DUFRY - Avolta: Long-Term Story Remains Intact Upgrade To Strong Buy

2023-11-14 09:52:44 ET

Summary

- Avolta reported a strong Q3 and raised its guidance on revenue and EBITDA, driven by continued momentum.

- We believe the recent weakness due to macro slowdown concerns remains overblown as demonstrated by resilient Q3 performance and its performance during 2008 recession.

- Avolta also announced a new dividend policy (~2.4% yield) which it had paused since the beginning of the pandemic signalling a positive intent.

- We believe its long-term story remains intact, driven by its new capital allocation policy along with passenger recovery and strong operational performance.

Investment Thesis

In continuing with our coverage on Avolta (DUFRY), formerly Dufry AG , we had ascribed a Buy rating on the back of 1) long term potential on passenger growth and consumption demand 2) recovery in China 3) removal of the overhang with Avolta winning all its bids in Spain and 4) relative undervaluation compared to pre-pandemic levels. Sentiment for the stock had been weak as investors knocked off about a third of its value since the last results as a result of concerns on the travel recovery given macro pressures. However, we believe the concerns are overblown as demonstrated by Avolta's strong Q3 results as well as its performance during the 2008 recession. We upgrade our rating to "Strong Buy" and continue to like the long term trajectory and inflection of growing passenger travel and resilient defensive category play post Autogrill acquisition.

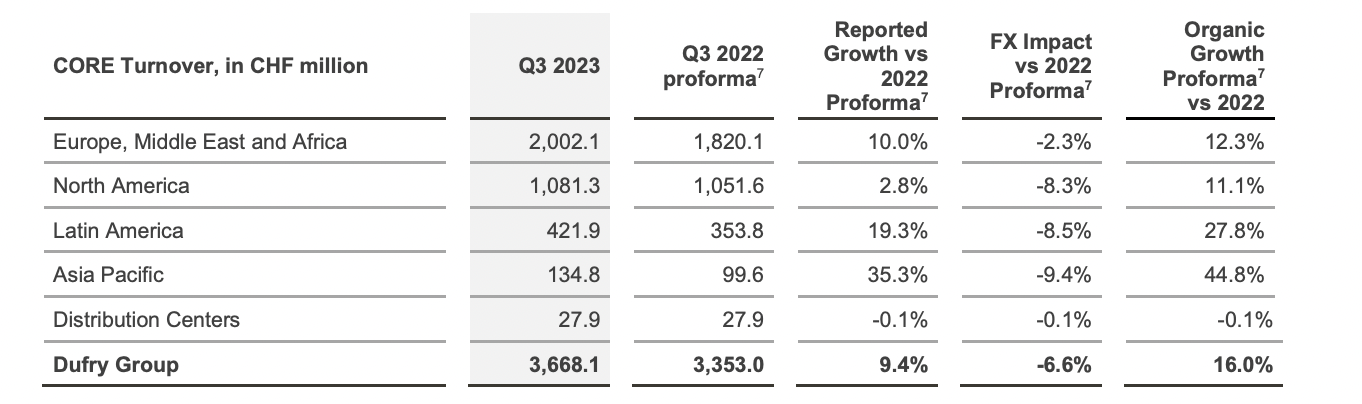

Robust Q3 Performance

The company reported strong Q3 with total sales up 9% YoY at CHF 3,668 mn, ahead of the consensus estimates. The strong growth was driven by a 16% organic growth with growth experienced across all regions despite facing relatively tougher comps compared to H1 2023, as organic growth as % of 2019 in Q3 2022 was ~90% compared to H1 2022 at just ~75% . This reflected slightly in the sales clip which decelerated slightly from 22% organic growth in Q2 but still a resounding growth. Growth in EMEA remained healthy at double digits driven by strong leisure demand, particularly in the Mediterranean which drove both F&B and Travel Retail spends higher. North America also reported a strong double digit growth benefited by Asian travel into Canada as well as sustained domestic demand. Asia Pacific growth remained strong at 45% but still off a low base as domestic travel and inbound travel in China showed continued signs of improvement while outbound travel continues to be pressured. Adverse Fx continues to impact growth which resulted about 7% decline on the sales growth for the quarter.

{kind=link}

Core EBITDA margins remained strong at 11.0% for Q3 driven by strong revenue growth, productivity improvements and synergy benefits, earlier than expected (higher than 9.5% growth in 9M 2023). It reported an Equity FCF of CHF 139 mn, down sequentially, primarily as a result of capex of the timing and integration costs.

