BGT - BGT: A Year Later The Buy Case For Floaters Persists

2023-08-17 11:03:07 ET

Summary

- BlackRock Floating Rate Income Trust has been a strong performer, outpacing the S&P 500.

- The fund is currently trading at a discount to its net asset value, making it an attractive investment.

- BGT's income has been increasing along with higher interest rates, making it a good option for investors looking for a high income stream.

Main Thesis & Background

The purpose of this article is to evaluate the BlackRock Floating Rate Income Trust ( BGT ) as an investment option at its current market price. The fund's objective is to "provide a high level of current income", and it does this by investing primarily in senior secured floating rate loans made to corporate and other business entities.

I began to get bullish on floating rate securities - and BGT by extension - last year. Since my buy call in August 2022 one year ago this fund has indeed been a strong performer. In fact, it has actually outpaced the S&P 500. While not really a benchmark for this fund at all, it is still interesting to note:

Fund Performance (Seeking Alpha)

As I have been making portfolio adjustments for the second half of the year, I wanted to take another look at BGT to see if a buy rating was still appropriate. Fortunately, many of the factors supporting buying it last year remain in place today. This tells me "buy" is still the correct outlook and I will explain why in detail below.

Despite Gain, Discount to NAV Has Widened

As my followers know, I am a very keen to focus on CEFs that trade at discounts when I make purchases. While not always a primary metric, I will certainly shy away from high premium funds. But discounts are preferable when I see a macro-backdrop that is favorable for a particular fund's strategy. That was the case last year when I recommended BGT. The fund sported a discount in excess of 5% and I believe the underlying securities were going to perform well.

Both of those factors turned out to be correct and investors were rewarded in turn. But today is a new day - so what is the valuation proposition now?

The good news is it has actually improved. Despite a 10% pop since last August, investors have been unwilling to bid this CEF up to premium territory. The discount has actually widened to over 7%:

{kind=link}

BGT's Valuation (BlackRock)

While not a huge move from last year it is notable since the fund has seen such a large gain in the interim. With momentum on its side and a very cheap price on the open market relative to what the fund is inherently worth, this is supportive of keeping the bullish outlook in place.

Equities Seem Pricey - Time To Shop Hedges

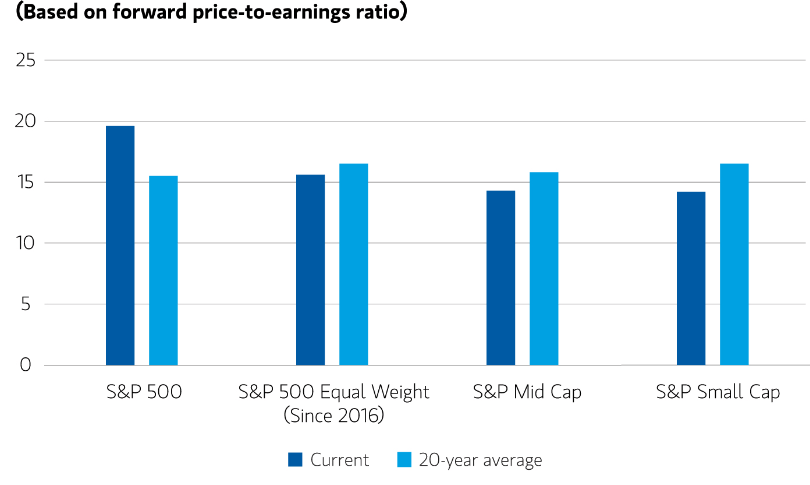

A second factor that is supportive of BGT is a metric that is supportive of many different investment strategies at the moment. What I am referring to is the expense of buying in to the S&P 500. It has gotten a bit frothy by historical standards and this makes me want to shop around for value. That could be a number of different themes/sectors/funds - but it is inclusive of BGT all the same.

