BGT - BGT: Floaters Still Look Attractive

Summary

- Floating rate debt should remain in demand as the Fed continues to raise its benchmark rate.

- Further, the market is starting to come to terms with the fact that rates will be "higher for longer".

- BGT has a sizable discount to NAV, which is actually wider than where it was during my last review despite a positive return in the interim.

Main Thesis & Background

The purpose of this article is to evaluate the BlackRock Floating Rate Income Trust ( BGT ) as an investment option at its current market price. The fund's objective is to "provide a high level of current income", and it does this by investing primarily in senior secured floating rate loans made to corporate and other business entities.

BGT has been my preferred option for floating rate exposure for a while. I reiterated a positive outlook on it back in August, and generally it has held up well since then despite quite a bit of market turbulence:

Fund Performance (Seeking Alpha)

Given the roughly seven months that have passed, I figured it was time to take another look at this fund. After consideration, I still see plenty of merit for owning this going forward. I will therefore be keeping the "buy" rating in place and I will explain the reasons why in detail below.

"Higher For Longer" Is The New Reality

I will begin with a macro-discussion on the broader interest rate environment. This is critical when evaluating floating rate products - including BGT. The simple logic is that this is an allocation that will perform especially well when interest rates are rising and are less relevant in the reverse scenario.

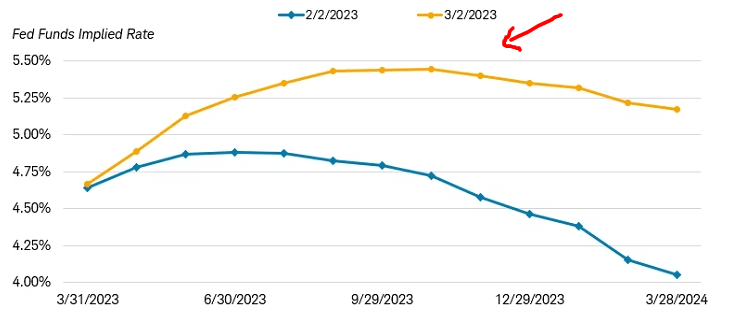

With this in mind - why consider floaters right now? To me this comes down to the "higher for longer" reality that is finally setting in to investor's minds. I have been surprised for a while that the market was anticipating a cut from the Fed later this year - the evidence simply didn't support it. It was a case of being overly optimistic in my view and the Fed has downplayed those expectations at every turn. It seems that with persistent inflation, the market has woken up and re-set forward outlooks for the year ahead. While investors have originally planned on seeing rates begin to decline by Q4, the thought now is rates will not only be higher than anticipated by year-end, but will be sustained at those levels for a longer period of time:

Forward Path of the Fed Funds Rate (Expected) (Charles Schwab)

{kind=link}

The implication here is that investments that perform well (or should perform well) in higher rate environments remain as relevant today as they did last year. This elevated rate environment is likely to persist for at least another year, which makes floating rate debt a continued choice for my portfolio.

The reasoning is straightforward. These are loans that re-set at prevailing interest rates based on a set timetable. When rates are rising, that income grows because the loans begin to charge higher rates as well. For investors looking to beat inflation/higher rates, this is a common way to do so.

And BGT has indeed performed in this manner. With rates rising consistently, BGT boosted the distribution aggressively in Q4 2022, as shown below:

BGT's Distribution History (BlackRock)

This was a great development and came at a time when many leveraged CEFs were cutting rates because of the more difficult investment backdrop. Floating rate funds like BGT were able to buck this trend and deliver on their objective. When I couple a positive return with an income boost, the buy case is clear.

Valuation Remains A Bargain

The fact is though that investors have many options when considering floating rate credit. BGT is a fund I have found attractive for a while, but there are other funds out there that have a similar credit quality and holdings make-up. But a key reason why I continue to like this particular fund is its valuation. Back in August, I saw value in BGT at a 6% discount to NAV. Today, despite the market price rising in value since that time, this discount has actually widened to almost 9%:

{kind=link}

I see this as another supporting factor for owning BGT. It has continued to pump out modest gains during a general market downtrend and its discount has actually gotten more attractive for prospective buyers. Of course, a 9% discount in no way guarantees a forward positive return, but it helps me justify positions in this particular fund when I see a strong backdrop for the underlying sector at the same time.

Default Rates To Rise, But Remain Contained

A word or two on risk - BGT has plenty of it. Despite positive attributes like higher income and a wide discount, this type of investment is riddled with credit risk that readers need to be aware of. I mostly focus on IG quality debt, so a push in to junk debt is rare for me and represents a small percentage of my overall portfolio. To understand why, consider that BGT holds mostly BB and B-rated debt, which are below investment-grade quality:

BGT's Credit Quality (BlackRock)

{kind=link}

The reference here indicates that BGT is more susceptible to delinquencies and defaults than funds that hold higher quality debt. With a more challenging macro-environment in 2023, the default rate is indeed expected to rise for leveraged loan issuers. This is simply an estimate, but suggests some level of caution is probably warranted:

Historical Default Rates (Leveraged Loans) (S&P Global)

{kind=link}

The good news here is that even if defaults do tick up to that 1% level, that is well within historical norms for this sector. So things may get "worse", but are still par for the course based on a longer time horizon.

