ACGLN - Baron Focused Growth Fund

2023-08-16 21:12:00 ET

Summary

- Baron is an asset management firm focused on delivering growth equity investment solutions known for a long-term, fundamental, active approach to growth investing.

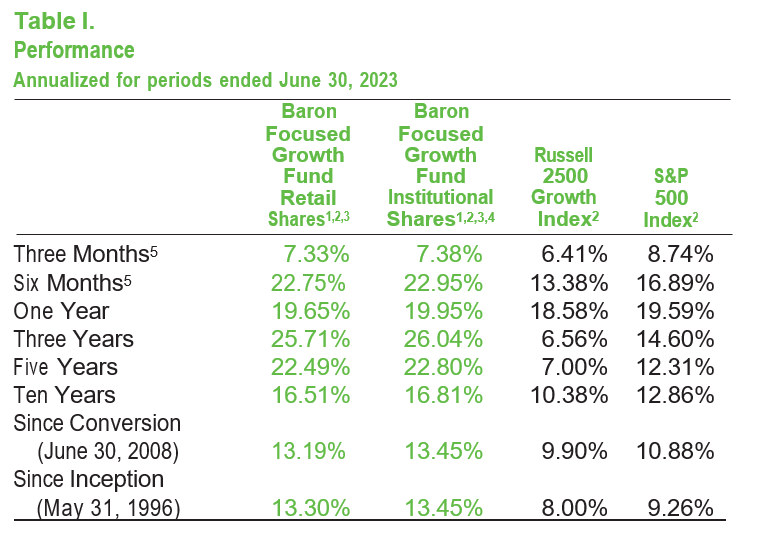

- Since its inception over 27 years ago, the Baron Focused Growth Fund has increased 13.45% annualized versus an 8.00% annualized return for the Russell 2500 Growth Index and a 9.26% annualized return for the S&P 500 Index.

- The Fund’s strong performance in the second quarter was principally due to what we call our Core Growth and Disruptive Growth companies, which include CoStar Group, Inc. in Core Growth and Tesla, Inc. and FIGS, Inc. in Disruptive Growth.

Performance

Baron Focused Growth Fund® (the Fund) performed well in the second quarter of 2023. This was despite continued investor concerns regarding consumer spending and enterprise capital investment due to high interest rates and elevated inflation. The Fund increased 7.38% (Institutional Shares) in the quarter. The Fund's primary benchmark, the Russell 2500 Growth Index (the Index), increased 6.41% in the period. The S&P 500 Index, which measures the performance of domestic large-cap companies, increased 8.74%.

The Fund has outperformed the Index for 1-, 3-, 5-, and 10-year periods, as well as since its inception as a private partnership on May 31, 1996. Since its inception over 27 years ago, the Fund has increased 13.45% annualized. This compares to an 8.00% annualized return for the Index and a 9.26% annualized return for the S&P 500 Index.

{kind=link}

Performance listed in the above table is net of annual operating expenses. Annual expense ratio for the Retail Shares and Institutional Shares as of December 31, 2022, was 1.32% and 1.06%, respectively. The performance data quoted represents past performance. Past performance is no guarantee of future results. The investment return and principal value of an investment will fluctuate; an investor's shares, when redeemed, may be worth more or less than their original cost. The Adviser may reimburse certain Fund expenses pursuant to a contract expiring on August 29, 2033, unless renewed for another 11-year term and the Fund's transfer agency expenses may be reduced by expense offsets from an unaffiliated transfer agent, without which performance would have been lower. Current performance may be lower or higher than the performance data quoted. For performance information current to the most recent month end, visit Baron Funds - Asset Management for Growth Equity Investments or call 1-800-99BARON.

