AUPH - Aurinia Rides High On Lupkynis But Not Without Cost (Rating Upgrade)

2023-09-27 01:48:57 ET

Summary

- Aurinia Pharmaceuticals reports Q2 2023 revenue of $41.5M, up 47% YoY, driven by Lupkynis sales; however, SG&A expenses still exceed revenue.

- Strong liquidity with $415.9M current assets, but insider selling and 9.93% short interest raise investor caution.

- Investment Recommendation: Upgraded from "Sell" to "Hold" due to improved financials but capped growth potential; watch R&D vs SG&A expenses.

At a Glance

In light of Aurinia Pharmaceuticals' ( AUPH ) Q2 2023 performance and strategic initiatives, I'm revising my previous "Sell" recommendation to a more nuanced "Hold." Revenue growth at 47% YoY and a narrowed net loss illustrate strong market adoption of Lupkynis and improved operational efficiency. However, SG&A expenses continue to overshadow revenue, limiting the financial upside. Although the company is well-capitalized with a lengthy cash runway, a notable insider selling trend and substantial short interest cast shadows on investor sentiment. While partnerships with Otsuka and global expansion efforts bode well for future revenue streams, financial and operational constraints make it prudent to remain on the sidelines for now.

Earnings Report

To begin my analysis, looking at Aurinia Pharmaceuticals' most recent earnings report , the company reported Q2 2023 total net revenue of $41.5M, a significant 47% increase from $28.2M in Q2 2022, predominantly driven by product revenue. Operating expenses, however, remain a concern: SG&A was $47.1M, down from $51.5M YoY but still eclipsing revenue. R&D expenses increased to $12.6M from $11.5M, likely supporting the company’s clinical pipeline. The net loss stood at $11.5M, a marked improvement from a $35.5M loss in the same quarter last year. These figures suggest a growing market acceptance of Lupkynis and optimized operational management but warrant close monitoring of the SG&A outlay in relation to revenue.

Financial Health & Liquidity

Turning to Aurinia Pharmaceuticals' balance sheet , the company reported total current assets of $415.9M as of June 30, 2023. Key liquidity components include cash and cash equivalents at $81.7M and short-term investments at $269M. The monthly cash burn, derived from "Net cash used in operating activities" for the past six months, is about $5.75M. With this burn rate, the company has an estimated cash runway of approximately 72 months, or 6 years, based on its current liquid assets. Note that these values and estimates are based on historical data and may not necessarily predict future performance.

In terms of liquidity status, Aurinia appears to be well-capitalized to meet its operational and strategic objectives for the foreseeable future. The company has no significant debt obligations, with total liabilities standing at $156.6M, a manageable figure considering its asset base. Given the positive liquidity ratios and a strong cash runway, Aurinia is in a good position to secure additional financing if needed, although the necessity for such a move appears low at the current stage. These are my personal observations, and other analysts might interpret the data differently.

Capital, Growth, Momentum, & Ownership

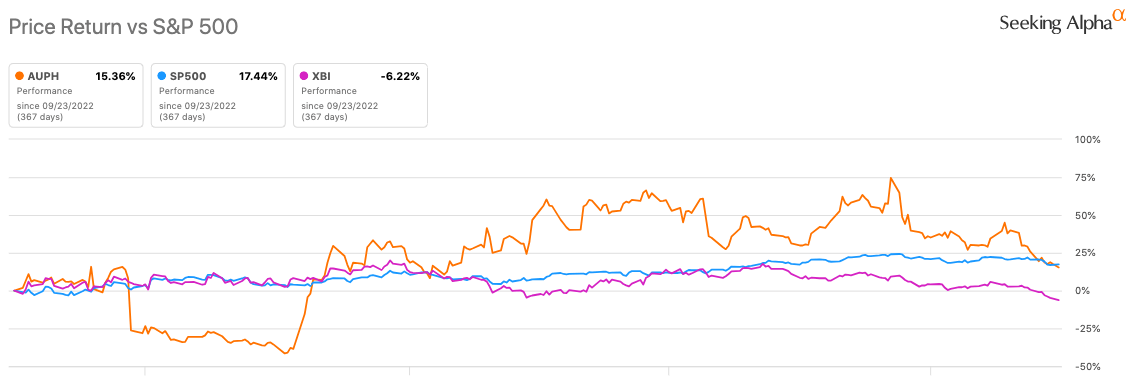

According to Seeking Alpha data, Aurinia Pharmaceuticals demonstrates a stable capital structure, with low debt relative to its market cap, providing a secure liquidity runway. Analysts project YoY revenue growth from $161.65M in 2023 to $287.03M by 2025, affirming solid growth prospects. Stock momentum reveals a mixed bag, underperforming SPY in the 3M and 6M timeframe but outperforming on a 9M basis.

