KIO - BGB: A Solid Income Fund With Limited Interest-Rate Risk

2023-12-08 01:54:06 ET

Summary

- The Blackstone Strategic Credit 2027 Term Fund offers a current distribution yield of 11.08%, comparable to other fixed-income funds.

- The fund has outperformed the broader bond market, with a 3.37% increase in shares compared to a 1.47% decline in the Bloomberg US Aggregate Bond Index.

- The fund primarily invests in floating-rate senior loans and high-yield junk bonds, which provide stability and potential income growth in a rising interest rate environment.

- The Fed seems unlikely to cut rates to the degree that the market expects, so it could be a good idea to hold a fund like this as a hedge.

- The fund's distribution is fully covered with NII, and it is trading at a double-digit discount.

The Blackstone Strategic Credit 2027 Term Fund ( BGB ) is a closed-end fund that income-focused investors can use to achieve their goals. This is immediately apparent in the fund’s 11.08% current distribution yield, which is easily on par with the yields currently being offered by comparable fixed-income funds. There may admittedly be some readers who get concerned when they see a fund with such a high yield, as for most of the past twenty years or so a double-digit yield was a sign that a fund could be overdistributing and be forced to cut the payment soon. However, this is no longer the case, as the Bloomberg High Yield Very Liquid Index ( JNK ) currently yields 8.32% in today’s much higher interest rate environment. It is not that difficult to get this up into the double-digits with the application of a moderate amount of leverage.

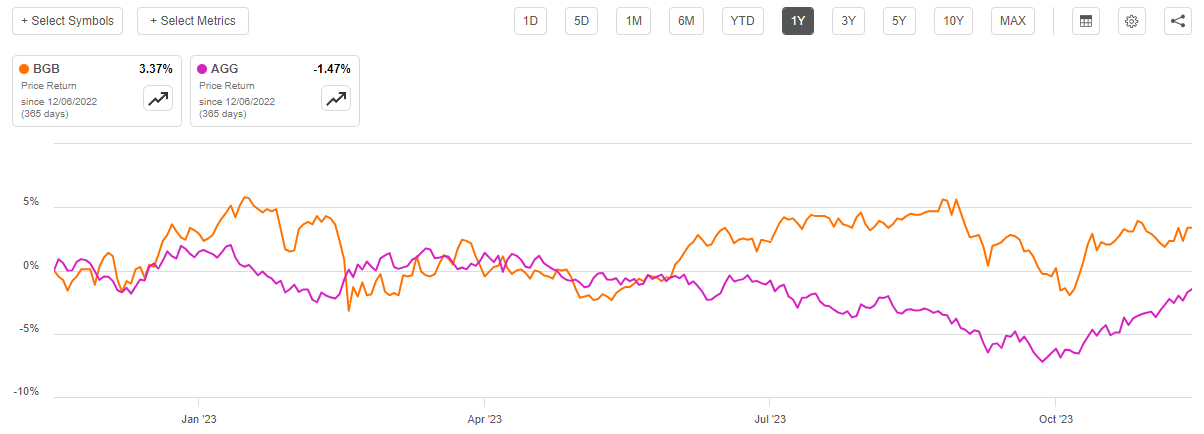

As everyone reading this is certainly well aware, the fixed-income market has not been especially strong lately as bond prices have generally declined over the past two years in response to the Federal Reserve tightening monetary policy and raising interest rates in an attempt to reduce the high level of inflation plaguing the American economy. However, the Blackstone Strategic Credit 2027 Term Fund has held up much better than the broader bond market. Over the past year, shares of this fund are up 3.37% compared to a 1.47% decline in the iShares Core U.S. Aggregate Bond ETF ( AGG ):

{kind=link}

The fund that the fund’s share price has outperformed the aggregate bond index does not tell the whole story, however. As is the case with most closed-end funds, the Blackstone Strategic Credit 2027 Term Fund delivers most of its overall returns in the form of direct payments to the fund’s shareholders. In fact, the fund generally aims to keep its net asset value relatively stable while paying out all of its net investment profits to the investors. As such, we should consider the fund’s distribution when analyzing its performance. When we do this, we see that the Blackstone Strategic Credit 2027 Term Fund delivered a 14.45% total return over the past twelve months. This is not only substantially better than the aggregate bond index, but it even beats the Bloomberg High Yield Very Liquid Index that tracks junk bond returns:

{kind=link}

As such, there could be a lot for income investors to like with respect to this fund. Let us investigate it further to determine if this is indeed the case.