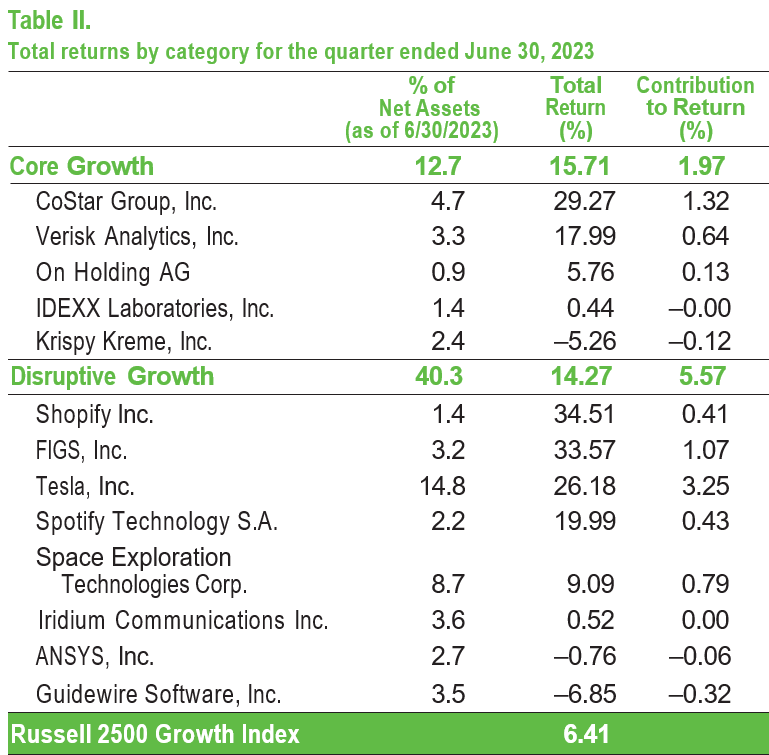

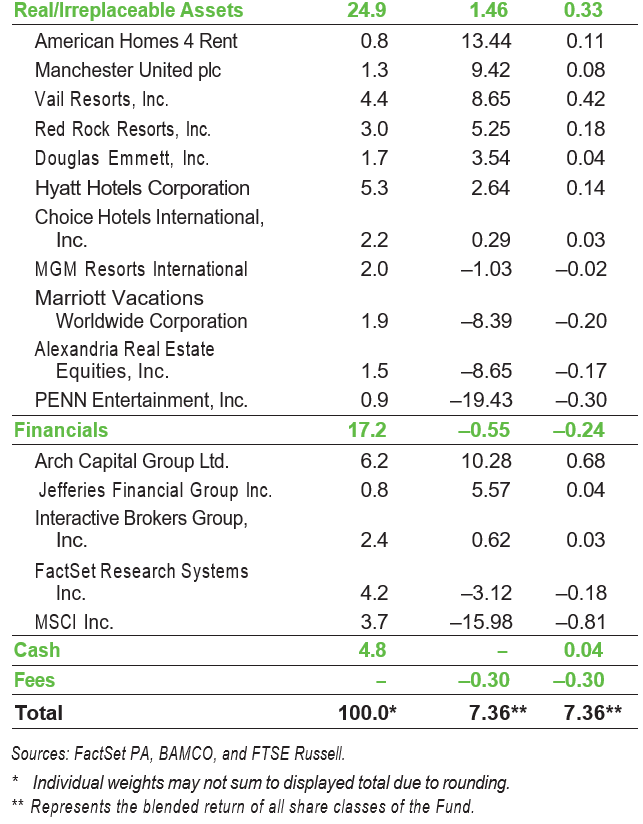

The Fund's strong performance in the second quarter was principally due to what we call our Core Growth and Disruptive Growth companies. These well-managed businesses are competitively advantaged, are growing quickly, have the potential to take large shares of their addressable markets, and generate strong returns on capital investments. These include CoStar Group, Inc. ( CSGP ) in Core Growth and Tesla, Inc . ( TSLA ) and FIGS, Inc. ( FIGS ) in Disruptive Growth. These gains were partially offset by underperformance of our Real/Irreplaceable Asset and Financials companies. Many portfolio businesses have been repurchasing their stocks at what we believe are attractive valuations. Companies repurchasing shares include Marriott Vacations Worldwide Corporation ( VAC ) and PENN Entertainment, Inc. ( PENN ) in Real/Irreplaceable Assets and FactSet Research Systems Inc. ( FDS ) and MSCI Inc . ( MSCI ) in Financials.