{kind=link}

Ownership is diversified, with 41.42% held by institutions, hinting at some level of market confidence. Insider trading shows a recent trend of share- selling by directors, though not in large quantities. A significant short interest of 9.93% with 6.39 days to cover could signal market skepticism but also offers potential for a short squeeze.

Lupkynis Strategies Bolster LN Market Presence

Management's recent commentary during the earnings call indicates a multi-pronged strategy for Lupkynis that complements the encouraging operational metrics. The key pillars—patient awareness, clinical differentiation, and accessibility—are echoed in the market performance data.

-

Patient Awareness and Activation: The 'Get Uncomfortable' campaign with Toni Braxton has notably scaled awareness, evident from 750 million impressions and robust website traffic. This dovetails with the YoY 50% increase in patients on Lupkynis therapy. For an LN drug, patient awareness isn't just a marketing checkbox; it's a lever for patient-led healthcare, especially given LN's often asymptomatic nature.

-

Clinical Differentiation: New data from the AURORA and AURORA 2 trials adds a clinical edge. Lupkynis shows histologic activity improvement with stable chronicity scores and is differentiated further in three-year eGFR efficacy and long-term safety. These developments likely contribute to the high conversion rates (89%) and intent-to-prescribe metrics. Clinically, the drug is not just meeting guidelines but exceeding them in certain areas, making it appealing to top-decile prescribers.

-

Accessibility and Adherence: Management highlighted a 65% rate of therapy initiation within 20 days and 54% 12-month persistency. This aligns with their focus on patient accessibility, further supported by an 80-85% adherence rate. This is a crucial underpinning for a chronic disease medication, where persistency is as important as initial uptake.

-

Global Reach: Expansion into Europe and prospective entry into Japan via partnerships like that with Otsuka add layers of revenue potential. This speaks to a globalization strategy that is timely and well-executed.

-

Revenue Projections: Uplifting the net product revenue guidance range to $150-160 million for 2023 validates the drug's market trajectory and reflects positively on all aspects of operations.

-

Summer Seasonality: Management’s candid acknowledgment of a “summer effect” affecting LN care suggests a nuanced understanding of market dynamics, which could be further investigated as a factor for any slow-downs in PSF growth.

-

Future R&D: Mention of the IND for AUR200 and pediatric study commitments shows an expansive view beyond Lupkynis, illustrating a pipeline strategy that aims to broaden Aurinia's therapeutic impact.

In summary, the management's strategies align with and likely contribute to the solid KPIs observed. The integration of clinical data with aggressive awareness campaigns and a transparent, hands-on approach to market dynamics is yielding positive traction. The persistent improvement in key operational metrics confirms this, positioning Lupkynis as a formidable player in the LN landscape.

My Analysis & Recommendation

In light of Aurinia Pharmaceuticals' Q2 performance and market activities, investors may have grounds for cautious optimism. The company's tactical emphasis on patient awareness, clinical differentiation, and accessibility is reaping quantifiable dividends, as seen in the YoY 50% increase in patients on Lupkynis therapy. The strategic collaboration with Otsuka Pharmaceutical and the prospective expansion into Europe and Japan augur well for geographic revenue diversification.

While the 47% increase in revenue YoY is impressive, it's essential to closely monitor the SG&A expenses, which, despite a decline, continue to outpace revenue. This could present a long-term financial constraint that could cap growth. Similarly, insiders have been selling shares, albeit in limited quantities, which could point to a cautious internal sentiment.

At a market cap nearing $1 billion and a substantial revenue guidance uplift to $150-160 million for 2023, the stock appears reasonably priced. Yet, given the limitations on the upside—potentially from operating expenses and the concentrated reliance on Lupkynis—I suspect the room for exponential growth is limited in the short to medium term. The company's strong liquidity position and positive cash runway mitigate downside risks but don't necessarily signal an upside breakout, especially when considering the substantial short interest of 9.93%.

Therefore, I'm upgrading my investment recommendation on Aurinia Pharmaceuticals from "Sell" to "Hold." With improved financial metrics but a capped upside, the stock is no longer a strong sell, but neither is it compelling enough for a buy recommendation at this juncture. Investors should maintain a close eye on R&D productivity vis-à-vis SG&A expenses and observe if management can parlay the positive momentum of Lupkynis into its upcoming assets, AUR200 and AUR300, slated for FDA submissions in 2023 and 2024 respectively.

For further details see:

Aurinia Rides High On Lupkynis, But Not Without Cost (Rating Upgrade)