About The Fund

According to the fund’s website , the Blackstone Strategic Credit 2027 Term Fund has the primary objective of providing its investors with a high level of current income. This makes a lot of sense considering the strategy that the fund employs to achieve this objective, which is also described on the website:

Blackstone Strategic Credit 2027 Term Fund is a closed-end fund that trades on the New York Stock Exchange under the symbol “BGB”. BGB’s primary investment objective is to seek high current income, with a secondary objective to seek preservation of capital, consistent with its goal of high current income. BGB invests primarily in a diversified portfolio of loans and other fixed income instruments of predominantly US corporate issuers, including first- and second-lien loans (“Senior Secured Loans”) and high yield corporate bonds of varying maturities. BGB must hold no less than 80% of its Managed Assets in credit instruments comprised of corporate fixed-income instruments and other investments (including derivatives) with similar economic characteristics. The Fund has a limited term and will dissolve on or about September 15, 2027, absent shareholder approval to extend such term.

This description essentially states that the Blackstone Strategic Credit 2027 Term Fund invests in a combination of floating-rate senior loans and high-yield junk bonds. This makes it pretty similar to some of the other funds that we have discussed over the past few weeks. For example, the Apollo Tactical Income Fund ( AIF ), the Ares Dynamic Credit Allocation Fund ( ARDC ) and the KKR Income Opportunities Fund ( KIO ) employ a similar strategy. For the most part, this strategy works pretty well in the current environment. After all, most senior secured loans are floating-rate securities, and these tend to outperform traditional fixed-rate bonds when interest rates increase. However, they tend to underperform fixed-rate bonds when interest rates decline due to the fact that they do not really increase in price in such an environment. For example, the BBG Floating Rate Notes 5 Yrs. Or Less Index ( FLOT ) has been almost perfectly flat over the past ten years:

{kind=link}

This is despite the fact that there were some changes in interest rates during that period, including the Federal Reserve’s attempt to tighten in 2018 and the ongoing attempt since the start of 2022. Thus, we can assume that the fund’s floating-rate bond portfolio will provide a certain amount of protection against rising interest rates. In fact, rising interest rates actually benefit the holders of these securities because that causes these securities to pay their investors a larger level of income. As such, the presence of these securities in the fund’s portfolio has almost undoubtedly caused its income to increase over the past two years.

Naturally, though, the fund’s ability to derive a growing income from the floating-rate securities in its portfolio is directly proportional to the amount of such securities that it owns. As of the time of writing, approximately 84.8% of the fund’s assets are invested in floating-rate securities:

Fund Fact Sheet

That is relatively in line with Blackstone’s other funds, which are all largely invested in floating-rate senior secured loans. This explains why this fund has managed to outperform traditional bonds over the past year or two, as these securities held their value and increased their interest payments while traditional fixed-rate bonds did not.

However, since about mid-October, the market has been widely anticipating that interest rates will decline over the next year. As I have pointed out a few times, the market is currently pricing for a federal funds rate of 4% to 4.25% at the end of 2024, which would be about 125 basis points of cuts over the next twelve months. A simple look at my Twitter feed suggests that people are widely believing that this will be the case, as I am seeing at least one person a day saying that there will be either five or six rate cuts over the next twelve months.

