DJIA - August CPI: Significantly Worse Than It Appears

2023-09-13 10:45:18 ET

Summary

- Core CPI and All items were slightly above expectations, accelerating from prior month.

- Core Services Ex Housing - Fed's most closely monitored metric - experienced worrisome acceleration.

- The Fed needs to maintain hawkish tone due to accelerating core CPI and rising energy prices.

- Disinflation may cease to be a tailwind for markets going forward and could become a significant headwind.

Summary Data and Analysis

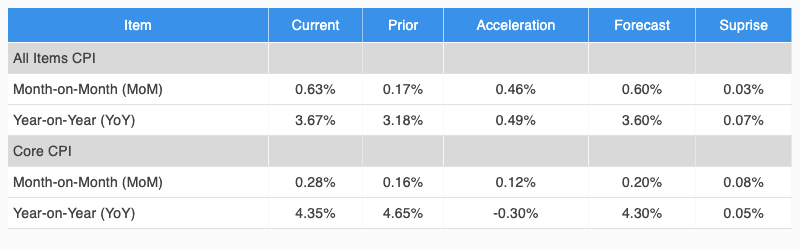

A summary of key data and analysis for this month's CPI report is provided in Figure 1.

Figure 1: Change, Acceleration, Expectations, and Surprise

{kind=link}

Core & All Items CPI (BLS, Investor Acumen)

Core CPI and All items were both slightly above expectations with both accelerating from the prior month.

Analysis of Core and Non-Core Plus Key Sub-Components

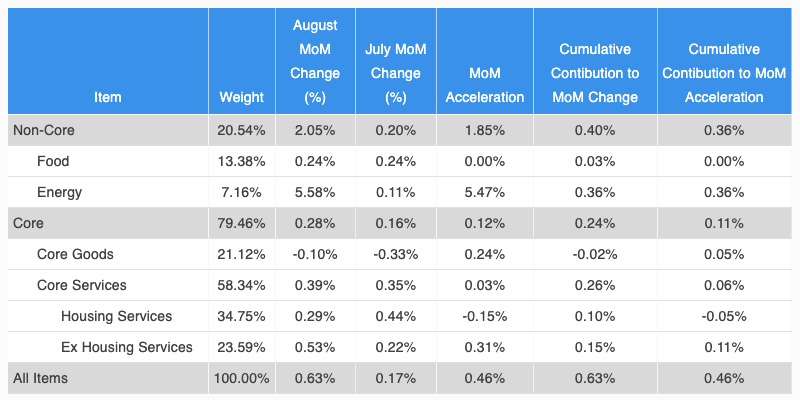

In Figure 2, we break down the analysis of change and acceleration of CPI into Non-Core and Core components. We further analyze two key subcomponents of non-core CPI and three key subcomponents of core CPI. Although all five columns in the table provide important information, we recommend that readers pay special attention to the rightmost column (Cumulative Contribution to Acceleration) as it reveals exactly what drove the MoM acceleration/deceleration in CPI during the current month compared to the prior month.

Figure 2: Analysis of Key Aggregate Components of CPI

{kind=link}

Aggregate CPI Component Analysis (BLS, Investor Acumen)

As can be seen in the table above, Core Services Ex Housing and Energy were the primary contributors to the acceleration of All Items CPI. However, the only item to decelerate was Housing Services.

Core Services except Housing - the indicator the Fed is currently paying most attention to - accelerated very significantly after several months of deceleration. This will be of concern to the Fed.

We now proceed to analyze the CPI report in greater depth. For more detailed information on how to read and interpret the tables and graphs in this article, please see the following Seeking Alpha blog post .

