RILYP - B. Riley Baby Bonds: Up To 12% Yield Plus Large Potential Price Increases

Summary

- We believe that the prices of the longer-term B. Riley Financial, Inc. baby bonds make them quite undervalued.

- These bonds are not only relative bargains in comparison to shorter-term B. Riley Financial baby bonds, but are also extraordinarily undervalued relative to B. Riley preferred stocks.

- We view this as an excellent opportunity to lock in double-digit yields to maturity, and with prices in the teens, these baby bonds also offer potentially large capital gains.

Introduction

In the current market, the volatility and illiquidity have created many mis-pricings and opportunities to purchase very undervalued securities. We do a lot of analytical work at Conservative Income Portfolio to identify the sweet spots in the market as well as relatively undervalued individual securities across all sectors and all fixed-income asset classes.

Currently, our work shows that the sweet spot in fixed-income is in the bond sector with maturities ranging from 2027 to 2029. Bonds in this maturity range offer the best yields as well as being short term enough to hold up better in price than preferred stocks or longer term bonds should interest rates continue to rise. I may do an article on how we determined this sweet spot sometime in the future.

{kind=link}

B. Riley Financial, Inc. ( RILY ) is a financial company with a diverse set of businesses. Here is what Yahoo Finance has to say:

B. Riley Financial, Inc., through its subsidiaries, provides investment banking and financial services to corporate, institutional, and high net worth clients in North America, Australia, and Europe. The company operates in six segments: Capital Markets, Wealth Management, Auction and Liquidation, Financial Consulting, Principal Investments Communications, and Brands. The Capital Markets segments offers investment banking, corporate finance, financial advisory, research, securities lending and sales, and trading services; merger and acquisitions, restructuring advisory, initial and secondary public offerings, and institutional private placements services; asset management services; and trades in equity securities. The Wealth Management segment provides wealth management and tax services. The Auction and Liquidation Segment offers retail store liquidation, and wholesale and industrial assets disposition services. The Financial Consulting segment provides bankruptcy, forensic accounting, litigation support, operations management and real estate consulting, and valuation and appraisal services.

Safety

The fact that RILY has a diverse set of businesses helps provide stability and safety. In fact, some of their businesses actually should thrive in bad markets, helping offset the investment banking sector which can struggle during economic and market turbulence. Those businesses that do well in bad times are their auction business, liquidation business, and consulting and restructuring businesses.

In fact, we saw this in the third quarter that just finished. RILY’s stock and bond underwriting businesses is a very important business for them, yet during the third quarter, there were very few IPOs. Yet despite this, RILY reported an excellent quarter earning $1.53 per share.

And what makes this earnings report great is that RILY also holds a significant number of investments in the common stocks of publicly traded companies. Since the third quarter was so terrible for stocks and bonds, one would have thought that RILY would have reported a large loss on their investments. But surprisingly, they actually had gains in their investment portfolio. That is quite an accomplishment.

Over the years, RILY has proven itself to have great investment prowess and an eye for buying undervalued businesses. And common stock investors have experienced huge gains in RILY common stock over the years.

10 Year Price Chart of RILY

{kind=link}

As you can see, RILY is up 750% in the 10 years since Bryant Riley started managing RILY. And it would have been up even more, but the company has paid out very large special dividends which partly account for the more recent price slide.

As the chart shows, RILY has crushed the blue chip investment banks like Goldman Sachs ( GS ), JP Morgan ( JPM ), and Morgan Stanley ( MS ). Like most investment banks, RILY’s balance sheet does carry leverage, however, it keeps itself quite liquid with its cash holdings plus its portfolio of publicly traded companies.

RILY Baby Bonds

Author

Two things stand out in the above chart, which is ordered by maturity date. The RILYN ( RILYN ) baby bond looks like a super value relative to the other 2026 baby bonds, RILYK ( RILYK ) and RILYG ( RILYG ). If you own RILYG or RILYK, it is a no brainer to sell RILYK and RILYG and purchase RILYN.

The other thing to note is what a huge difference there is in yield between RILYO and RILYZ despite only 4 years difference in their maturity dates. Whereas 1 year ago, there was not much difference in yield to maturity ((YTM)) between RILYZ and RILYO, now the difference is enormous. I consider this a historic mispricing as this kind of yield difference between bonds with a 4 year difference in maturity is something I haven’t seen before. This looks like a great opportunity, and when pricing normalizes in the market, I expect RILYZ and RILYT is where you want to be.

Whereas one year ago, when the Fed started tightening, I recommended staying short term, and RILYO was a mainstay core holding for me. And as you can see, it still trades fairly close to par. But times have changed, as you can see from the chart below.

{kind=link}

As you can see, RILYZ ( RILYZ ) and RILYT ( RILYT ) have had huge selloffs relative to the other RILY baby bonds, and this is where the price upside is now. Not only do you have very large YTMs of 11.8% and 12%, but these bonds should rocket higher in price should the market turn, and even a simply more rational pricing structure, without a market turn, should take RILYZ and RILYT higher.

Thus, my recommendation is to sell RILYO, RILYG and RILYK and look to buy RILYN, RILYT and RILYZ. It is hard to imagine that RILYZ IPO’d at a 5.25% YTM last year and now has a 12% YTM. That just seems way overdone and hard for me to understand, even in this bear market.

It is my feeling that the largest risks we have in the market are going to occur over the next 12 months. These include war risk, inflation risk, recession risk and the risk that Fed tightening breaks something in the financial system. Thus, for me, owning a 2025 bond, for example, doesn’t make me feel more secure than owning a 2028 bond. And yet you are rewarded handsomely for adding a little more duration to your portfolio – I would say you are getting much more reward than the added risk when you go out 3 or 4 years longer in maturity.

