ASHTF - Ashtead: U.S. Construction Market Indicates Near-Term Uncertainty

2023-09-20 11:46:36 ET

Summary

- Ashtead's stock price has inched up since I gave it a hold rating four months ago. It has released two sets of results in the time.

- Company performance continues to be healthy, with both revenue and earnings growth. Its market multiples also indicated some upside.

- However, there are risks from the continued drop in leading indicators from the US market and its own rental revenue has grown at the lower end of the guidance range too.

- While in the medium term, there's still an upside to Ashtead, in the near term, there could be a better price point at which to buy it.

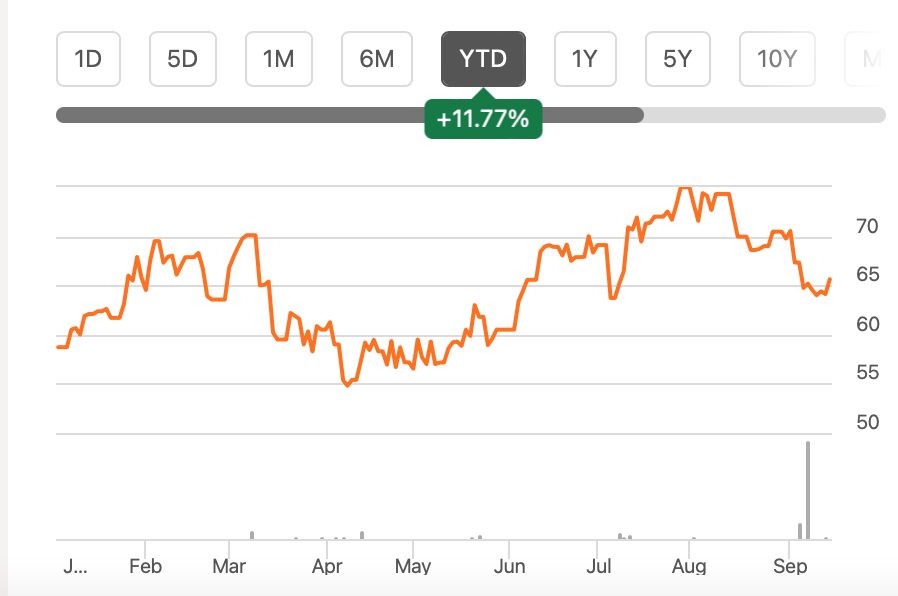

When I last wrote about the construction equipment rental company Ashtead Group ( ASHTF ) in May this year, I gave it a Hold rating based on the uncertain outlook for the US construction sector, its big market. However, in the four months since, its price has risen by 8.5%. This isn't the most impressive price rise, to be sure, but it is enough to merit a relook at the otherwise high-quality stock.

{kind=link}

Financial update

The company has released two sets of results since. Its full-year FY23 number and earlier this month, its first quarter (Q1 FY24, ending July 31, 2023) results.

