WFCNP - BDJ: An Attractive Covered Call Fund But Valuation Gives Pause

2023-03-21 12:15:46 ET

Summary

- BDJ has been a long-term position in my closed-end fund portfolio.

- The fund is attractive and delivers dependable monthly distributions.

- However, with only a slight discount, I'd be hesitant to consider adding even after financials took a big hit.

Written by Nick Ackerman, co-produced by Stanford Chemist. A version of this article was originally published to members of the CEF/ETF Income Laboratory on March 6th, 2023.

BlackRock Enhanced Equity Dividend Trust ( BDJ ) couldn't buck the bear market of 2022 completely. However, it was able to keep declines minimal due to two specific reasons. First, the portfolio was tilted towards value rather than growth. The second reason was the fund's covered call strategy, while only a slightly defensive strategy, still helped limit losses.

That covered call strategy can also help keep the distributions to investors flowing, even with bear market challenges. All that being said, the fund continues to be at a persistently pesky higher valuation than it historically has traded at. Perhaps this is because other investors are picking up on its otherwise attractive strategy during these sorts of markets.

Since our last update , the fund had been doing well and then was hit by the bank failures. This fund carries a sizeable allocation to financials, making it a larger impact to the fund.

BDJ Performance Since Prior Update (Seeking Alpha)

Overall, the fund remains a hold, but that doesn't mean we current shareholders shouldn't continually evaluate what we are holding. With a new annual report recently posted, now is the perfect time for an update. So, today's article is more of an update piece rather than presenting an idea for a buy. For a longer-term investor, one could consider a dollar-cost averaging approach. Even then, patience for at least a shallow discount would probably be preferable.

The Basics

- 1-Year Z-score: 0.43

- Discount: -0.24%

- Distribution Yield: 8.12%

- Expense Ratio: 0.84%

- Leverage: N/A

- Managed Assets: $1.667 billion

- Structure: Perpetual

BDJ's primary objective is to "provide current income and current gains." The fund intends to achieve this by "investing in common stocks that pay dividends and have the potential for capital appreciation." They concentrate on dividend-paying stocks with "80% of its total assets in dividend-paying equities."

The portfolio is dominated by mostly large-cap stocks, with an average market cap of holdings of over $102.6 billion. Those that can generally offer dividends as their rapid growth days are well behind them.

They will also utilize an option strategy on single stocks within the portfolio to "enhance distributions paid to the Trust's shareholders." This is a common strategy for funds that aren't leveraged as a way to boost higher distributions. This has also benefited BDJ relative to other CEFs leveraged during this rising interest rate time. Leverage costs are rising for those leveraged funds if they aren't hedged, adding more uncertainty at this time. That's what can make a fund such as BDJ relatively more conservative.

This fund also has a rather low expense ratio for a closed-end fund. While being generally higher than most passive ETFs, it's fairly competitive with the average 0.70% expense ratio of actively managed ETFs. Something that not a lot of CEFs can say themselves.

Performance - Strong Relative Results

In 2022 the market experienced a bear market; however, it was hardly felt by shareholders in BDJ. The total share price and NAV declined only over 10% during the depths in October, which have remained the market low for now.

Ycharts

Over the long term, a covered call writing fund such as BDJ will underperform in a bull market. Additionally, being tilted towards value-oriented sectors in most of the last decade meant the upside was given up. However, I believe this helps provide a reason why diversification matters. I can't reliably predict when or how long a bull or bear market may last, but what I can do is make sure that I have funds that benefit each type of environment.

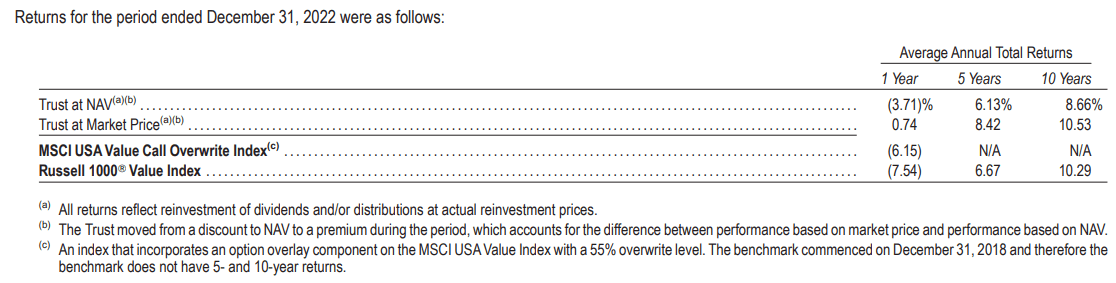

They also put themselves against the Russell 1000 Value Index rather than the S&P 500. They've put up impressive short-term results against that index and their MSCI USA Value Call Overwrite Index, besting both of these benchmarks. Over the longer term, it's been competitive against the Russell Value Index, considering the call-writing component of the fund.

{kind=link}

BDJ Performance Comparison (BlackRock)

During times of volatility, we generally see funds drop to wider than usual discounts. For BDJ, that simply didn't occur. In fact, the discount had only narrowed materially over the last year. Even the latest bout of volatility has done little to shake the fund's higher relative valuation.

