EVEX - Between eVTOL Elation And Lilium's Limitations

2023-08-15 14:28:02 ET

Summary

- I believe Lilium reveals a company with a unique focus on the eVTOL premium segment but has notable challenges and lacks near-term catalysts to keep investors engaged.

- Lilium's 1H23, in my view, shows a firm striving for commercialization and near-term financial stability, but still facing technical and financial headwinds throughout 2025.

- Given the intricate dance between Lilium's potential and its challenges, my investment stance is clear: Hold.

For those keeping tabs on the exciting and rapidly evolving electric vertical takeoff and landing (eVTOL) industry, the story of Lilium N.V. ( LILM ) is nothing short of extraordinary. Emerging as a pivotal player with a dedicated focus on premium segments and backed by groundbreaking propulsion technology, Lilium's trajectory is one that demands attention from investors, technophiles, and aviation enthusiasts alike. In an industry where innovation, agility, and foresight are key, Lilium stands out as a promising yet risky venture. After an exhaustive analysis of their recent 1H 2023 reports, cross-referencing industry trends, and delving into comparative financials, I am initiating a "Hold" stance on Lilium ( LILM ).

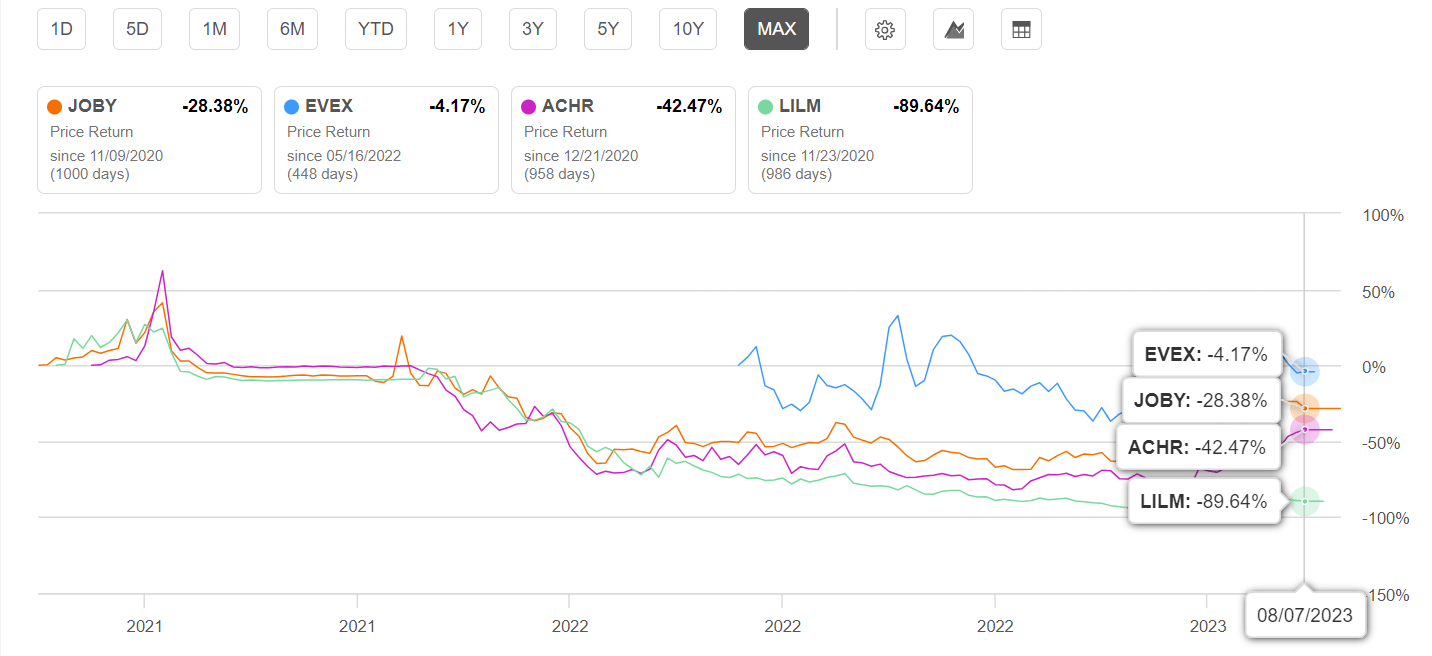

As I see it, they are trading roughly in-line with competitors like Eve ( EVEX ) and Archer Aviation ( ACHR ), yet they lack the short-to-mid-term catalysts to outperform. Interestingly, I find myself more optimistic on LILM compared to Joby Aviation ( JOBY ) (see my “sell” case for JOBY here ). But, if you're looking for my eVTOL top pick, it's Eve Holding ( EVEX ), as per my “buy” thesis still resonates strongly with the ongoing market dynamics.

