BSFFF - Basic-Fit: Staying Strong Initiate At Buy

2023-11-01 21:13:17 ET

Summary

- Basic-Fit is a Buy with strong leadership, growing premium membership, and potential for margin expansion.

- The company is the largest low-cost health and fitness club player in Europe, with over 1,300 clubs.

- Despite the impact of COVID, Basic-Fit has reported strong recovery and continued growth in memberships and revenues.

Investment Thesis

We rate Basic-Fit ( OTCPK:BSFFF ) a Buy on the back of its 1) strong leadership within the European segment 2) improving mix of premium membership with penetration of 44% 3) growing monthly average revenue per user 4) potential for margin expansion on the back of improving mix and moderating inflation 5) robust return ratios with ROIC of 30%+ and 6) relative undervaluation compared to its peers.

Company Background

Basic-Fit is the largest low cost health and fitness club player in Europe with a total of 1,300 clubs across France, Netherlands, Spain, Belgium, Luxembourg and Germany. It primarily focuses on health clubs which are underserved by competitors and boasts over 3.6 mn members across its chain. It has more than 2x clubs compared to its closest competitor in Europe demonstrating its significant leadership and brand resonance.

{kind=link}

Company presentation

The company recently entered in Germany in 2022 and provides an untapped growing potential with a strong pipeline on the back of 65 signed contracts expected to be operational within next 18 months. Unlike many peers, it operates its own gym.

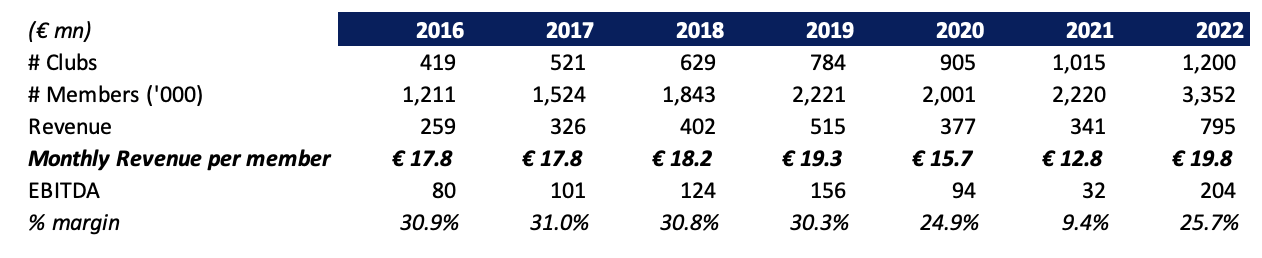

Historical Track Record

The company reported a strong growth in clubs historically with total number of clubs jumping 3-fold over 2016-2022 period along with a 17% growth in memberships. Revenue grew at 26% CAGR during the pre-COVID period with margins upwards of 30%. However, COVID led to a significant decline in its operations during the 2020-2021 period with EBITDA margins tumbling 20 percentage points to under 10% as a result of sticky fixed costs amidst shuttering of its clubs. It has reported strong recovery in 2022 with revenues increasing 16% on a 2 year stack period. EBITDA margins remain depressed compared to its pre-COVID period as a result of continued operating deleverage and higher average rentals as well as rising wage costs in an inflationary period.