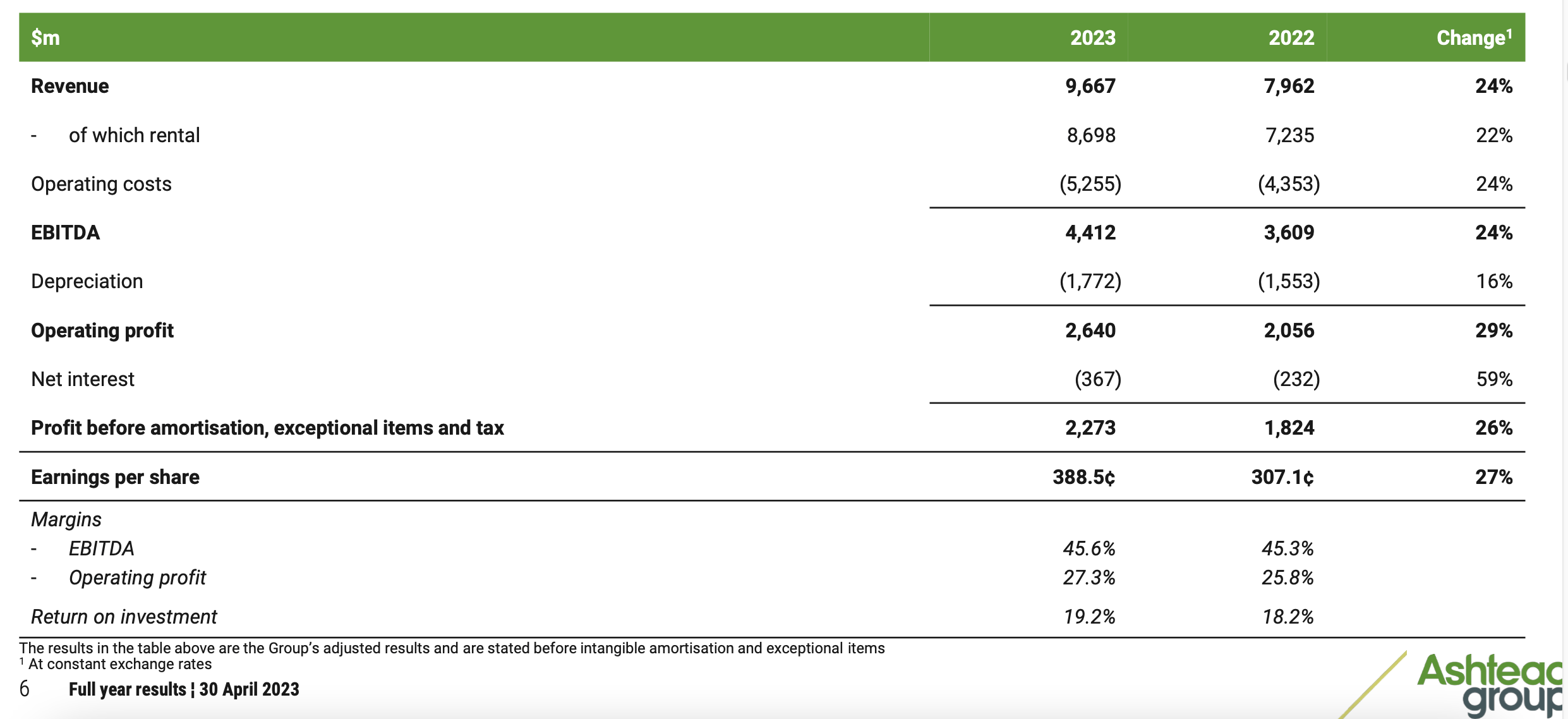

Strong FY23 performance

Let's start with a quick look at its full year figures . Ashtead continued to show a robust 24% revenue growth at constant exchange rates. This was supported significantly by its big rental revenue segment, which contributed to 90% of its total revenue in FY23, with the remaining coming from the sale of both new and used equipment.

The segment saw a 22% rise, which was exactly at the midpoint of the company's guidance range. Total revenue was also significantly pulled up by the sale of used equipment, even as new equipment sales shrank.

The company also saw an improvement in the operating margin to 27.3% for the full year, compared to the already strong 27% for the first nine months of the year (9M FY23), both of which were improvements from the 25.8% margin seen in FY22.

{kind=link}

Revenue growth did slow down to 19% year-on-year (YoY) in Q4, though, resulting in slightly lower FY23 figures than the 25% growth seen until 9M2023. Similarly, EPS growth in Q4 also declined to 19%, bringing the full year figure down to 32% from 36% up to 9M FY23. The softening was already baked into Ashtead's full year forecasts, so it was no surprise, really.

