HYG - AVK: Income Rising But Leverage Remains Elevated

2023-08-30 12:52:39 ET

Summary

- Advent Convertible & Income Fund has seen an increase in income generation but also elevated leverage, making it a riskier fund.

- The fund's distribution rate is high, hindering appreciation on the NAV level, which causes the leverage ratio to remain elevated, too.

- AVK's portfolio consists primarily of exposure to convertibles and high-yield securities, but it also has a relatively smaller weighting to the tech sector.

Written by Nick Ackerman, co-produced by Stanford Chemist.

Earlier this year, we took a look at the Advent Convertible & Income Fund ( AVK ), and since then, we have a new semi-annual report showing us that the income generation of the underlying portfolio is on the rise. Unfortunately, without some significant appreciation in the underlying fund, we also see that the leverage is elevated, and that makes this a riskier fund.

The high distribution rate has also been keeping the fund from achieving some appreciation on the NAV level. While the total NAV returns are fairly attractive this year, it has mostly come from the distribution the fund has paid out. Therefore, the assets aren't rising in the fund, which would reduce the fund's leverage ratio. However, the discount has also widened a touch during this time, which can compensate for some of the higher risk.

The Basics

- 1-Year Z-score: -0.88

- Discount: -8.55%

- Distribution Yield: 12.65%

- Expense Ratio: 1.79%

- Leverage: 45.42%

- Managed Assets: $768.28 million

- Structure: Perpetual

AVK's investment objective is "to provide total return, through a combination of capital appreciation and current income." They will attempt to achieve this by "investing at least 80% of its managed assets in a diversified portfolio of convertible securities and non-convertible income securities." They will also invest "at least 30% of its managed assets in convertible securities and up to 70% of its managed assets in lower-grade, non-convertible income securities, although the portion of the Fund's assets invested in convertible securities and non-convertible income securities will vary from time to time."

Besides the borrowing costs rising materially in the latest report , the fund's expense ratio also rose. It went from 1.56% to 1.79%. When including the borrowing costs, the fund's total expense ratio went from 3.54% at the end of fiscal 2022 to 5.36%.

The fund has total borrowings on its credit facility of $173 million. The good news is that some of this is actually based on fixed rates; the bad news is that the majority of it is based on SOFR+1.25%. A 1.25% spread on top of SOFR is actually quite high from what I'm used to seeing in the CEF space. This is generally under 1%. As of today , that would mean that the borrowing costs on the majority of this leverage are at 6.55%.

{kind=link}

The fund also incorporates reverse repurchase agreements. The rate for this leverage is mostly the same as it is for the fund's credit facility, meaning that it is now at a higher rate as well since this last report.

{kind=link}

Besides the rising borrowing costs, the fact that the fund's leverage ratio is running at just over 45% also needs to be considered before investing. There is a good chance that if we see any sort of market correction, AVK could be in a position where they get a margin call to deleverage their portfolio.

Performance - Discount Needs To Widen Further To Be More Attractive

The performance of the fund since our update has provided a fairly attractive total return for being a convertible and fixed-income fund. It hasn't matched the S&P 500, but that's all equity with a heavy emphasis on the magnificent 7.

AVK Performance Since Prior Update (Seeking Alpha)

Given that the portfolio is roughly 46% convertibles and 38% high yield, seeing how the fund has performed against iShares Convertible Bond ETF ( ICVT ) and iShares iBoxx $ High Yield Corporate Bond ETF ( HYG ) might be a more appropriate benchmark. In that case, we see mostly, as we would expect, the fund comes somewhere in the middle of these two.

That being said, given the higher weighting to convertible securities, it could also be considered a laggard too. Given the leverage, it's likely a fairly disappointing longer-term result overall on a total NAV return basis. ICVT's inception date is June 2, 2015, which is where this comparison starts.