Contributions to Monthly Change in Core CPI

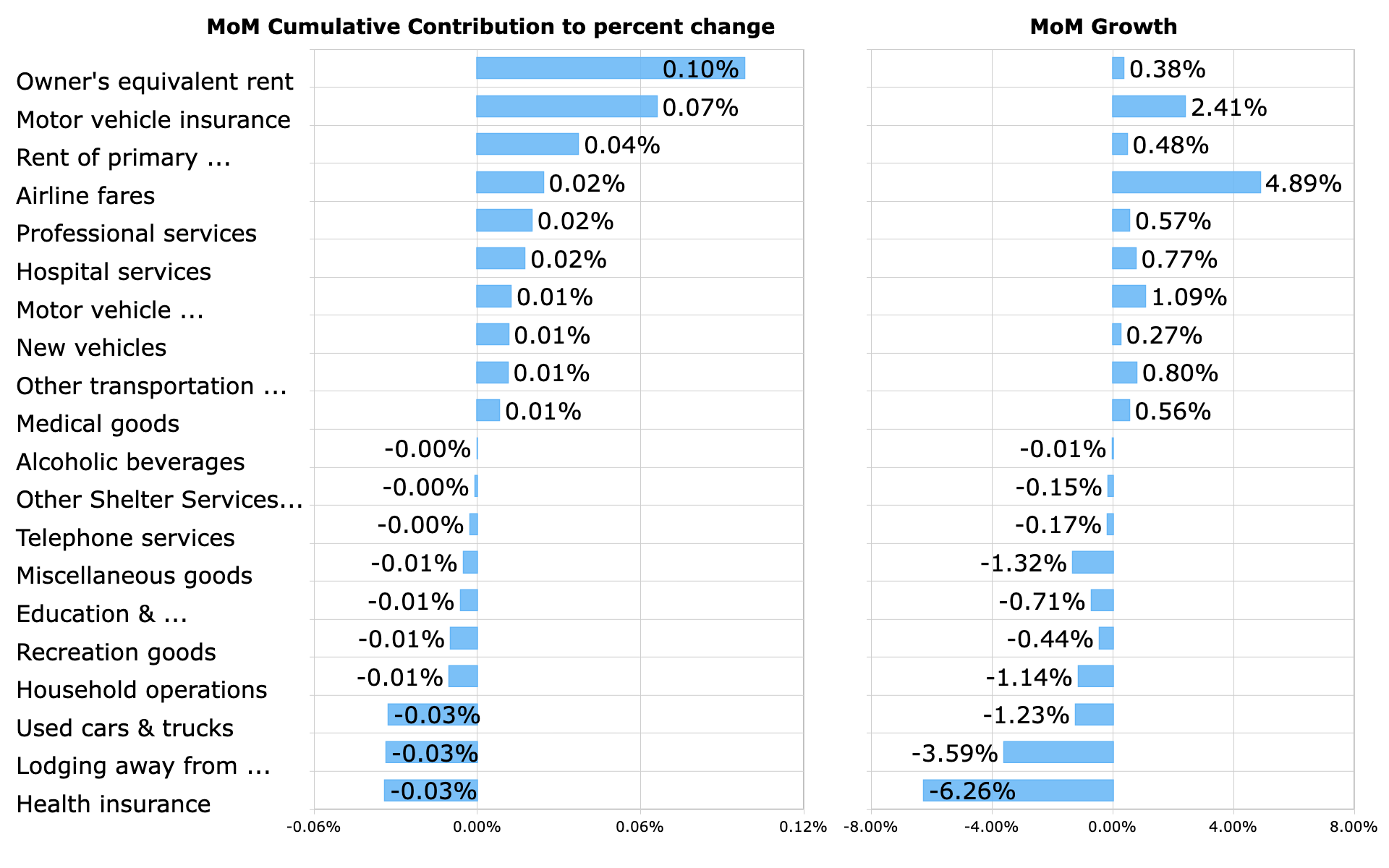

In Figure 3, we provide a bar chart that highlights the major positive and negative contributors to the MoM percent change in Core CPI. These contributions take into account both the magnitude of the MoM change in each component as well as the weight of each component in CPI.

Figure 3: Top Contributors to MoM Percent Change

{kind=link}

Top CPI Contributors (BLS, Investor Acumen)

Once again, Owner's Equivalent Rent was the most important positive contributor to the monthly change in CPI. And again, Used Cars & Trucks -- a highly volatile item - contributed negatively to the monthly change in CPI. Real-time indicators suggest that the deflationary trend in the used car market may at least pause in the next few months, which would eliminate this particular drag on core CPI.

Housing components have the largest weight in the CPI (accounting for about 40% of core CPI) and it's important to note that real-time indicators suggest that there will continue to be significant disinflation in the housing components of CPI for the remainder of 2023.

