AXFOY - Axfood: Timeless Swedish FMCG Is A Buy Below This Level

2023-08-16 09:00:00 ET

Summary

- Axfood is a dominant player in the Swedish FMCG market, with impressive operating margins above the industry average.

- The company has shown strong sales growth and outperformed the broader market thanks to excellent selections and competitive prices.

- However, Axfood stock is currently trading at a valuation that offers limited upside potential, making it a "HOLD" at the moment.

Dear readers/followers

Axfood ( AXFOF ) ( AXFOY ) was one of the first companies I wrote about on Seeking Alpha. This was due to the massive appeal of the company at a sub-150 SEK share price (hard to believe today), and the sector overall. I invested over 8% of my capital into the company, which paid off in spades when the company rose above 300 SEK/share. At its apex, the company represented more than 14% of my portfolio - the largest single position I have ever held in any company.

This was probably the company that formed the basis of my "trim"/rotation strategy. Back when the company traded at its absolutely massive premium, I spent days calculating back and forth before landing on my stance that "I have to rotate this". I locked in a dividend-inclusive RoR of over 130% and remained with only 10% of my original position. This was one of the best investment decisions at the time because you can see what happened to Axfood after hitting those 300+ SEK high notes.

{kind=link}

My choice to sell - and at later points of around 220-230 SEK start buying back slightly was obviously the right one. It also shows you why valuation investing is key to any serious outperformance in my portfolio - if you hadn't trimmed or sold, those gains would have been normalized down to a 6-year 48% RoR.

Let's look at where the company is today and what we could expect from the company.

Axfood - Upside in FMCG's - if they're cheap.

So, as mentioned in one of my original pieces, the Swedish FMCG market is essentially an oligopoly. At the time of writing this article, it was actually possible through investing to gain exposure to around 70% of that market. That is no longer possible, with the dominant player ICA, being taken private about a year or so ago. This was another one of my better investments at the time.

The competition that remains isn't publically traded - with the sole exception of Axfood. Coop is a cooperative, City Gross is privately owned, Lidl is privately-owned, and Netto isn't available on the stock market either. This makes your options limited.

