BSVN - Bank7: A Growth Bank Stock

2023-05-03 10:53:23 ET

Summary

- Bank7's 2023 Q1 EPS of $1.04 set a quarterly earnings record for the company.

- I expect 2023 EPS to be in the mid $4 range, which would lead to the stock price being fairly valued around $30. This represents over 30% upside from today.

- Uninsured deposits are at safe levels as are the bank's capital ratios, which are well in excess of regulatory requirements.

- Historical EPS growth has been around 20%, challenging rates of return of many growth stocks. The forward dividend yield is 2.6%.

- There are many risks involved in owning a bank stock, particularly at a time where bank solvency is back in the focus of regulators.

Bank7 (BSVN) is a full-service regional bank headquartered in Oklahoma, with twelve branches in total across Oklahoma, Texas, and Kansas. The bank primarily makes loans for commercial uses in the following four categories: (i) commercial real estate (ii) hospitality (iii) energy, and (iv) industrial. Although the company does make personal loans, those funds represent a small portion of the overall loan book.

A Growth Bank Stock?

One of the things which makes Bank7 such an attractive investment is the growth of the company's bottom line. The company's 2019 EPS was $1.96 and analysts expect 2023 EPS to be $3.84. This represents a CAGR of 18%, which is a strong level of growth for a regional bank with only twelve branches.

However, I believe the analysts are wrong; I expect this stock to earn $4.67 for FY 2023. Over FY 2022, the company's sequential QoQ EPS increased at a CAGR of 8%. Simply extrapolating this growth rate for 2023 EPS will leave us with the following schedule:

Q1 (announced): $1.04

Q2 (expected): $1.12

Q3 (expected): $1.21

Q4 (expected): $1.30

2023 EPS (expected): $4.67

Let's adjust downwards for a margin of safety. This is an arbitrary number, but let's assume the company does 20% worse than expected. The 2023 EPS would still be $4.20. This represents a CAGR of 21% instead of 18%, again proving this is a tiny powerhouse of a regional bank.

What is the Primary Driver of this Growth?

Banks must lend out money to earn a return in excess of what it cost to acquire those funds. Therefore, profitability is dependent on core deposits growing. Otherwise, profits remain stagnant as there is no additional capital to earn a return on and as a result, the bank would be forced to make riskier loans to earn a higher rate of interest on the funds it already possesses. In the case of banks, it is counterintuitive that the growth of liabilities (deposits) increases profit.

