ATLKY - Atlas Copco: This Is A Good Time To Sell The Shares (Rating Downgrade)

2023-12-17 09:16:53 ET

Summary

- Atlas Copco shares have seen a rapid increase in value, outperforming the S&P 500 index.

- The company has strong financials and competitive advantages, but the share price may have outpaced improvements in fundamentals.

- Near-term headwinds, such as reduced order intake, and a high valuation are reasons to consider selling the shares.

The last time we wrote about Atlas Copco AB ( OTCPK:ATLPF )( OTCPK:ATLKF )( OTCPK:ATLKY )( OTCPK:ATLCY ) we argued shares were finally at an attractive price. This is a company with a strong competitive moat and enviable financials, and it is therefore rarely on sale. The market, however, might have now gone too far in re-rating the shares.

We believe it has gone from undervalued to overvalued pretty quickly. In roughly a year and a half, shares have delivered a total return of almost 60%, roughly triple the return obtained from the S&P 500 index ( SPY ) during the same period. We believe the share price has increased faster than the fundamentals have improved, leading us to examine whether this is a good time to sell the shares.

SeekingAlpha

Company Overview

As a reminder, the company manufactures and sells industrial equipment such as gas and air compressors, vacuum pumps, and other sophisticated equipment used by industrial clients. Some similar companies include Ingersoll Rand ( IR ) and Illinois Tool Works ( ITW ). Atlas Copco AB is based in Sweden, and it is one of their most important and well-known industrial companies.

As such, the native shares trade in the NASDAQ OMX Stockholm exchange in SEK, but they are also available in the OTC Market for US investors and there are ADRs for its two share classes. ATLKY is the ADR for Class A shares, and ATLCY for its B Class. The difference is in voting power. An A share represents one vote at the Annual General meeting, while a B share represents 1/10 of a vote.

Financials

While Atlas Copco delivered strong third quarter results, it did warn that sequentially order volumes were somewhat down. One big positive is that its services revenue continues growing, and the company was able to deliver record revenues and operating profit. The company accomplished this despite vacuum equipment being markedly down, as there continues to be significant weakness in its semiconductor end-market.

Despite weakness in some of the company's operating segments, it is currently operating with profit margins above its historical averages.

The high profit margins, returns on equity ('ROE'), and returns on invested capital ('ROIC'), clearly paint the picture of a company with strong competitive advantages. These are the result of a very strong brand, a culture of innovation, and high customer switching costs that give the company strong pricing power. Switching costs are high because customers probably don't want to modify and validate again their production processes, which could result in downtime and having to re-train employees to use new equipment.

Growth

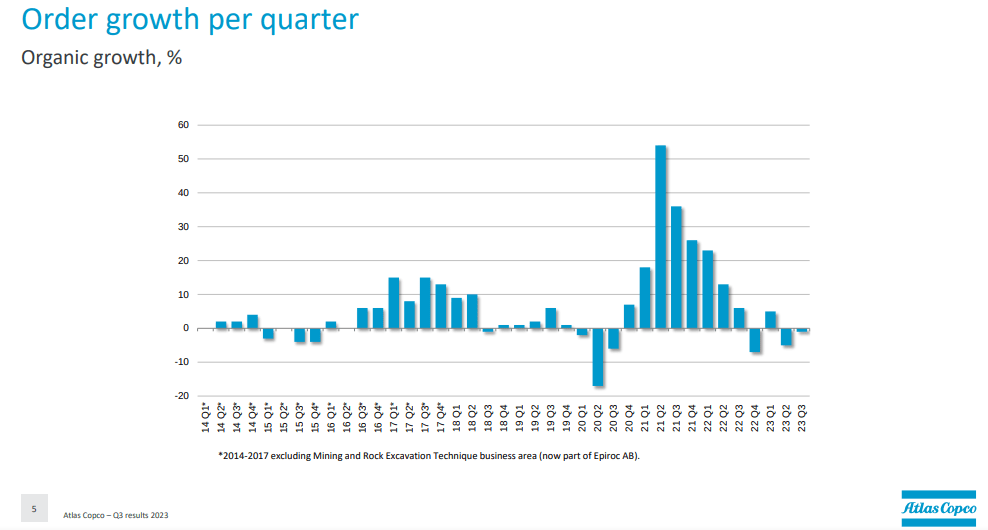

Atlas Copco's revenue has historically shown cyclicality, as two of its most important end-markets tend to be cyclical as well. These are the semiconductor and automotive markets, which have historically shown significant cyclicality.