Lilium – 1H 2023 Highlights

1Q23 Recap – A Steady March To Commercialization

The Q1 results pr ovided notable insights into Lilium’s progress to commercialization, and below I highlight what stood out to me:

- Certification Progress – Lilium’s strides towards EASA certification showed great progress, achieving 78% Means of Compliance and having 100% of Certification Plans accepted.

- Focus on OEM Sales – With 645 units under MOU, up from 640 in the previous quarter, Lilium continues to target premium segments, aiming to convert these into binding orders

- Financing – €62M spending in Q1 and expected €125M in 1H23 showed strategic planning, but the need to raise additional capital in 2024 highlighted challenges in balancing growth and capital expenditure

My takeaway from Q1 is that wile the company demonstrated great intent and planning, technical challenges and significant cash burn slowed down its growth pace.

2Q23 Review – Gaining Momentum But Still Some Turbulence

The Q2 Shareholder Letter revealed continuous progress, with a few areas that particularly caught my attention:

- EASA Certification On Track – Agreement on 78% of its Means of Compliance remains unchanged from Q1, pointing to stability but also a risk of delays if progress stalls in 2H23

- Increased Sales Pipeline – With an additional 105 units Q/Q, interest from China and the Middle East, and suppliers for 90% of BoM selected, Lilium is positioning itself for initial assemble very well

- Near-Term Liquidity Secured – Lilium’s recent capital raise of $192M and total liquidity of $386M is reassuring. However, the ramp-up in cash burn into 2024 and expected adj cash burn of €170M in 2H23 underscores the financial obstacles, in my view

My reading of the Q2 data is that Lilium is similar to Q1: Lilium is progressing, but the balanced risk/reward profile and the potential technical challenges still advocate caution, and there are a substantial lack of catalysts to keep investors engaged.

LILM My Hold Investment Case

Lilium is arguably one of the highest-risk bets in the eVTOL market, particularly due to its sharp focus on premium OEM sales backed by innovative propulsion tech, and the lower market cap in comparison to peers.

1.0 The Bull Case: Reasons To Buy

- Differentiation – Lilium’s strategy of targeting the premium segment offers a distinct competitive edge in the eVTOL landscape:

{kind=link}

Lilium_Investor_Presentation_August_2023

- Technical Superiority – the firm’s aircraft blueprint promises unique benefits, such as reduced noise and elevated payloads, potentially setting the stage for increased consumer preference and adoption

- Short-term Financial Stability – the recent fundraising endeavors have efficiently addressed immediate liquidity concerns, instilling increased confidence in the firm’s ability to maneuver financial hurdles

- Valuation – in comparison to JOBY, ACHR, and EVEX, Lilium appears to have the most attractive relative valuation in terms of P/B, and cash as % of equity, which could reduce the risks of buying at today’s prices. See below:

{kind=link}

Author's Data

- eVTOL Potential – the larger eVTOL market is primed for exponential growth. An investment in Lilium represents a stake in this high-growth, transformational sector. Additionally, LILM has strong partnerships in place, with an expected timeline to certification by 2025 as shown below:

{kind=link}

Lilium_Investor_Presentation_August_2023

However, I have reason to believe that the 2025 certification date is set too early and explained my rationale for this timeline in my “sell” investment case for JOBY . Here is a brief overview of that:

The FAA’s recently released Advanced Air Mobility (AAM) Implementation Plan is akin to a sobering splash of cold water. It outlines a measured "crawl, walk, run" approach, setting 2028 as a more pragmatic target year for meaningful operations. While some optimists may clutch onto the mention of 2025 for potential operations, I argue that full-scale commercial eVTOL usage is likely a story for the later part of the decade

With this in mind, I am not setting a price target on Lilium, as I believe the company projections are entirely unpredictable and not reflective of their intrinsic value.

2.0 The Bear Case: Reasons To Sell

- Capital Concerns – With projected investments in infrastructure and tech, I foresee potential capital raises in FY24 and beyond. Thus, leading to potential dilution for existing shareholders. Especially with Lilium’s market cap at ~$560M, as of writing, this means that (for example) a $100M share dilution will significantly dilute shareholders in comparison to JOBY (~$5.3B market cap), EVEX (~$2.3B), and ACHR (~$1.46B)

- Comparative Catalysts – In the near-term, Lilium appears to lag behind its peers in terms of market performance and actionable catalysts that can excite and retain investor interest. For some context, see Lilium’s 2Q23 Shareholder Letter , page 18, where the only upcoming catalyst is the 3Q23 business update:

{kind=link}

Lilium_Investor_Presentation_August_2023

LILM’s competitors such as EVEX and JOBY have numerous upcoming catalysts in the next 12 months to keep investors engaged and LILM is largely lagging behind in this case.

