XRAY - Bausch + Lomb: Still A Favorable Risk-To-Reward Prospect

Summary

- Bausch + Lomb has had a rocky time over the past few quarters, with sales coming under pressure and margins contracting.

- Most of the issues, though, seem transitory in nature and the firm is likely to see some improvement moving forward even though some issues might be longer lasting.

- At present, the firm still looks cheap, both on an absolute basis and relative to similar firms.

Although there is no right answer, most people would agree that the ability to see is the most important of the five senses that humans are typically granted. Unfortunately, there are many individuals in this world who struggle with vision-related problems. But one company dedicated to solving or mitigating these is Bausch + Lomb Corporation ( BLCO ). At first glance, you might think that this space would be doing quite well almost irrespective of broader economic conditions. After all, people need to see even when the economy is struggling. Interestingly though, the company has been hit hard by rising costs and foreign currency fluctuations. Obviously, if this lasts long term, the pain for shareholders could be felt. But under the assumption that financial performance will eventually revert back to what it was previously, shares do look quite affordable at this time. Because of this, I still believe that the company deserves a 'buy' rating even though the stock has moved up nicely in recent months.

Taking another look

Back in early June of 2022, I wrote an article discussing the bullish thesis that I had regarding Bausch + Lomb. In that article, I talked about how encouraging sales had been for the company leading up to that point. At the same time, however, the firm's continued bottom line deterioration turned me off. Fortunately, this was more than offset by just how cheap shares were, even if financial performance did not improve. At the end of the day, this led me to rate the company a 'buy' to reflect my view that shares should outperform the broader market for the foreseeable future. Since then, things have played out quite nicely. While the S&P 500 is down 2%, shares of Bausch + Lomb have generated upside of 15.1%.