This fund is only partially positioned for such a scenario, should it actually play out. We can see that 15.1% of the fund’s portfolio is invested in junk bonds, which are generally fixed-rate securities that should appreciate in value if interest rates decline. That is nowhere near the 50% or so exposure that the Ares Dynamic Credit Allocation Fund currently has. It is certainly nowhere near the exposure that some of the pure junk bond funds that we have discussed in recent weeks have. As such, this fund is probably not as good as some other funds if interest rates decline significantly since the floating-rate securities will deliver a lower level of income to the fund as interest rates decline, and the fund does not have sufficient exposure to fixed-rate securities to make up the difference through capital gains. It is still better than a pure floating-rate fund in this respect, though, and there is nothing preventing the fund from increasing its junk bond exposure should market conditions become favorable to such a strategy.

With that said, it seems rather unlikely that the Federal Reserve will actually cut the federal funds rate to anywhere near the degree that the market is currently anticipating. As Simon White, Bloomberg’s macro strategist, points out , the Federal Reserve typically never cuts short-term interest rates by 125 basis points in a single year except in cases of a severe recession:

Zero Hedge/Data from Bloomberg

Per Mr. White:

There has only been one occasion, in the mid-1980s, when the Fed has cut rates by more than this amount at a non-recessionary time (i.e. not immediately before, during, or after a recession.

As such, barring a very severe recession, it is highly likely that the market is wrong about interest rates going down by 125 basis points. Realistically, unless there are massive layoffs that push the unemployment rate up to close to 6% (circa 2008, during the lead-up to the Great Recession) within the next three months, it is almost certain that the Federal Reserve will not cut rates to the degree that the market is currently anticipating. Personally, I find that scenario highly unlikely considering that 2024 is an election year and the politicians in Washington will probably use every tool at their disposal to avoid such a severe recession. If the market is wrong about interest rates, it will punish fixed-rate bonds and probably stocks. Floating-rate securities should do just fine though, so this fund appears to be well-positioned for the scenario that the market is incorrect with respect to its interest rate projections. That could be a good thing considering how unlikely it is that the market is right.

As I have pointed out a few times in the past, one of the defining characteristics of floating-rate loans is that they tend to be issued to companies that have relatively weak balance sheets or very large amounts of debt. After all, in the case of these securities, the company is taking on the interest rate risk as opposed to the investor. The only reason that a company would willingly take on such a risk is if it had difficulty obtaining financing through more traditional channels. This is something that may be concerning to more risk-averse investors since a company that already has a lot of debt or has a very weak balance sheet could struggle to make its debt payments and thus expose the investor to the risk of losses when it defaults. Fortunately, the Blackstone Strategic Credit 2027 Term Fund appears to be taking measures to protect its investors against such risks.

One of the measures that the fund is employing to protect its investors against default losses is ensuring that it does not have outsized exposure to highly risky securities. We can see this by looking at the credit ratings of the securities in the fund’s portfolio. Here is a brief summary:

Fund Fact Sheet

An investment-grade security is anything rated Baa or higher by Moody’s. As we can clearly see that only accounts for 0.2% of the portfolio’s assets. Thus, essentially all of the debt securities that are held by this fund are junk-rated debt. However, we can see that fully 90.8% of the fund’s assets are invested in securities that are rated either Ba or B, which are the two highest possible ratings for speculative-grade debt. According to the official bond ratings scale , companies whose securities have one of these ratings have sufficient financial capacity to carry their debt and avoid default even if a short-term economic shock occurs. The market is clearly predicting that such a shock will occur within the next few months, so that is a risk that we should consider. When we consider that most of the companies in the portfolio should have sufficient financial resources to weather a recession though, we should be able to sleep reasonably well at night with this fund’s portfolio. That is especially true when we consider that the average position size of a single issuer is only 0.22% of the fund’s assets. As such, any single default should not have a noticeable impact on the fund’s overall portfolio.

Leverage

As is the case with most closed-end funds, the Blackstone Strategic Credit 2027 Term Fund employs leverage as a method of boosting the effective yield of the assets in its portfolio. I explained how this works in a number of previous articles. To paraphrase myself:

In short, the fund borrows money and uses that borrowed money to purchase floating-rate debt securities and junk bonds. As long as the yield that the fund receives from these purchased assets is higher than the interest rate that it has to pay on the borrowed funds, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, that will ordinarily be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much leverage because that would expose us to an excessive amount of risk. I generally do not like to see a fund’s leverage exceed a third as a percentage of its assets for this reason.