To understand why, let us look at the forward P/E of the S&P 500. This is relevant for me (as I'm sure it is for most readers) because the S&P 500 is my primary benchmark and also my largest exposure in my portfolio. So knowing when (or if) to add is critical for my overall allocation. When I see the index pushing above-average valuations, I tend to look elsewhere:

{kind=link}

P/E Ratios (Morgan Stanley)

Now this does not inherently mean BGT is going to automatically keep going up from here. That is not what I am saying. But I wanted to bring this up to help readers understand why I am even looking at this type of fund in the first place. Equities seem expensive and with the headwinds on the economic horizon it makes sense to diversify. Whether this is through fixed-income, floating rate debt, or more defensive equity sectors (or all three) is up to each individual. But for me it paints the story of why BGT continues to have value.

Fund Is Raising Income Like It Should Be

My next topic goes back to BGT directly. As a floating rate fund, this should be an income stream that is increasing along with higher interest rates. In this environment - interest rates are going up - so BGT's income should be too. If that wasn't the case I would have to question the validity of buying this product. But the good news is, income has indeed been rising.

This is true in a big way in 2023. The fund has seen two distribution increases in 2023, which one coming quite recently in June:

BGT's Income Stream (BlackRock)

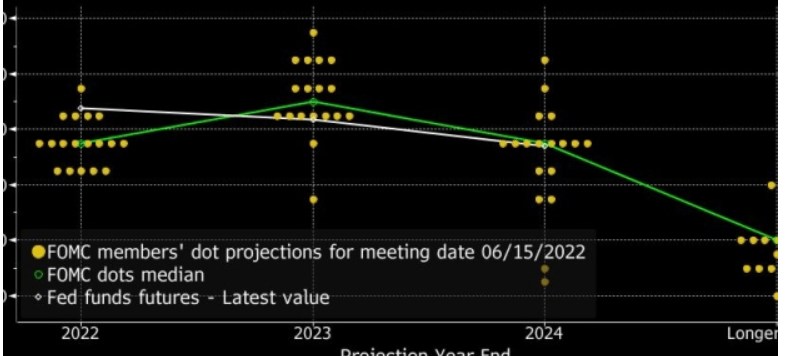

This helps set BGT apart from its peers that are focused more on diversification or fixed-rate debt. Many leveraged CEFs have seen cuts in 2023. This is inclusive of corporate debt and muni funds. The increase in leverage expense was just too much to handle. But BGT, by contrast, has been able to benefit from those higher interest rates by the nature of these loans. The loans and debt issues re-set at the prevailing (higher) rates, making it the borrowers problem. And this income flows to the holders of the debt and investors of BGT by extension. With rates expected to remain higher for longer, this is great news:

{kind=link}

Current Fed Dot Plot (Bloomberg)

What this shows is that rates are likely to be moderately lower in a year but the pace of that decline is going to be slow. That gives investors in BGT plenty of time to collect a high income stream at a good price.

This is something, however, I will keep a close eye on. While BGT has been working over the past year that is not going to be the case forever. I expect the short-term to continue to be good for this fund, but once rates start to decline, greener pastures will exist elsewhere. So while I am a buyer here, I will change my tune as economic conditions warrant it.

A Reminder: These Are Below IG-Rated Holdings

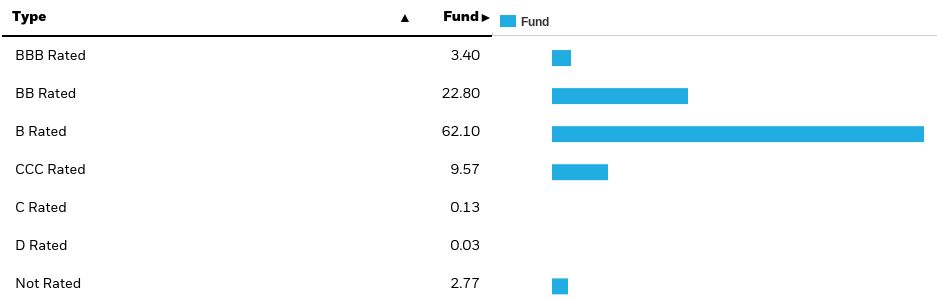

I have painted a positive picture for BGT thus far and I stand by that. But I need readers to remember this is not a "risk free" product by any stretch. It has returned strong gains but that came with a cost - in terms of risk. While the backdrop has been favorable for floaters and that is still the case today, many of these issues come from low quality compared (at least when compared to large-cap US stocks). The graphic below shows the fund's rating breakdown:

{kind=link}

Credit Quality (BlackRock)

With economic conditions a bit uncertain at the moment, I would not fault anyone for wanting to steer clear of below IG-rated issues. Personally, floating rate debt is one of the few areas where I would push the risk envelope because the growing income stream is attractive. But, generally speaking, I believe IG-rated debt is an inherently better place to be for the more risk averse investor.

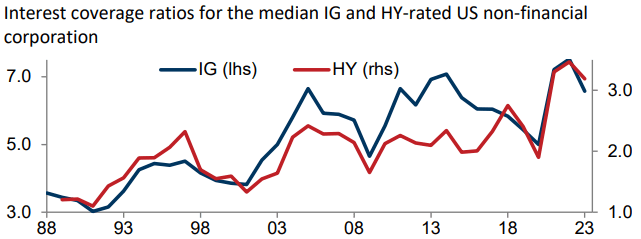

While this caution is well-founded, the backstory is not all doom and gloom. The good news is that corporate America has been slashing costs and maintaining a resilient hold on profits. The net result is that interest coverage ratios, while having declined slightly, are still at historically high levels for both high grade and junk debt issuers:

{kind=link}

Interest Coverage Ratios (FactSet)

While the short-term downward trend isn't great it is comforting to know that the starting point is from a historically high level. This puts some of my concerns for BGT to bed for the time being. The fund is filled with junk issues, but those are not as "junky" as they may have been in the past. That is another supporting factor for continuing to own this fund.

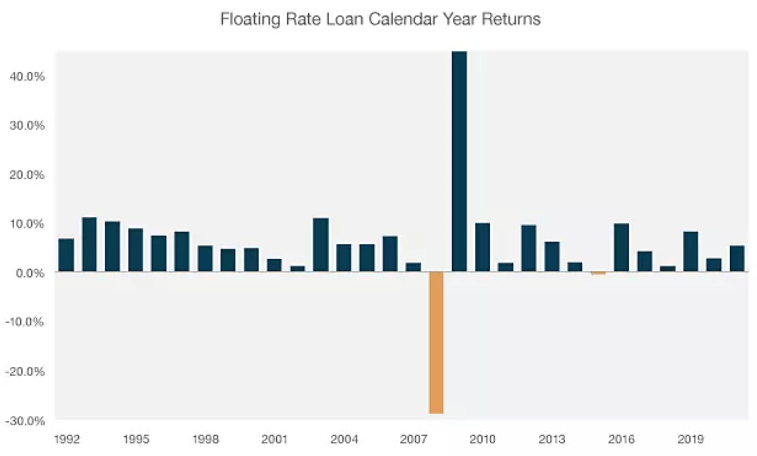

This Is A Time-Tested Strategy

My final point ties back to floating rate debt as a whole. This is relevant for BGT but also for any other fund with a similar strategy that readers may have their eye on. While calendar year returns fluctuate for this sector just like any other - the result is almost always positive:

{kind=link}

This suggests that investors will probably be okay in this asset class no matter what is happening with the Fed on any given month. Over time, the ride is pretty smooth and that could be what many may be looking for holistically.

Bottom Line

BGT has been a big winner over the past year and more gains could be on the way. The income stream is rising, the discount to NAV has widened, and interest coverage and lower-rated issuers is still strong historically. All of these factors add up to keeping this fund as a buy candidate in my eyes. As a result, I would encourage readers to give this idea some consideration at this time.

For further details see:

BGT: A Year Later, The Buy Case For Floaters Persists