Contributions to Monthly Acceleration in Core CPI

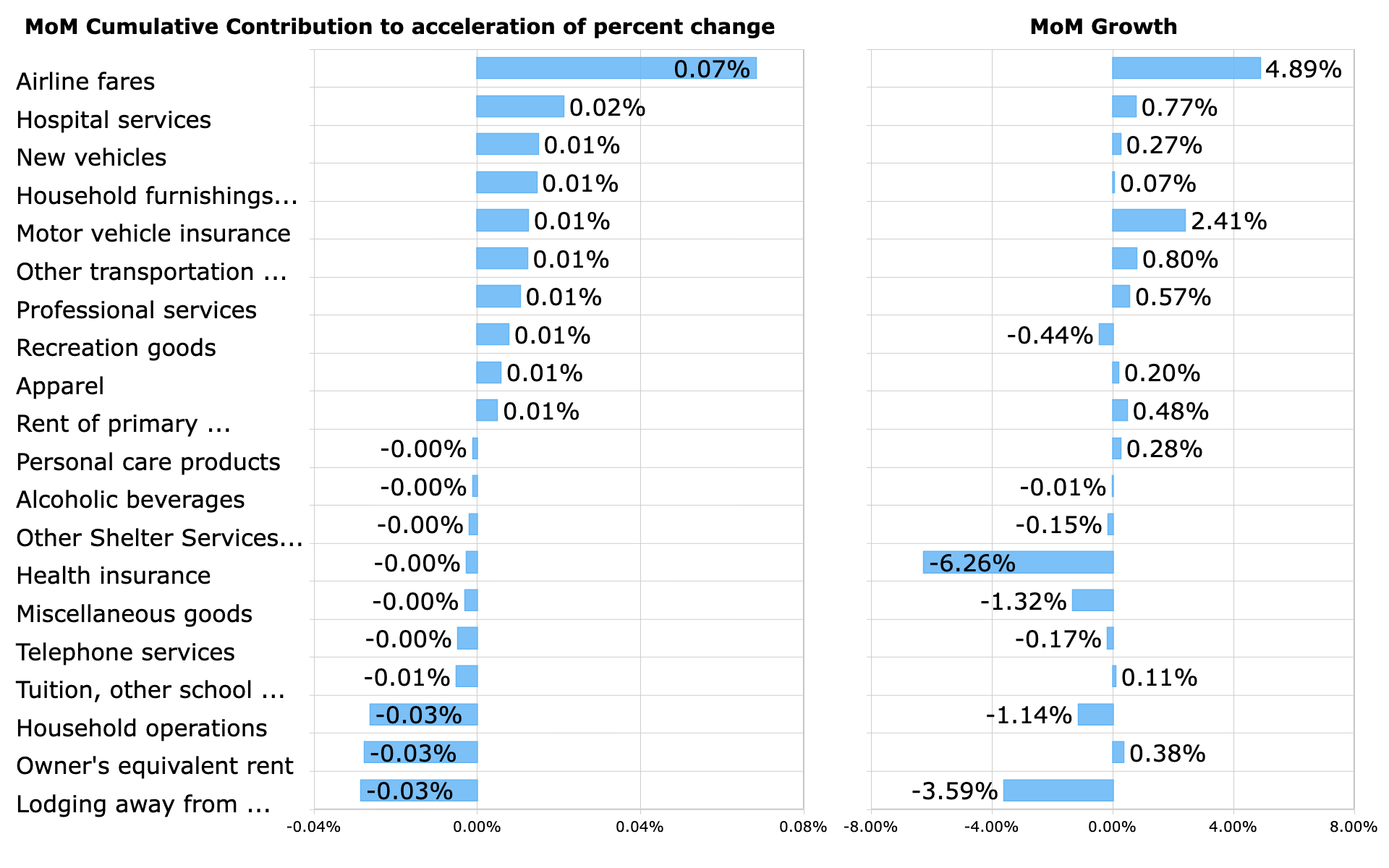

In Figure 4, we provide a bar chart that highlights the major positive and negative contributors to the MoM acceleration in Core CPI. These contributions take into account both the magnitude of the MoM accelerations in the components as well as the weight of each component in CPI.

Figure 4: Top Contributors to MoM Acceleration

{kind=link}

Top CPI Acceleration Contributors (BLS, Investor Acumen)

It's worthwhile to examine this table carefully as it's likely to include most or all of the items that caused deviations from forecasters' expectations of Core CPI.

Airline fares, a volatile component, rebounded from the previous month's deflation. Rising energy price could continue to push airline fares up.

On the side of deceleration, Household operations and Lodging Away from home - both volatile items - both contributed to deceleration of CPI this month.