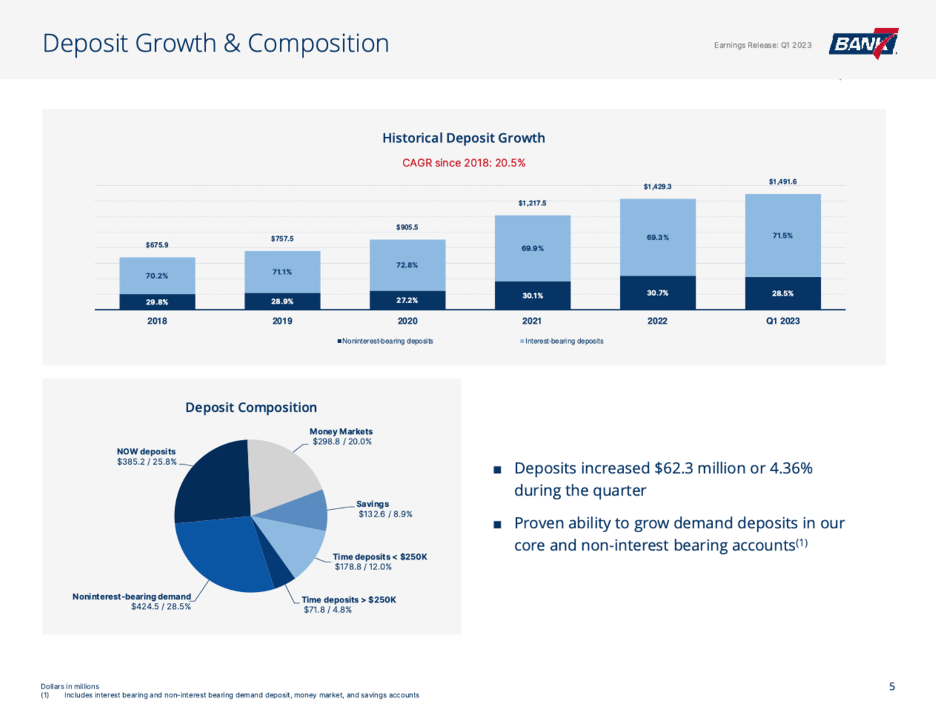

Deposit Growth (Bank7 Q1 2023 Presentation)

{kind=link}

Bank7 has grown its deposits by almost 21% since 2018 and over 4% this past quarter. The latter achievement is particularly notable given that many banks at the moment are facing degrees of runs as woes concerning solvency mount.

Note: In December 2021, Bank7 acquired Cornerstone Bank which increased deposits by about 20% at that time from $1B to $1.2B.

Bank7's Loan Book

A bank's future is only as good its loan book. Over 98% of Bank7's loan book is for commercial purposes, while less than 2% is for personal loans. I personally avoid banks which primarily make personal, unsecured loans. These are the riskiest banks in a rising interest rate environment as consumers default on their loans and the banks have no collateral to hedge this risk.

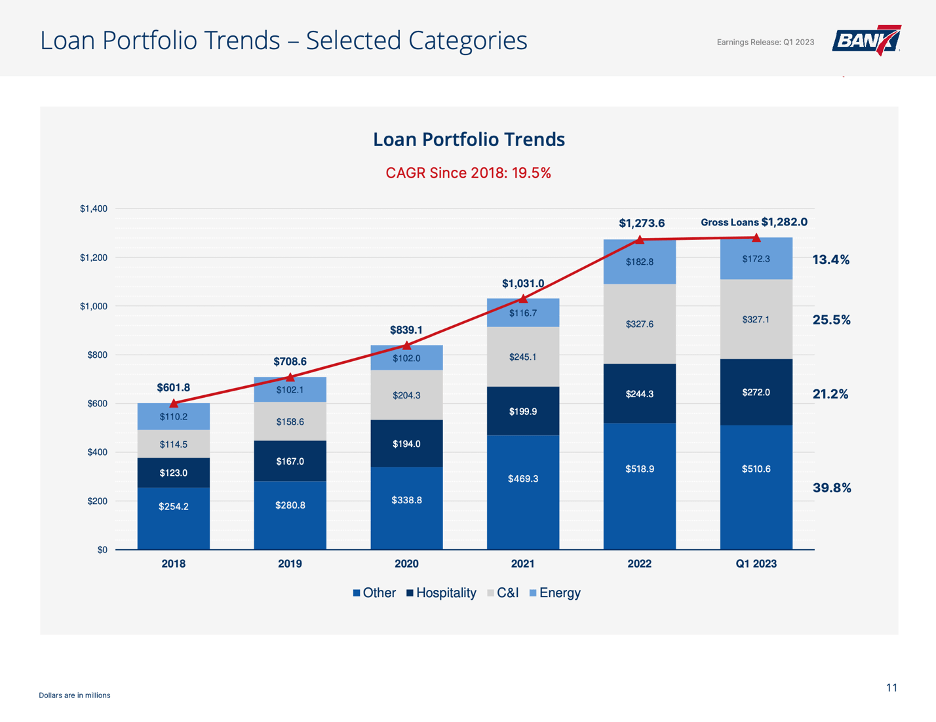

Types of Loans

Below is an excellent table representing the types of loans Bank7 currently has and how each category's proportion has changed over time. The 'other' category primarily reflects commercial real estate loans in various industries.

