HCXY - BDC Weekly Review: Premium Valuations For Internally-Managed BDCs

Summary

- We take a look at the action in business development companies through the third week of February and highlight some of the key themes we are watching.

- BDCs had a strong week, bouncing back due to continuing strong earnings.

- We take a look at some of the reasons internally-managed BDCs tend to trade at elevated valuations.

- And take a peek at some earnings announcements.

This article was first released to Systematic Income subscribers and free trials on Feb. 19.

Welcome to another installment of our BDC Market Weekly Review, where we discuss market activity in the Business Development Company ("BDC") sector from both the bottom-up - highlighting individual news and events - as well as the top-down - providing an overview of the broader market.

We also try to add some historical context as well as relevant themes that look to be driving the market or that investors ought to be mindful of. This update covers the period through the third week of February.

Be sure to check out our other Weeklies - covering the Closed-End Fund ("CEF") as well as the preferreds/baby bond markets for perspectives across the broader income space. Also, have a look at our primer of the BDC sector, with a focus on how it compares to credit CEFs.

Market Action

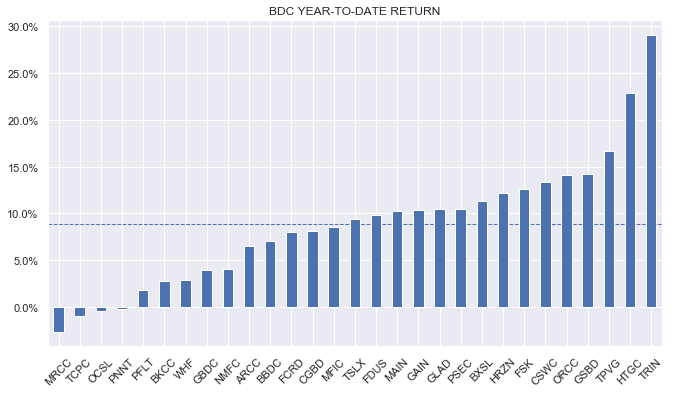

The sector bounced back strongly this week with a 2% total return. As we have discussed in previous weeklies, strong earnings and further dividend hikes continue to support the sector. Year-to-date, the sector is up close to 10%.

{kind=link}

The sector has climbed to a high since the initial drawdown in the early part of last year. In total return terms, BDCs are flat to where they started 2022 - a great result for investors.

Systematic Income

Sector average valuation is trading at 99% - only a few percentage points below its long-term average.

Systematic Income

Market Themes

A subscriber touched on an interesting dynamic in the BDC space of internally-managed BDCs trading at a significantly higher valuation than externally-managed BDCs. Within our 29-name coverage universe which has 4 internally-managed BDCs - [[CSWC]], HTGC, [[MAIN]] and [[TRIN]] - the average valuation of these stocks is 133% versus 94% for the other BDCs. Three of the top 3 BDCs by valuation in our coverage are internally-managed ones. What's driving this dynamic?

In our view, the reasons are two-fold. One, is that internally-managed BDCs tend to have lower management fees, in part because they do away with incentive fees and have only employees to pay rather than a larger management umbrella organization. And two, they tend to have above-average total NAV returns. TRIN has underperformed recently so it could very well slip on this metric but the other three internally-managed BDCs boast significantly higher total NAV returns than the sector average. One reason for this better performance is, of course, the lower fees though that doesn’t explain all of it.

There is a view that internally managed BDCs have better aligned interests between management and shareholders and that drives enhanced performance. It's fair to say that externally-managed BDCs are incentivized to add assets regardless of quality since they get paid more base management fees the more assets there are.

This argument is sensible however it runs into two difficulties. One, a number of externally-managed BDCs boast very strong returns such as ARCC and TSLX without a significant tail of non-accruals or net realized losses. And two, incentive fees accrue on total returns and are large enough that they provide a strong counterincentive to stuffing the company with assets regardless of quality. Finally, if this incentive were a strong factor in performance you would see a significant difference in leverage between internally and externally managed BDCs which you don’t.

Overall, these two reasons are insufficient to explain the performance divergence so there are probably some squishy cultural factors at play as well which would be hard to pin down.

Market Commentary

Sixth Street Specialty Lending ( TSLX ) had a great quarter. The base dividend ticked up by a penny to $0.46 and there was a new $0.09 supplemental declared. Net income rose 36% from the previous quarter (1.5% year-on-year). Total dividend coverage is high at 119%.

The large qoq net income gain was largely due to prepayment fees – a great result in a period of fairly low deal activity.

Systematic Income BDC Tool

The NAV rose by 1%. Portfolio quality was stable with effectively no non-accruals (0.01% of the portfolio). Given its consistent outperformance, TSLX remains pretty decent value at 118%. One way to gauge value here is that dividing the 3Y total NAV return by the valuation gives a figure of 13.7% which is 5.3% above the sector average i.e. given its return profile, TSLX should trade at an even higher valuation. For people who don’t absolutely hate buying stuff at a premium to NAV, TSLX is as good a case to do it. Hercules Capital ( HTGC ) put in a strong quarter. Net income rose 14% as both fees and investment income contributed. Non-accruals rose by 1 to 0.1% by fair-value. Coverage of the base dividend is 121%.

The company upped the base dividend from $0.36 to $0.39 but cut the quarterly supplemental from $0.15 to $0.08 for a lower dividend overall. The base dividend reflects the typical net income bump in the sector while the lower supplemental is likely a function of the now smaller spillover which was a still pretty high $1.03 as of Q4. The valuation of 154% is the second-highest in the sector and is very elevated for the company (it has only been higher 6% of the time over the last 5 years).

Systematic Income BDC Tool

Stance and Takeaways

We made a couple of rotations in the BDC sleeve of our Income Portfolios. We added to the Saratoga baby bond ( SAY ) and ( OCSL ) in equal measure by moving capital from ( PNNT ). We also reduced our ( ARCC ) allocation to add to OCSL.

By the time of the move, PNNT had outperformed OCSL year-to-date so it offered a good time to rotate. ARCC has also outperformed OCSL by around 10% since our original OCSL to ARCC rotation and is less compelling now.

For further details see:

BDC Weekly Review: Premium Valuations For Internally-Managed BDCs