PAGP - Better High Yield Buy: Enterprise Products Partners Or Plains All American?

2023-09-21 07:45:00 ET

Summary

- Both Enterprise Products Partners and Plains All American Pipeline offer investors high yields and investment grade credit ratings.

- EPD has a better long-term track record, but Plains has massively outperformed EPD over the past three years.

- We compare them side-by-side and offer our take on which is the better buy today.

Plains All-American Pipeline ( PAA )( PAGP ) and Enterprise Products Partners ( EPD ) are high-yielding investment-grade energy midstream businesses. In the past, we have been very bullish on Plains, but its stock has significantly outperformed the midstream sector ( MLPA ) over the past year:

As a result, we are now re-evaluating it to see if it is still an attractive buy at these levels. Moreover, we are comparing it to another one of our favorite midstream businesses - EPD - which has also had a good, albeit less impressive, run to see which is the better buy today.

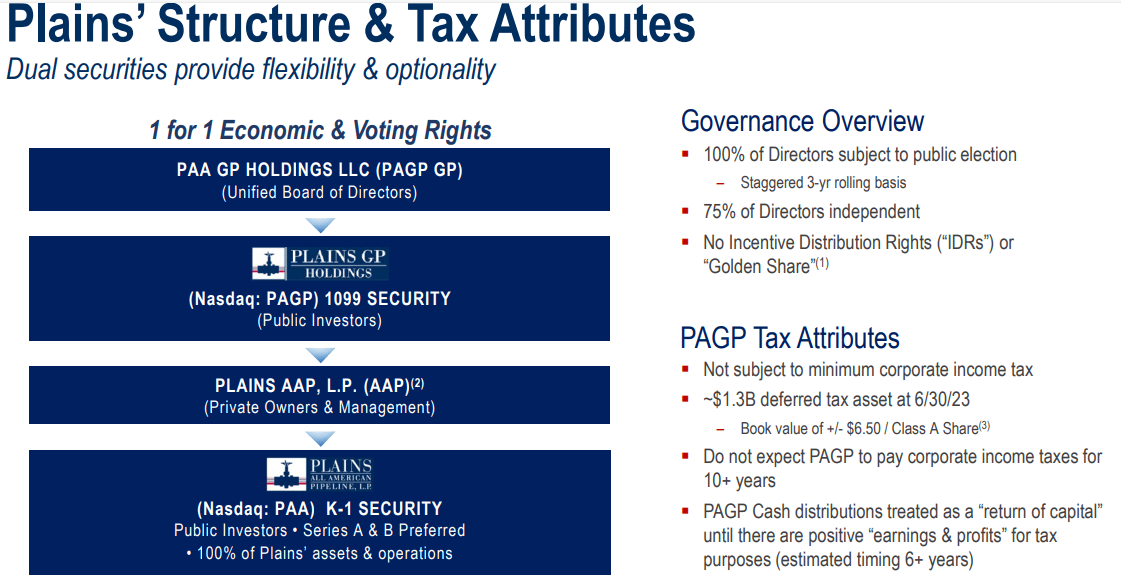

Note that in this article, we will be comparing EPD to both PAA and PAGP. PAA and PAGP are economic equivalents to each other, but PAA issues a K-1 tax form while PAGP issues a 1099 tax form. PAGP typically trades at a premium to PAA due to the additional convenience provided to many tax filers for its 1099 tax form compared to the more complicated K-1 tax form issued by PAA. The differences between PAA and PAGP are explained pretty well here:

{kind=link}

EPD Stock Vs. PAA/PAGP Stock: Business Models

EPD is often considered to have a better business model than Plains has, as evidenced by its better and more consistent returns on invested capital:

EPD also has a far more impressive distribution growth track record than Plains does. While EPD has grown its distribution for 25 consecutive years, Plains has suffered several painful distribution cuts:

As a result, it should come as little surprise that EPD has delivered total returns that crush those generated by Plains over the long-term:

On the other hand, Plains has significantly outperformed EPD over the past three years:

With this in mind, let's take a closer look at the underlying asset portfolios of each of these MLPs.

First and foremost, both businesses generate pretty stable cash flows, with the vast majority of their cash flows coming from long-term, commodity-price-resistant contracts. This provides good visibility into supporting their distributions, continuing to deleverage their balance sheets, and invest in growth projects moving forward, regardless of where energy prices head.