{kind=link}

{kind=link}

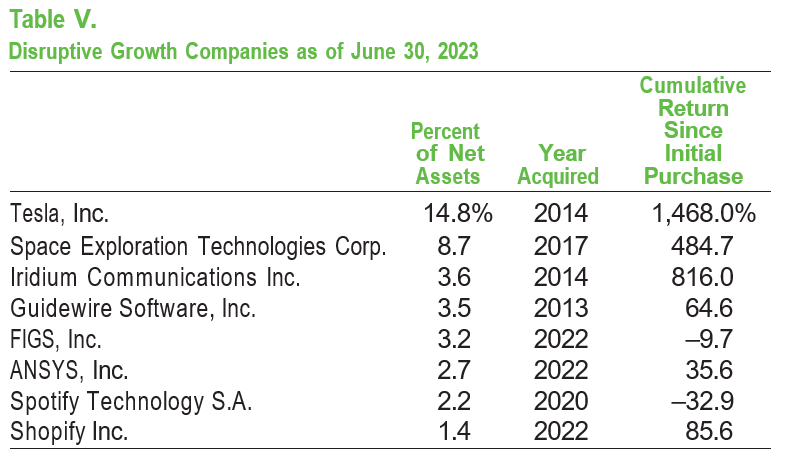

Tesla, Inc. designs, manufactures, and sells electric vehicles (EVs), related software and components, and solar and energy storage products. Despite the negative impact of macroeconomic challenges on results, Tesla shares contributed to performance in the period. We believe investors were encouraged by the recent stability in Tesla's vehicle pricing, following price reductions with reports suggesting record quarterly deliveries. In addition, the company announced that all versions of Model 3 and Y were eligible for tax credits of the Inflation Reduction Act in the U.S. China extended its EV tax benefits, providing further support for EV demand. The adoption of Tesla's charging solutions by competitors, including General Motors, Ford, Rivian, Volvo, and Polestar, highlight Tesla's strong market position and provide additional revenue opportunities. Finally, Tesla's extensive investments in artificial intelligence ((AI)), particularly through the development of Dojo and autonomous capabilities, are expected to benefit from recent advancements in the field and provide additional support to the company's long-standing commitment to AI.

Tesla's stock price increased 26.2% in the second quarter and added 325 bps to Fund performance. The company saw robust orders for its cars after price reductions. As a result, Tesla continues to increase its EV market share. The company remains the lowest cost provider of high-quality EVs and continues to pass through these cost savings to consumers as price reductions. Further, Tesla continues to produce its vehicles more efficiently, while ramping new factories in Texas and Berlin. This should mitigate gross margin declines from startup costs, while still generating strong cash flow for further high-return investments. Among those investments are additional factories, batteries, robotics, and, most importantly, self-driving AI full self- driving software. The company is building its fifth factory, which will be in Mexico, and it should open early next year. This will add capacity to meet demand, while helping lower overhead and logistics costs.

Tesla will also benefit from the Inflation Reduction Act. Consumers will receive a $7,500 credit against income taxes when they buy an EV, while Tesla receives a $3,500 tax incentive for every EV car sold. The average new internal combustion engine car in the U.S. costs $48,000. After U.S. tax credits, Tesla EV cars, with their extraordinary quality, have an average cost of approximately $33,000!! Combining Tesla's strong 40% EBITDA to cash conversion rate and over $22 billion cash and nominal debt puts Tesla in an exceedingly strong financial position.

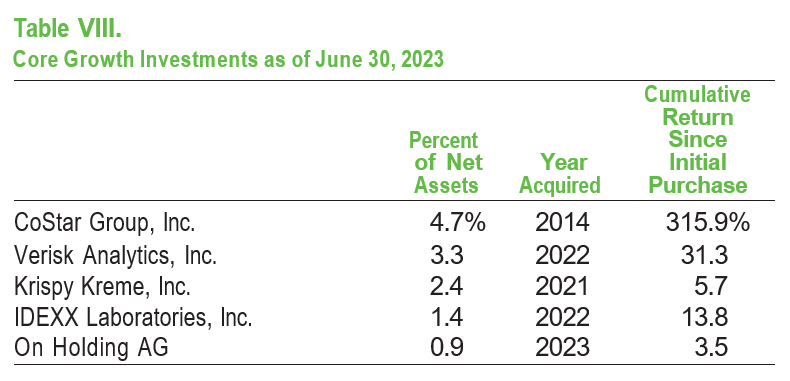

CoStar Group, Inc. is a provider of marketing and data analytics to the commercial and residential real estate industries. Shares increased on robust financial performance, with net new sales growing 18% in the quarter. These results were driven by acceleration in multifamily bookings, which expanded 110% year-over-year, but were partially offset by slower results in the commercial real estate business. We are encouraged by early signs of traction in CoStar's nascent residential offering. We estimate that CoStar invested around $230 million in this initiative in 2022 and is targeting a total investment approaching $500 million in 2023. While this is a significant upfront commitment, we believe residential represents a transformative opportunity for CoStar. We believe the company's proprietary data, broker-oriented approach, and best-in-class management uniquely position it to succeed.

CoStar's share price increased 29.3% in the quarter and helped the Fund's performance by 132 bps. That was due to an acceleration in daily active users on its Homes.com platform. CoStar's monthly active users reached 35 million, up from 24 million in the first quarter. We believe CoStar has demonstrated it can drive meaningful growth to its platform even before a huge branding campaign. CoStar expects to more than double its residential marketing investment from 2022 levels to approximately $500 million this year. We believe that increased investment should boost organic growth on its Homes.com platform. Over the next five years, CoStar's residential investment could add at least $1 billion to annualized revenue at a significantly accretive margin. A 50% increase in CoStar's $2 billion annual revenue could increase its EBITDA 75%. Longer term, we believe this investment opportunity represents several multiples of $1 billion annual revenue. CoStar continues to experience strong new bookings and strong retention rates despite implementing price increases. CoStar's balance sheet remains strong with $5 billion cash and $1 billion of debt.