{kind=link}

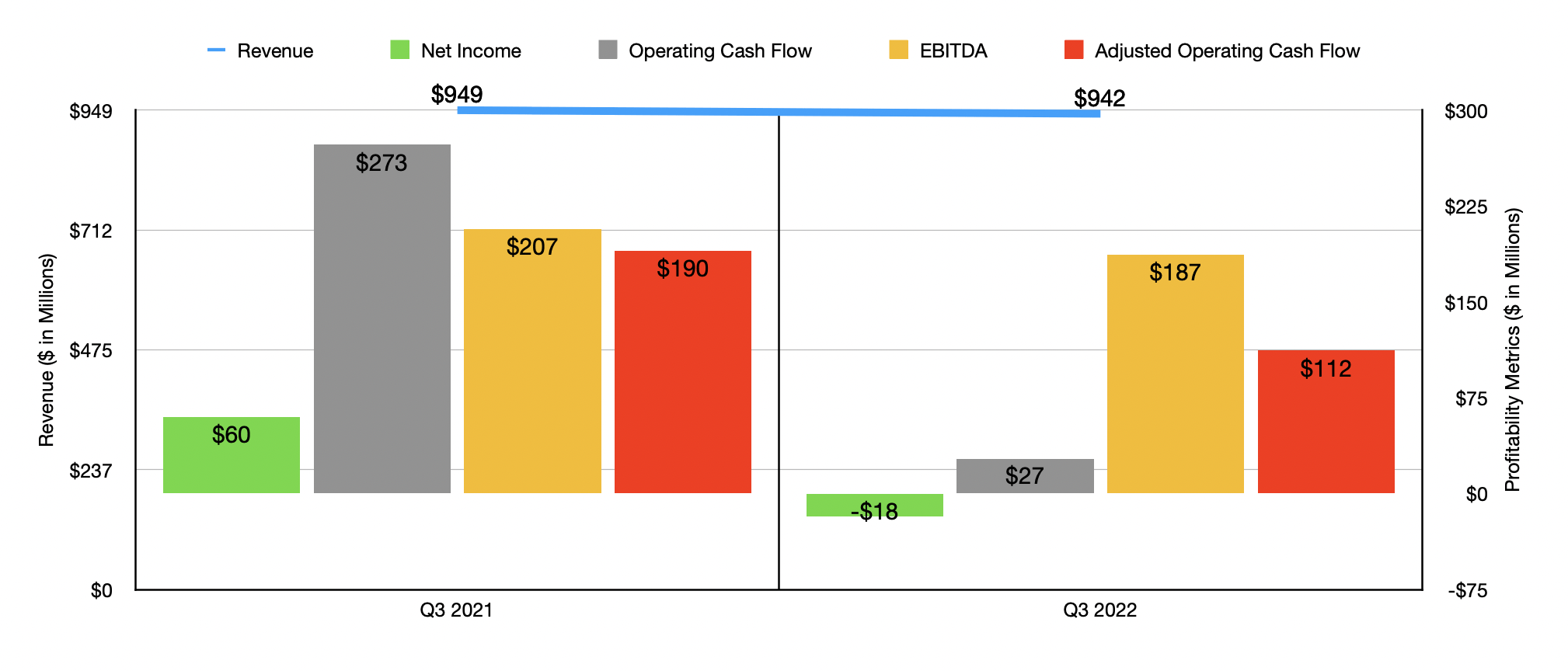

Interestingly, this return disparity developed even as top line and bottom line results for the company have worsened. To see what I mean, we should first look at financial data covering the third quarter of the company's 2022 fiscal year. This is the most recent quarter for which data for the firm is available. During this time, revenue came in at $942 million. That's actually down from the $949 million reported the same time one year earlier. According to management, actual organic revenue for the company expanded nicely year over year, with growth of 5%. The reason why sales were down, however, had to do with foreign currency fluctuations. Those impacted revenue negatively to the tune of $55 million. On the organic side of things, the company benefited from a rise in volumes shipped and higher pricing, much of which was associated with its Vision Care segment.

On the bottom line, the picture for the company looked even worse. The firm went from generating a net profit of $60 million in the third quarter of 2021 to generating a net loss of $18 million the same time last year. On top of being hit by the decrease in sales, the company also was hit by higher costs. The aforementioned unfavorable impact caused by foreign currency fluctuations, as well as higher manufacturing variances resulting from inflationary pressures and higher manufacturing efficiency ramp up costs hit the company significantly. Selling, general, and administrative costs also took a toll, rising $33 million year over year because of a rise in professional fees and higher compensation expenses, much of which were related to separation costs and a loss of synergies as the company became a standalone entity. Higher selling expenses also hurt the firm. Other profitability metrics for the company followed a similar trajectory. Operating cash flow plunged from $273 million to $27 million. Though if we adjust for changes in working capital, the decline would have been a somewhat more modest amount, dropping from $190 million to $112 million. And finally, EBITDA for the company shrank from $207 million to $187 million.

