BACHF - Bank of China: Sluggish Economy Creates Significant Uncertainty

2023-09-26 12:11:46 ET

Summary

- Bank of China is one of the largest state-owned banks in China, providing banking and financial services globally. Its recent performance has been solid, with profit and EPS growth.

- The outlook for BOC in 2023 and beyond depends on the state of the Chinese economy, but the bank is focusing on strengthening its core pillars and supporting government policies.

- I believe Bank of China is currently overvalued by c. 4.8%. While it has a safe monster yield of 9.5%, more weakness might lie ahead regarding its share price.

- I have a long position in BOC but advise potential investors to be patient and wait for a better entry point, giving the Chinese economy time to get back on its feet.

Bank of China ( BACHF ) ( BACHY ) is one of the largest state-owned banks in China which provides banking and financial services in Mainland China and internationally. According to Forbes , BOC provides the following banking and financial services: "Corporate Banking, Personal Banking, Treasury Operations, Investment Banking, Insurance, and Others. The company was founded on February 5, 1912, and is headquartered in Beijing, China". It operates in over 62 countries globally.

In this article, I present my view on BOC post Q3 2023 earnings. I also present an outlook for the remainder of 2023 and beyond.

In preview, I believe the Bank of China is currently overvalued by c. 4.8%. While it has a safe monster yield of 9.5%, more weakness might lie ahead regarding its share price due to the uncertain and challenging macro environment. I advise potential investors to be patient and wait for a better entry point, giving the Chinese economy time to get back on its feet.

Overview of Bank of China's recent performance

The global banking sector has been facing some turmoil first during the pandemic, and now post-COVID with rising interest rates, sticky inflation and a possible recession are now persistent problems on the horizon. In China, we can add to this list of challenges the government's crackdown on the heavily indebted property sector causing major upheaval. Luckily, however, the impact of the property sector on BOC is relatively minimal.

Despite all this turmoil, BOC has been growing its profit and EPS YoY for the past several years.

Profit for the Year - 2022 (BOC Annual Report 2022) EPS (basic) 2022 (BOC Annual Report 2022)

What's interesting, however, is that none of this performance has translated into its share price.

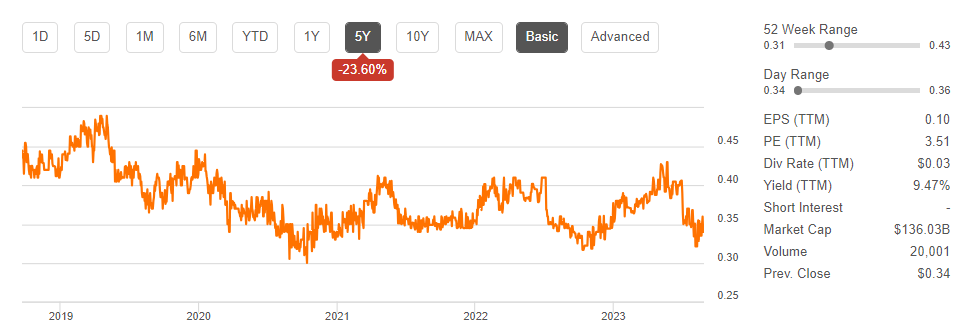

5-year Share Price (Seeking Alpha)

{kind=link}

As can be seen from the share price summary of Seeking Alpha, in the past 5 years, BOC is down -23.6%, despite weathering several major storms and a continued improvement in Net Profit and EPS.