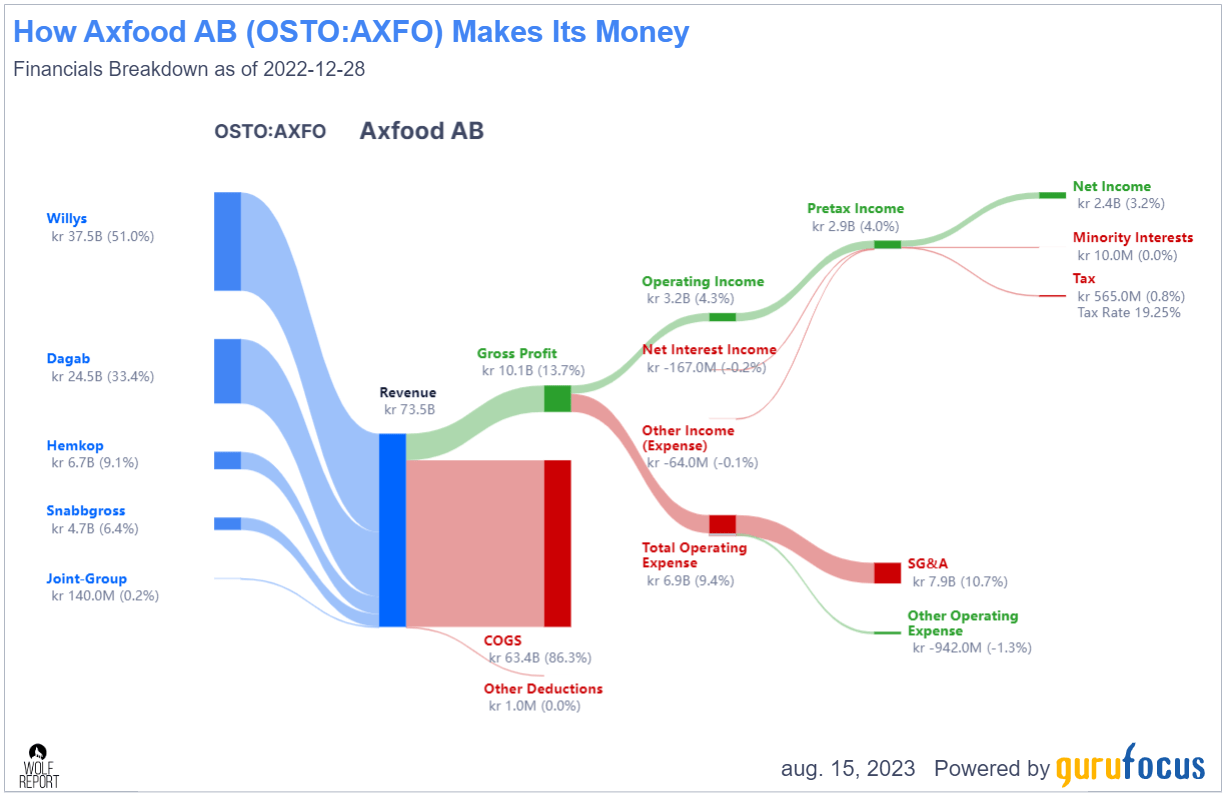

The company's history since its beginnings in 2000 when it fused from several smaller companies has been nothing short of stellar. What marks Axfood from both international and regional competition (outside of Sweden at least) is its impressive operating margins , for a FMCG company. The typical margin is on the 2-4% level and a 0.5%-2% net margin. Axfood typically manages 1-2% above that.

{kind=link}

The reason they manage this is a much more favorable trading environment for the stores in Sweden - even more so than in the US. Regulation prevents excessive litigation, and this enables players like Axfood to leverage their market position to introduce private label "copies" essentially of brands that have become loved, with these brands having very little recourse. This is common not just for Axfood, but for other of the larger players as well.

This does not make qualitative brands harder to buy in Sweden - such as Orkla ( ORKLY ), but it does mean that these FMCGs do have an advantage - and that's where that margin variance comes from.

Axfood manages a net margin of over 3% - and that's actually down from previous years. It's been over 4%.

{kind=link}

And whenever you're talking about an FCMG with numbers and structures like this, you're looking at a fundamentally appealing company. Because what could happen to a 22%+ market share player in this field? Inflation? They'll raise prices - and have. Competition? It's been tried, by Lidl, and they're still at sub-10%, and no longer as cheap as they were when they were introduced to Sweden.

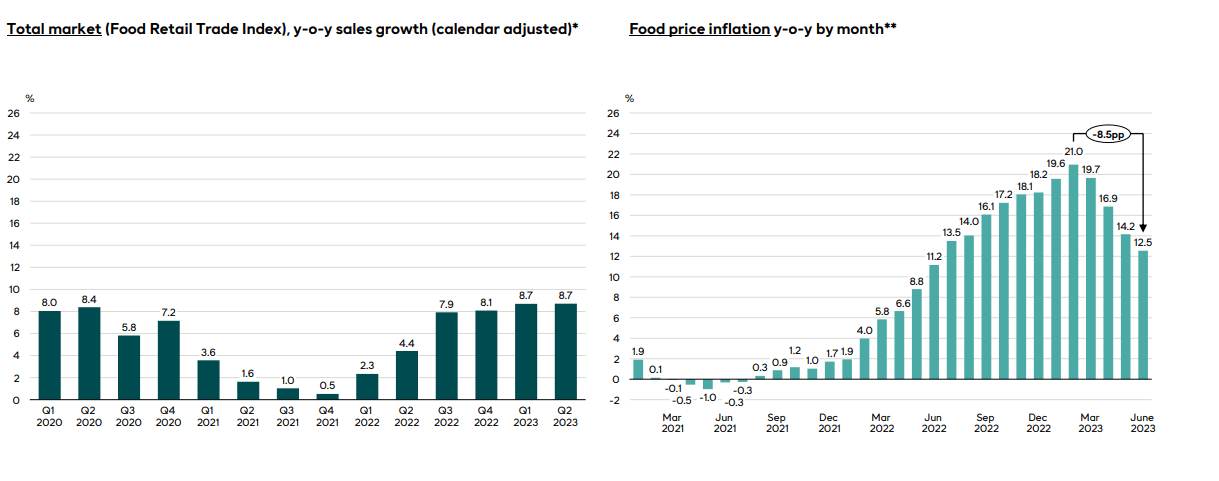

Axfood is a supremely entrenched player with exposure across the entire nation. I don't see it going anywhere. The latest results we have from the company is 2Q23, and naturally, aside from earnings, the focus is on inflation. This gives you a very good picture of what Swedish society has been battling in terms of food prices.

{kind=link}

Let me state clearly that I believe that food prices were far too cheap a few years ago. I'm actually in favor of higher prices for food, provided that producers and quality also rise.

