AVACF - Avance Gas: Strong Results Are Continuing Longer Than I Had Anticipated

2023-06-21 11:27:00 ET

Summary

- Avance Gas owns a relatively modern fleet of VLGC carriers.

- The charter rates remained very strong in the first quarter, and although Q2 will be weaker, the company will still print cash.

- Expect the dividends to decrease, but Avance Gas likely will still have very generous dividends.

Introduction

Avance Gas ( OTCPK:AVACF ) has continued to positively surprise me. In a previous article I was very impressed with the company’s dividend yield of almost 20% in 2022 and I argued the exceptionally strong performance may not be repeated this year as about four dozen new VLGC carriers will hit the waters this year. I did mention Q1 would likely still be strong, but given the recent and current charter rates but it's now starting to look even the second quarter and perhaps the third quarter may be stronger than I had anticipated.

{kind=link}

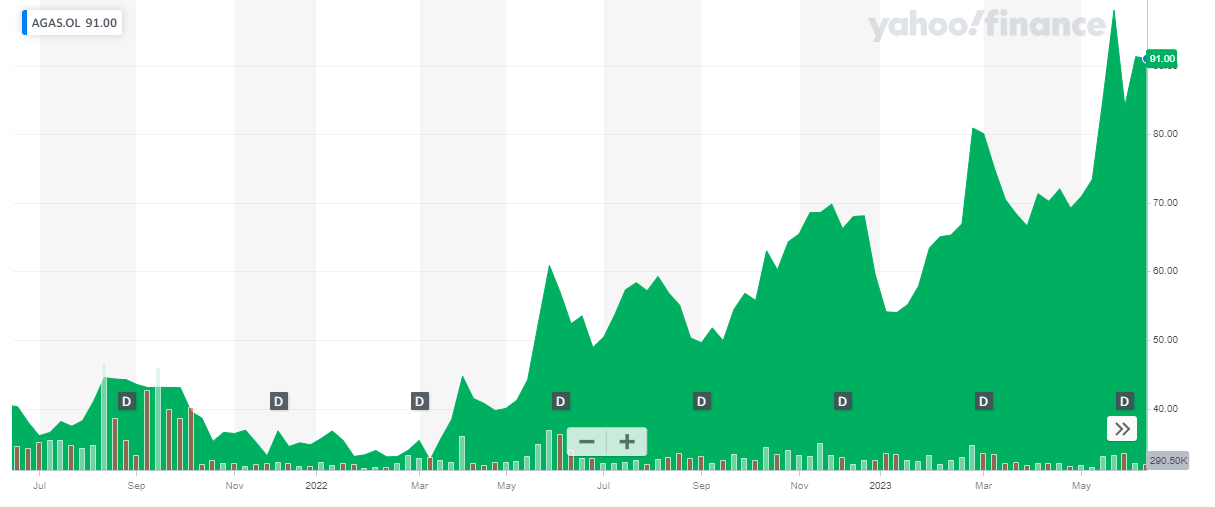

Avance Gas has a primary listing in Norway where it's trading with AGAS as its ticker symbol. The average daily volume in Oslo is approximately 100,000 shares per day . At the current USD/NOK exchange rate of 10.7 , the shares of Avance Gas are trading at approximately $8.50 per share. I will use the US dollar as base currency throughout this article as that’s the currency Avance Gas is reporting its financial results in.

The cash flow is still pouring in

As this article is meant as an update to previous coverage on Avance Gas, I’d like to refer you to those earlier articles to get a better understanding and idea of how the company operates. The business model is very straight forward: Avance Gas owns VLGCs (Very Large Gas Carriers) which it charters out to third parties for the transportation of LPG products.