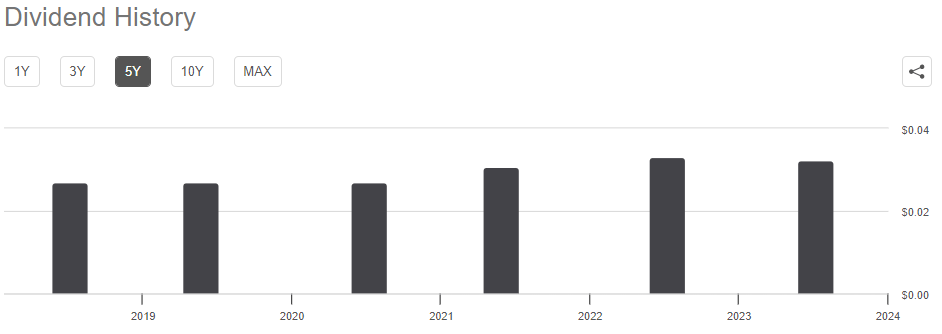

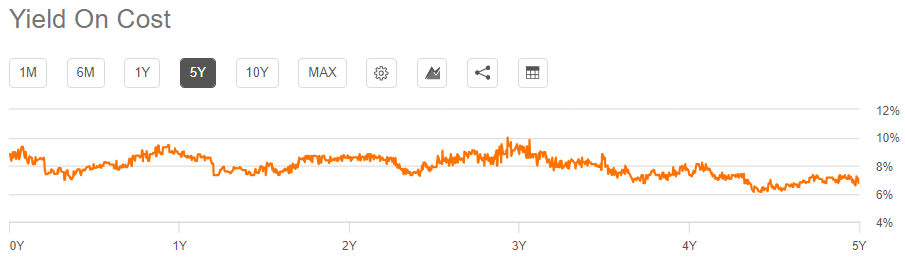

5-year Dividend History (Seeking Alpha) Yield On Cost (Seeking Alpha)

{kind=link}

{kind=link}

As the dividend history and Yield on Cost charts show, dividend cuts also do not explain this underperformance. BOC has had a monster year-end yield of between 6.4% and 16.3% over the 5-year period. I also checked the shares outstanding to see if there was significant equity dilution (which there was not) as shares outstanding remain virtually unchanged over the past 5 years.

2023 Q3 Interim Results

In the earnings call on August 30th, Management broke up their performance summary into four parts:

- Financial Efficiency: Operating income grew 8.92% YoY, reaching RMB 319.7bn (US$46.3bn), net interest income grew 4.75% to RMB 234bn (US$33.9bn), net fee income increased 4.34% to RMB 46.4bn (US$6.7bn). Profit after tax amounted to RMB 128 bn (US$18.5bn), growing 3.4% YoY.

- Earnings Efficiency: Net Interest Margin decreased from 1.76% in 1H 2022 to 1.67%, caused by a drop in interest rates of domestic RMB denominated loans, driven by Government requests for the big Chinese banks to 'support the development of the real economy' (more on this later).

- Assets & Liabilities: BOC's assets grew by 7.59% YoY, outpaced by loan growth of 9.75% YoY. Deposits also grew 11.13%. As stated by the President of BOC during the earnings call, RMB deposits and loans reached record highs.

- Risk Resilience: There was also an improvement in BOC's 'risk resilience'. A key metric for banks, the 'non-performing loan ratio' decreased to 1.28%, while its other key metric the 'provision coverage ratio' reached 188.39%. Last, BOC's CAR (capital adequacy ratio) reached 17.13%, which is considered a safe level.

Overall, I would call their YTD results solid. These results should be interpreted in the context of the wider Chinese economy, which after a brief growth spurt post-COVID 'reopening' at the beginning of the year has seen a steady deterioration of all major economic indicators. As such, I believe BOC has done very well in a challenging macro environment.

Outlook - 2023FY and beyond

The outlook for 2023FY I believe is more of the same as the one seen in the 1H. Looking beyond that will require taking a view on the state of the Chinese economy, which is hard to predict. The government is trying to move its economy from a (government) investment-led economy to a domestic consumption economy. The goal is for individuals and households to save less and spend more. Challenges in the healthcare and pension provisions make this difficult to achieve. That said, I do believe in the long term, once the Chinese government sets their mind to something, they will achieve it.

For BOC, I thus believe most important is to make sure they are doing all the right things to benefit once the macro and political environment improve.