The first thing to note is loans have steadily increased over time. The big jump from 2021 to 2022 was primarily the result of Bank7 acquiring Cornerstone Bank and its loan book. You will also notice the proportions have not shifted much over time other than to capitalize on certain macro-factors such as rising oil prices in recency (more loans directed to energy companies as the bank will earn a higher rate in an inflationary environment which favors oil producers).

Loan Portfolio Trends (Bank7 Q1 2023 Presentation)

{kind=link}

Loans Gone Bad

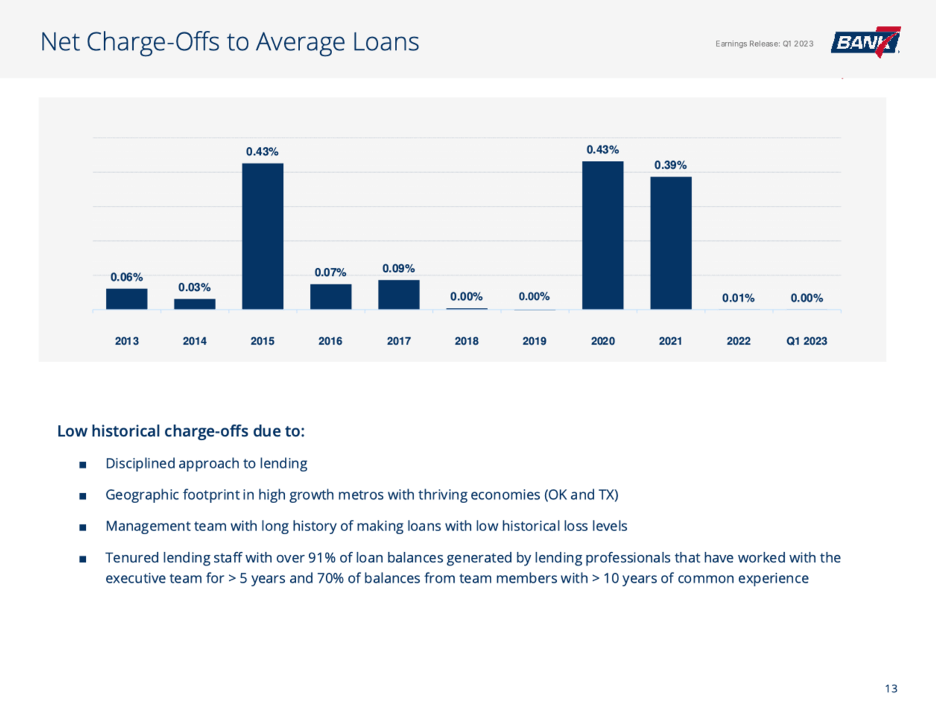

As evidenced from earlier, Bank7's deposits and loans are increasing, but none of that matters if the borrowers are not credit-worthy. In the below table, we can see that for ten straight years the company had negligible to no charge offs each year. Even in 2020 when small businesses were being eviscerated by the day, the bank's loan book was rock solid. The management team clearly practices prudent lending. The quality of borrowers is high since their credit risk is low.

Net Charge Offs (Bank7 Q1 2023 Presentation)