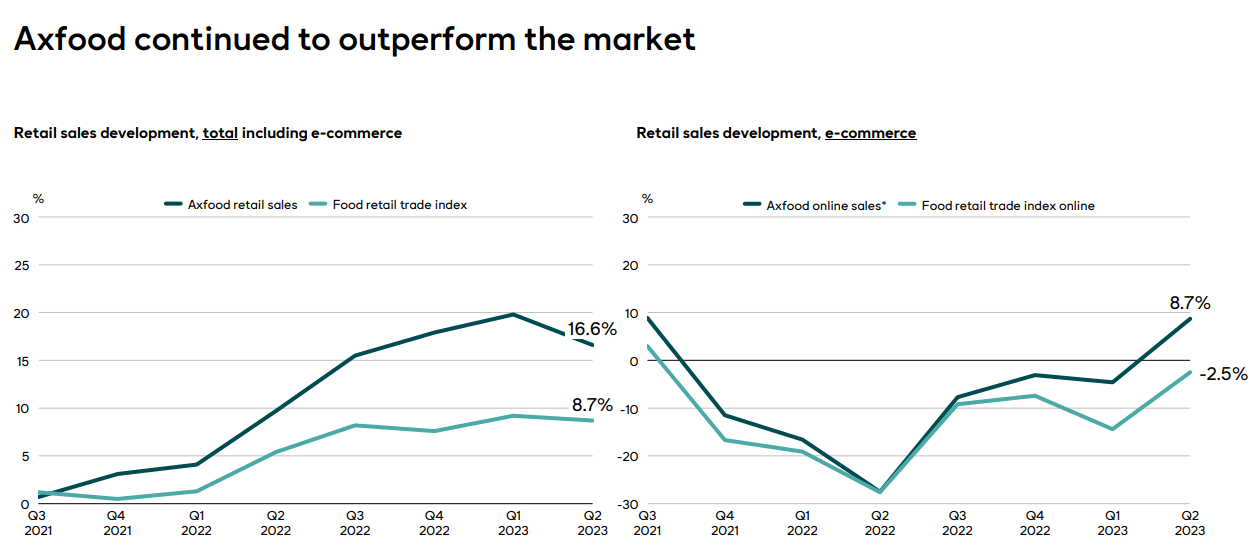

But for the company, and my thesis for Axfood, what remains important is that Axfood continues its streak of outperformance . And the company does. Since 2021 at least, the company has outperformed the broader market thanks to excellent selections and competitive prices, and this has continued until now.

{kind=link}

The company is seeing strong net sales growth despite inflation. a 12.6% sales increase, with 16%+ retail sales nearly doubling the market in terms of retail. E-commerce, despite increasing softness in this market as people become more price and fee-aware is also growing.

At an adjusted EBIT margin, the company is still above 4.4% , which is absolutely stellar for both the sector and the cost trends we're seeing. On an adjusted EBIT level, the company managed nearly a billion SEK in EBIT, which annualized to a run rate of 4B. Every segment grew its earnings. Willys, the company's largest segment and brand, grew exceptionally as customers moved from pricier alternatives like Coop and ICA to Axfood.

{kind=link}

When it comes to priciness in Sweden, Coop and ICA are the most expensive, followed by Axfood with a shared 2nd-3rd place with Lidl and CityGross. So this type of move is, as I see it, expected as pressure increases. Not only that, I believe the trend is likely to continue on a forward basis.

The company owns the nation's most recommended retail chain and has been since 2020 (Source: YouGov Benchmarking Study).

If you're interested more in the company's various brands and how they "attack" various segments of the market, I recommend that you peruse the selection of earlier articles I've written on the business. In the totality of the 5+ articles on Axfood, you'll find the most relevant information on the business and the consideration of Axfood as an investment.

Overall, the first entire half of the fiscal was nothing short of stellar. With an adjusted operating profit growth of 14.3%, I now expect over 4B SEK in adjusted EBIT for the full year, and certainly over 100B SEK in net sales revenue - over 150B SEK even.

On a cash flow basis, 1Qs are always tricky due to net inventory buildups prior to easter. But this always sees a 2Q normalization - so too this quarter. The company's overall fundamental position is absolutely solid. Net debt is up slightly, due to loans and leasehold debt, but compared sequentially is down to lower utilization of credit. To put it into a number, the company has a net debt/EBITDA of 1.8x - but again, this is accounting for IFRS 16 leases. Without IFRS 16, the company would be at a net debt/EBITDA of 0.3x.

That's an important difference.

I would continue to, on a forward basis, look at things like food price inflation, general retail sales trends, and the evolution of the company's brands. I foresee very little change on a high level for the company, or for any Swedish FMCG. This is an extremely mature market - every permutation of competition has been tried, in both national and coming from International markets. All have failed to generate real impact or market share, Lidl being the most successful with billions in investment. And what sort of market share has that resulted in?

5.7%.

Sweden is a tricky market in terms of groceries. As Lidl found, unless you offer the products people are used to (as opposed to natively German products, which is where the company began), you won't generate much in terms of sales or market share.

Let's look at Axfood's valuation.

Axfood valuation - Plenty to like, but not at this price.