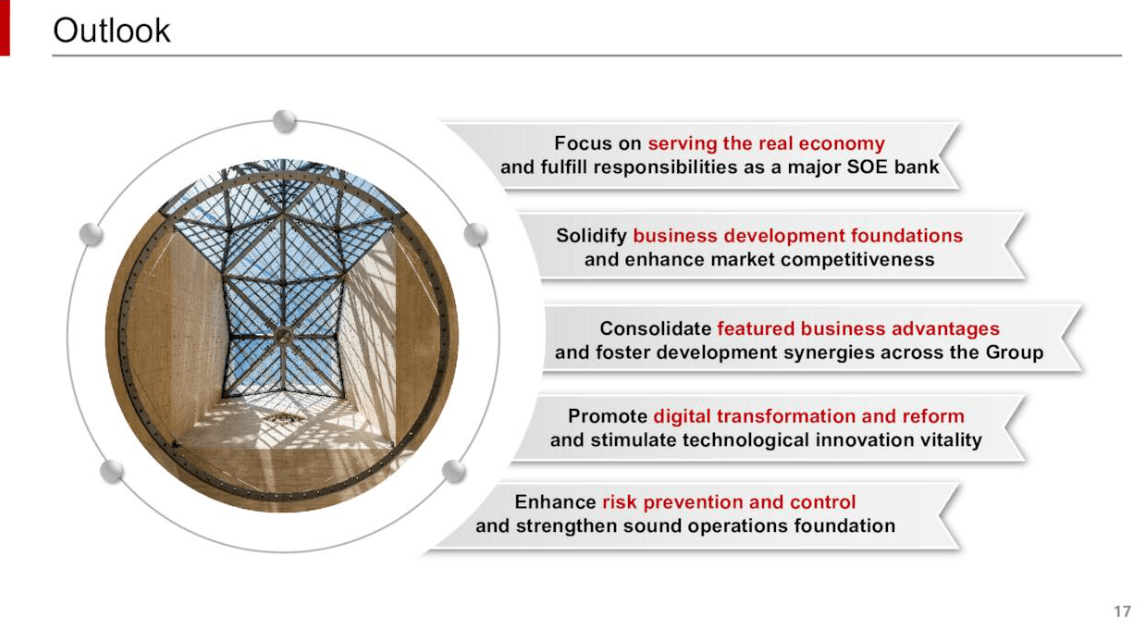

Looking ahead, BOC is focusing on a few key priorities:

- 'Supporting the real economy' : As one of the largest state-owned banks, BOC is an extension of the government and a tool they can use to impact and implement monetary policy. This is very different from retail and commercial banks in the West. To stimulate the sluggish economy, BOC has been directed by the state to provide financing at lower rates than they might otherwise offer to support key areas of the Chinese economy. Examples of these areas include Construction, Manufacturing, Industrial, 'Energy Transition, Tech & Innovation and SMEs, as well as driving the 'common prosperity' agenda outside major cities.

- BOC is working on strengthening their core pillars, including improving its assets, liabilities, loans, and deposits and improving key risk indicators as stated in their most recent results announcement.

- Related to their core is their ongoing digital transformation , which aims to drive efficiency and enhance customer services.

- In addition to its core, there are several key regions and projects where BOC is seeking to support state goals, including the ' Belt and Road ' initiative and the Greater Bay Area in Southern China.

Outlook (Bank of China Q3 Results Presentation)

{kind=link}

Overall, I believe BOC is doing the right things and that its efforts are not being recognized in its share price. I hope to see these goals paying off in continued profit growth, and hopefully some dividend hikes going forward. I believe the recent poor performance is more the result of the Chinese and the Global economy, and that fundamentally BOC is moving in the right direction. As an investor investing in state-owned enterprises, you cannot avoid policy interventions, and it is clear BOC is investing heavily in supporting government policies. One good thing about state ownership is that the dividend is likely extremely safe.