FIGS, Inc. is a direct-to-consumer apparel and lifestyle brand dedicated to the healthcare community. Shares outperformed during the quarter after reporting stronger-than-expected quarterly results. Revenue growth and profitability exceeded consensus estimates. Active customers grew more than 20%, a testament to strong consumer demand for the brand. Margins were also solid despite a more promotional apparel environment. We continue to believe FIGS has a long growth runway as its strong brand and route-to-market strategy create durable competitive advantages.

FIGS' 33.6% share price increase in the quarter added 107 bps to the Fund's performance. The company's strong customer additions continued with record website reactivations. FIGS' current above normal promotions will help reduce inventory levels substantially for the balance of the year. The company's inventory build-up over the past 18 months due to supply-chain concerns had been a large user of cash. We believe the company has a large growth opportunity selling its medical customers non-scrubs outerwear and underwear. It also should achieve greater international penetration and increase its customer base through extended size offerings. The company continues to expand brand awareness with digital marketing. Its international business is in its infancy with initial strong results in the U.K. and Canada. FIGS' direct-to-consumer model for its healthcare uniform business with replenishment characteristics, strong brand, and superior quality provide durable competitive advantages. We expect FIGS to continue to gain share in the $80 billion global healthcare apparel market. We believe the company could double its revenue over the next three years with EBITDA margins that ultimately could exceed 20%.

{kind=link}

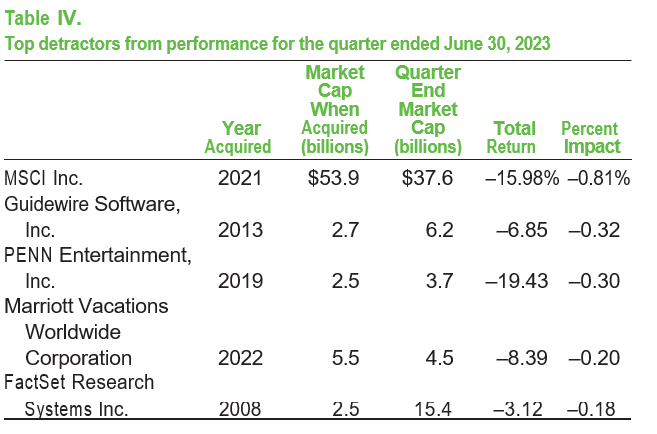

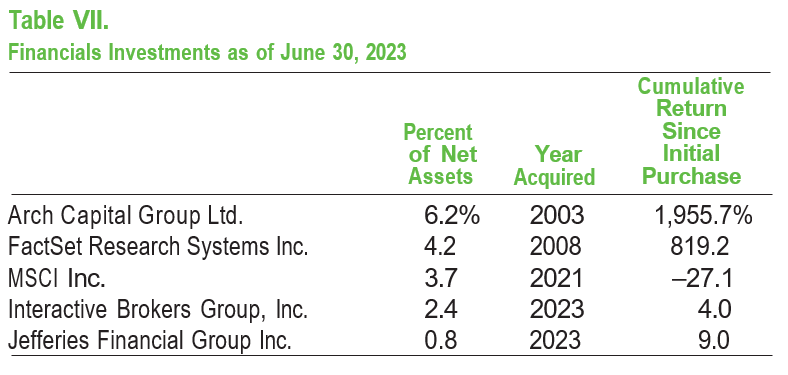

Shares of MSCI Inc. , a leading provider of investment decision support tools, fell 16.0% in the second quarter and penalized Fund performance by 81 bps. This underperformance was due in part to slower ESG sales growth, given political controversy in the U.S. Broader macro uncertainty leads to tightening wealth manager customer budgets. As a result, MSCI experienced lengthening of sales cycles, though it continues to have a strong pipeline of new deals. While the longer sales cycle near term should be expected, the company continues to grow with strong retention rates. MSCI is an extremely well-run business committed to protecting profitability. It has significant secular long-term growth opportunities relating to the increased use of data analytics in the investment process. Asset managers outsourcing back-office functions provide additional opportunity. The company continues to generate resilient earnings and cash flow and is benefiting from improved performance in the global equity markets, which impacts MSCI's asset-based fee revenue. MSCI owns strong, all-weather franchises. We believe its core equity index business continues to be a durable double-digit grower, while its climate change tools offer another important avenue for growth. Climate tools help banks and credit providers understand climate emission rates of borrowers and the footprint of their loan books. Climate today is an $80 million revenue business . MSCI believes in 10 years it could be a $1.5 billion business with high margins. Finally, MSCI has an important opportunity in private markets, especially in fixed income and private credit. The company continues to generate strong cash flow, which it uses to invest in its business and repurchase its stock.