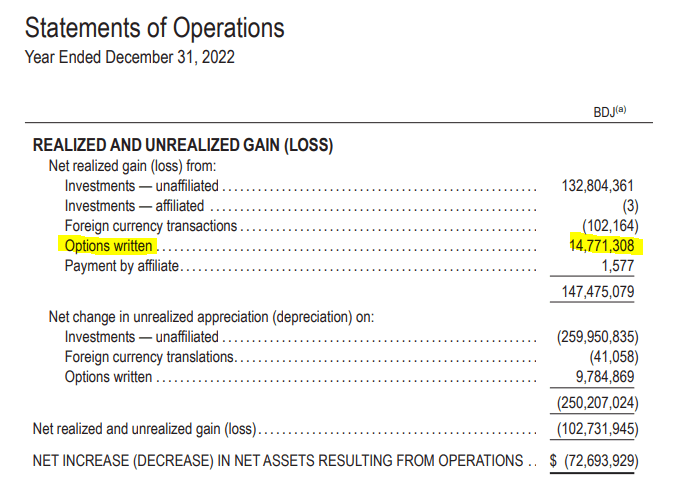

Combining the value-oriented portfolio with the valuation tightening for this fund helped contribute to the fund's results in the previous year. A covered call strategy benefits no matter the market conditions that helped drive realized gains for the fund too.

{kind=link}

BDJ Realized/Unrealized Gains/Losses (BlackRock)

However, it should be noted that it was relatively less than some other call-writing funds. Against its $1.647 billion in total assets, it only works out to gain 0.90% off of that amount. BlackRock Enhanced Capital And Income Fund ( CII ), a sister fund, had written options to contribute a 3.2% return of their total assets: a small absolute difference, maybe, but a significant relative basis.

There can be a number of reasons for this, but a big factor is simply due to underlying portfolio volatility. BDJ's portfolio held up relatively better, meaning less volatility, generally speaking. Since their portfolio held up better, there could have also been cases where they had to close out their covered calls at a loss or 'risk' having the position called away.

Either way, it still helped contribute to a small reason why the fund's declines were less severe.

Distribution - Steady And Sustainable

The fund's current monthly distribution works out to a yield of 8.12%. The fund's NAV rate is 8.10%, being at almost parity with the NAV means these two figures are nearly identical.

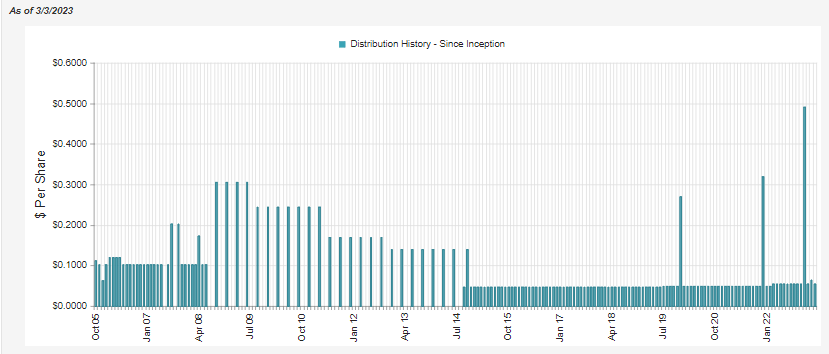

The fund has paid out large year-end specials in the last couple of years. While the fund is susceptible to cuts during longer and deeper bear markets, the current rate seems more than reasonable.

{kind=link}

BDJ Distribution History (CEFConnect)

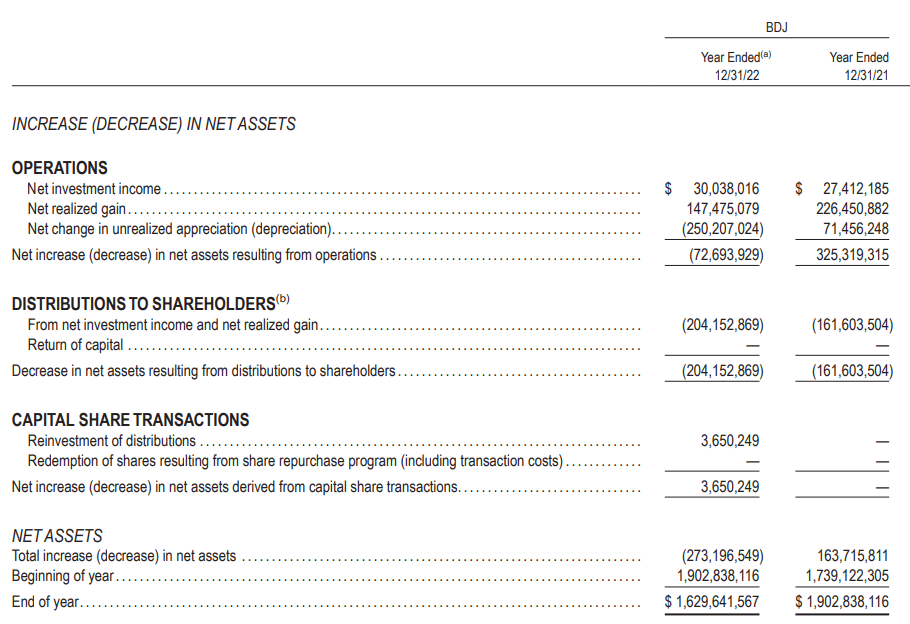

As we already saw above, realized gains from their underlying portfolio and the help of the contributions from their call-writing strategy delivered the gains they needed to fund their distribution. They've also experienced an increase in net investment income over the year, coming in at an increase of nearly 9.6%.