Ycharts

Despite bonds being the smaller sleeve of the fund's main two focuses, they provide returns against the Bloomberg U.S. Aggregate Bond Index in their reporting material. Interestingly, this is also an index that is made up of investment-grade bonds and not the high-yield bonds that the fund is most heavily invested in.

{kind=link}

So the above comparison, despite AVK showing an outperformance in the longer term periods, doesn't seem to be a really great representation. Instead, I believe they should focus on incorporating a convertible and high-yield blended benchmark to more appropriately show a comparison for the fund. This isn't even to mention that they also have some international exposure in the fund that isn't going to be represented in the above return comparison either.

Given the current discount, it could indicate that the fund still has some further discount widening to go until it goes below the longer-term average. However, the discount also represents a sharp decline from the premiums that it was trading at heading through 2021 and into 2022.

Ycharts

Looking at the shorter term, we see an average discount of -6.27% over the last year. That's partially thanks to trading right near parity with its NAV heading into this period - then, in February and March of 2023, it traded much closer to its NAV per share.

Still, given the current environment of higher interest rates that AVK has to face on a portion of its leverage and the elevated leverage, a wider discount might seems appropriate over the longer term. A discount of 10%+ would provide a more comfortable entry for a margin of safety that is more adequate for this current environment.

Distribution - Rising Income

The good news besides all of what we mostly touched on as being negatives for the fund is that as yields have risen, so has the income generation in their underlying portfolio.

{kind=link}

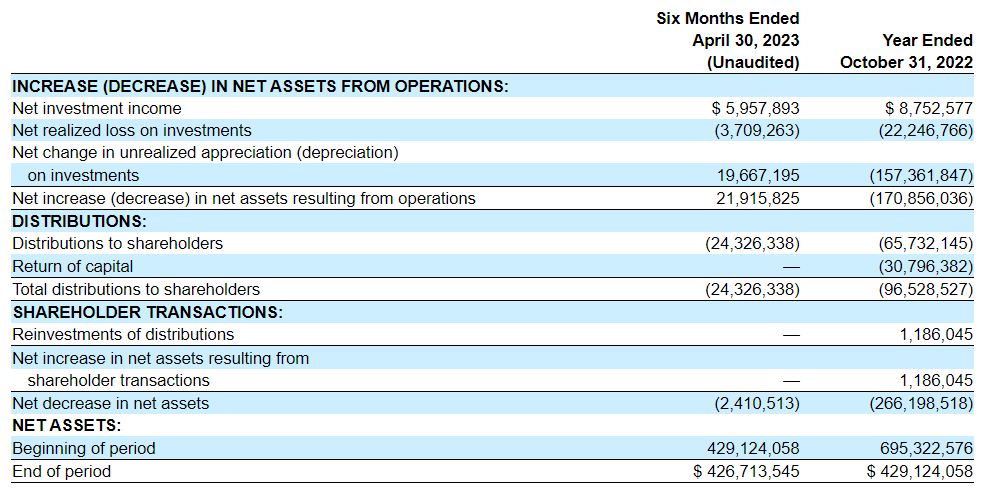

On a per-share basis, the net investment income in this last report came to $0.17 or what would be annualized to $0.34 to be comparable to the $0.25 last fiscal year. This is despite the rapidly rising borrowing costs the fund has faced, meaning that its portfolio has kept up with those rising costs and then some to produce even more NII.

Additionally, Calamos has noted that the premium for conversions has come down and that higher-quality companies are starting to issue convertible securities. The reason for higher quality companies to offer convertible securities is so that they can better manage the rising rate environment as well. They don't want to see their costs balloon, and by issuing convertibles, they can dilute equity in the future but keep interest costs more in check.

Of course, the bad news goes back to what we noted at the opening of the article. The distribution rate for this fund is high at 12.65%. Thanks to the discount, the NAV rate is a bit lower, but still elevated at 11.57%.

{kind=link}

That means despite a fairly strong year so far, the NAV has gone from $12.31 to start off the year to $12.16. That will mean that unless they deleverage, they'll most likely be in a situation where their leverage ratio stays high, and their distribution yield will also remain high.

