BGT - BGT: The Glory Days For Floaters May Be Ending

2023-12-02 04:31:23 ET

Summary

- The article evaluates the BlackRock Floating Rate Income Trust as an investment option at its current market price.

- Investing in floating rate securities has been a successful strategy, delivering strong total returns. But that could change next year.

- I see an uptick in default rates and a more dovish Fed in 2024 as potential headwinds that will moderate returns going forward.

Main Thesis & Background

The purpose of this article is to evaluate the BlackRock Floating Rate Income Trust ( BGT ) as an investment option at its current market price. The fund's objective is to "provide a high level of current income", and it does this by investing primarily in senior secured floating rate loans made to corporate and other business entities.

Investing in floating rate securities was a no-brainer to me in 2023 and I reiterated this stance back in the summer. Funds like BGT that offered exposure to debt that who interest payments rose along with higher interest rates were performing very well and delivering strong total returns. Despite some market expectations of lower rates, I pushed ahead with buy ratings because I saw a continued favorable environment. In hindsight, this optimism has been rewarded:

Fund Performance (Seeking Alpha)

Looking back, this CEF has been a big winner for me as the Fed has embarked on an aggressive rate hiking cycle. It has provided high, growing income, and strong capital returns to boot. To say I am satisfied with its performance over the past year and a half is an understatement.

But investing is not about looking back, but forward. That is where the challenge for me is with respect to BGT right now. While past, and even current performance, has been solid, I am concerned about the opportunity going forward. While I am not predicting a massive sell-off or anything close to it, I think the days of "alpha" generation from this security have passed. For this reason I am downgrading it to "hold", and I will explain why below.

How We Got Here

To begin, I want to take some time to discuss why BGT has been such a strong performer over the past couple of years. Remember, this is a fund that holds floating and variable rate securities. What this means is that this debt of debt is preferable (for an investor) in a rising rate environment, all other things being equal. This is because as the benchmark rate rises, so too does the interest of the debt/loan. This means the borrower sees their obligations rise when the broader interest rate environment is rising, shifting the interest rate risk on to the borrower, not the lender. As long as the debt holder is still able to make good on their obligations, the lender (or investor) wins because their income stream grows.

This is a way to hedge inflation because investors in fixed-income securities often have to rotate out of their holdings and in to higher yielding securities to keep pace with the rising cost of living/higher rate environment. For those holding floating rate debt, whether through BGT or another type of investment, they can just sit back and enjoy the higher income stream without making any adjustments.

This has precisely been the case for BGT over the past few years. As the federal funds rate has moved higher since Q1 2022, BGT has delivered multiple boosts to its distribution:

{kind=link}

Federal Funds Rate Movements (Federal Reserve)

BGT's Distribution History (BlackRock)

This should make it fairly clear why BGT has performed well. Floating rate debt has held up as the economy avoided a recession (limiting credit risk) and investors have been drawn in to this sector in droves. This has supported valuations in the underlying assets and also offered investors higher income levels, both of which are responsible for sending BGT's total return higher. It is a win-win that I have personally benefited from and I am very pleased with the result.

Why The Future Isn't As Rosy

The prior paragraph helps to explain why BGT has been recommended by myself so consistently and why performance has been strong. But, as mentioned earlier, if one is considering buying in now then the future outlook is more relevant than the past. That is always the rub with investment decisions - what has worked before may or may not work again.

In this light, I see a more limited opportunity for BGT heading in to 2024. This is primarily due to the interest rate outlook. As rates have risen, BGT has profited. But now the outlook is less hawkish and this means the gains BGT has delivered are going to be a lot harder to come by.

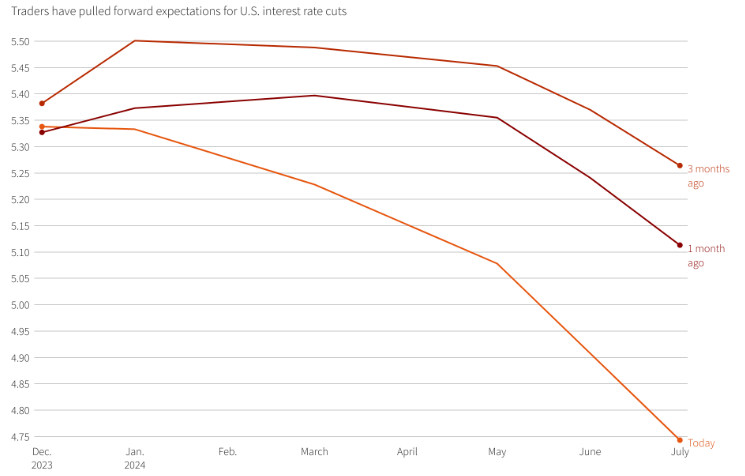

The general concern is that investors are anticipating (or perhaps hoping ) for rate cuts in the new year. Traders are seeing a Fed "pause" turning in to Fed cuts and generally cooling inflation and economic growth as supportive of this outlook. The futures market is currently suggesting a 40% chance of a 25-basis-point cut by the Fed's March meeting, with additional cuts to follow after that. This is a more dovish outlook than traders had earlier in the year:

{kind=link}

Futures Market - Fed Funds Rate (Reuters)

I do want to manage expectations here by saying this is not disastrous for BGT by any means. Of course, investors in this fund want rates to be moving higher in a manageable way in order to collect their principle back and higher income streams. That is ideal, while a falling rate environment is not. But seeing rates decline by .5% - 1% over the course of a few quarters is not catastrophic.

That is an important point to emphasize because I am not trying to be alarmist here. As noted earlier, my rating is now "hold", not "sell" because there is a path forward for continued gains for BGT. I personally think the risk-reward environment has shifted so the fund is not as attractive as it was over the past eighteen months. But there is a chance that the Fed does hike rates further and/no rates do not get cut. If either of those scenarios occur, BGT will likely do just fine and will continue to act as an equity and fixed-income hedge. So weigh this possibility carefully before making any decisions within your portfolio.

Other Markets Offer Upward Sloping Yield Curves

Another factor to consider is that the interest rate outlook in the US is not the same as the rest of the world. This doesn't make it "good" or "bad", just different. And they are different enough to the point where readers should be evaluating different bond options across developed and emerging markets depending on what their individual goals are.

For example, if one wants to continue allocating resources to floating-rate securities, perhaps they would be best served exploring non-US markets. Take Japan as an example. While the talk in the US is whether or not the Fed will begin cutting rates in 2024, traders in Japan are expecting rates to increase going forward. This is precisely the type of environment investors in floating rate assets want to see:

Yield Curve (Japanese Government Bonds) (Bloomberg)

The conclusion I draw here is that investors have plenty of options and for those who want exposure to an area that will see higher macro-rates, then overseas securities could be a better play.

Valuation Still Attractive, Has Narrowed

Looking at BGT in isolation, another metric that may be piquing investor's interest is the fund's valuation. On the surface, a discount to NAV in excess of 6% does look fairly tempting, so keep that in mind:

{kind=link}

BGT Fast Facts (BlackRock)

I would point out, however, that BGT has a history of trading at a discount to NAV so a thesis that relies on this metric moving to par (or in to premium territory) is a bit optimistic. Further, during my last review, BGT's discount was over 7%, so this has narrowed over the past quarter, making new entry points less attractive by comparison.

While overall this valuation story is probably supportive of buying or holding, I lean towards hold because the discount has just as much chance of widening here (in my view) as it does narrowing. It is no longer the flashing red buy signal that it used to be.

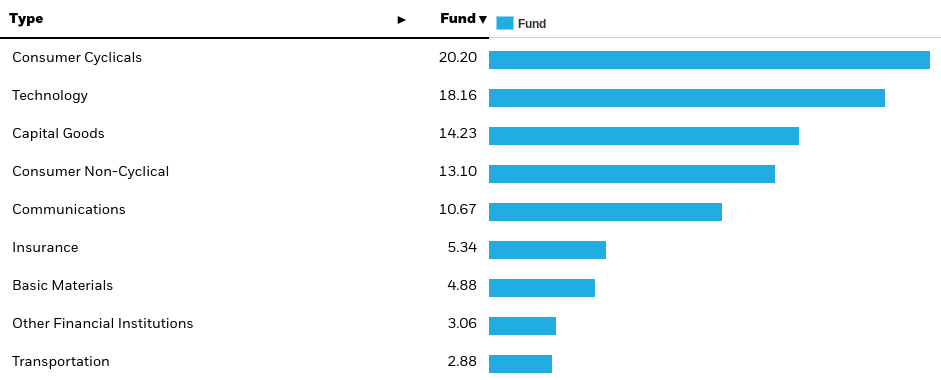

Consumer Exposure Should Be Monitored Closely

I will now shift to a look at BGT's portfolio. Specifically, this is a fund that is pretty well diversified, but does have about one-third of its exposure tied to Consumer-oriented sectors:

{kind=link}

BGT's Sector Breakdown (BlackRock)

Paying specific attention to the inner-workings of the debt market is critical right now because conditions are getting more difficult. This makes asset (including sector) selection a more important source of criteria for any buy recommendation right now. TO see why, consider that default rates have ticked up noticeably from a year ago:

Leveraged Loan Default Rate (Aggregate, US) (Fitch Ratings)

This indicates some weakness in the market and is likely the result of higher interest rates. As I mentioned before, higher rates are a positive for investors in this type of floating rate debt because it means the income should increase. But that assumes all other things are equal - and oftentimes all other things are not equal.