The average quarterly year-over-year growth rate shown below probably understates the organic growth rate, as the company has sold or separated certain businesses in the past. At the same time, it has also made some acquisitions, which have contributed to inorganic growth. One significant event was the split of its mining, infrastructure and natural resources segments in 2018. The company formed Epiroc AB ( OTCPK:EPOKY ), which is now a fully independent company. These businesses were very cyclical, as they varied with commodity prices, and their separation aimed in part to reduce Atlas Copco's cyclicality.

Headwinds

While revenues are currently near a record high, it is clear that the next few quarters are going to be more difficult. Order intake has been decelerating quickly, as semiconductor and automotive customers reduce capex.

{kind=link}

Balance Sheet

Atlas Copco does carry a considerable amount of debt in its balance sheet, even if more than a third could be repaid with cash and short-term investments. Still, the net debt is very manageable for Atlas Copco, and we are not overly worried about the balance sheet strength. Leverage remains quite low, with debt to assets at less than 20% and financial debt to EBITDA at less than 1x.

Its debt is well laddered, and debt maturing before 2026 is not very significant. It is also well balanced between public debt and bank loans.

Atlas Copco AB

Outlook

What we do worry about, is the company being priced at a high multiple for what are probably cyclically high earnings. The company has already warned investors that near-term order intake is likely to suffer as a weakened economic outlook results in lower capital expenditure plans for Atlas Copco’s industrial and manufacturing customers.

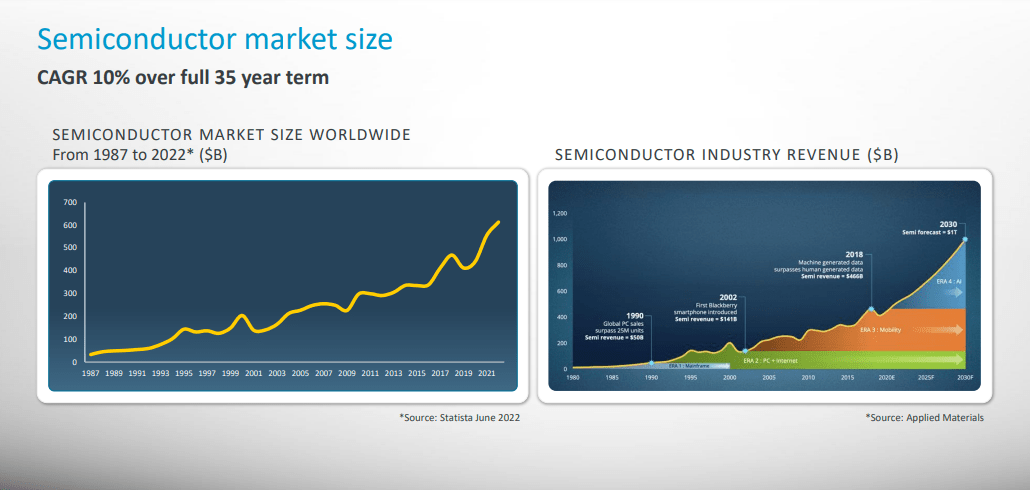

Looking further ahead, there are some reasons for optimism. Its vacuum technique sells to companies in the semiconductor industry, which is currently experiencing weakness, but has shown very strong historical growth. During its capital markets day in 2022, Atlas Copco highlighted the roughly 10% CAGR this industry has delivered, and Atlas Copco believes it can grow this segment even faster than the industry it serves as it takes market share and grows its services offering. The company has focused a lot of its innovations in making its products more energy efficient, further motivating customers to choose them over their competitors.