{kind=link}

Author, Company filings

Strong YTD Performance

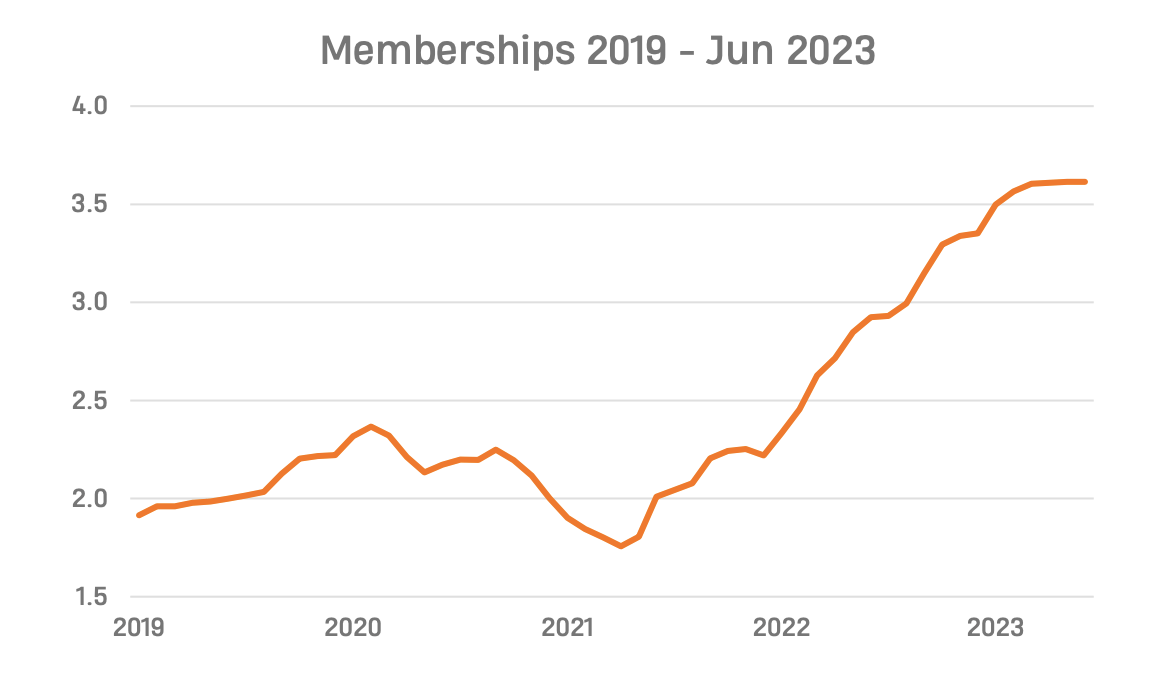

BSFFF reported strong performance for the year with revenues up 36% YoY primarily driven by strong 18% YoY growth in memberships, new net addition of clubs along with an uptick in the monthly revenue per member which improved 3.5% to €23.3. It reported continued growth in memberships across all countries and mature clubs with both joiners and leavers trends normalized to pre-COVID levels.