Shares of property and casualty (P&C) insurance software vendor Guidewire Software, Inc. ( GWRE ) detracted from performance after announcing mixed quarterly results. On the positive side, the company made excellent progress on subscription gross margins, grew annual recurring revenue ((ARR)) faster than consensus, and gave upside margin guidance for fiscal year 2024. On the downside, new ARR deals came with steeper ramps, services revenue slipped due to some legacy fixed price service contracts, and cash collection cycles extended in the quarter. Despite the mixed performance, we remain optimistic about the company's long-term prospects. The company has crossed the midpoint of its cloud transition and is demonstrating more consistent recurring revenue growth and durable gross margin expansion. We believe Guidewire will be the critical software vendor for the global P&C insurance industry, capturing 30% to 50% of its $15 billion to $30 billion total addressable market and generating margins above 40%.

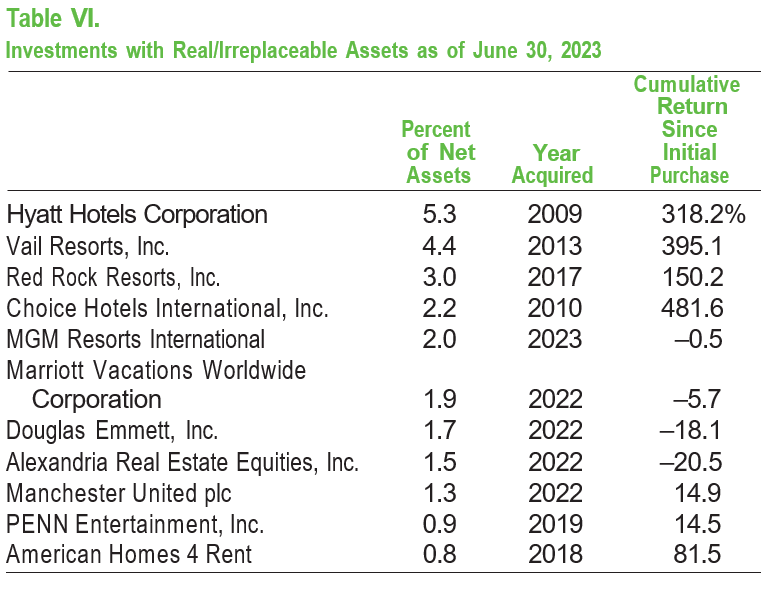

PENN Entertainment, Inc. is an operator of regional casinos across the U.S. Its share price fell 19.4% in the second quarter and penalized the Fund's performance by 30 bps. The decline was due to investor concerns that a potential recession would negatively impact visitation and spending levels. While startup costs for digital sports betting and economic deterioration in certain regional markets are currently pressuring results, we believe PENN will successfully navigate these headwinds. This is especially the case given its strong balance sheet and cash flow profile. We think the company will continue to invest in its digital gaming opportunity and return cash to shareholders through buybacks. We believe PENN's stock, which sank to an historical trough EBITDA multiple during the quarter, should revert to its historical average multiple as its digital gaming operation becomes profitable. We believe PENN's business should regain its growth trajectory over the next year, e specially due to the competitive advantages of its unique entertainment facilities and its importance as a taxpayer and job provider.

Investment Strategy & Portfolio Structure

We remain committed to long-term investments in competitively advantaged growth businesses. These businesses have large market opportunities, are taking market share, and are managed by exceptional executives whom we trust.

Despite market volatility, our companies continue to invest to accelerate revenue growth, while using excess cash to return capital to shareholders through buybacks and dividends. We believe this reduces Fund volatility, an important factor in a concentrated fund.

One of the reasons we believe our companies should continue to grow in all market environments is that they invest for growth through all market environments.

We continue to invest for the long run in a focused portfolio of what we believe are appropriately capitalized, well-managed, small- and mid-cap growth businesses at attractive prices. We attempt to create a portfolio of between 20 and 30 securities diversified by GICS sectors that will be approximately 80% as volatile as the market. Businesses in which the Fund invests are identified by our analysts and portfolio managers using our proprietary research and time-tested investment approach.