{kind=link}

BDJ Annual Report (BlackRock)

Now that the fund has been flirting with a premium, we will likely see reinvesting of distributions and at-the-market shares driving the total outstanding shares up. This is a positive since, when done at a premium is accretive to NAV for all shareholders.

However, it does make trying to forecast coverage levels harder due to the share count rising an unknowable amount. At the end of 2022, we see 186,416,092 shares outstanding. Annualizing out their monthly $0.0562 gives us $0.6744, resulting in the estimated annual amount paid to around $125,719,012.

The larger amount reflected above from their annual report also reflects the year-end they paid. Given that, the NII coverage for their regular distribution comes to around 24%. The rest would need to be made up from capital gains.

Therefore, even with the written options gains they recorded, they need a sizeable portion of their portfolio to perform well to consider the distribution covered. That can certainly be difficult to achieve in a bear market, but we are still at a sustainable level over time. Given the current levels, I suspect they won't need to cut their distribution.

For tax purposes in 2022 , the fund's earnings are rather consistent with what we see for the tax classifications. That is primarily long-term capital gains and qualified dividends. That can make it more appropriate for a taxable account, given the tax-friendliness of these tax classifications.

{kind=link}

BDJ Distribution Tax Classification (BlackRock)

BDJ's Portfolio

Interesting to note, and what I mentioned in our previous update persists even now. That is, BlackRock is often fairly regular with updating information on their funds. Most of their funds are reflecting January 31st, 2023, holding information. For whatever reason, BDJ's website seems to be stuck on the September 30th, 2022, reporting for holdings and exposure breakdowns. That being said, we still have the December 2022 information available from their annual report.

The fund remains heavily tilted towards healthcare and financials, belonging to the more value-oriented sectors. One reason I find BDJ appealing is that it is fairly differentiated from the mostly tech-heavy positioning of other funds. However, the bank failures lately have certainly put pressure on the financial space.

That being said, they still have a meaningful allocation to tech; it isn't completely absent from the fund. Their energy sleeve also would have contributed to some of the fund's success last year.

BDJ Sector Allocation (BlackRock)

Given the fairly elevated portfolio turnover in the last year of 81%, there wasn't an overly dramatic shift in the fund. At the beginning of 2022 , financials made up 25.72% of the fund, and healthcare was 21.09%.

Overall, we can see that the fund's fairly balanced with diversification despite their rather low 78 counts for the number of holdings.

When we see a limited number of holdings, the top ten usually make up a significant part of the portfolio. That actually doesn't appear to be the case with BDJ, and once again, they reflect a fair bit of diversification with no position at over 3% of the weighting.

BDJ Top Ten Holdings (BlackRock)

Banking giants Wells Fargo ( WFC ) and Citigroup ( C ) have remained in significant positions in the portfolio over the last year. Those two have helped contribute to the fund's weighting to financials. That being said, the weightings in these holdings fell from 4.02% and 3.14%, respectively. Worth noting is that these aren't the regional banks that are having issues but are being dragged down nonetheless. In fact, they could be beneficiaries in the longer run.

At the beginning of 2022 , they held 1,521,080 shares of WFC. That had been reduced to 1,108,398 at the end of 2022. They held 925,758 shares of C, but they actually increased that a bit to 957,550 shares.

BP ( BP ) was a riser in their portfolio, previously the 10th largest holding at a weight of 2.03%. The share count for that name went from 7,597,042 to 7,828,407. So besides strong relative performance, the increase in share count helped push that name to a now 2.9% holding.

Enterprise Products Partners ( EPD ) was another energy name that had moved up from a 2.08% weight to a 2.4% weight. The unit count on that name went from 1,487,454 to 1,542,031.

Here's a look at these four names' price performance in the last rolling 1-year period to help reflect just how strongly BP had performed. Even with EPD in the energy space, as an MLP, they didn't participate in the upside nearly to the same degree.

Ycharts

Conclusion

I continue to believe that BDJ is positioned well for the current environment. Their covered call writing strategy has also been beneficial. Perhaps not as beneficial as some of their 'peers,' but that's primarily due to their underlying portfolio being better positioned in value-oriented plays. That being said, the valuation at this time just isn't tempting. Historically, we've seen this fund trade at a discount, and it would have to get back there before I was a buyer. On the other hand, those already holding don't necessarily have to consider rushing out the door as we aren't at a level of gross overvaluation, in my opinion.

For further details see:

BDJ: An Attractive Covered Call Fund, But Valuation Gives Pause