{kind=link}

Company presentation

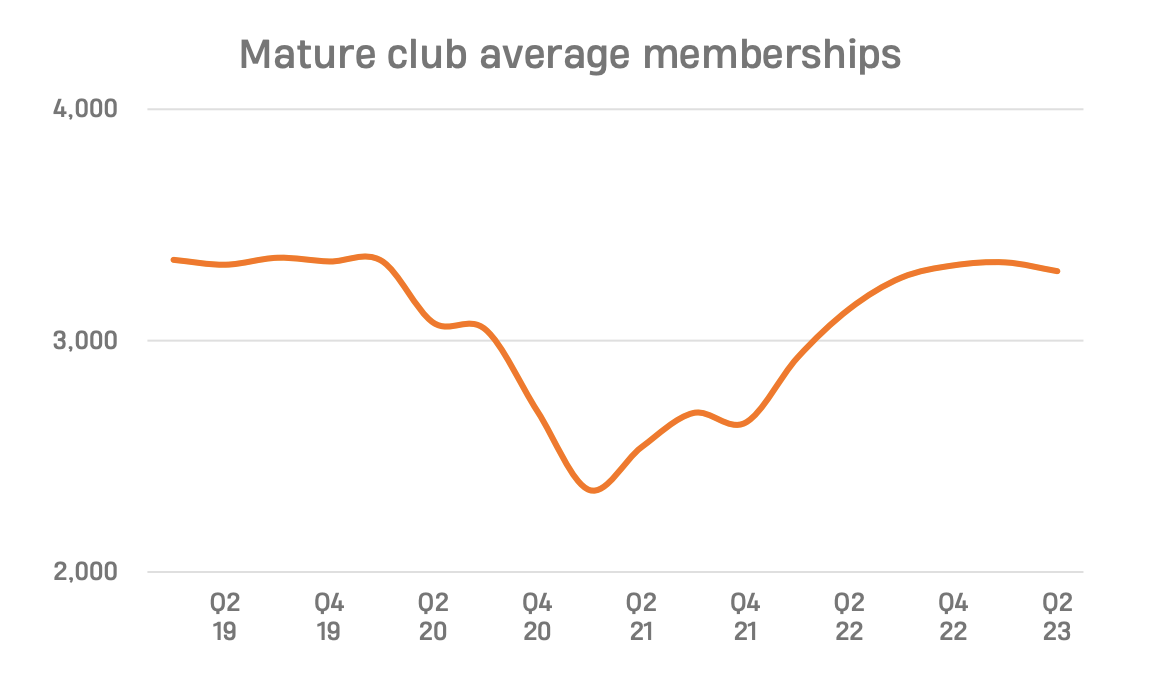

Premium membership uptake increased 55%+ YoY with penetration increasing from 23% in 2019 and 30% last year to 44% by Q3 FY23 driven by continued perceived benefits from its new and existing users. In addition, mature club average memberships reached to pre-COVID levels which remains a testament to the company's focused growth approach and strong brand resonance within its country of operations.

{kind=link}

Company presentation

EBITDA margins, however, declined by about 300 bps YoY in H1 2023 primarily as a result of higher energy costs as well as higher rent and personnel costs due to the current inflationary environment. The company reiterated its guidance for the full year revenue guidance to be €1bn+ which implies a flattish revenue growth for Q4 and seems reasonable on the back of stable memberships as well as improving monthly average revenue per user which is inching closely towards the management's guidance of €24.5 driven by increasing share of premium subscribers as well as price hikes. In addition, H2 EBITDA is likely to be higher than H1 primarily as a result of improving maturity profile of the newly opened clubs, strict cost controls as well as declining energy costs and moderating inflationary pressures and expect 2023 margins to close at 27%+ implying a 150 - 200 bps expansion for the full year and significantly higher than the sub-23% in H1 2023. In addition, it has renegotiated energy contracts which will help save them about €1.5 mn in energy costs in 2024. We believe Adj. EBITDA margins for 2024 to improve near its pre-COVID levels but remain sub-30% primarily driven by robust utilization and improving product mix.

Leverage ratios remain comfortable with Net Debt/ TTM EBITDA of 2.7x and no near term maturities. We believe the company's leverage profile provides them the flexibility to further expand and add new stores driven by strong cash generation in its existing clubs along with improving maturity profile of the recently opened clubs.

We believe the company is further likely to report 20%+ growth in 2024 revenues driven by strong membership addition and expect net new clubs of over 100 in 2024 with the company likely to exceed its 200 net clubs additions for the year, having achieved 196 openings by mid-October itself.