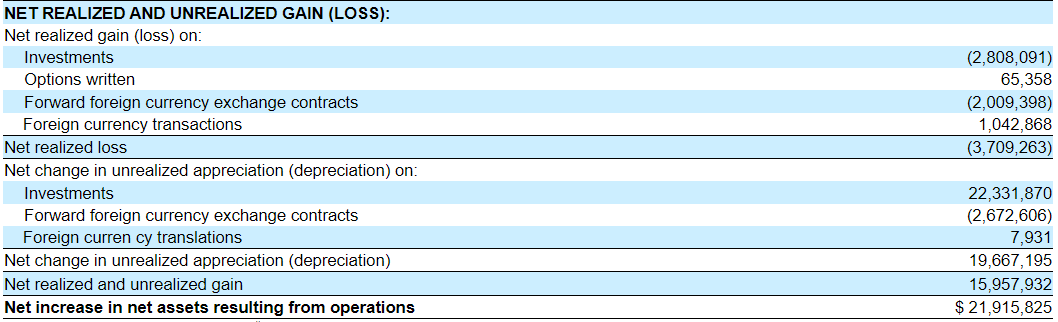

However, the other side of this is that if they deleverage, then the income the portfolio can generate will also decline, and that can make them rely even more on capital gains in the underlying portfolio. Of course, capital gains are already required in significant amounts to fund the distribution. An additional way this fund generates gains is through writing options and other currency-related derivatives. The unfortunate news is that none of those strategies really helped them in this last report.

{kind=link}

AVK's Portfolio

The managers of this fund are quite active, with the turnover rate coming in at 55%. For a six-month period, that's actually slowed down from the prior years of 186%, 126% and 242% turnover rates being reported.

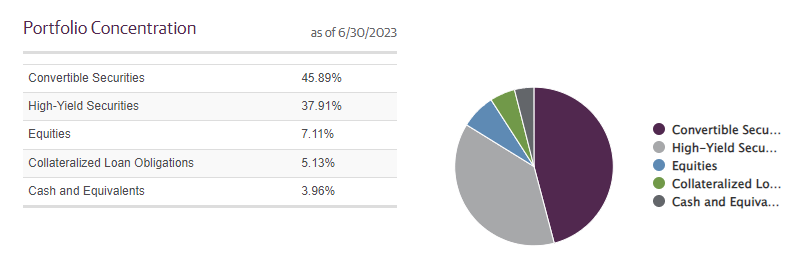

Despite this, the portfolio still generally is pretty consistent with having a high weight to convertibles and high-yield securities. So, the overall structure and exposure of the fund don't change too wildly, which is quite common for closed-end funds - even CEFs with such high turnover rates.

{kind=link}

In our last update, convertible exposure was listed at 48.73%, and high-yield securities were at 44.65%. This does mean there was a higher percentage elsewhere as equities saw a small increase, and so did cash and equivalents. We even have some collateralized loan obligations, or CLO, exposure at this time.

That being said, at a fairly minimal weighting of the fund, I wouldn't necessarily see this as a material change at this point. It is something to watch going forward to see if they will include more CLO exposure. It could be a benefit to the fund as CLOs are exposed to floating-rate senior loans, which means as rates head higher, so too should those yields. It also isn't listed, but the fund held a couple of senior loans as of their last report as well. This was only listed at 1.8% of assets.

