AZIHF - Azimut Holding: The M&A Splurge Does Not Excite Me

2023-05-02 18:04:49 ET

Summary

- In this article, I am reviewing the long thesis on Azimut Holding since my last coverage.

- The latest financial report (FY22) was OK, with recurring fees reaching a new ATH.

- Management focuses on AUM growth at any cost, but I am concerned as international expansion is not as profitable as the domestic market.

- Shares may look optically cheap at 7x P/E, but I am in no rush to buy back into the stock.

Review of my investment thesis

When I last discussed Azimut Holding ( AZIHF ) ( AZIHY ) in 2019, I held a positive view of this stock. I based my investment case on three factors. First, the company had a good execution track record. During the 2010/2019 decade, Azimut grew AUM steadily at a CAGR >10%. Results were even more impressive considering that Azimut is a traditional active asset manager relying on a network of financial advisors to distribute its products. Therefore, the company seemed to have been successfully fighting off a mega-trend of consolidation and passive investing democratization through ETFs. Second, Azimut traded at an attractive P/E ratio, showing a considerable discount to its historical averages. Lastly, consensus estimates were below what I expected Azimut to deliver for the next quarters and FY2019.

Azimut proved me right; results came in ahead of the Street's expectations, and shares rallied. Even if Covid-19 caused some market turmoil and the share price fell during the first half of 2020, the strong recovery allowed me to sell shares in 2021 at the price target of €26 I envisioned in my article . I no longer hold a position, but I still follow the company. The stock has lost about one-fourth since then and is trading at around €20 per share. I am somewhat unconvinced that shares are a genuine bargain, though the company trades at extremely undemanding multiples.

FY2022 results: Make-up operation

At first glance, the price drop seems consistent with the company's results. Revenues contracted 11%, totaling €1.29 billion vs. €1.45 billion in 2021. The consolidated net profit also fell by 34% vs. the record results of 2021. The absolute figure came at €402 million or €2.89 per share vs. €605 million, or €4.35 per share the year before. However, Azimut ascribed much of the negative results to a different revenue mix and pointed at recurring fees reaching a new all-time high in 2022 at about €1.1 billion. Indeed, the figure is well ahead of the €0.97 billion earned in 2021 and €0.77 billion in 2020.

{kind=link}

However, the company has been winding down variable fees from its products for several years, and 2021 results were a notable outlier. In the future, Azimut expects variable fees to contribute only 5% to 10% of total revenues. To further clarify the point, Azimut introduced investors to a new "recurring EPS" metric, showing a comforting growth from €2.24 in 2021 to €2.55 in 2022. I understand but do not welcome the choice, as management sought to use the figure to erase the faltering net result from its presentation completely.

Looking at P/E

With a current P/E multiple of 7x, equivalent to an earnings yield of 14.3%, Azimut appears downright attractive compared to the "fair" 12x mid-cycle multiple I assigned a few years back. Even considering only the €2.55 "recurring EPS" amount, Azimut would still trade approximately 1x turn higher or 8x its TTM earnings.

In 2019, I argued this company could and should have traded at least back to around 12x earnings, a 20% discount to the then five-year P/E average of 15x. Looking at the closest competitor Anima Holding ( ANNMF ), the company currently sells for 11x, but against a 9x five-year average. It is, therefore, increasingly challenging to present an investment case based on relative undervaluation now that Azimut's historical average has gradually decreased to 9x. I see no catalyst for an expansion, and the compression results in a very low baseline multiple, highlighting the market skepticism towards Azimut's future growth prospects.