Balance sheet position continues to improve as it ended with total liquidity of CHF 3.0 bn including cash and cash equivalents of over CHF 0.9 bn. Net debt position continues to be stable at CHF 2.7 bn, lowest since 2015 despite Autogrill acquisition with leverage position continue to be stable at Net Debt/ EBITDA of 2.6x and on track of its target to under 2.0x driven by new capital allocation policy. Debt has no near term maturities with over 80% of debt on fixed rate interest providing sufficient flexibility.

{kind=link}

The company revised its guidance upwards and now expects organic growth to be up 20% YoY (vs 7-10% YoY earlier) implying sales of ~CHF 12.5 bn, ahead of the consensus estimates. It also expects Adj. EBITDA margin of 8.5% - 8.7% (vs 8.3$ - 8.4% previously) driven by strong follow through performance in Q3 and earlier than expected realization of the synergy benefits. It also now expects EFCF of CHF 270 - 290 mn and has announced a new dividend policy with proposed dividend of CHF 0.7 per share (implying a yield of 2.4%) which was paused since COVID-19 through its new capital allocation policy. It also expects to invest two-thirds of EFCF in deleveraging and growth investments and further expects to provide the remaining third as a dividend which provides visibility on the cash flows and signals positive intent from management to drive shareholder value.

Addressing the Near-Term Weakness

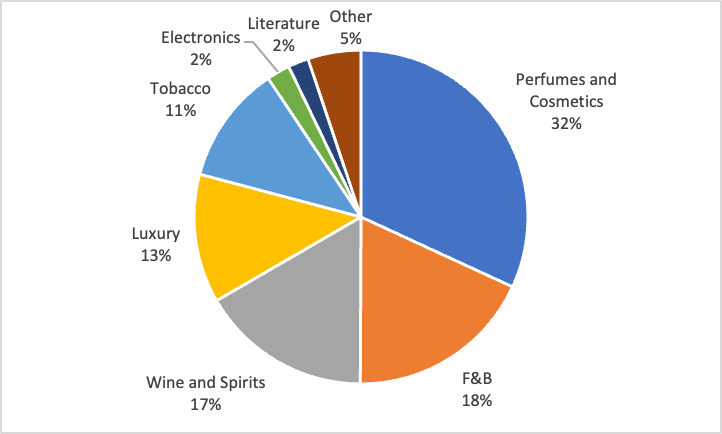

Dufry or Avolta shares have fallen by a third during the past three months, significantly underperforming the peers. We reckon the near term weakness is likely on the expectation of slowing sales momentum in a post pandemic world driven by macro pressures and looming recessionary fears. We believe in the event of an eventual consumer downturn, Avolta is more equipped as a result of higher share of defensive categories than history. As of 2019, the discretionary categories comprising of perfumes and cosmetics, luxury, electronics and literature formed about 52% of the total revenues with only 48% coming from defensive categories such as F&B, tobacco and liquor.

2019 Product Sales Split

{kind=link}

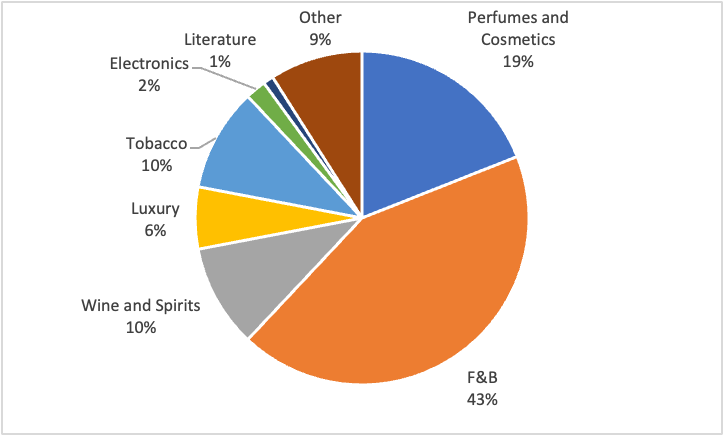

However, post the Autogrill acquisition, its category segmentation has heavily skewed towards defensive categories with discretionary categories contributing less than 30% of total sales. So we believe even in case of a potential downturn in consumer spends, Avolta is much better placed to deal with the situation.