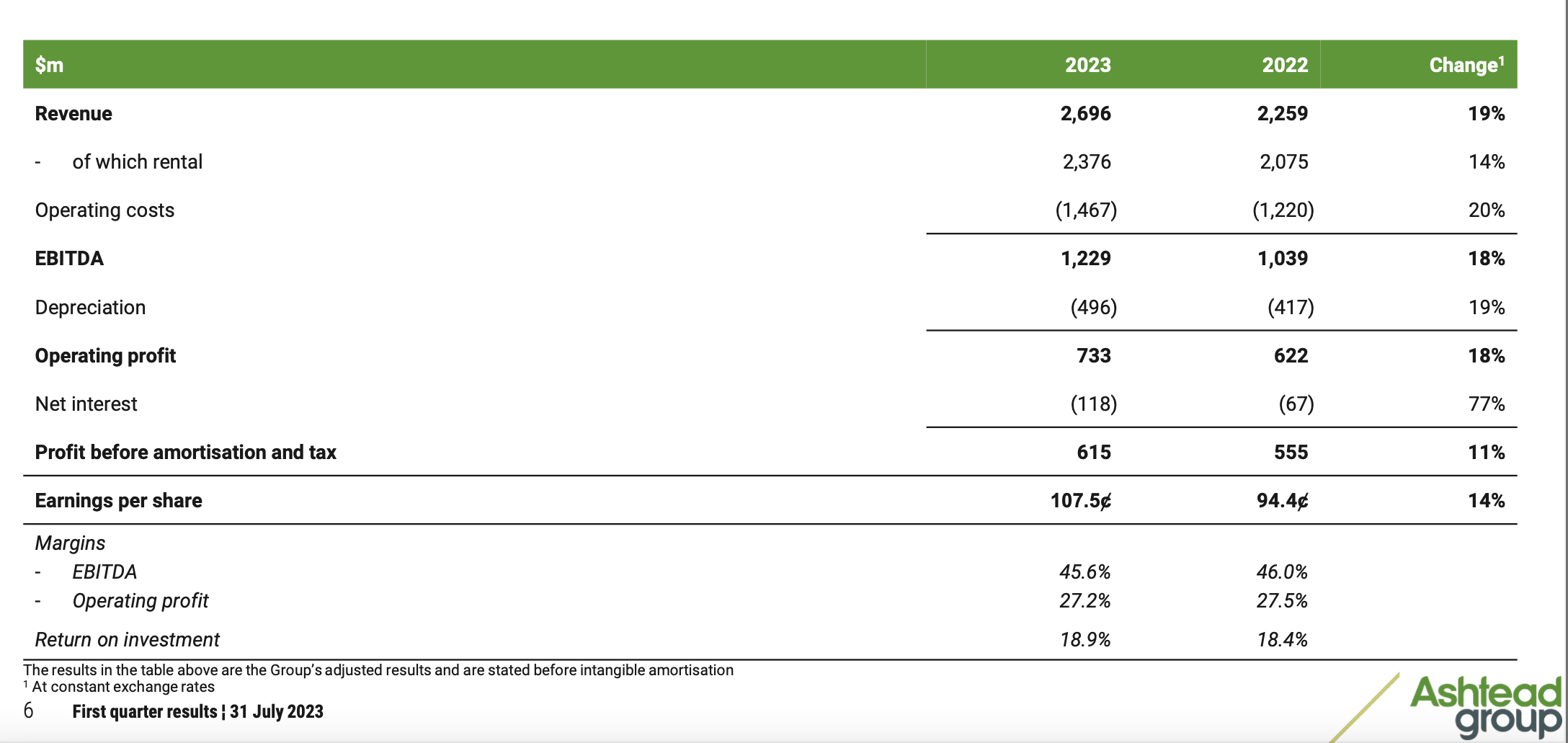

Q1 figures show continued softening

In fact, the softening has continued into Q1 FY24 as well. Ashtead reported 19% YoY revenue growth during the quarter, the same as in Q4 FY23. EPS growth has slowed down further to 14%. Even this isn't a bad result, just a relatively weaker one than what we saw last year.

There are also notable positives to it. First, despite the slowing down in EPS growth, the net margin is still at 18.8%, just slightly lower than the 19.1% seen in Q1 FY23. Similarly, the operating margin at 27.2% is also not very different from the 27.5% in Q1 FY23. It's also essentially unchanged from the full year FY23 figure.

{kind=link}

Next, its rental revenue growth at 14% is in line with the company's expectations of 13-16%. This, speaks of Ashtead's accurate assessment of the environment in which it operates and second, which in turn means that there might not be any nasty surprises ahead. And I say that, considering the weakening in the US construction market, a discussion of which is up next.

The US construction market

The company's revenues come from its three markets, the US, Canada and the UK. But, the US is really the one to focus on here, considering that it contributed to 86% of the company's revenues and 94.4% of the profits in Q1 FY24.