{kind=link}

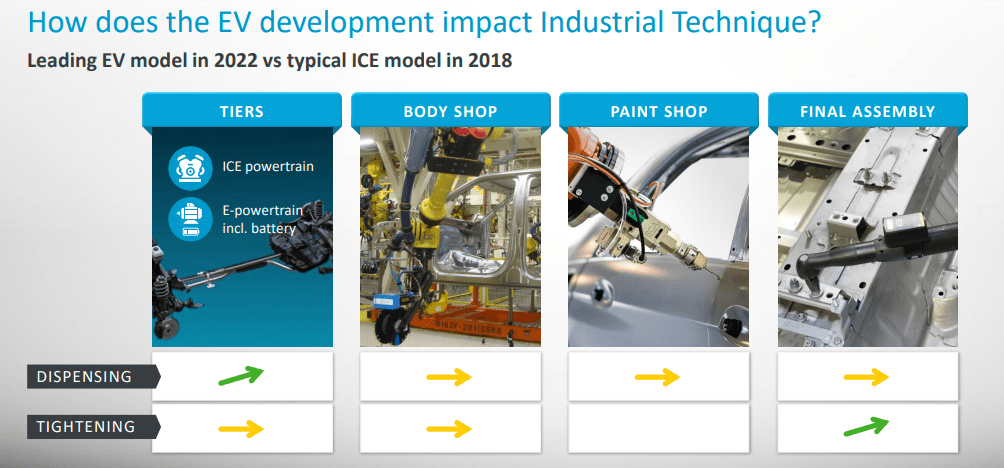

Another critical segment for the company is industrial technique, whose most important end-market is the automotive industry. We are a little bit less optimistic about this business segment, even though there are some positives to point out. For example, Atlas Copco expects some benefit from the transition to EVs, and from increased automation in manufacturing. In particular its machine vision offering looks very promising, as well as the increase in service revenues.

{kind=link}

Valuation

If the valuation was not as demanding, we would be less concerned about the risk of near-term weakness in some of its end-markets. At current prices, shares yield around 1.5%, despite the company traditionally paying about half its earnings as dividends. The EV/EBITDA ratio is a few turns above its ten-year average, and earnings are probably close to a cyclical high. Morningstar ( MORN ) recently raised their fair value estimate for the shares to 140 SEK, but this is still below current prices of 172 SEK, and Morningstar's analyst agrees that shares look pricey.

Atlas Copco is trading higher compared to similar industrial companies like Rockwell Automation ( ROK ), ABB ( OTCPK:ABBNY ), and Illinois Tool Works. They should all benefit from increased customer spending in factory automation. The only one with a higher multiple is Ingersoll Rand, which has an 'F' valuation rating from Seeking Alpha.

Risks

With its strong profitability, cash generation capacity, and solid balance sheet, we are not too worried about the company surviving an economic downturn. It has strong investment grade credit ratings from Fitch, Moody's ( MCO ), and S&P ( SPGI ).

Atlas Copco AB

The financial strength of the company is also reflected in a high Altman Z score, comfortably above the critical 3.0 threshold. Still, while we believe the company could easily survive an economic downturn, the main risk we see for investors is the high valuation that does not appear to be pricing this risk accurately.

Conclusion

Atlas Copco remains a high-quality business, the biggest change since the last time we wrote about the company has been the valuation. At current prices we believe shares to be overvalued, especially with clear signs of demand getting weaker in some of its business segments. We remain optimistic about its long-term growth potential, especially the part of the business that services semiconductor customers. Still, given the high valuation and near-term headwinds, we are double downgrading our rating to 'Sell' from 'Buy' previously.

For further details see:

Atlas Copco: This Is A Good Time To Sell The Shares (Rating Downgrade)