ASOMF - ASOS And The Fast Fashion Headwinds

2023-04-28 11:08:15 ET

Summary

- ASOS is up 42% since the start of 2023 and investors appear focused on the turnaround plan of its new CEO.

- Total group revenue was down by 3% in the four months till the end of December.

- The company is guiding for fiscal 2023 cash outflow to not be greater than £100 million.

- This is set against a sales multiple that has dropped to its lowest-ever level.

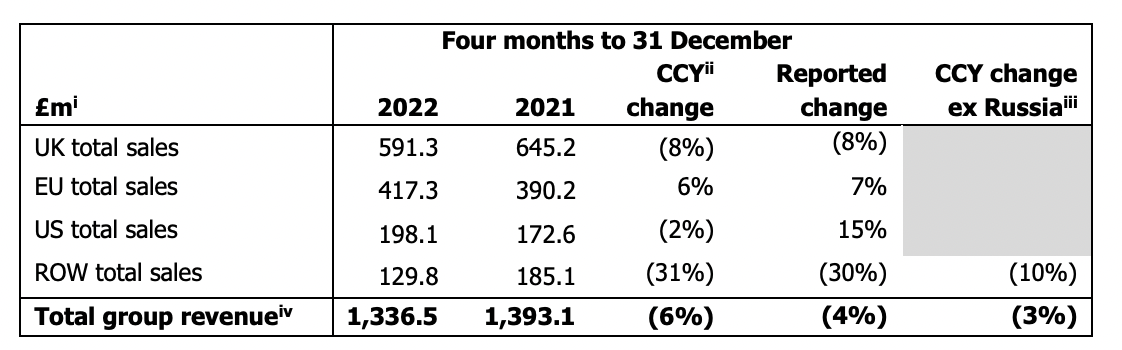

ASOS (ASOMY) (ASOMF) is blazing. The common shares of the fast fashion etailer are up 42% year-to-date, partially reversing a close to two-year decline to offer tepid hope to long-suffering bulls. Are the shares now a buy and what's driving the renewed investor enthusiasm? This is a company that moved to hire a restructuring expert in January on the back of its debt burden. This was against continued losses from operations and intense executive turnover. ASOS has replaced its chairman, CEO, COO, and CFO in recent years. However, the current market cap at £720 million perhaps represents some value against total group sales for the four months ended 31 December 2022 of £1.34 billion .

The next few months will be key as ASOS moves to execute the 12-month plan, unveiled back in October, of its new CEO José Antonio Ramos. This is centered on reducing stock, cutting spending, and raising prices to survive a broad inflation-led cost-of-living crisis that has made consumers less inclined to spend on fashion items. The fast fashion space has also become more intensely competitive with ASOS now forced to defend its market share from increasingly energetic competition from China whilst facing down higher costs from inflation and poor investor sentiment from a rising interest rate environment.

Fast Fashion Faces Hurt

Fast fashion companies are in dire straits as a pandemic-led boom in spending has fully given way to tough year-ago comps as consumer demand gets softened by still-rising interest rates. Critically, the company's sales multiple has compressed to a record low at 0.179x. To be clear here, the market is valuing each £1 of realized sales at under 20% versus a valuation multiple of over 150% two years ago at the start of 2021. Hence, ASOS would have to realize revenue that's 8.4x as high just to trade on the same market cap that it previously did.

Assuming a reversion of this multiple to 1x would see common shareholders provided with a 5.5x uplift to their position without ASOS having to realize any meaningful expansion in revenue. However, this is highly dependent on a normalization of the current macroeconomic environment, whether that's energy-led inflation falling back to 2% or recessionary jitters being replaced by economic growth. Whilst ASOS will still have to turn around its ailing operations, the current macro backdrop is entirely antithetical to the type of business ASOS is set to be for the near future.

{kind=link}

The company's last trading update, covering the four months till the end of December, saw ASOS realize a 6% revenue decline. UK sales fell by 8% over their year-ago comp to £591.3 million with the rest of the world sales falling by 31% to $129.8 million on the back of the company's exit from Russia. The EU was the only region where the company realized growth with sales increasing by 6% over its year-ago comp to £417.3 million. Total group sales excluding Russia only fell by 3% with ASOS also stating during its update that gross margins were broadly flat from 43% in the year-ago period. Active customers at 25.5 million were also flat versus its year-ago comp.

A Turnaround In 12 Months

The company is targeting £300 million in profitability measures for its current fiscal year ending in August and provided full-year guidance for cash outflow of zero to £100 million on the back of the execution of its plan. At least half of the stock identified for write-off has already been extracted from its network, office space is being rationalized, and the company is on track to remove 35 unprofitable brands from its platform. The move to stronger order economics and a lighter cost footprint has also seen the company lay off 10% of its headcount with low single-digit price increases instituted.

Cash and undrawn facilities were at £430 million as of the end of December. This provides flexibility as management tries to steer the company back to positive operating cash flows. Crucially, if the somber turnaround plan fully leads to a cash-generating operating footprint, then I believe ASOS could see its current multiple double from its current level. The present operational tumult looks like it's being addressed but there are still macro risks that abound. UK inflation has proved sticky and remains the highest in the G7 to retain pressure on margins and consumer earnings. This backdrop will make any meaningful multiple expansion harder to realize with the Bank of England now likely to keep raising rates and keep them elevated for longer. I'm not entirely enthusiastic about taking a position in the company against this. The specter of another profit warning is materially increased as long as inflation in the UK, which last came in at 10.1%, remains high. This is a hold.

For further details see:

ASOS And The Fast Fashion Headwinds