As of the time of writing, the Blackstone Strategic Credit 2027 Term Fund has leveraged assets comprising 35.34% of its assets. As such, it exceeds that one-third limit that I generally would prefer from a risk-management perspective. However, in this case, it is probably acceptable. This fund is invested primarily in floating-rate debt securities, which tend to be incredibly stable in terms of price. As such, the risks of using leverage are lower than they would be if the fund were invested in more volatile assets such as common stocks. When this is combined with the fact that the fund’s leverage does not significantly exceed the one-third level, it is probably fine as far as the balance between risk and reward is concerned. We should not really need to worry too much about the fund’s leverage.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the Blackstone Strategic Credit 2027 Term Fund is to provide its investors with a very high level of income. In pursuance of this objective, the fund invests in a portfolio that primarily consists of speculative-grade leveraged loans and junk bonds. These securities have fairly high yields today, with the Bloomberg High Yield Very Liquid Index currently yielding 8.32%. The fund collects the payments that it receives from the securities in the portfolio and then borrows money to purchase more income-producing securities. As a result, it is receiving income payments from more securities than it could otherwise control with just its own equity capital, which has the effect of boosting the effective yield that it earns from its net assets. The fund also might be able to generate a certain amount of capital gains from the securities in its portfolio by exploiting changes in interest rates, but its opportunities to do this are somewhat limited because floating-rate debt securities do not fluctuate very much. The fund collects all of the money that it receives from these investment operations and then pays it out to its own investors, net of the fund’s expenses. As such, we can probably expect that this would cause the fund’s shares to have a very high yield.

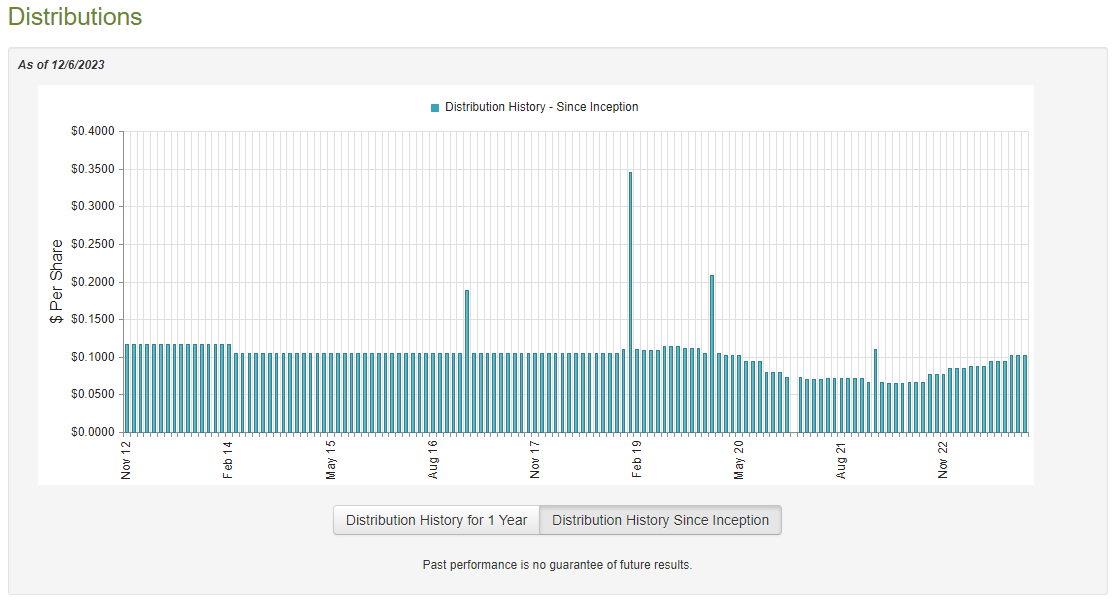

This is certainly the case, as the Blackstone Strategic Credit 2027 Term Fund currently pays a monthly distribution of $0.1020 per share ($1.2240 per share annually), which gives it an 11.08% yield at the current price. This yield is comparable to other funds that are employing a similar strategy so income-focused investors should not ignore it as a potential source of income. However, the fund’s distribution has varied quite a bit over the years as we can see here:

{kind=link}

As clearly shown, the fund’s distribution has changed a lot over the past five years, although it was generally a bit more stable prior to that. This is not particularly surprising, however, as we can clearly see that the distributions have somewhat tracked the changes in the federal funds rate. This fits in pretty well with the statements that I have made throughout this article about floating-rate securities providing an increasing level of income as interest rates increase. The fund appears to be using its higher income to provide a higher distribution to the shareholders, which is very nice to see right now considering the impact that inflation has been having on the budget of many households. The more money the fund pays us, the easier it is for us to afford the necessities and luxuries that we want in our daily lives.

As is always the case though, we want to have a look at the fund’s finances to determine how well it can afford its distributions. After all, we do not want it to be paying out more than it realizes via its investment operations because that is not sustainable over any sort of extended period.

Fortunately, we have a relatively recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund’s most recent financial report corresponds to the six-month period that ended on June 30, 2023. As such, this report will not include any information about the fund’s performance from the past five months, but it is still more recent than the reports that some other funds have released so far. The first half of this year was an interesting one for fixed-income funds as the market generally assumed that the Federal Reserve would cut interest rates during the second half of 2023 and was pricing bonds accordingly. Obviously, that belief was proven to be wrong, but the opportunity still existed to realize some capital gains by trading fixed-rate bonds. This fund probably did not take advantage of that to any great degree due to the heavy exposure to floating-rate securities, but it still might have been able to make a little money.

During the six-month period, the Blackstone Strategic Credit 2027 Term Fund received $12,796,567 in interest from the assets in its portfolio. The fund had no income from any other source so that money accounted for all of its total investment income during the period. The fund paid its expenses out of this amount, which left it with $8,788,058 available for shareholders. That was sufficient to cover the $8,234,407 that the fund paid out to the investors during the period. This is a repeat of the fund fully covering its distributions out of net investment income during the full-year 2022 period.

Thus, it appears that the Blackstone Strategic Credit 2027 Term Fund is simply paying out most of its net investment income to the shareholders. This is exactly what we like to see from a fixed-income fund. The fund should be able to sustain its current distribution as long as its income remains at today’s levels. For the most part, as long as interest rates stay right around today’s levels, investors should not have to worry about a distribution cut. That may be a tall order, as the Federal Reserve might still reduce interest rates next year even if it does not cut to the degree that the market expects.

Valuation

As of December 6, 2023, the Blackstone Strategic Credit 2027 Term Fund has a net asset value of $12.53 per share but the shares currently trade for $11.07 each. This gives the fund’s shares a 11.65% discount on net asset value at the current price. This is not quite as good as the 12.27% discount that the shares have had on average over the past month, but it is still a double-digit discount. As I have pointed out in the past, a double-digit discount is generally a reasonable price to pay for any fund even if it is not necessarily the best price possible. As such, potential investors should be fine buying the fund at today’s level.

One interesting thing about this fund is that the discount should narrow over the next few years. That is because of the scheduled liquidation in September 2027. On that date, all of the fund’s assets will be liquidated and the money distributed to the fund’s shareholders. However, it may be too soon to buy the fund hoping to profit from this due to the fact that a lot could happen with interest rates between now and then.

Conclusion

In conclusion, the Blackstone Strategic Credit 2027 Term Fund appears to have a lot to offer to risk-averse income investors. The fund’s assets consist of a mix of floating-rate senior loans and fixed-rate junk bonds, which positions the fund pretty well if the market is wrong about the magnitude of interest rate cuts next year as appears likely. The fund’s distribution is fully covered by net investment income, which should be reasonably comforting, and it is diversified enough to avoid significant losses due to defaults. As such, this fund might be worth purchasing today as a hedge against interest rate risk and as an income vehicle.

For further details see:

BGB: A Solid Income Fund With Limited Interest-Rate Risk