EPD has one of the best portfolios in the midstream sector, well-diversified by asset type, energy commodity, and geographical presence as evidenced by its four distinct business segments: NGL Pipelines & Services, Crude Oil Pipelines & Services, Natural Gas Pipelines & Services, and Petrochemical & Refined Products Services. Moreover, its business model is fully integrated and it has assets that enjoy durable competitive advantages due to their strategic location and also typically provide management with plenty of opportunities for high-returning organic growth investment opportunities as well as synergistic bolt-on acquisitions.

EPD Asset Portfolio (Investor Presentation)

EPD insiders are also very well aligned with unitholders given that they own ~32% of EPD's equity, an alignment that is reflected in the firm's conservative posture, impressive distribution growth and total return track records, and consistently high returns on invested capital.

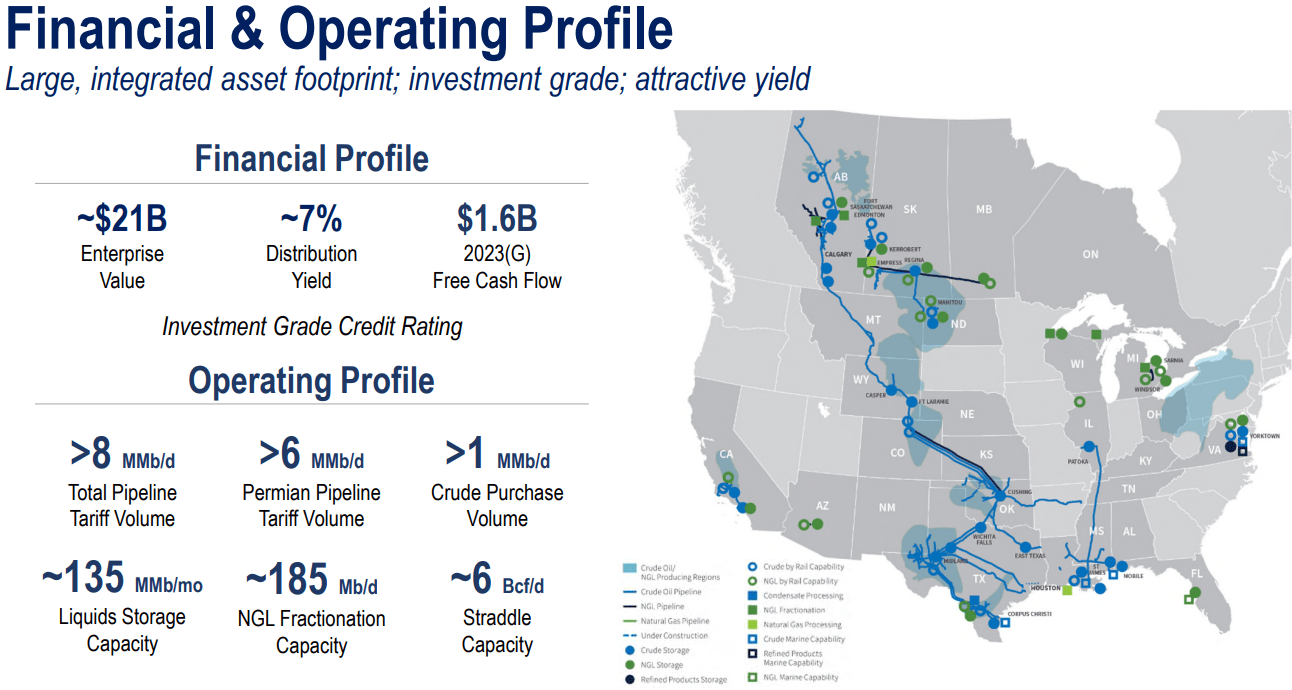

Plains, meanwhile, does not have nearly the diversification that EPD enjoys. However, it still owns some high-quality assets, particularly its Permian crude oil business which is likely benefiting from the current boom in oil prices.

{kind=link}

Its business model is divided into two main business segments: its crude oil business (primarily based in the Permian basin) and its NGL business. ~83% of its 2023 expected adjusted EBITDA comes from its crude oil business and the remaining ~17% of its 2023 expected adjusted EBITDA comes from its NGL business.

While its Permian business is definitely its core operation, Plains still feels strongly about the value added by its NGL business and would only sell it if it felt it was getting a very attractive price offered for it. It has largely completed its dispositions of non-core assets over the past several years and feels good about investing in its current portfolio to position the business for long-term growth.