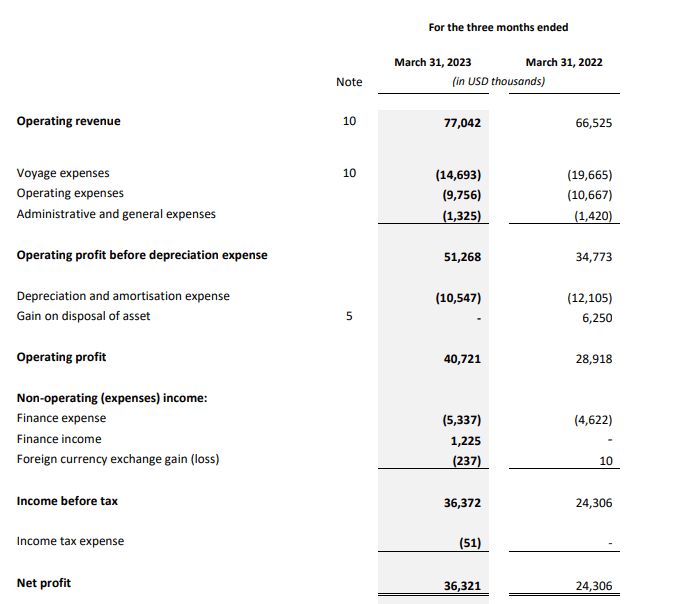

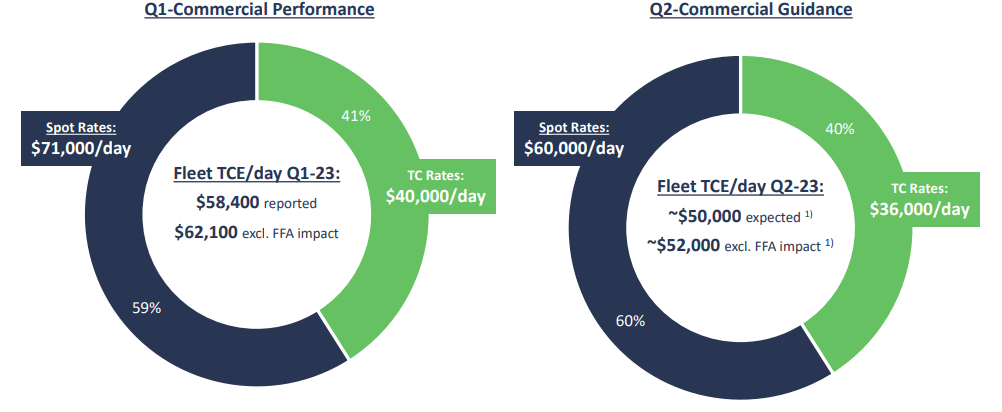

In the first quarter of 2023, the actual performance has beat the guidance as the company reported a total time charter equivalent rate of almost $58,400/day , which was slightly above the previously issued guidance of $58,000 per day. This excellent average was generated through the combination of longer-term charters (at an average of $40,000/day) and the exposure to spot markets at in excess of $70,000/day.

{kind=link}

This resulted in a total revenue of just over $77M, as you can see below. The total operating expenses were pretty low, and this helped boost the EBITDA to $51.3M, an increase of almost 50% compared to the first quarter of last year.

That's impressive, not in the least because Avance Gas was able to combine a higher revenue with a lower operating cost (likely due to the lower oil price and lower bunker fuel prices). The total operating profit was a very strong $40.7M, and as the interest expenses remained relatively stable, the pre-tax income and after-tax income came in at approximately $36.3M, or $0.47 per share.

