BMRRY - B&M European Value Retail: Discount Retailer Dominating Its Market

2023-10-10 20:14:48 ET

Summary

- B&M’s revenue has grown at a CAGR of +18% during the last decade, with an incredibly consistent upward trajectory. EBITDA has exceeded this at +20%.

- B&M’s growth can be attributed to a compelling business model, allowing it to aggressively increase store count, conduct M&A, and maintain strong like-for-like growth.

- B&M has shown supply chain excellence, with a post-pandemic bump contributing to margins normalizing at an elevated level.

- We believe the affordable retail segment will continue to perform well, owing to difficult macroeconomic conditions and comparable quality.

- B&M’s valuation suggests a reasonable upside, with the key for us being an improvement in its NTM FCF yield.

Investment thesis

Our current investment thesis is:

- Although B&M’s business model is not complicated, we do think it’s unique enough to be defensible in its core markets. The business has developed a strong geographical presence and brand, with an impressive cost-to-price value proposition. Its peers lack the variety and broader supply chain capabilities to replicate this.

- From a financial perspective, we see a good runway for further growth, with normalization at margins above its pre-pandemic level. This improvement does not look to be wholly priced in, with an NTM FCF yield in excess of its historical average (6%).

Company description

B&M European Value Retail ( BMRRY ) is one of the leading variety retailers in the UK and Europe, offering a wide range of products including groceries, household goods, and general merchandise. With a focus on providing high-quality products at affordable prices, B&M operates a network of stores across multiple countries, catering to diverse consumer needs.

Share price

B&M’s share price performance since it was listed has been respectable, with strong returns when including dividends. This is attributable to its continued strategy execution, in conjunction with a post-pandemic acceleration.

Financial analysis

{kind=link}

Presented above are B&M's financial results.

Revenue & Commercial Factors

B&M’s revenue has grown at an impressive +18% CAGR during the last decade, with broadly consistent growth throughout this period. The driving force has been new store expansion throughout the UK, alongside acquisitions and sequential improvement in its organic trajectory. Profitability has exceeded this, with EBITDA growing at +20% and NI growing at +23%.

Business Model

B&M's core business model revolves around offering discounted products. By negotiating bulk deals with suppliers and focusing on a limited selection of fast-moving products, B&M keeps its operational costs low and passes the savings on to the customers.

B&M's primary appeal is its value proposition. Offering quality products at significantly lower prices than competitors attracts budget-conscious consumers. This model has been a clear winner during the last decade suggesting consumer interest is increasing, with businesses such as Dollar General ( DG ) and Dollar Tree ( DLTR ) significantly outperforming.

B&M offers a wide range of products, from groceries to household items, electronics, furniture, and seasonal goods. This diversity in product offerings attracts a broad customer base. The company competes with a range of “traditional” retailers across its key geographies, owing to this broad product range. B&M places a significant focus on private-label products, allowing for lower prices. These in-house brands often yield higher profit margins compared to reselling established brands.

B&M has displayed adaptability by quickly adjusting its product offerings to align with consumer trends. This is important as B&M’s business model only succeeds if consumers keep frequenting its stores.

Given the focus on price and thus cost, B&M focuses heavily on maintaining an efficient supply chain, ensuring products are stocked consistently and costs do not materially vary. Effective inventory management has allowed for reduced wastage and cost management, enabling the company to maintain its competitive pricing strategy (GPM remained between 34-35% between the years FY13 and FY21, illustrating this).

A strong component of B&M’s supply chain management is utilizing its physical locations. In order to operate this effectively, the company has limited the ability to purchase online. B&M strategically locates its stores in areas with diverse customer demographics but with sufficient density of its core demographic. This is not a business that will be seen in central London but has several locations in East London.

B&M has grown significantly through acquisitions, expanding its store network and market presence. Most recently, the company has acquired 51 Wilko Stores (a competitor that recently collapsed), allowing for an accelerated entry into attractive markets (cost was ~£13m).