That being said, EPD's business model currently provides it with far more growth investment opportunities than Plains has, so EPD is pouring much of its cash flow into growth investments whereas Plains has been focused primarily on paying down debt and growing its distribution. Both EPD and Plains have made modest opportunistic unit repurchases in recent years as well.

EPD Stock Vs. PAA/PAGP Stock: Balance Sheets

While both businesses have seen their respective leverage ratios decline substantially in recent years, EPD has the clear edge here with its A- credit rating from S&P compared to Plains' BBB- credit rating from S&P.

EPD's A- credit rating is well deserved too, given its extremely conservative 3.0x leverage ratio, whopping $4 billion in liquidity, weighted average term to maturity on its debt of 19.7 years with 51% of its debt not maturing for 30 or more years, and 96.7% of its debt having a fixed interest rate of 4.6% on a weighted average basis. Last, but not least, it is able to fully fund its growth investment pipeline and distribution from cash flow, removing any need for it to access capital markets other than for occasional debt refinancings (although it could also pay these down if it wanted to reduce its growth project budget). As a result, it is not only at very low risk of financial distress, but it also is relatively immune to changes in capital market conditions, putting it on a very firm footing and giving it enormous flexibility to deliver value for unitholders for years to come.

Plains, meanwhile, has worked very hard since late 2020 to improve its balance sheet. It has dramatically reduced its capital expenditures from over $2 billion in 2018 to about one-quarter of that number today by selling off non-core assets and dramatically reducing its growth investment capital. As a result, it is now able to fully self-fund all capital expenditures in addition to its distribution, removing its dependence on capital markets to deliver value to unitholders.

It has also paid down debt very aggressively, deleveraging from a 4.5x ratio in 2021 to an expected year-end leverage ratio below 3.5x in 2023. With a weighted average term to maturity of ~10 years and a positive outlook from S&P, it appears that Plains could have an upgrade to BBB in store in the near future and is in little danger of financial distress.

EPD Stock Vs. PAA/PAGP Stock: Distribution Outlook

EPD's distribution outlook is good at an expected ~5% CAGR for the foreseeable future and this growth rate should be very dependable given its rock-solid financial shape and impressive asset portfolio. EPD's 2023 distributable cash flow is expected to cover its distribution this year by 1.74x, further enhancing the perceived safety of its payout.

Meanwhile, Plains has a particularly exciting growth outlook for its distribution, as management is driving to grow its distribution aggressively until its DCF coverage ratio is down to ~1.6x. As a result, analysts forecast a 13.7% distribution per unit CAGR through 2025 and a 9.3% distribution per unit CAGR through 2027. As a result, we find Plains' distribution growth potential to be much more exciting than EPD's over the next half decade.

EPD Stock Vs. PAA/PAGP Stock: Valuations

When it comes to valuation, it appears to be quite close:

| Metric |

| EV/EBITDA |

| 5-Yr EV/EBITDA |

| P/DCF |

| Distribution Yield |

| PAA |

| 9.15x |

| 9.12x |

| 6.62x |

| 7.5% |

| EPD |

| 9.35x |

| 9.97x |

| 7.84x |

| 7.6% |

PAA is clearly cheaper than EPD on a P/DCF basis, but this makes sense given that it has a much higher leverage ratio. However, on an EV/EBITDA basis, the comparison gets much tighter, and relative to their respective five-year averages, EPD is actually cheaper. EPD also has a slightly higher NTM distribution yield.

Also, note that to buy PAGP instead of PAA you will have to pay a 4.4% premium as of this writing, which brings its distribution yield down to 7.3%.

EPD Stock Vs. PAA/PAGP Stock: Investor Takeaway

Both midstream businesses are performing well and have very healthy balance sheets and business fundamentals. EPD clearly wins the quality competition with its vastly superior track record, business model, and balance sheet. However, Plains offers investors a much more exciting distribution growth profile, while offering a similar current yield.

We currently favor EPD because - on an EV/EBITDA basis - they are trading at nearly the same price, but with EPD you get much better quality for your money and a larger historical discount. As a result, EPD offers superior risk-reward to Plains. Consequently, we rate EPD as a Buy and Plains as a Hold.

For further details see:

Better High Yield Buy: Enterprise Products Partners Or Plains All American?