{kind=link}

Company filings

Valuation

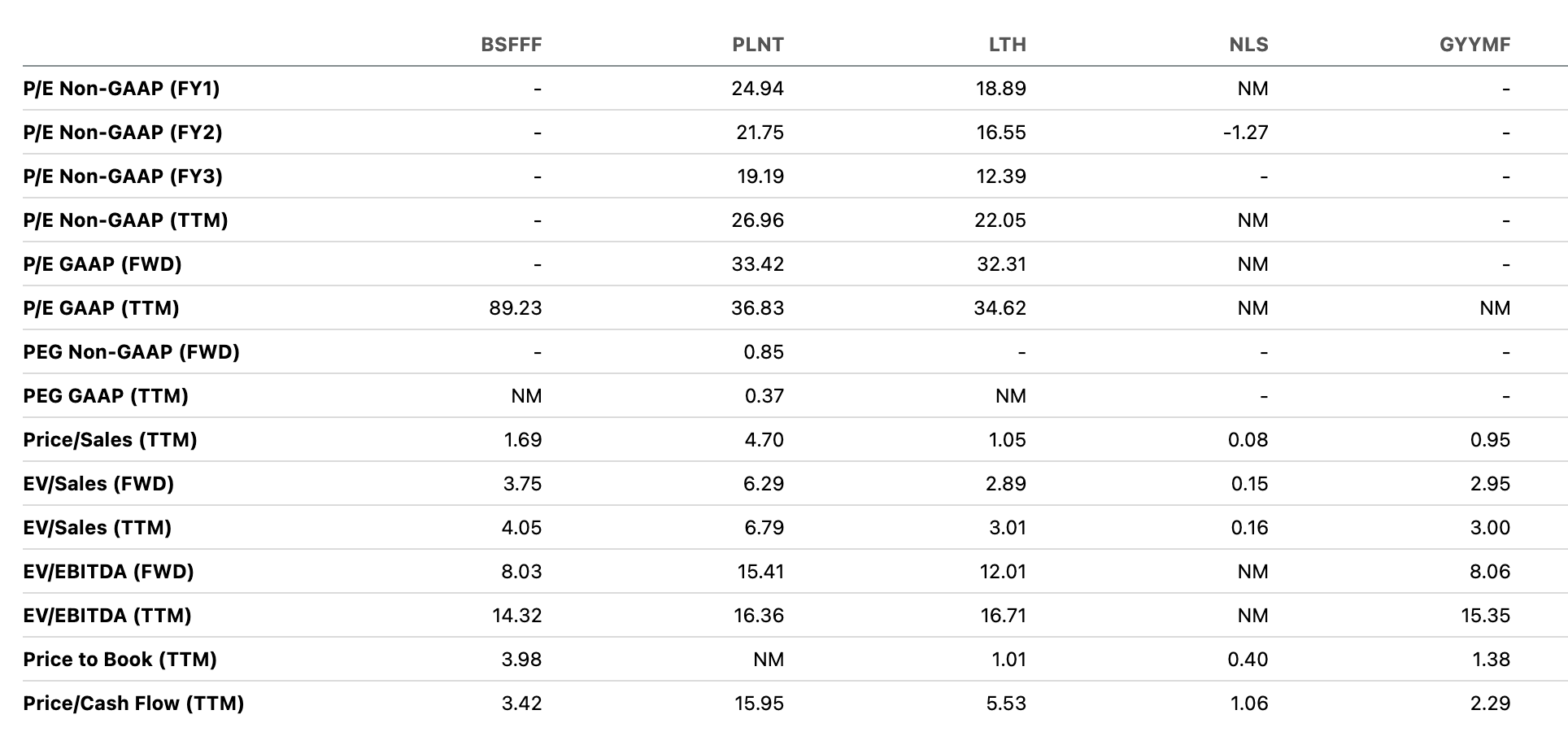

We compare Basic-Fit with other listed peers operating fitness centers, health clubs and gyms globally given limited peer set within European region. On an EV/ Fwd EBITDA basis, the company trades at just 8x Fwd EBITDA, at a discount to its US based counterparts which are trading at about 14x as well as its UK based peer The Gym Group ( OTCPK:GYYMF ) which trades at just 8x, primarily because of relatively lower margins and return ratios.

{kind=link}

Seeking Alpha

We believe the company's strong earnings momentum, better visibility in the near term driven by robust growth in its premium membership, strong and active development pipeline of new clubs and an unassailable 30% ROIC margins provide a favorable risk reward. Its relative undervaluation despite generating robust returns and continued growth provides sufficient margin of safety. We initiate with a Buy with a target price of $30 (at 10x Fwd EV/ EBITDA).

Risks to Rating

Risks to rating includes

1) Persistent macro headwinds leading to a squeeze in consumer wallets could lead to lower propensity for people to join gyms

2) The company relies on limited suppliers and vendors for site fit outs, equipment or maintenance and any disruption in its service or inability to procure services at favorable rates can lead to significant pressure on margins

3) Company operates in an asset heavy model and has high operational gearing and may not be substantially scalable as a result of high upfront costs and cash flow mismatches in case of a downturn or weakening fundamentals

Final Thoughts

Basic-Fit has remained strong in a tough macro backdrop driven by its strong leadership, attractive offering of a low cost fitness membership, owned operations reflecting greater control and strong return ratios bodes well for the company in the long run. The company has massive untapped potential in Germany We believe there are major drivers to margin expansion to its pre-COVID levels on the back of improving utilization as an operating gym largely has limited fixed costs, improving premium membership penetration driving higher monthly average revenue per user and tight cost controls. Initiate with a Buy ascribing a target price of $30.

For further details see:

Basic-Fit: Staying Strong, Initiate At Buy