9M 2023 Product Sales Split

{kind=link}

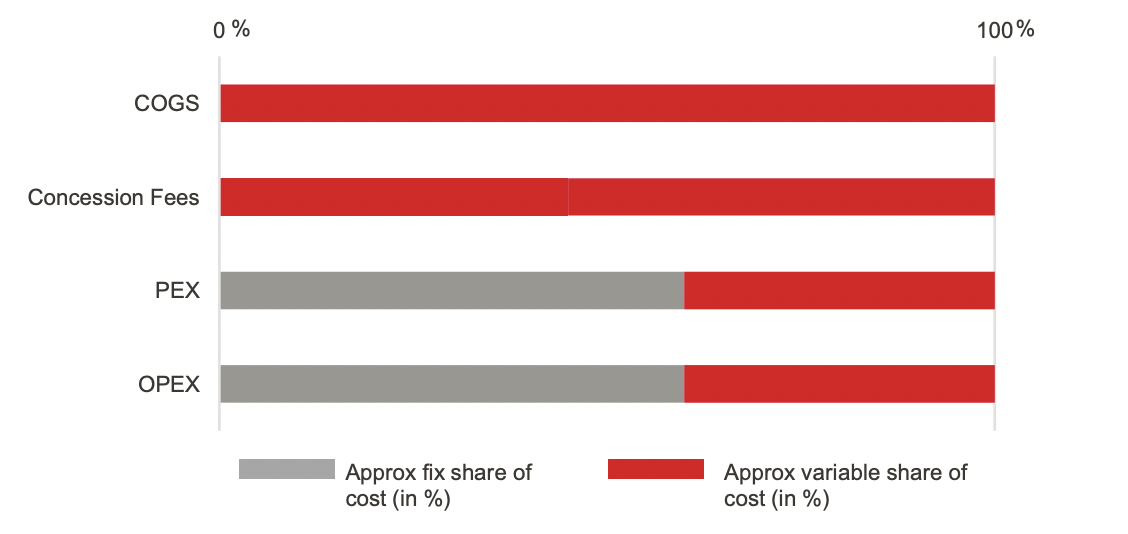

Dufry's cost base is highly flexible with a significant share of variable costs allowing them to defend margins even at the worst opportune times.

{kind=link}

Even during 2008 recession, the company recorded a strong double digit revenue growth in 2009 post a 9% growth recorded in 2008 driven by sustained travel demand. In addition, driven by its highly flexible cost base, the company reported resilient EBITDA margin of 12.7% compared to 13.9% in 2008 reflecting the cost efficiency and highly adaptable nature of the business.

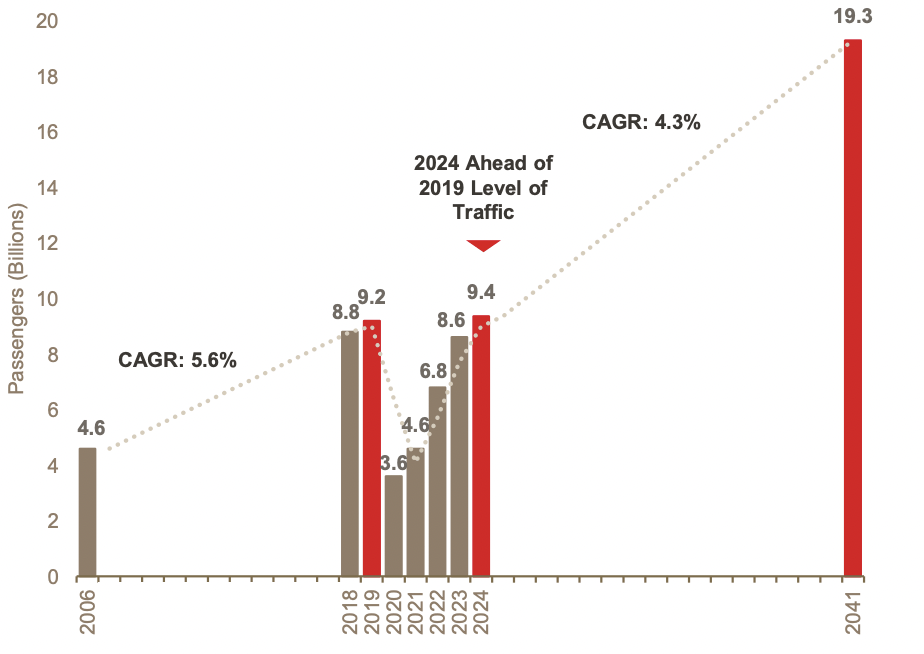

In addition, travel recovery continues to improve and is expected to surpass pre-COVID levels in 2024 and expect a stable growth of 4% CAGR in the future, slightly lower than 5.6% growth in the previous two decades.

