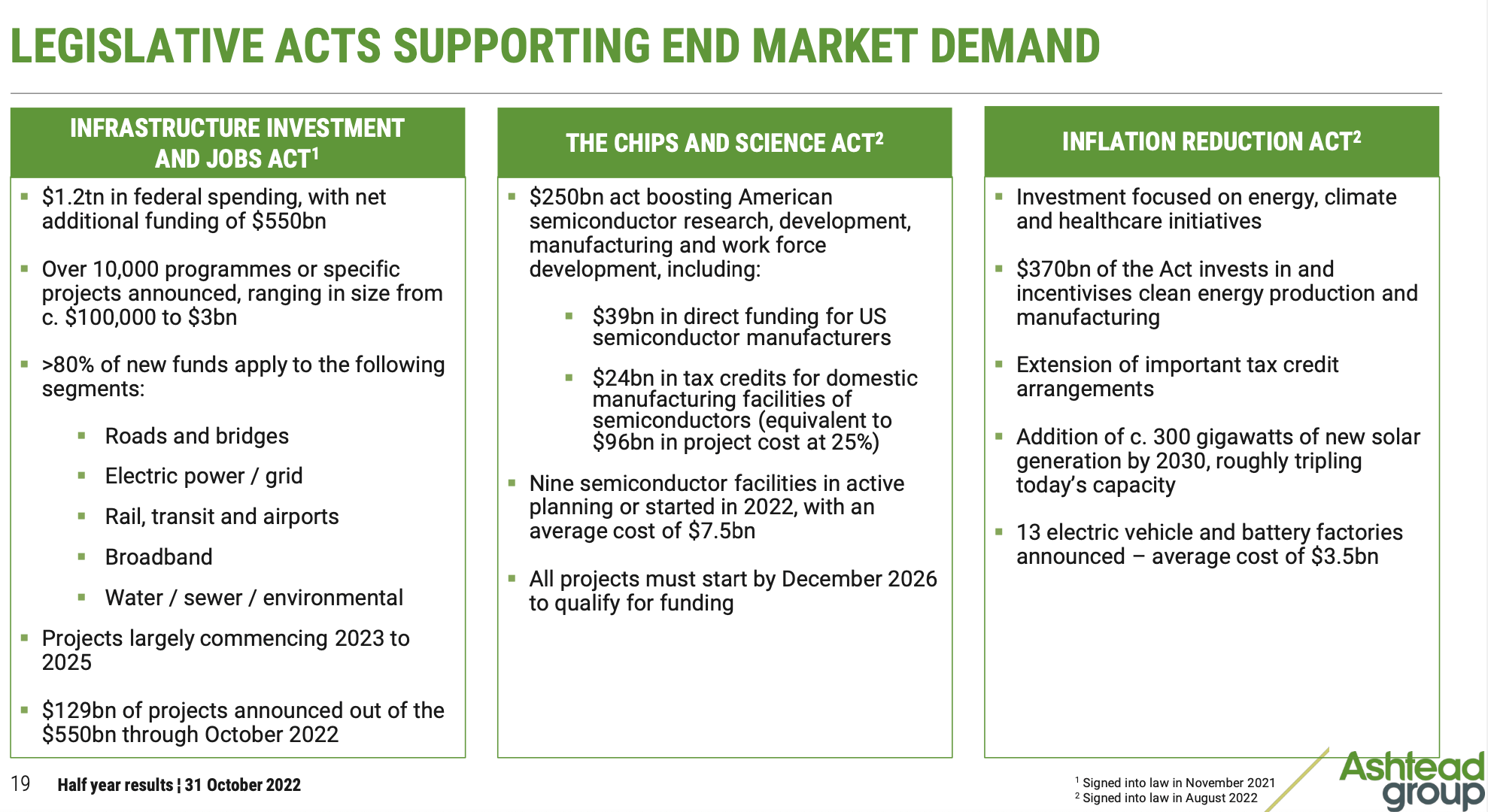

This is in line with Ashtead's own assessment that "Infrastructure, CHIPS and Inflation Reduction Acts bolster and underpin already strong construction market...". It's possible that the January 2023 numbers for starts will show some correction too, but clearly, the medium-term story is looking positive in any case.

{kind=link}

What the P/E says

Just going by the company's market multiples, it seems that at least some further price increase is due. Ashtead's ADRs currently trade at a GAAP price-to-earnings (P/E) ratio of 20.3x, which is less than that for the industrials sector at 21x. This alone indicates a small upside of 3.5% to it. However, it's worth pointing out that Ashtead is currently trading above its last 10 years' median P/E of 17.2x, which indicates a 15% downside to its price.

What next?

Which way will it go? I think at this time, there is a good chance that Ashtead's price can continue to rise further. The markets are more inclined towards cyclical stocks right now. And they are fairly buoyant too. Moreover, its upcoming results look positive too. I do believe that it can come off at some point during this year though, especially if its FY24 outlook is less positive. Analysts are expecting a slowing down in growth to 8.4% for the year. That would be a good time to buy it.

But it's hard to time when it's going to fall. I think it remains a good long-term buy in any case. Over the last 10 years, Ashtead has risen by almost 760% and by 128% in the last five years alone. Moreover, it pays a dividend too. Its yield of 1.21% looks small, but that needs to be seen in the context of its rising share price. The company has grown its dividends every year for the last 10 years.

For further details see:

Ashtead: Still A Long-Term Buy