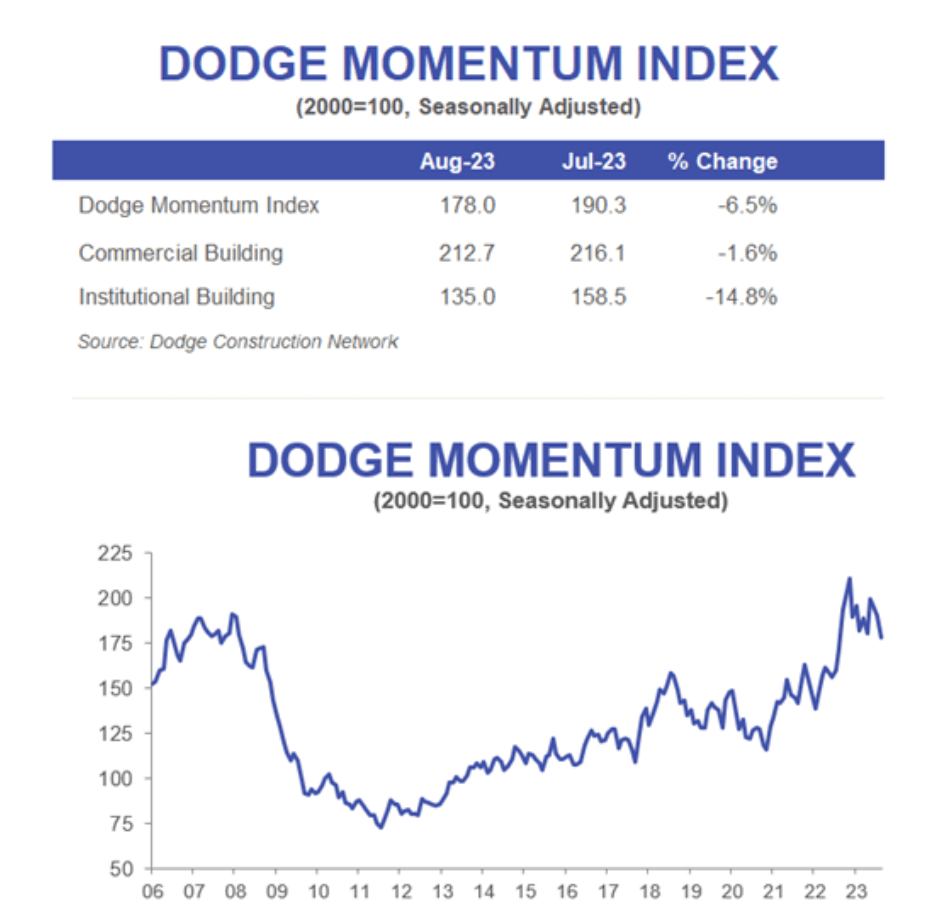

Leading indicator turns negative

The Dodge Momentum Index ((DMI)), which is a leading indicator for the US construction industry, has consistently declined month-on-month (MoM) since I last checked. It's also worth noting that the declines are getting steeper, with a 6.5% fall in August.

According to the Dodge Construction Network, which releases this monthly report, the tightening in interest rates and lending standards is the likely reason for the trend. It further expects that the remainder of the year would "continue to be constrained".

{kind=link}

Construction GDP and policy changes encouraging

That said, it is still some solace that the US construction GDP growth actually turned mildly positive. It showed 1.3% quarter-on-quarter (QoQ) growth in Q1 2023 after declining for a year and a half (see table on Page 29 of link). At this point, it's a lagging indicator but seen in conjunction with the continued robust US GDP growth in Q2 2023, there may well be a construction uptick in the quarter as well.