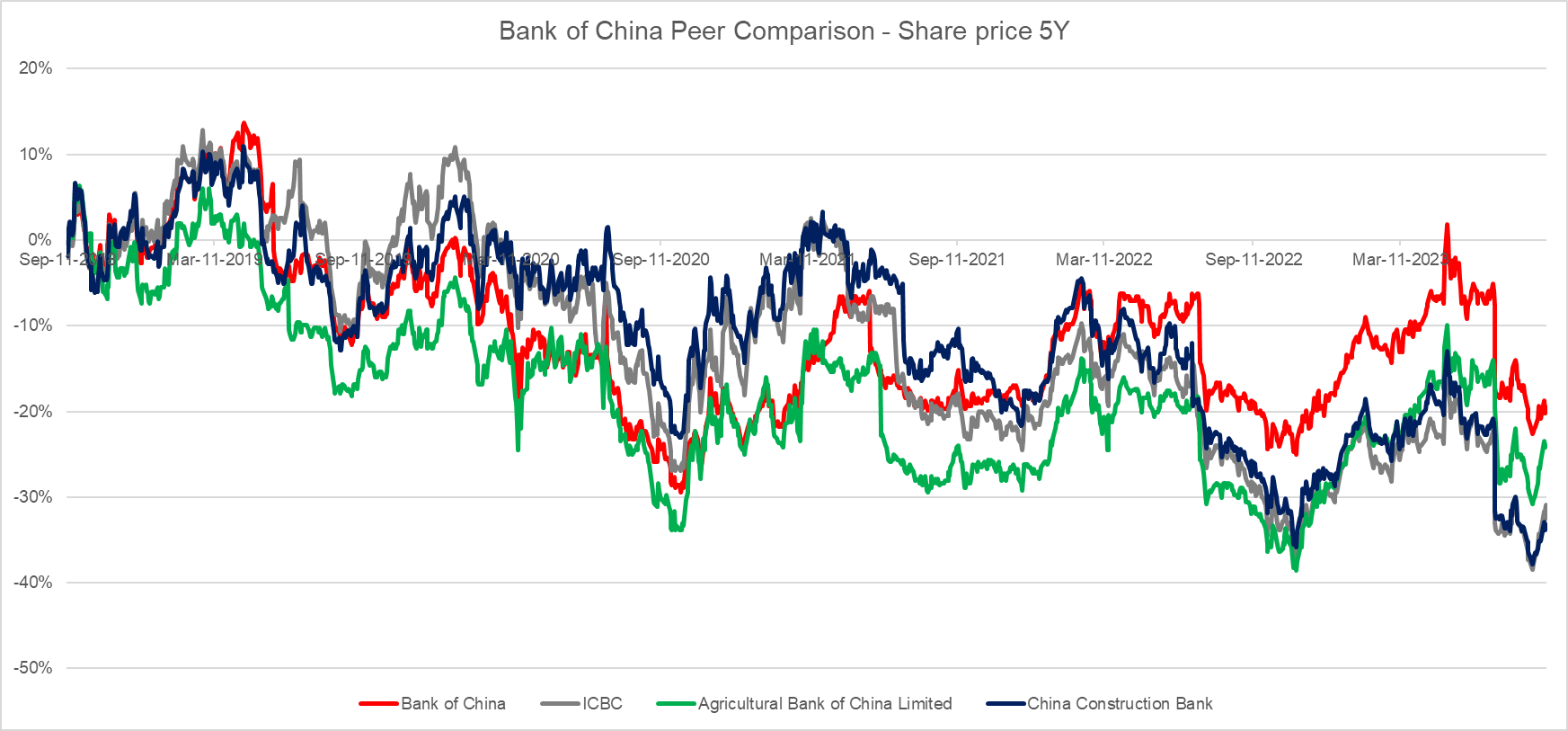

Peer Comparison

Taking a broader view of the competitive landscape, I did a comparison between BOC's share price performance over the past 5 years and that of some of its major peers.

5-Year Share Price - Peer Comparison (Capital IQ)

{kind=link}

As can be seen above, the market has not been kind to any of the major Chinese banks over the past 5 years, but relatively, BOC has fared slightly better than others.

Valuation Multiple Comparison (Capital IQ & Respective Recent Results Presentations)

{kind=link}

Taking a look at relative valuation, BOC is relatively fairly valued compared to its major peers, while its NPL ratio is better overall. To me this signals that there is no cause for concern on a relative basis.