For example, just because a borrower is required to pay a higher cost to borrow doesn't mean they can and will. While they are "required" to, we always have to consider credit risk. If the rates rise to high that the borrower is pushed in to default then, floating rate or not, the lender or invest may get nothing. That is not a desirable scenario.

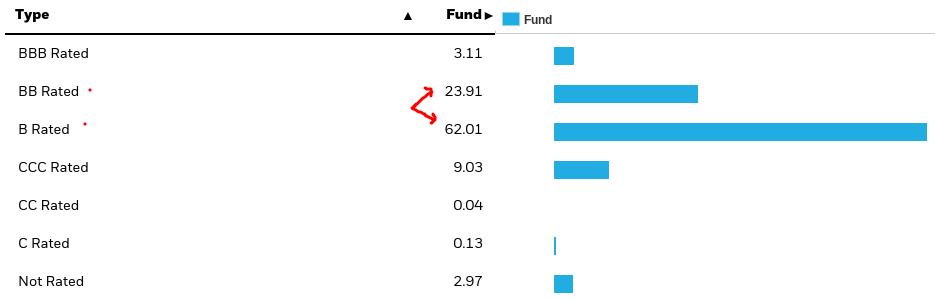

While credit risk tends to be minimal in IG-rated bonds and loans in most investment cycles, the same cannot be said for below IG-rated or leveraged loans (that tend to be below IG-rated). Such is the case for most of the securities in BGT's portfolio, which are not considered investment grade quality:

{kind=link}

BGT's Credit Quality Breakdown (BlackRock)

This is why paying close attention to whether the credit markets are deteriorating is so very important for holders (or prospective holders) of BGT.

Again, my point here is not to alarm. While a 3% default rate is not exactly a great sign, it doesn't warrant fleeing out of risk-on asset classes all together. But it does mean investors should be more selective and be willing to be active when and if conditions change.

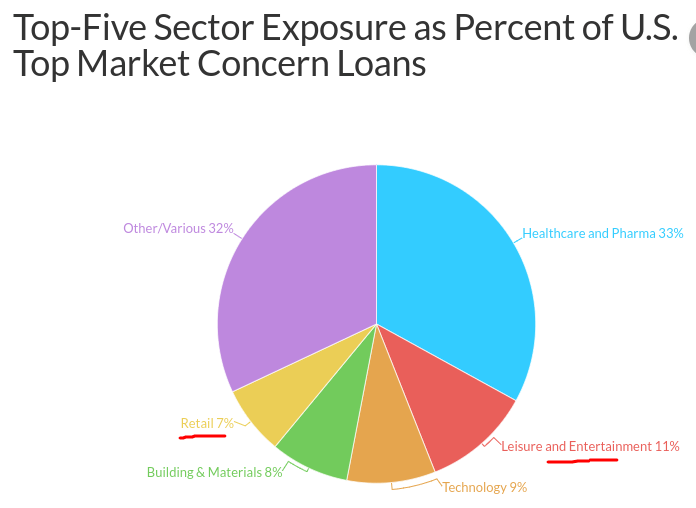

For me, BGT is certainly at risk if the climate deteriorates further because of this consumer-dominated exposure. According to Fitch Ratings, some of the areas that are of "most concern" are indeed consumer-related. These include the sectors of Retail and Leisure & Entertainment:

{kind=link}

Areas Most "At Risk" (Fitch Ratings)

What I am conveying here is that BGT is not a risk-off play and will need to see continued economic strength related to consumer-oriented areas in order to have its underlying securities appreciate. Further, the ideal backdrop is an increasing rate environment, and that may be coming to an end. Ultimately, both of these factors are influential in my downgrade going forward.

Bottom Line

BGT has taken advantage of floating rate debt being a top performing asset class since the beginning of 2022. I have been long and strong this CEF, and that has continued through this calendar year. However, looking ahead to 2024, my outlook is more modest. The economic environment is getting more challenging and that could push defaults higher, including in the consumer-oriented sectors that BGT relies on. In addition, investors are anticipating lower interest rates here in US, which is in contrast with other developed markets. This makes US-originated floating rate debt less attractive by comparison. As a result, a downgrade to "hold" for BGT is well supported at this time, and I suggest to my followers that they approach any new positions carefully.

For further details see:

BGT: The Glory Days For Floaters May Be Ending