{kind=link}

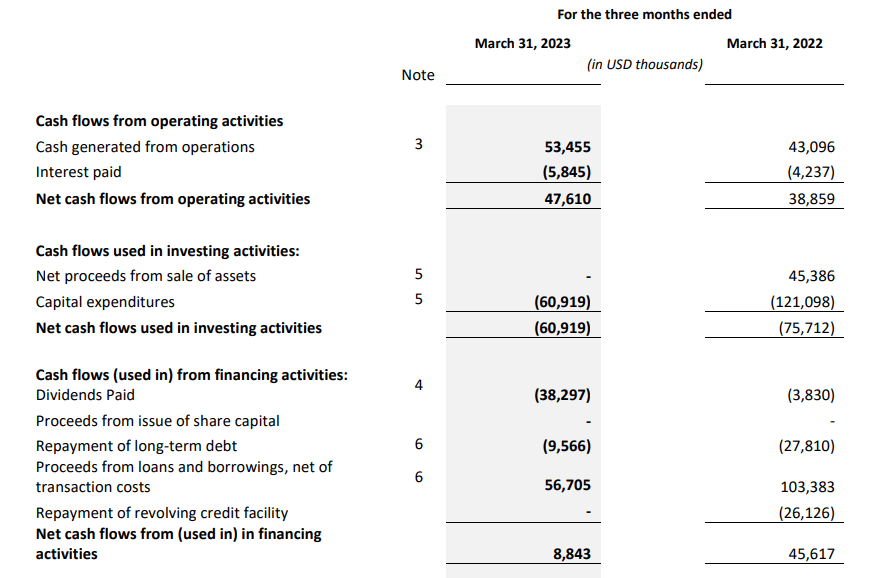

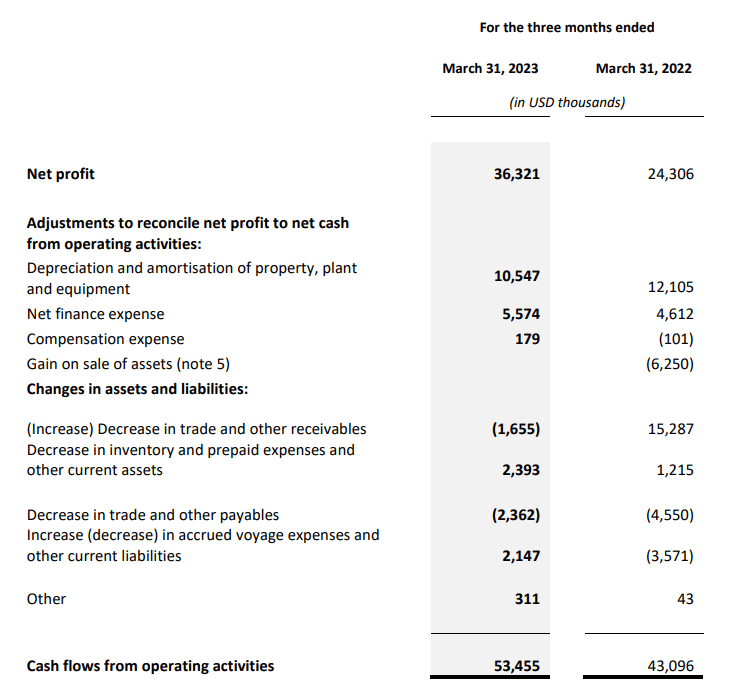

The cash flow result also was very strong. The reported operating cash flow was approximately $47.6M (shown above), but as you can see below, this actually includes a $0.5M contribution from changes in the working capital position. This means that on an adjusted basis, the operating cash flow was approximately $47M.