RILYZ, RILYN and RILYT Are Extraordinary Values Relative to RILY Preferred Stocks

So not only does the YTM spread between RILYO/RILYG/RILYK and RILYZ/RILYT/RILYN support the thesis of a large relative undervaluation for RILYN, RILYT and RILYZ, the comparison of the yield on RILY preferred stocks relative to these baby bonds really drives this thesis home.

Author

This shows some of the current pricing madness that we have in the current market. How can anyone choose to buy preferred stock RILYL, and even RILYP, over RILYZ. RILYL preferred stock has virtually no price upside and a puny 7.44% yield compared to baby bond RILYZ with a 12% YTM and lots of price upside with its current price of $18.60. The relative undervaluation of RILYZ is just enormous here. And even RILYP’s current yield doesn’t come close to competing with RILYZ. How can the RILYZ bond, a safer security than the preferred stocks, have such a higher yield and price upside compared to the preferred stocks of the same company? I can’t answer that. I can only suggest that people act logically in their investments and take advantage of completely illogical pricing.

Thus, I recommend a swap out of the RILY preferred stocks and into RILYN, RILYT or RILYZ.

RILYL is a very strong sell here.

Excellent Entry Point For RILY Baby Bonds

I have found that you get excellent entry points for fixed-income securities not only when they are relatively cheap, but also when they have lagged the market and/or lagged their common stock. Here we can see what has happened over the last month.

{kind=link}

The drop of from 7% to 10% in the RILY bonds that look best is quite a large drop for preferred stocks over a 1 month period. One would think that either interest rates jumped a lot or there was some issue with RILY. Here we can see that this large drop in the price of the RILY bonds surprisingly coincides with a large price increase in RILY common stock and RILY baby bonds also dropped significantly more in price than the long bond ETF ( TLT ). Thus, there was no fundamental reason for the large drop over the last month in the price of RILYZ. This just adds to the attractiveness of RILY baby bonds and bolsters the undervaluation thesis.

{kind=link}

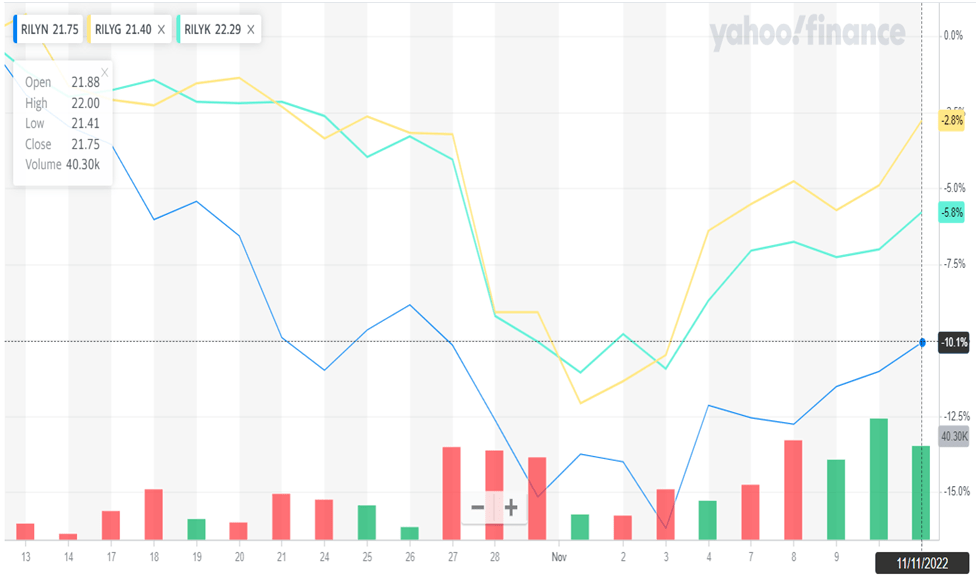

Above is a one month price chart of the 3 RILY baby bonds that mature in 2026. As you can see, RILYN got smacked much harder than the other 2 bonds, and there is no logical reason for that. And we saw in an earlier chart that RILYN has a much higher YTM than the other 2 2026 bonds. RILYN looks to be a strong bargain here.

Summary

RILY has proven itself to be a very well-run company, with its common stock up 750% over the last 10 years. Yet its baby bonds sell at YTM’s up to 12%. RILYZ, with its 12% YTM, IPO’d just last year with a 5.25%. The selling in RILYZ just seems extremely overdone to me and at a price in the teens, also has a lot of capital gains potential over the coming year.

The large drop in price of RILY baby bonds over the last month is totally disconnected from the performance of RILY common stock and what has happened with interest rates. This smacks of a buying opportunity.

As we saw from the above chart, RILYN, with its 2026 maturity, looks very undervalued versus RILY’s 2 other 2026 bonds. Additionally, the huge spread in yield between the 2024 RILYO bond and 2028 RILYZ and RILYT bonds is historically ridiculously wide.

Lastly, RILYZ and RILYT bonds are extraordinarily undervalued relative to the RILY preferred stocks. While preferred stocks carry more risk, have no maturity date, and can have dividends suspended, the 2 RILY preferred stocks, RILYL and RILYP, have current yields that average only a bit above 8% versus a 12% YTM for RILYZ. I have never seen such crazy pricing with the securities of the same company with maybe one exception.

Bottom line, we recommend the purchase of RILYZ, RILYT and/or RILYN, and if you own RILYP, RILYO, RILYG and/or RILYK, we recommend selling. And a very strong sell on RILYL.

For further details see:

B. Riley Baby Bonds: Up To 12% Yield Plus Large Potential Price Increases