- Inherent eVTOL risks – the eVTOL segment, though brimming with potential, comes with its own set of challenges. Certification, commercialization, competition, and other regulatory bottlenecks

3.0 Lilium’s Stock Story So Far

At just over a dollar, LILM stock promises an adrenaline-packed journey. Since the beginning of January, the stock has seen a modest depreciation of ~6%. However, looking back, it’s down by 60% over the past year and a staggering ~90% since its public debut. Despite this downward trajectory, Wall Street still sees potential, with the avg price target for LILM hovering at $3.0, suggesting a whopping ~150% upside. See below:

{kind=link}

Seeking Alpha

While the figures might be daunting, it’s worth noting that Lilium still garners a moderate ‘buy’ consensus among industry analysts . However, it’s essential to tread with caution. With the company still in its pre-revenue phase , any investment in Lilium at this juncture is speculative.

Discounted Cash Flows Analysis

Setting a definitive price target for Lilium at this stage feels premature. The anticipated 2025 commercialization, in my view, presents an optimistic scenario, and I'd argue that pegging Lilium's price solely based on its intrinsic valuation via a DCF might not capture the entire picture. Still, this DCF exploration offers a glimpse into a best-case scenario, helping investors understand consensus estimates through 2030 and potential intrinsic value points for Lilium.

{kind=link}

DCF Analysis (Author's Data)

I've leaned towards a somewhat aggressive 21.2% WACC when discounting Lilium's UFCF. Though the initial computation landed at 11.2%, I've layered on a 10% firm-specific risk premium. This adjustment gives weight to the unpredictable elements linked with eVTOL commercialization, potential regulatory hiccups, and the ebb and flow of competition. To determine Lilium's intrinsic value, I've incorporated a 1% TGR and a 10.0x EBITDA multiple.

{kind=link}

Calculation of Firm Value (Author's Data)

The notable variance between the exit multiple and perpetuity growth methods underscores another reason I've abstained from pinning a price target on Lilium. I also entertained a few different scenarios, pondering the timelines of Lilium's eventual commercialization. My optimistic forecast leans towards approval by late 2025 to early 2026. A more grounded projection eyes late 2026, while a more pessimistic view stretches to 2028, coupled with intensified competition and a dwindling market share.

LILM Sensitivity Analysis (Author's Data)

The accompanying illustration sketches out Lilium's potential risk/reward landscape up to, perhaps, the end of 2025. Should everything align—the preservation of their competitive edge, minimal regulatory hitches, and a timely commercialization by late-2025—their intrinsic valuation might hover around $6 a share. A more pragmatic lens, expecting commercialization by late-2026 and factoring in a 12.5x EBITDA multiple, a 2% terminal growth rate, plus a 10% firm-specific risk premium, circles closer to ~$3.3 a share as a representative valuation by 2025. On the other hand, in a scenario where competitors overshadow Lilium, regulatory hurdles multiply, and commercialization drags to 2028, the path to calculating Lilium's intrinsic value becomes foggy, with potential for a staggering 90%+ drop by 2025.

Crunching these numbers was an intriguing exercise. Who's to say? Lilium's stock could skyrocket 1,000% by 2025 given some favorable winds in upcoming quarters. But for now, given the clouds of uncertainty hovering over Lilium, pinning down an intrinsic valuation remains a challenge. Consequently, I'm refraining from setting a definitive price target for Lilium.

Conclusion

Going through the eVTOL market is akin to piloting through uncharted skies, and Lilium's journey is one that I've followed with both curiosity and caution. The more I analyzed Lilium, the more I found myself appreciating its innovation and yet recognizing its obstacles.

In my analysis, the "Hold" stance on Lilium emerged not from a lack of promise but rather from a complex interplay of factors. From its exciting technical superiority to its somewhat alarming capital concerns, Lilium's path is neither a straightforward ascent nor a precipitous fall.

So here's where I stand: I'm holding on LILM, not because I don't believe in its potential, but because I see a company in a delicate dance with both opportunity and challenge. Lilium has the ingredients for success, but the recipe is still being perfected. Finally, I see LILM as fairly valued at current prices due to a lack of catalysts and differentiation in the medium-term, and remain bullish on my personal pick of the crowd, EVEX.

For further details see:

Between eVTOL Elation And Lilium's Limitations