As of June 30, 2023, Baron Focused Growth Fund held 29 investments. The Fund's average portfolio turnover for the past three years was 26.6%. This means the Fund has an average holding period for its investments of approximately four years. This contrasts with the average mid-cap growth mutual fund, which typically turns over its entire portfolio every 17 months based on a 3-year average. From a quality standpoint, the Fund's investments have stronger sales growth than holdings in the Index, higher EBITDA, operating and free-cash-flow margins, and stronger returns on invested capital.

While focused, the Fund is diversified by sector. The Fund's sector weightings are significantly different than those of the Index. For example, we are heavily weighted in Consumer Discretionary businesses with 37.8% of net assets in this sector versus 12.9% for the Index. We have no exposure to Energy versus 3.9% for the Index and lower exposure to Healthcare stocks at 4.6% of the Fund versus 22.6% for the Index. We believe the performance of businesses in these sectors can be affected by factors that cannot be predicted and therefore feel it is undesirable to invest in these stocks in a concentrated portfolio for the long term. The Fund is further diversified by investments in businesses at different stages of growth and development.

{kind=link}

Disruptive Growth firms accounted for 40.3% of the Fund's net assets. On current metrics, these businesses may appear expensive; however, we think they will continue to grow significantly and, if we are correct, they have the potential to generate exceptional returns over time. Examples of these companies include EV leader Tesla, Inc. , commercial satellite company Iridium Communications Inc. , ( IRDM ) and P&C insurance software vendor Guidewire Software, Inc. All of these companies have large underpenetrated addressable markets relative to the current size of these competitively advantaged businesses.

{kind=link}

Companies that own what we believe are Real/Irreplaceable Assets represented 24.9% of net assets. Vail Resorts, Inc. , ( MTN ) owner of the premier ski resort portfolio in the world, upscale lodging brand Hyatt Hotels Corporation ( H ), and the largest U.S. regional casino gaming company PENN Entertainment, Inc. , are examples of companies we believe possess meaningful brand equity and barriers to entry that equate to pricing power over time. PENN's state-granted licenses for its regional casinos provide important protection from competitors. Online sports betting and internet-casino gaming offer large opportunities for future growth.

{kind=link}

Financials investments accounted for 17.2% of the Fund's net assets. These businesses generate strong recurring earnings through subscriptions and premiums that generate highly predictable earnings and cash flow. Those businesses use cash flows to continue to invest in new products and services, while returning capital to shareholders through share buybacks and dividends. These companies include Arch Capital Group Ltd. ( ACGL ), FactSet Research Systems Inc. , and MSCI Inc.

Arch, one of the leading specialty insurers, continued to increase premiums written and raise prices. This strong pricing is resulting in robust returns on investments, with increased earnings and cash flow that the company is using to repurchase its shares. We believe Arch could continue to generate mid-teens returns on capital over the long term.

{kind=link}

Core Growth investments, steady growers that continually invest in their businesses for growth and return excess free cash flow to shareholders, represented 12.7% of net assets. An example would be CoStar Group, Inc. The company continues to add new services in the commercial and residential areas of real estate, which have grown its addressable market and enhanced services for its clients. This has improved client retention and cash flow. CoStar continues to invest its cash flow in its business to accelerate growth, which we believe should generate strong returns over time.

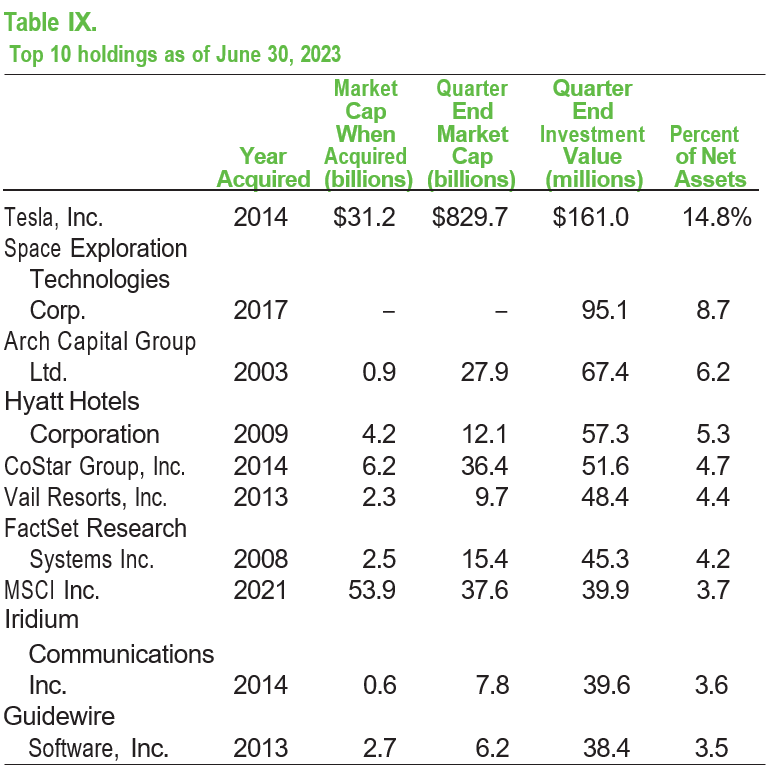

Portfolio Holdings

As of June 30, 2023, the Fund's top 10 holdings represented 59.2% of net assets. A number of these investments have been successful and were purchased when they were much smaller businesses. We believe they continue to offer significant appreciation potential, although we cannot guarantee that will be the case.