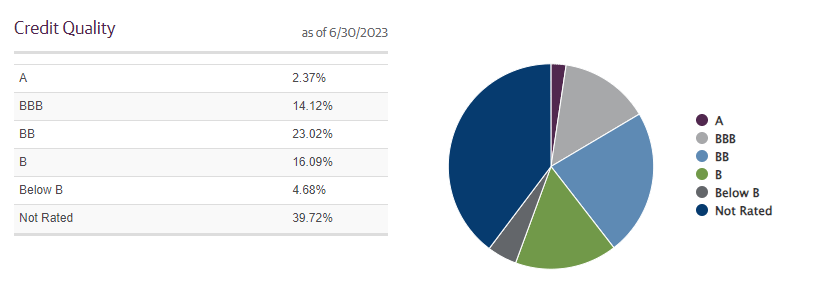

In looking at the credit quality of the portfolio, the largest weighting is allocated to the "Not Rated" category. This isn't that uncommon due to the convertible securities the fund holds. A good portion of these will be sold privately, and to get them issued faster and cheaper, companies will forgo the rating process. This is where investors have to trust the Guggenheim team to have their own process for rating and coming up with what they believe is appropriate for the portfolio.

{kind=link}

Since our last update, these weightings haven't changed materially. As expected, a significant portion is allocated to what would be considered high-yield or junk-rated debt.

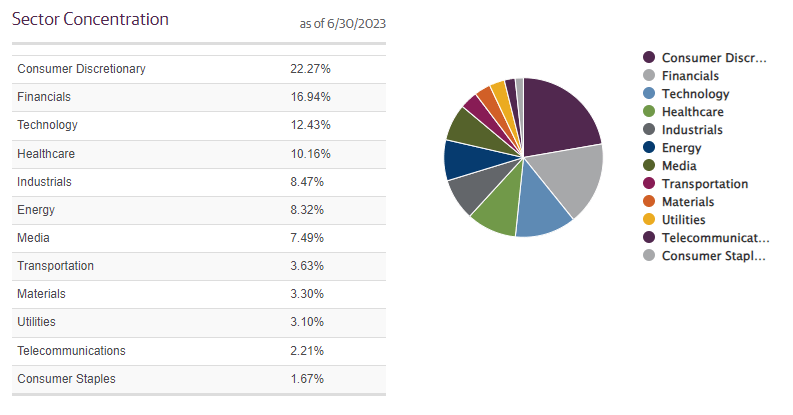

Another notable characteristic of this fund is that it doesn't overweight the tech sector. This is consistent with the last time we gave a look at the fund as well. Most convertible funds are heavily invested in tech, though the weightings have been coming down in the last couple of years as tech cooled off in 2022.

{kind=link}

Finally, as is generally the case with high-yield funds, they attempt to protect themselves through a high amount of diversification. We've already seen this is a fairly hybrid allocation in terms of asset weightings and sector exposure, but the fund also has listed 350+ holdings.

We see this diversification come through in their top ten as well, with no individual position carrying a materially outsized weighting. In fact, by the fourth largest position, we are already under a 1% allocation.

AVK Top Ten Holdings (Guggenheim)

Conclusion

AVK is an interesting fund, but it would appear we have more negatives than positives going on.

The high amount of leverage can quickly turn against an investor during a market correction, potentially causing the fund to deleverage and cause permanent damage. They deleveraged during Covid, but the massive rally following that in convertibles led by the "buy growth at any possible cost" made recovery possible (before falling rapidly back in 2022.) I don't think that scenario is something to count on in the future, though, either.

The distribution rate certainly is attractive. However, there is a reason I mention that "[AVK] offers a tempting distribution rate if one wants to reach for yield..." in my recent Calamos Convertible Opportunities & Income Fund ( CHI ) update piece .

The distribution yield is great for now, but it's pretty precarious. It puts the fund in a situation where they can't get out of it unless we see some serious rebounding. This year was a perfect example, as YTD's total return has been quite respectable. However, NAV per share still saw a small decline as the returns came entirely from the distribution, keeping its leverage ratio and NAV distribution rate elevated.

Given that the discount isn't necessarily putting it at a screaming buy either, I will still be on the sidelines for this fund. The silver lining to trading at a somewhat tempting discount is that if the distribution is cut, the fallout is generally fairly shallow.

For further details see:

AVK: Income Rising, But Leverage Remains Elevated