{kind=link}

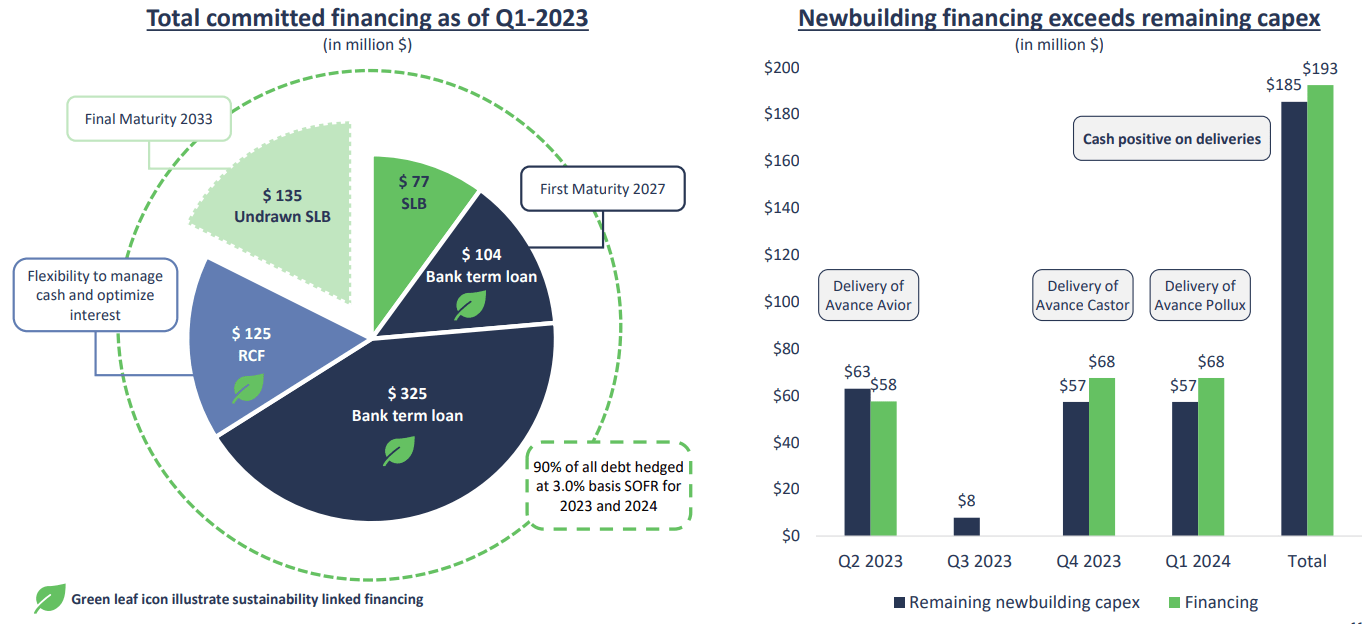

The total capex was $61M as Avance Gas continues to invest pretty heavily in newbuilds. This means the company was free cash flow negative and it also means dividends weren’t covered by the free cash flow result. But keep in mind these capital expenditures are mainly up-front sunk costs. Also keep in mind the new vessels will rejuvenate the fleet while the company remains fully funded for the fleet expansion program.

Avance Gas confirmed once again its newbuild expansion program is still fully funded and its exiting access to financing sources actually exceeds the remaining capex for the newbuilds. Sure, this will temporarily increase the net debt levels, but it also means Avance Gas isn’t left behind as other competitors are investing in new vessels.

{kind=link}

Subsequent to the end of the first quarter, Avance Gas announced it had signed an agreement to acquired two mid-sized LPG and ammonia carriers which will be delivered in Q4 2025 and Q1 2026 (shipyards are still pretty full these days). The total investment is approximately $123M for both vessels and Avance Gas secured the right to order two more vessels at the exact same terms.

As of the end of Q1, Avance Gas had about $220M in cash and a total debt of just under $500M. As the EBITDA and cash flows will remain strong, I’m not too worried about the debt level although I would probably prefer lower dividends in favor of a higher percentage of self-funding the fleet expansion and rejuvenation program.

And while the second quarter will likely exceed my expectations, it won’t be as strong as the first quarter. According to the updated guidance provided by the Avance Gas management, the anticipated average TCE rate is approximately $50,000/day. While that's still very healthy and while Avance Gas will still generate very healthy cash flows, the charter rate is about 15% lower than in the first quarter and this will likely reduce the EBITDA by approximately $10M per quarter.

{kind=link}

Investment thesis

This means my original thesis I published in April is still valid. Avance Gas has indeed published truly excellent Q1 results, but we already see a deterioration in the second quarter. This doesn’t mean Q2 will be "bad," it simply won’t be as strong as the first quarter and shareholders should prepare themselves for lower dividends (and that really shouldn’t come as a surprise).

I have to tip my hat to the Avance Gas management team as it has done a superb job in maximizing the incoming cash flows while continuing to invest in the rejuvenation of its LPG fleet. The two oldest vessels will be 15-years-old this year and perhaps Avance Gas will try to sell them and recycle the cash to fund the two (or four) newbuilds that will be delivered in 2025/2026. The smart capital allocation policy is still appealing, but I currently have no position anymore. I would be interested in going long again but I’m in no rush.

For further details see:

Avance Gas: Strong Results Are Continuing Longer Than I Had Anticipated