The top five positions in the portfolio, Tesla, Inc. , Space Exploration Technologies Corp. , Arch Capital Group Ltd. , Hyatt Hotels Corporation , and CoStar Group, Inc. , all have, in our view, significant competitive advantages due to irreplaceable assets, strong brand awareness, technologically superior industry expertise, or exclusive data that is integral to their operations. We think these businesses cannot be easily duplicated, which enhances their potential for superior earnings growth and returns over time.

{kind=link}

Recent Activity

In the second quarter, we purchased shares of On Holding AG ( ONON ), a developer and distributor of athletic footwear, apparel, and accessories. On is one of the fastest-growing scaled athletic sports companies in the world. It specializes in products featuring the company's proprietary cushioning technology, most notably Cloud Tec (flex plates in shoes), Speed board (injection molding), Mission grip (for trails), Helion (super foam cushioning) and The Roger franchise for tennis (Roger Federer invested $50 million in 2019). The products are sold through 8,100 premium retail stores which account for 60% of revenue, and direct-to-consumer sales account for the balance, with the majority of direct-to-consumer done through its website. On has expanded outside of Switzerland and Europe. It operates one flagship retail store in New York City and four smaller format retail stores in China. Roughly half of its revenues are generated in North America, 44% in Europe, and 5% in Asia Pacific.

On has a large market opportunity operating in the $300 billion global sportswear industry, which is forecast to grow at a high single-digit rate through 2025, making it one of the fastest-growing pockets within consumer. The factors driving growth in the industry include continued trends toward athleisure as consumers pivot towards more comfortable and casual attire combined with trends towards healthier lifestyles. The industry is highly competitive with Nike and Adidas garnering 15% and 11% share, respectively. In footwear, the industry is even more consolidated with Nike and Adidas taking over 50% share in the U.S. and over 40% globally. Regardless, we believe On has an opportunity to continue taking share from Nike and Adidas as has been the case over the past couple of years.

This is due to the extraordinary quality of its products. Demand is so strong that On has not been able to meet consumer demand for its shoes.

We believe On should be able to grow revenues 20% to 25% annually for many years, while expanding margins. We expect the company to continue to reinvest in its business at high rates of return. It is debt free. Its growth should be driven by growing brand awareness as On expands its geographic footprint. Eventual upselling of its running sneakers across lifestyle, outdoor, and tennis as well as from footwear to apparel and accessories is another long-term opportunity.

We also added to our investment in Interactive Brokers Group, Inc. ( IBKR ), a leading securities brokerage company that provides securities brokerage to both retail and professional investors. Interactive Brokers differentiates itself through its low prices, the vast array of markets it serves, and its strong growth from countries where low-cost brokerage is not well penetrated. 80% of Interactive Brokers customers are from outside the U.S., while 80% of their assets are invested in the U.S. The company offers its clients low-cost trading due to its high level of automation. This while providing competitive margin loans and securities lending rates and offering attractive yields on uninvested cash balances. The company continues to hire software and computer engineers with a focus on automating many of the processes that competitors rely on employees to perform.

With its low-priced offering and leading range of capabilities, we believe that Interactive Brokers is well positioned to not just continue its rapid pace of account growth from just over 2 million clients today but to accelerate growth. The company's focus on automation should enable it to continue being the low-cost provider, while earning best-in-class margins, which we believe should lead to double-digit revenue and earnings growth over the long run.

Outlook

We believe the prices of many of our stocks reflect investors' expectations for significant declines in earnings this year. Investors obviously remember operating declines during the 2008/2009 Global Financial Crisis and are pricing in similar declines today. If we do not go into a deep recession this year or if the slowdown and expected decline in earnings are not as bad as feared, we could see significant near-term upside in our investments. We believe our stocks are cyclically depressed, not secularly challenged, and should recover to peak levels achieved in November 2021 during the next 18 months. Through June 30, 2023, most of our portfolio companies have not experienced significant slowdowns in sales or earnings growth, and their outlooks remain strong. Our businesses' balance sheets have been strengthened compared to pre-COVID levels.