{kind=link}

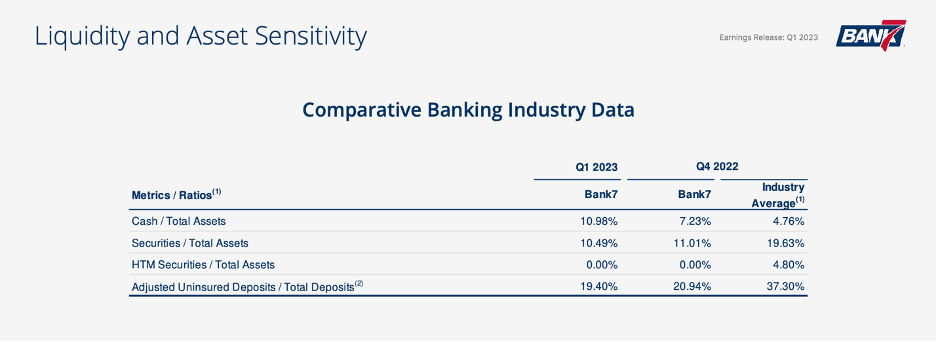

Uninsured Deposits

The FDIC guarantees individual accounts at certain banks up to $250,000. Amounts deposited in excess of this amount are considered "uninsured" meaning the individuals' capital is at risk should the bank become insolvent. As a result, many depositors yank their uninsured deposits if they sense there are financial problems at their bank. If a bank bleeds its deposits, it will not survive long.

Uninsured Deposits (Bank7 Q1 2023 Presentation)

{kind=link}

The most recent example is First Republic Bank, which had a ratio of uninsured to insured deposits of about 67% and a 111% loan to deposit ratio. In contrast, Bank7's uninsured ratio is 20% (the industry average is 37%) and its loan to deposit ratio is 86%.

Note: Bank7's ratio of 20% is actually adjusted for collateralized uninsured deposits and insider uninsured deposits. Adjusting insider uninsured deposits is misleading (insiders can and will flee if they need to) so realistically the bank's uninsured rate is 24%, which is still better relative to peers.

Valuation

Typically, large banks are pegged to a fair value 12 P/E and regional banks to a 10 P/E. Considering the turmoil in the banking sector, investor sentiment has changed. As a result, I would expect a reduction in the multiple investors are willing to pay for a bank stock. In other words, I would expect large banks to trade at an 8-10 P/E and regional banks even lower at a 6-8 P/E.

Therefore, if Bank7 earns $4.20 per share in 2023, then its fair value stock price could potentially be in the range of $25 to $34 per share.

Bank7 currently trades at $23 per share. If we take the midpoint of our range (~$30/share), then there is potential to make a capital gain of over 30%.

Bullish Fast Facts

- Record quarterly EPS of $1.04 achieved this past quarter (14% increase vs. Q4 2022)

- Industry leading efficiency ratio of 36.6% (due to the branch lite model)

- NIM consistently over 5% vs industry average 3.5%

- 2023 shares outstanding (9.2MM) reduced by over 10% verse IPO

- Tangible book value of $15.75/share (grown at a CAGR of almost 16% since inception)

- Forward dividend of 2.6% and total dividend increased by 56% compared to three years ago

- Insiders own 58% of shares

Bank7's branch lite model and quality assessment of borrower credit risk has enabled the bank to earn quite a few outstanding achievements. Industry leading performance has been a consistent theme over the years. For example, in 2020 the company declared its very first dividend… in the middle of the pandemic crash. The company was in rock solid shape while other businesses were having major solvency issues due to mal-investments. We see a similar outcome today as the company just posted record EPS in an environment where regional banks are posting abysmal results.

In both cases, I benefited greatly as a shareholder amidst a lot of others suffering and it was a result of Bank7's management team being prudent.

As Warren Buffet once famously said,

Only when the tide goes out do you see who has been swimming naked.

Risks

There are a number of risks to keep in mind when considering an investment in Bank7.

Interest Rate Risk

An increase in interest rates cause borrowing to become expensive and thus, can lead to an increase in defaults.

My thoughts : Bank7 primarily makes loans for commercial purposes which are safer when compared to unsecured personal debt. Of course, commercial loans are not immune to risk as borrowers' default in recessions as well. However, risk is on a scale and I would rather own a bank making calculated loans to commercial borrowers than calculated loans to personal borrowers. Another thing to keep in mind is the bank's loans have shorter durations, which mathematically is less sensitive to changes interest rates in the event the value of the loan needed to be sold.