The conclusion I draw here is to be aware of these risks and stay within your risk tolerance for below-IG credit. Do I see value in floaters and BGT? Absolutely. But I would caution readers not to go "all in" or get over-exposed in this climate. The credit market is weakening, and funds like BGT that hold a lot of junk debt could find themselves facing a more volatile year as a result.

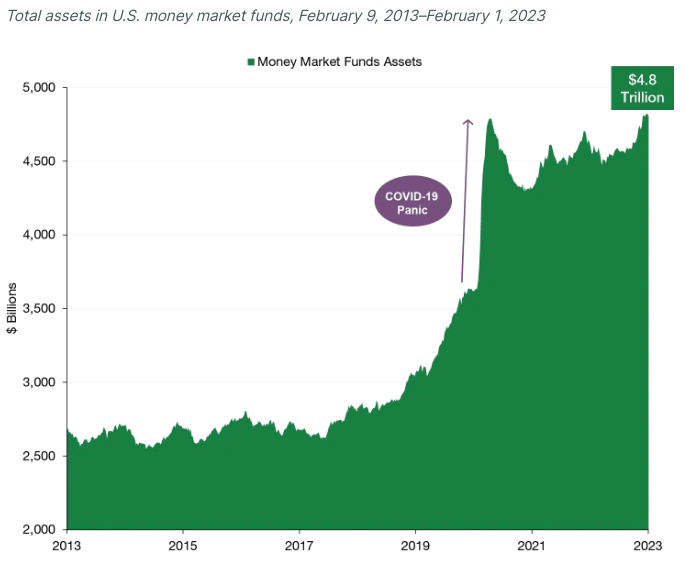

Investors Have A Lot Of Cash - It May Wind Up Going Somewhere

My final point has to do with the investor mindset. As it stands now, investors do have quite a few alternatives compared to equities. This is something I discussed in recent reviews where I noted we have gone from "no alternative" to "lots of alternatives" in the investment realm. What I mean is, investors were pushed in to equities and other riskier assets because rates were low and alternative uses for cash were limited. Today, with rates higher on bonds, savings accounts, and certificates of deposits - there are plenty of places to park cash.

This is an important phenomenon because investors are sitting on piles of cash at the moment. This is true in absolute terms and with a historical perspective, as the following graphic illustrates:

Money Market Balances (U.S.) (Lord Abbett)

{kind=link}

So - what does this mean for us?

In my view it means one of two things. One, investors could just keep this cash sitting where it is. That makes this reality somewhat irrelevant when trying to capitalize on it. Two, investors could begin to put this cash to work elsewhere. There are a lot of options on where to put it, as I stated, but this record amount of liquidity is probably going to wind up in multiple places.

One of those places very well may be floating rate debt. If so, funds like BGT are set to get a boost. I see this as a realistic possibility for the reasons already mentioned: floating rate is a good asset class when rates are rising, BGT's valuation is attractive, the recent income increase, etc.

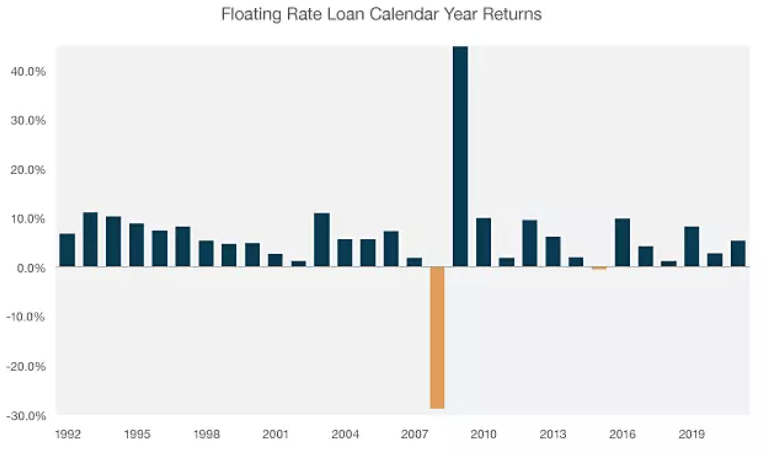

An extension to this bull thesis has to do with floating rate debt's historical performance. If we look back at the past three decades, we see this is a sector that generally registered positive returns. In fact, in only two years since 1992 has the sector seen a negative total return for the calendar year:

Floating Rate Loans Calendar Year Performance (New York Life Investments)

{kind=link}

What I draw from this is that if investors are looking for ways to deploy their piles of cash, floaters are a reasonable option. They make practical sense in our current environment and have a strong track record of performance over the long-term. This plays right in to the hands of BGT.

Bottom-Line

BGT is a fund that is for the more risk-on investor, but offers value at these levels. It has enjoyed a recent income boost, sits at a hefty discount to NAV, and should benefit from the higher for longer narrative with respect to interest rates. Fixed-income is also starting to offer some value, but I see a compelling story-line for floating rate debt in this environment. Therefore, I am reiterating my "buy" recommendation for BGT and suggest readers give this idea some consideration going forward.

For further details see:

BGT: Floaters Still Look Attractive