In the past, after wars, pandemics, financial panics, higher-than-normal inflation, and significant market declines, as interest rates stabilize and are ultimately reduced, equity stock prices have increased substantially. We believe that will happen again, although the timing remains uncertain.

Thank you for investing in Baron Focused Growth Fund. We continue to work hard to justify your confidence and trust in our stewardship of your family's hard-earned savings. We also continue to try to provide you with information we would like to have if our roles were reversed. This is so you can make an informed judgment about whether Baron Focused Growth Fund remains an appropriate investment for your family.

Respectfully,

Ronald Baron, CEO and Portfolio Manager.

David Baron, Portfolio Manager.

Footnotes

1. Reflects the actual fees and expenses that were charged when the Fund was a partnership. The predecessor partnership charged a 15% performance fee through 2003 after reaching a certain performance benchmark. If the annual returns for the Fund did not reflect the performance fees for the years the predecessor partnership charged a performance fee, the returns would be higher. The Fund's shareholders will not be charged a performance fee. The performance is only for the periods before the Fund's registration statement was effective, which was June 30, 2008. During those periods, the predecessor partnership was not registered under the Investment Company Act of 1940 and was not subject to its requirements or the requirements of the Internal Revenue Code relating to registered investment companies, which, if it were, might have adversely affected its performance.

2. The Russell 2500 ™ Growth Index measures the performance of small to medium-sized companies that are classified as growth. The S&P 500 Index measures the performance of 500 widely the performance of small to medium-sized U.S. companies that held large cap U.S. companies. All rights in the FTSE Russell Index (the "Index") vest in the relevant LSE Group company which owns the Index. Russell® is a trademark of the relevant LSE Group company and is used by any other LSE Group company under license. Neither LSE Group nor its licensors accept any liability for any errors or omissions in the indexes or data and no party may rely on any indexes or data contained in this communication. The Fund includes reinvestment of dividends, net of foreign withholding taxes, while the Russell 2500 ™ Growth I ndex and S&P 500 Index include reinvestment of dividends before taxes. Reinvestment of dividends positively impacts the performance results. The indexes are unmanaged. Index performance is not Fund performance; one cannot invest directly into an index.

3. The performance data does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares.

4. Performance for the Institutional Shares prior to May 29, 2009 is based on the performance of the Retail Shares, which have a distribution fee. The Institutional Shares do not have a distribution fee. If the annual returns for the Institutional Shares prior to May 29, 2009 did not reflect this fee, the returns would be higher.

5. Not annualized.

Investors should consider the investment objectives, risks, and charges and expenses of the investment carefully before investing. The prospectus and summary prospectus contain this and other information about the Funds. You may obtain them from the Funds' distributor, Baron Capital, Inc., by calling 1-800-99BARON or visiting www.BaronFunds.com. Please read them carefully before investing.

Risks: The Fund is non-diversified which means, in addition to increased volatility of the Fund's returns, it will likely have a greater percentage of its assets in a single issuer or a small number of issuers, including in a particular industry than a diversified fund. Single issuer risk is the possibility that factors specific to an issuer to which the Fund is exposed will affect the market prices of the issuer's securities and therefore the net asset value of the Fund. As of the most recent quarter-end, about 15% of the Fund's net assets are invested in Tesla stock. Therefore, the Fund is exposed to the risk that were Tesla stock to lose significant value, which could happen rapidly, the Fund's performance would be adversely affected. Specific risks associated with investing in small and medium-sized companies include that the securities may be thinly traded and more difficult to sell during market downturns. The Fund may not achieve its objectives. Portfolio holdings are subject to change. Current and future holdings are subject to risk.

The discussions of the companies herein are not intended as advice to any person regarding the advisability of investing in any particular security. The views expressed in this report reflect those of the respective portfolio managers only through the end of the period stated in this report. The portfolio manager's views are not intended as recommendations or investment advice to any person reading this report and are subject to change at any time based on market and other conditions and Baron has no obligation to update them.

This report does not constitute an offer to sell or a solicitation of any offer to buy securities of Baron Focused Growth Fund by anyone in any jurisdiction where it would be unlawful under the laws of that jurisdiction to make such offer or solicitation.

Free cash flow ((FCF)) represents the cash that a company generates after accounting for cash outflows to support operations and maintain its capital assets.

BAMCO, Inc. is an investment adviser registered with the U.S. Securities and Exchange Commission ((SEC)). Baron Capital, Inc. is a broker-dealer registered with the SEC and member of the Financial Industry Regulatory Authority, Inc. ((FINRA)).

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Baron Focused Growth Fund