{kind=link}

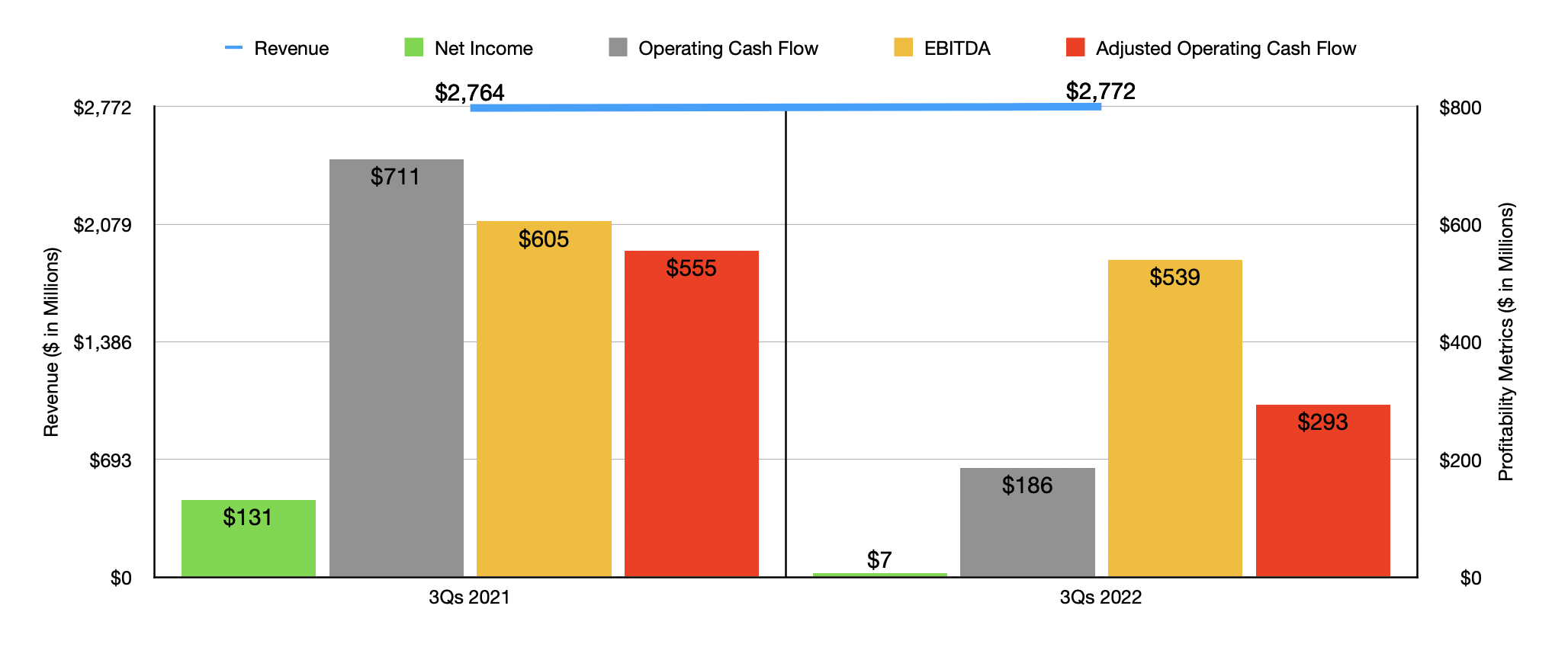

Although revenue suffered some during the third quarter of the year, revenue for the first nine months of 2022 as a whole was positive. Sales went from $2.76 billion to $2.77 billion. But the bottom line very much mirrored what the company saw in the third quarter alone. Net profits shrank from $131 million to $7 million. Operating cash flow plunged from $711 million to $186 million, while the adjusted figure for this declined from $555 million to $293 million. Also on the decline was EBITDA, which shrank from $605 million to $539 million.