{kind=link}

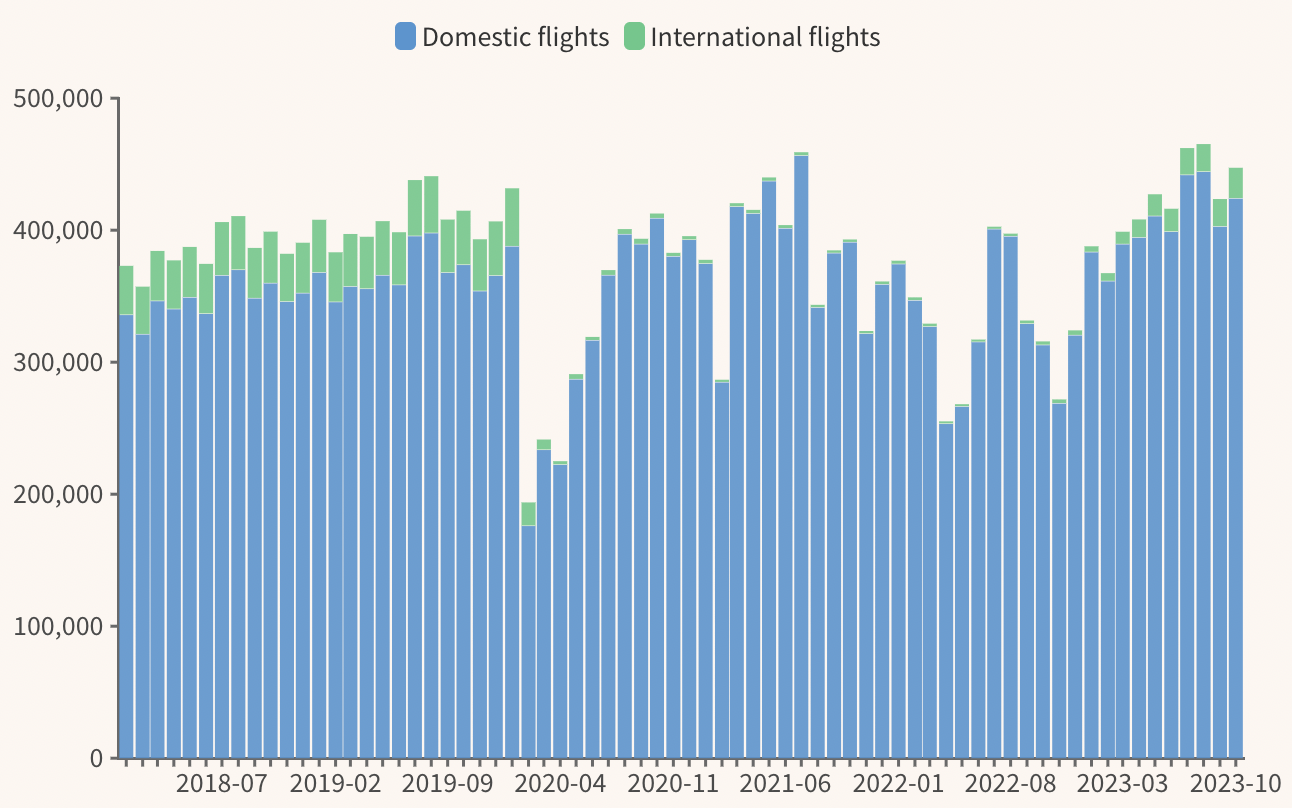

China's domestic flights have recovered strongly , however, outbound travel continues to languish and still treads at ~50% of the pre-COVID levels. We believe while the recovery may be slow, trends remain healthy on the back of pent up travel demand as well as governmental steps in the right direction such as visa on arrival for overseas business people to boost economic growth.

{kind=link}

Valuation

Post the recent decline, Avolta trades significantly cheaper compared to its historical long term averages. From an EV/ Fwd EBITDA perspective, it trades at just 4.9x at a significant discount to its historical average of 9.9x. We believe that there is a significant upside potential driven by its new capital allocation policy focusing on driving shareholder value and its improved ability to withstand any potential downturn. We continue to be positive on the overall long term play and believe there is a significant disconnect between the price and performance. We upgrade our rating to a Strong Buy as a result of steep discount and reiterate our target price of $6.0 (at 6.3x EV/ Fwd EBITDA, 30% discount to its long term average)

Risks to Rating

Risks to rating include

1) Decline in retail spends due to macroeconomic uncertainties and probable recession in the near future

2) Passenger recovery remains sluggish in China and any macro impact can significantly hamper further recovery

3) Capital spending remains higher due to Autogrill integration or otherwise which can lead to the company missing its free cash flow targets and may not lead to grow or maintain its dividends or delever its balance sheet as anticipated

Conclusion

We believe the concerns on the potential impact of recession and travel slowdown on the company are overblown and believe Dufry is well placed to withstand it as a result of category skewed towards defensives, highly efficient cost base, significantly lower leverage, strong operational performance and upside potential for travel recovery. Upgrade our rating to a Strong Buy and reiterate our target price of $6.0.

For further details see:

Avolta: Long-Term Story Remains Intact, Upgrade To Strong Buy