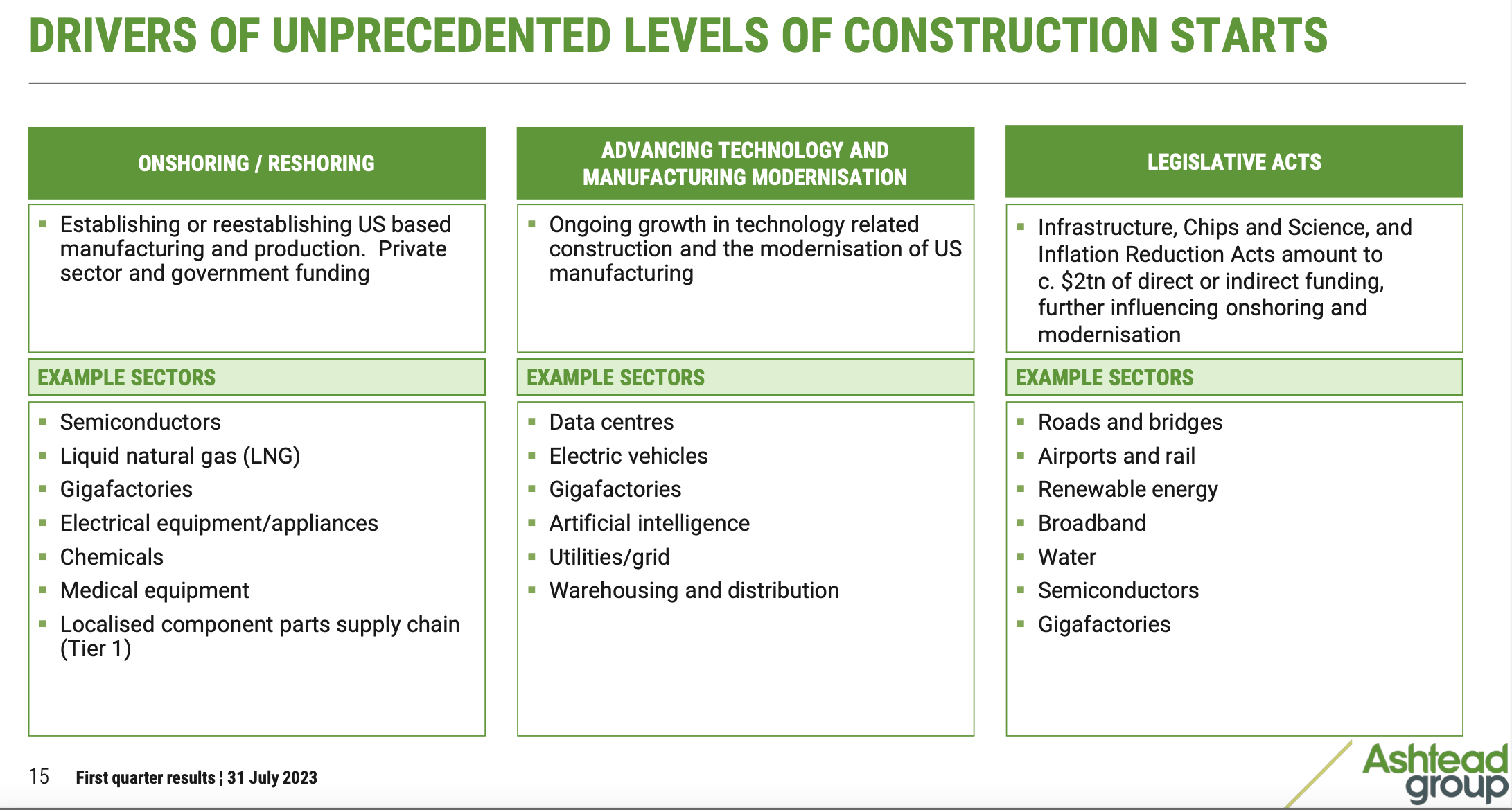

The company also points to support for construction from both private and public funding across a host of sectors, particularly as manufacturing ramps up and there's a fresh impetus from the Infrastructure, Chips and Science and the Inflation Reduction Acts (see chart below).

{kind=link}

The market multiples

ASHTF's trailing twelve months ((TTM)) GAAP price-to-earnings (P/E) ratio at 17.1x, hasn't moved much from the 17.3x it was at the last time I checked.

But there are two points to note here. It's now lower than that for the industrial sector at 19.4x and even slightly smaller than its own 10-year average of 17.7x . Further, is forward GAAP P/E ratio at 15.2x is also lower than that for the sector at 19.75x. On average, I'd expect around a 10% increase based on this.

What next?

Is this enough increase to merit a change in rating to buy? I'm not sure. Not because of anything fundamental to Ashtead, it's still a healthy company that I have no doubt can be rewarding for investors over the long term.

My only focus in a rating assessment is the price point at which to buy it. Over the next few months, there is likely to be a continued slowdown in the US construction sector, which can be exacerbated if the US economy too slows down after avoiding near-recession conditions for a while.

Further, unlike last year, when the company upgraded its forecasts after better than expected performance, its rental revenue growth has come in at the lower end of the guidance range in Q1 FY24. It's not poor growth, but it does reflect a slowing down. I reckon there may well be further weakness reflected in the company's financial performance in the next quarter. I'm maintaining a Hold rating until then, especially considering there isn't significant upside for now.

For further details see:

Ashtead: U.S. Construction Market Indicates Near-Term Uncertainty