Recession Risk

A recession could materially impact charge offs and cause profitability to suffer.

My thoughts : Historically, Bank7's net charge offs each year are negligible (0% to 0.50%) and until management proves otherwise, it appears they do a good job assessing credit risk.

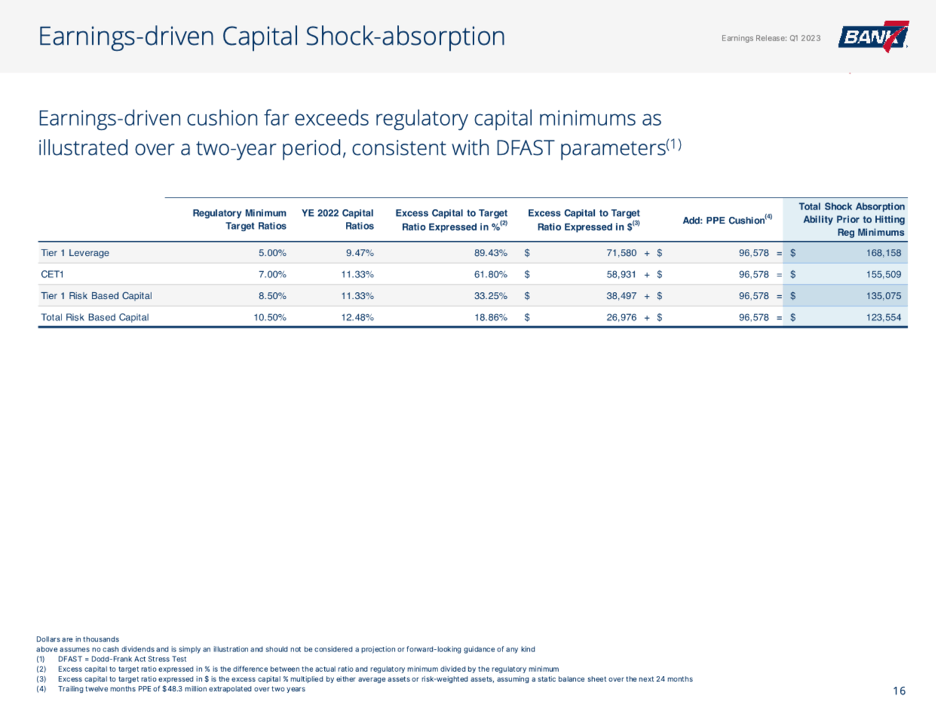

Regulatory Risk

Capital Ratios (Bank7 Q1 2023 Presentation)

{kind=link}

With the recent banking crisis, it is likely only a matter of time before Congress passes additional regulations involving regional banks.

My thoughts : Bank7 is well capitalized with plenty of cash and no debt. The company's capital levels far exceed regulatory minimums and should handle anything Congress potentially throws at the industry (within reason).

Geographically Concentrated

Bank7 does its business with clients in Oklahoma, Texas, and Kansas. Given their loan book is concentrated in these areas, any negative shock affecting one or more of these states could lead to a substantial decrease in profitability.

My thoughts : This is a double-edged sword as it is smart the company is focusing on its area of expertise, but it is risky to be confined to a small area. It has not proven to be an issue, but investors should keep this in mind.

For the company's set of risks, please click here and go to page twelve.

Takeaway

Bank7 had another outstanding quarter as one of the industry leading regional banks. I believe the stock is undervalued by over 30% at the moment. There are many risks involved in buying an individual stock and those specific to a bank stock. I commented on some, but please keep in mind there are many additional risks.

For investors looking for an opportunity to buy into the banking sector during uncertain times for the best price, Bank7 is a must consider stock. It's double-digit EPS growth rate offers the qualities found in a growth stock, while it's consistently increasing and well covered dividend provides qualities found in income producing stocks.

For further details see:

Bank7: A Growth Bank Stock