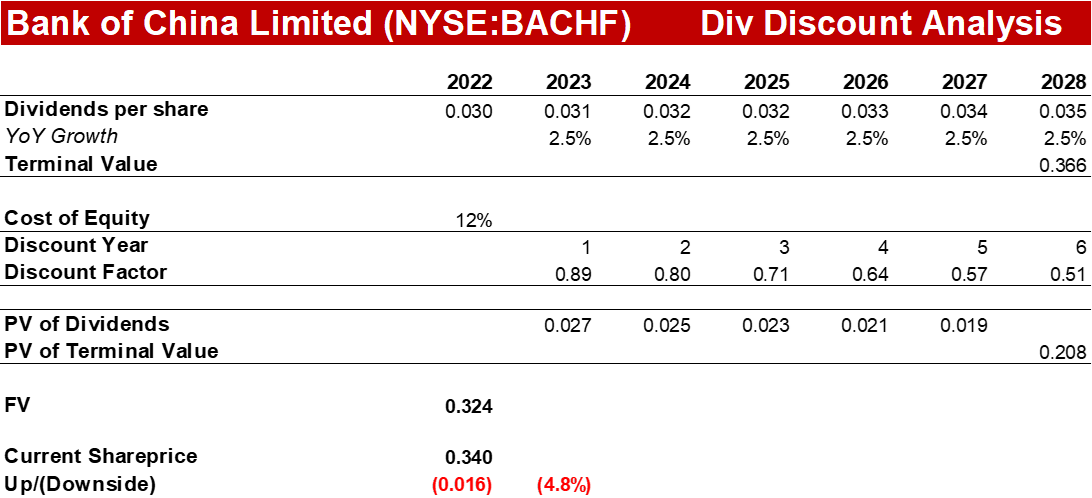

Valuation - Dividend Discount Model

While valuing banks is tough, I believe it makes most sense to value BOC using a Dividend Discount model, since the main reason to invest in this stock is its high yield and dividend stability.

Dividend Discount Analysis - BOC (Author's Calculations)

{kind=link}

As can be seen above, based on a 12% cost of equity (from Capital IQ ), I believe BOC is currently trading overvalued by 4.8%. I used a 2.5% YoY growth rate for the dividend as this is the 10-year average from 2012-2022. As such I rate BOC as a 'Hold'. If I did not already own shares in BOC, I would wait and see how the macro environment, especially in China, develops before buying any shares. Since I already own shares in BOC, I will look for further corrections (5-10% drops) before adding more. As BOC only pays dividends once a year in July / August, any potential dividend hikes will not be announced until next year. By then there will be more information on how things develop in China, and if any dividend increases are forthcoming. That could make the stock a potential 'Buy' for me.

Risk and Downsides

The main risks for BOC are two-fold:

- General 'China Risk' - as a state-owned bank, BOC will have to support policy objectives that might not be in the financial best interest of non-governmental shareholders. This risk is hard to quantify, and I believe one just must be comfortable with it in order to invest in any major Chinese company.

- China's economic environment - this risk I see is no different from the macroeconomic risk in the US, Europe or globally. As we cannot predict what will happen, a major recession either in China, Asia or globally will likely have significant implications. To mitigate this risk, I would advise any potential investors not to place big bets, but rather place smaller bets and average down your costs over time. Especially for BOC, I think there is no rush as the dividend only comes once a year.

Takeaway

I believe Bank of China is currently trading 7.4% above its fair value based on a Dividend Discount analysis. BOC performs in line, and arguably slightly better than its major peers, and on a relative basis is fairly valued. While BOC offers a safe and incredible yield of 9.5%, due to the uncertain economic environment in China and globally, more weakness might lie ahead regarding its share price. I advise potential investors to be patient and wait for a better entry point, giving the Chinese economy time to get back on its feet.

I plan to start adding to my position around $0.3 per share.

Note on investing in this stock: While BOC trades at $0.34 per share at the time of writing, the minimum stock lot is 1,000 shares, so a minimum purchase value would be $340 at current prices.

For further details see:

Bank of China: Sluggish Economy Creates Significant Uncertainty