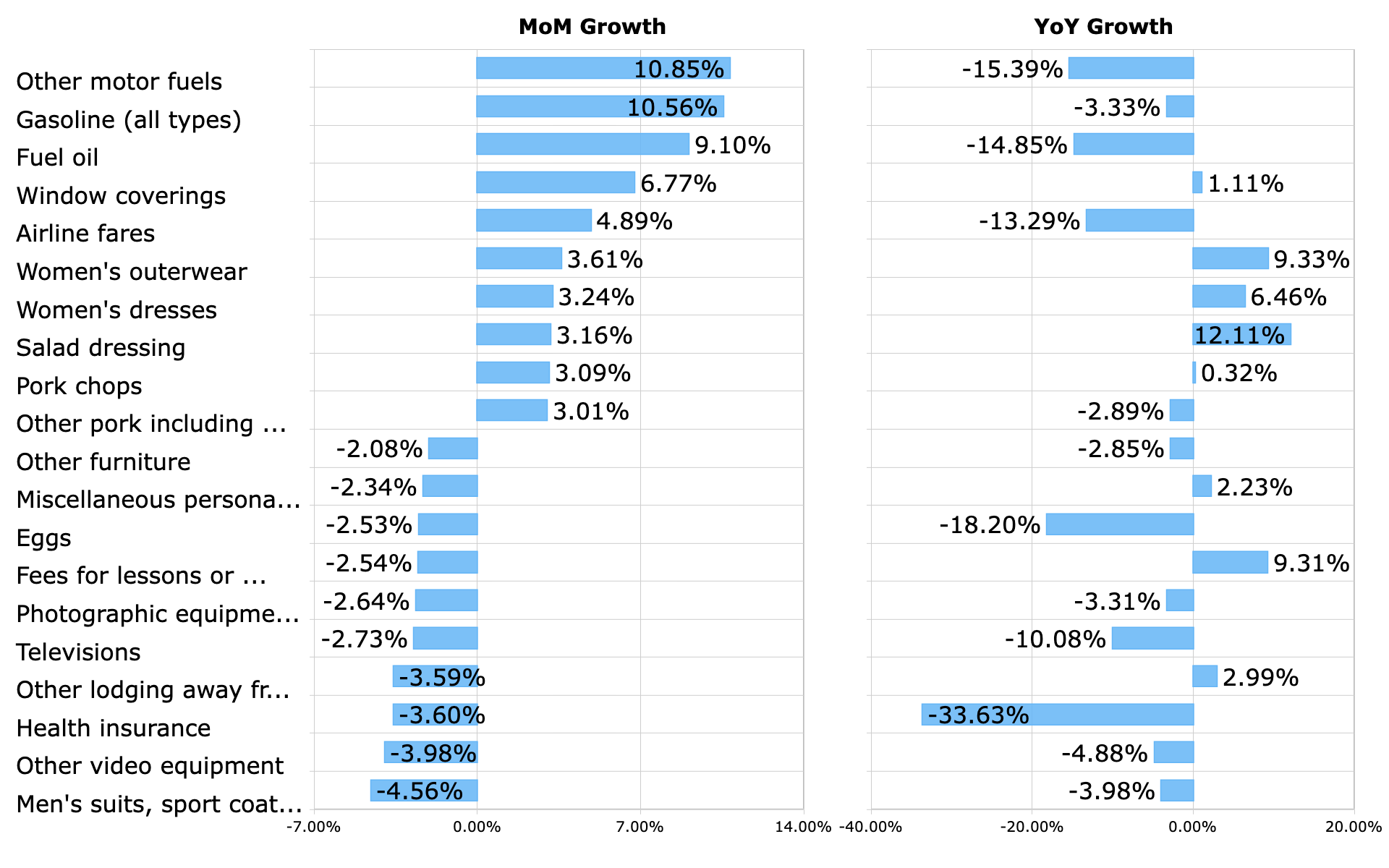

Top Movers

For general interest purposes, in Figure 5 we highlight the CPI components (most granular level) that exhibited the largest positive and negative change during the month. The YoY change in these particular components is displayed to the right.

Figure 5: Top Movers MoM Percent Change

{kind=link}

Top CPI Movers (BLS, Investor Acumen)

Rising gasoline prices, motor fuel and airline fares showed notable rises in the August report. Health insurance also had a notable fall this month.

Implications for the Economy

The two most important details in this report were the following: First, Core Services, ex Housing - the indicator that the Fed is currently watching most closely - experienced a very significant acceleration. Second, if you exclude the effects for certain highly volatile items such as lodging away from home, health insurance, used cars and household operations, the core CPI was significantly worse than it appears at first glance. Without these volatile items, core CPI would have been over 0.4% for the month rather than 0.3% - and well above the 0.1% to 0.2% range that the Fed would like to see.

As a result, it is my view that the Fed will need to maintain a hawkish tone in its communications. Core CPI is still too high and might be accelerating.

Furthermore, the Fed needs to be concerned about rising energy prices. The last time there was a major spike in oil prices, it triggered a major wave of inflation throughout the economy.

Overall, the Fed is going to have to remain very cautious, keeping pressure on interest rates and liquidity in the economy.

Implications for Financial Markets

As of the writing of this report, markets do not seem to have quite processed the negative internals in this report as detailed above. However, over the course of the next month or so, the implications are negative as the Fed will be forced to maintain tight monetary policy and hawkish rhetoric despite the fact that the economy seems to be poised for a significant - and potentially dangerous - deceleration.

Conclusion

This CPI report was significantly worse than it appeared. Since last year, I have been telling investors that 2023 would be a year of disinflation - and has been. But we are currently at an inflection point where the disinflationary process has at least "paused" and there is risk of a re-acceleration of inflation. If such a re-acceleration occurs - particularly in the context of a slowing economy, the implications for equity markets would be very negative.

Our portfolios will be looking to capitalize on possibilities of market downside in coming months.

For further details see:

August CPI: Significantly Worse Than It Appears