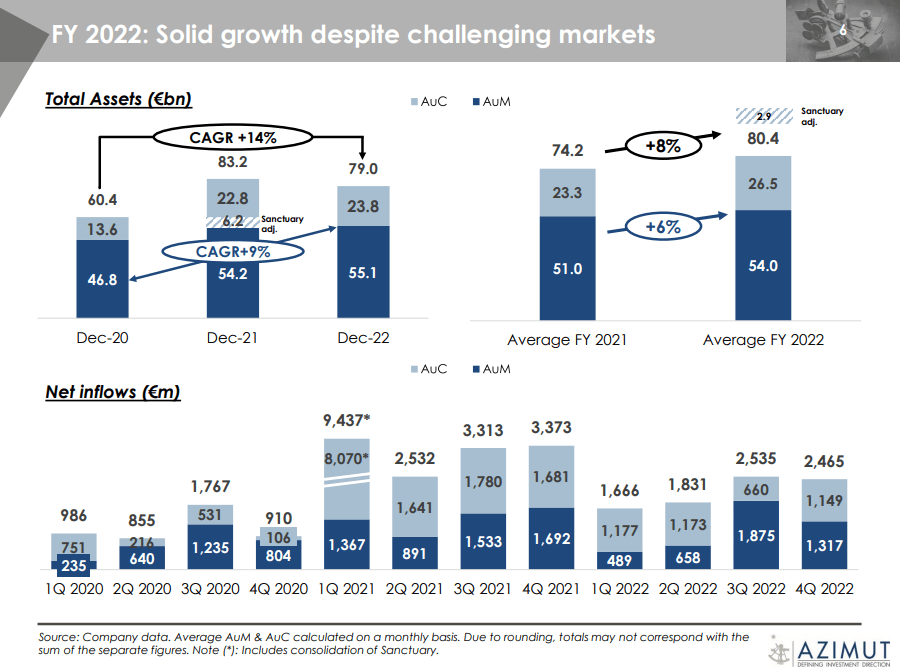

While results are superficially strong, I have also grown somewhat cautious about their sustainability. The company has decisively invested in M&A to boost its top-line results but might have gone too far to maintain appearances. With the weighted average performance on its fund turning negative last year, even the aggressive acquisition of new money masses could not prevent a fall in total AUM. The sluggish market performance determined a slight decline (-5%) in total assets from €83.2 billion at the end of 2021 to €79 billion at the end of 2022.

Azimut's growth

For an asset manager, the best way to gauge long-term growth potential is to understand the evolution of the company's assets under management ((AUM)). The higher the AUM, the bigger the recurrent fees the manager can receive. At face value, Azimut's results have been steady. Even if market turmoil prevented the company from achieving a new all-time high at the end of 2022, AUM still increased at an impressive 15% CAGR from the €19.6 billion managed at the end of 2012.

However, the main problem with this general assessment is that assets can grow in many different ways. The company can a) generate an outstanding performance of the managed funds; b) increase net money inflows from existing customers or find new customers through its existing distribution platform of financial advisors; c) find inflows from new customers acquired through M&A activities. Arguably, method (a) is the best, (b) is OK, and (c) is the worst, and for good reason. First, acquiring new masses in this way comes at a higher cost, and second, even if investment assets are somewhat sticky, there is no way to keep them captive, thus exposing the firm to the risk of paying for a bunch of melting ice.

Azimut's investors deck, April 2023

{kind=link}

Organic growth vs. M&A

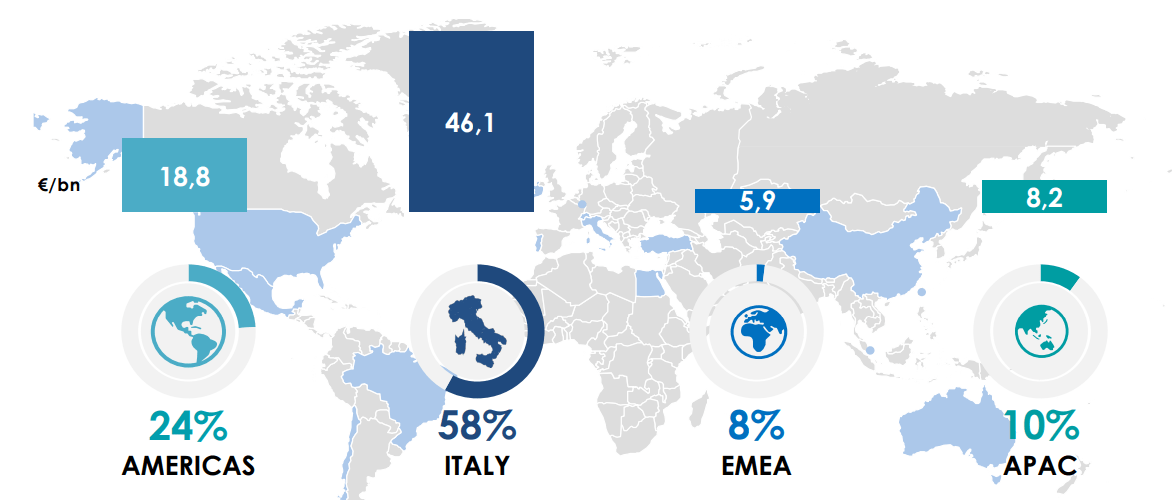

Over the last few years, Azimut has decided to venture into a geographical diversification strategy and grow outside the Italian domestic market. To achieve it, the company aggressively targeted the acquisition of boutique investment firms, especially in the US and Australia.