Overall, we believe the company’s business model is extremely strong, illustrated by its growth and margins. So long as the business can continue to source products and manage its supply chain as it is, which appears more than reasonable, we see the company continuing to gain market share from the “traditional” segment. A larger portion of the public is increasingly resonating with the affordable segment, as the UK (similarly to the rest of the West), has seen growth in the wealth gap.

Margins

{kind=link}

B&M’s margins had been broadly flat over the historical period, which is understandable given the market dynamics and level of competition. Following the pandemic, however, the company has seen a noticeable appreciation, despite inflationary pressure. We consider this a reflection of its growth in competitive positioning, with consumer demand increasing and the value proposition of discount retailers improving.

We do believe a degree of normalization is ahead, primarily due to the current weakness, although this will not be substantial given the affordable segment will be more robust. An EBITDA-M of 11.5-12.5% is realistic in our view, higher than the 9-11% prior to the pandemic.

Recent results

B&M’s recent performance has been muted, with a decline relative to its pandemic peak but a normalization subsequently. In its last 2 half-years, revenue growth was +1.8% and +11.2% (following +1.2% and (6.0)%). In conjunction with this, margins have slipped, with two successive half-years of ~12%.

We believe the slowdown is a reflection of the current macroeconomic climate, with consumers cutting back on discretionary spending and other larger-ticket purchases (such as houses impacting demand for furniture products). This is due to the combination of inflation and interest rates, with the combined impact being soaring living costs.

Discount retailers will often perform well during economic downturns. During times of financial hardship, consumers tend to seek out more affordable options. This is why, despite the slowdown, we consider B&M’s performance strong, as it is superior to the wider market.

Looking ahead, we see continued economic struggles in the UK (B&M’s key market), similar to the rest of the West. Although some will be negative regarding Brexit, etc., The UK recently revised its economic growth results, implying it is actually a top performer ( 2% larger than expected ). The reality is, it will follow the US, as it has for an extended period. To us, this implies a recovery in mid-to-late 2024.

Key takeaways from the company’s most recent quarter are:

- Trading momentum has improved, with growth acceleration. Relative to Q1’23, the Group’s total revenue growth was +13.5%.

- Grocery and general merchandise categories have performed exceptionally, owing to consumers flocking to the affordable segment for essentials.

- Management believes the business is well positioned for the transition into the autumn/winter period, with strong controls over product and pricing.

Balance sheet & Cash Flows

B&M’s balance sheet is relatively clean, with an ND/EBITDA ratio of 2.6x. This represents an interest coverage of 7.9x, which is comfortable in our view. Further, the company has a tremendous conversion of profitability to FCF, allowing for reinvestment and shareholder distributions at an attractive rate. As the following illustrates, its ROE has consistently improved, even prior to the pandemic.