{kind=link}

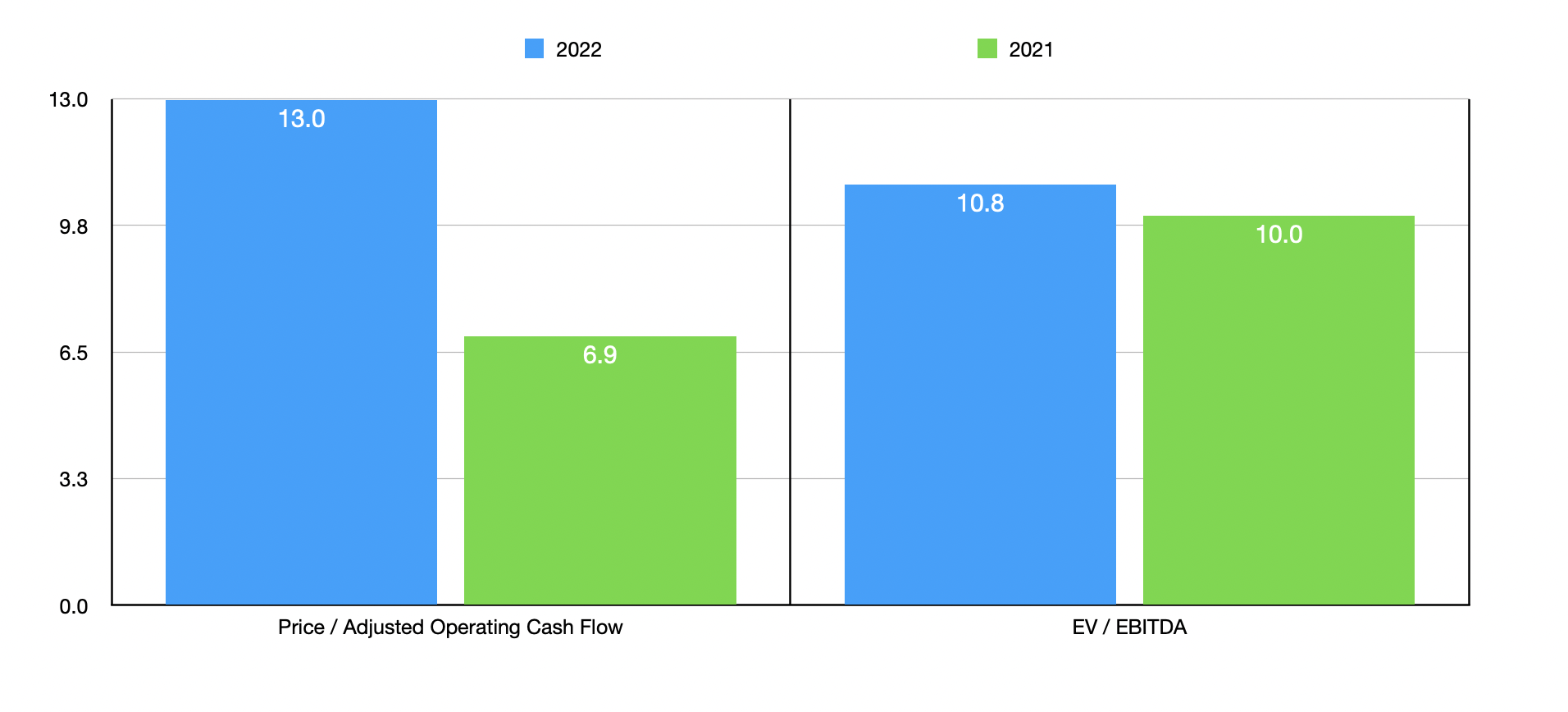

When it comes to 2022 in its entirety, management said that sales should be between $3.75 billion and $3.80 billion. This is higher than the prior expected range of between $3.70 billion and $3.75 billion. Overall organic growth during this time, according to management, should be between 4% and 5%. The only profitability metric that management gave guidance on was EBITDA. This is expected to be between $740 million and $780 million. Previously, the range forecasted was for between $715 million and $755 million. No guidance was given with the other metrics. But if we assume that adjusted operating cash flow should rise at about the same rate that EBITDA should, then we should end up with a reading of $460.9 million. based on these numbers, the company is trading at a price to adjusted operating cash flow multiple of 13 and at an EV to EBITDA multiple of 10.8. By comparison, if we were to use the data from 2021, these multiples would be 6.9 and 10, respectively.

As part of my analysis, I decided to compare Bausch + Lomb to five similar firms. On a price to operating cash flow basis, these companies ranged from a low of 13.6 to a high of 196. In this case, our prospect was the cheapest of the group. Using the EV to EBITDA approach, the range is a bit lower, starting out at 9.5 and ending at 79.4. In this case, only one of the five companies was cheaper than our target.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Bausch + Lomb |

| 13.0 |

| 10.8 |

| ConvaTec Group ( CNVVY ) |

| 21.6 |

| 21.3 |

| Haemonetics ( HAE ) |

| 17.8 |

| 22.4 |

| ICU Medical ( ICUI ) |

| 196.0 |

| 32.2 |

| Neogen ( NEOG ) |

| 54.5 |

| 79.4 |

| Dentsply Sirona ( XRAY ) |

| 13.6 |

| 9.5 |

Takeaway

When I look at a company with worsening fundamentals, I like to ask myself whether the future holds continued pain or if the picture is likely to revert back to the kind of performance it achieved in the past. Considering that much of the pain here seems to be related to supply chain issues and foreign currency fluctuations, the answer to that would be a yes. Although it's important to note that any loss of synergies created from its split from its parent company is likely to be longer-lasting, which does damper its prospects to some degree. In the event that shares were looking pricey right now, I would say that would be a good enough reason to stay away until we have a better idea of how much of an impact that will have permanently. But the good news is that, even if financial results were to stay where they are today, the stock looks affordable. It looks downright cheap if such a return to prior levels occurs.

For further details see:

Bausch + Lomb: Still A Favorable Risk-To-Reward Prospect