Azimut's investors deck, April 2023

{kind=link}

The strategy seems questionable at best. The American market can arguably turn into a vast ocean of growth for Azimut, but at the same time is one of the most competitive markets in the world. To venture without appropriate financial backing or a disruptive plan seems like a high-risk operation with no other apparent purpose but to gain new investment masses for show.

Of €8.5 billion net inflows registered in 2022, Americas contributed €5.3 billion, 62% of the total. While the M&A deal terms usually remain undisclosed, the total impact on cash flow is public. Azimut disclosed a 2022 total spending in M&A of €180 million (but also absorbed liabilities worth €60, so communicated to investors a total expenditure of €240) on top of €140 spent in 2021. Azimut spent €380 million over two years, or 51% of the cash generated. This value compares to about €90 million/year in 2019/2020 (20% of the cash generated) and €60 million/year in 2017/2018 (32% of the cash generated).

Azimut has increased reinvestment to over half of its profits to prevent AUM from falling, hoping that the acquired assets' stickiness will eventually allow Azimut to recoup acquisition costs. I am not sure I like the odds of this gamble, and as a result, Azimut's dividend payout ratio has decreased considerably. When I held the stock, I appreciated management's commitment to return over 70% of its profits. That seems like a thing of the past now. Despite generating approximately €12.6 cumulative EPS since 2019, the four-year cumulative dividends dropped to €4.6 or about 37% payout ratio.

AUM vs. AUC

In addition, I am concerned about the "quality" of the assets Azimut is acquiring at hefty prices. When the company refers to "total assets," the figure (correctly) includes both AUM and Assets Under Custody (AUC). The evolution between 2014 and 2022 shows how the growth of custodian assets has outpaced the placement of Azimut's proprietary products:

And Value For All

The FY14 breakdown shows that almost 90% of Azimut's total assets were under proprietary funds. By 2018, the distribution structure had changed to 80/20. Now, the FY22 balance indicates how the AUM share of the business has further declined to less than 70%. The trend coincides with Azimut's push to diversify away from its home country and pursue international expansion, demonstrating the difficulty in replicating the distribution model that works so well in Italy.

Even if AUC still represents business brought under Azimut's roof, assets under custody, by definition, these assets do not produce management fees. As international clients favor passive funds, Azimut has no choice but to provide them. But how sticky can these assets be?

Valuation

Even if I agree with the market that Azimut's outlook is uncertain, it also appears that much of this uncertainty is already baked into the share price. Using a simple DDM model, I value the firm's equity at approximately €23.6 per share.

Even if, in theory, the current payout of €1.3 is well below Azimut's cash generation potential, the lofty price tags paid for assets acquired through M&A seem like an increasingly necessary cost of doing business, and the actual payout may be much closer to 75%-80%. Assuming a 20%-25% real reinvestment rate and a 25% ROE generated, I expect Azimut to grow EPS at a 5%-6% rate going forward. The growth figure is, on one end, well below the company's last 10-year average of 8.9% but, on the other end, significantly ahead of its most recent 3-year growth of 2.9%. I used an 11% discount rate.

The target assigns a 9x multiple on Azimut's recurrent earnings from last year. Even if the multiple appears relatively low, it is worth noting that Amundi ( AMDUF ), which I consider a vastly superior business, currently trades at just 11.5x earnings.

Investors' takeaway

Even if Azimut has enjoyed relatively better growth than its competitors in the past decade, I am skeptical of its current direction. Management has spent too much capital on M&A, only to acquire money masses that might prove still bloated by a 15-year-long bull market or more volatile than expected.

The current valuation appears undemanding based on earnings, but the same could be said for Azimut's most important peers in the Italian (Anima) and European (Amundi) markets. Despite seeing a potential mild undervaluation, I am not ready to act on it at this time. Therefore, I assign a hold rating.

For further details see:

Azimut Holding: The M&A Splurge Does Not Excite Me