{kind=link}

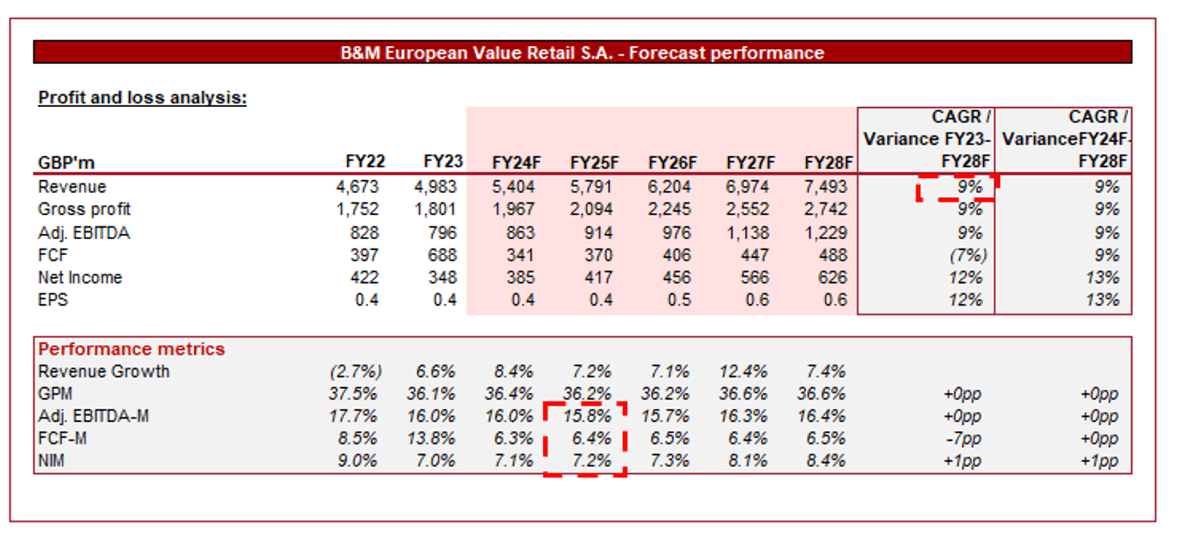

Outlook

{kind=link}

Presented above is Wall Street's consensus view on the coming 5 years.

Analysts are forecasting a continuation of its strong growth, although at a level below what has been achieved historically.

The slowdown in growth is inevitable given the proportionate store openings cannot continue exponentially. This said, we consider a 9% rate an impressive trajectory in a highly mature industry, illustrating its long runway to penetrate the UK market further.

Further, margins are expected to flatten at its current level, a reasonable view given the company is already above its historical average. The scope for operating cost leverage is reasonable, so we could see this creep up.

Industry analysis

{kind=link}

Presented above is a comparison of B&M's growth and profitability to the average of its industry, as defined by Seeking Alpha (19 companies).

B&M’s performs well relative to its peers. The company has superior margins and FCF, owing to its strong market position and superior supply chain management. Its growth lags behind its peers, although we attribute this to the composition of the peer group. Many broadline retailers are tech-enabled, for example, contributing to outsized growth. If we compare B&M to a subset of mature retailers, its growth is above average.

Valuation

{kind=link}

B&M is currently trading at 13x LTM EBITDA and 9x NTM EBITDA. This is a discount to its historical average.

Our view is that a discount to its historical average is warranted, owing to the company’s strong growth thus far attributable to store growth. This is unsustainable and so we expect the trajectory to soften in the coming decade. We would suggest a ~15% discount to account for this.

B&M is also trading at a discount to its peers, with a 15% delta on an LTM EBITDA basis and a 37% delta on an NTM P/E basis. Given the growth delta, a discount is equally warranted from this perspective. Again, we would suggest ~15%.

This implies a reasonable upside at its current valuation (~12%), which we believe is strong, particularly when factoring in an NTM FCF yield of 5.9%. As the following illustrates, the company’s yield has progressively improved, suggesting it has become cheaper despite the growth and improvement in profitability.

{kind=link}

Key risks with our thesis

The risks to our current thesis are:

- Economic downturn impacting consumer spending - The longevity of contractionary policy will impact the demand for non-critical spending, contributing to variability in its overall growth.

- Inability to compete effectively in the online space - B&M’s strategy is to drive footfall to its stores. The risk is that online retailers will continue to take market share, contributing to a decline in its growth trajectory. We feel its value proposition currently is sufficient to offset this.

Final thoughts

B&M is a high-quality business in our view, which is rare in the retail industry. The affordable retail segment in the UK is less developed than in the US when it comes to a variety retailer (far more fragmented). B&M offers everything at an attractive cost-to-quality ratio, which has allowed it to grow incredibly well.

We believe its business model is defensible, owing to its scale across the UK, which it is committed to expanding. When we compare the company to other broadline retailers, it performs exceptionally well.

Although its valuation does not glaringly imply a significant upside, we see attractive returns and good growth ahead. At an FCF yield of 6%, we consider the stock a buy.

For further details see:

B&M European Value Retail: Discount Retailer Dominating Its Market