As I present Axfood, you'll get the impression that this is a company you want to own, no matter the price. The first part is right, the second isn't. It's the biggest mistake Scandinavians make with FMCG investments. They overpay - not just for Axfood, but competitors like Kesko (KKOYF) as well.

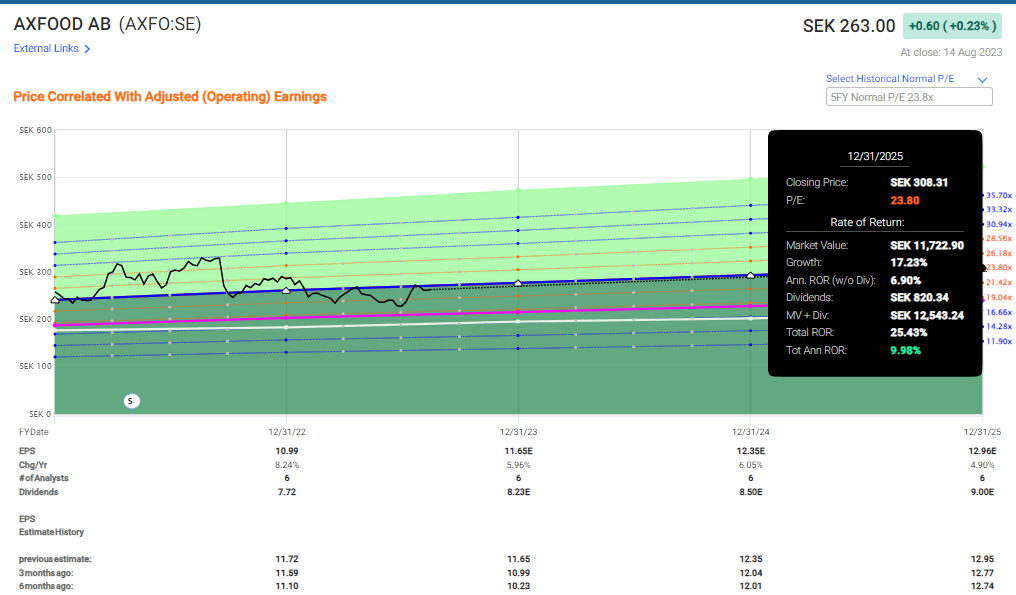

Axfood as a business and stock currently trades at an average mixed P/E of 23.1x with a 5-year normalized P/E premium of just south of 24x. Based on its current yield of 3.1% and a growth rate of about 5-6%, this marks the company for a single-digit upside in this environment, albeit close to a double-digit one.

{kind=link}

This is not a good enough upside or potential for me to invest straight into the common share - my minimum conservative upside for that is at 15% or above. I've also looked at the various ways of investing in the company through options - and none of those mark it as an appealing entry point here.

S&P Global gives us a target range of 230 SEK on the low side and 300 SEK on the high side. The average for the 4 analysts following it is 272 SEK, which has 2 of them at a "BUY", 1 at a "SELL" and 1 at "HOLD". I would say the average PT is about 40 SEK too high, which makes sense to me from the relative premium offered by the company even at this valuation. What we have to remember is that many investors would in fact be thrilled with 10% RoR per year - and if it was risk-free and guaranteed, I'd invest in that all day long. The problem is that outside of the risk-free rate, currently at around 4%, there are no such guarantees, which is why I go for 15% and above to make up for the inevitable underperformance of some investments.

No one has "all winners" - no one that I've met at any rate.

Axfood is a superb company and a superb investment - at the right price. But in order for me to see the upside and return that I am looking for, I won't buy it above 235 SEK/share. I've written plenty of Puts around the 220-225 SEK level over the past few months, annualizing everything from 6-14%. I currently do not have puts running, but I do have some shares left in the company.

Here is my current thesis for Axfood.

Thesis

- My thesis for Axfood includes wanting to own the only publically-traded FMCG company in Sweden at a good price. At that good price, it combines a 3-4%+ yield with an annual upside in the low double or high single digits, making for a compelling mix of quality and safety while offering market outperformance.

- The company is a, to me, surefire investment at any price below 220 SEK. At anything above 240 SEK, it becomes dicey in terms of double-digit upside, at its current valuation and scale.

- I've played the company both with puts and calls, and plan to sell some attractive covered calls if we see 290 SEK or above again while selling puts below 245 SEK, and constantly looking at the annualized appeal of buy-writes on a 12-month forward basis.

- The company warrants a "HOLD" from me at 260 SEK/share, with a PT of 235/share at the very highest.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company lacks a meaningful market-beating upside on a forward basis at a price of over 260 SEK/share, and for that reason, I'm at a "HOLD" here.

For further details see:

Axfood: Timeless Swedish FMCG Is A Buy Below This Level