GNENY - Big 4 Lithium Stocks And Spot Lithium Prices - Why I Am Bullish On SQM

2023-12-31 09:00:46 ET

Summary

- A controversy has arisen over whether lithium is a commodity. Two things define a commodity. One is standardization and the other is single-pricing.

- Although most experts still think that lithium is a "specialty chemical", only produced by certain companies, evidence is growing to demonstrate that this is changing drastically.

- The Chinese spot market may be contributing to this process to the extent that it is related to lithium companies’ pricing mechanisms with a serious impact on their stock prices.

- In this article, this line of reasoning is applied to the analysis of Albemarle, SQM, Ganfeng, and Tianqi, over the period January 31-September 30 2023.

- Spot prices and non-price-related factors have a significant effect on the Big 4 stock prices. With these results and other reasons, I show why SQM is my top 2024 pick.

There is an ongoing debate about whether lithium is a commodity. In economic terms, we can think of a commodity as a traded product that is standardized and has the same price in any part of the world, leaving other expenses, such as shipping and taxes, aside. In this connection, most mainstream analysts argue that lithium chemicals (particularly, lithium carbonate and lithium hydroxide) are “specialty chemicals” of different quality and, consequently, distinct price. However, evidence is mounting to indicate that such refined raw materials are becoming standardized and rapidly converging toward a single price across the planet. It has therefore been argued that the Chinese spot market is contributing to this process. By contrast, analysts have responded that this could not be the case given the insignificant size of the spot market in China.

In several tweets posted over the last three years or so, I have undermined this last stance because even if the volume of the lithium products traded in the spot market is relatively small, the spot price has become the referential price in the industry. This is because the largest lithium companies in the world have decided to shift from fixed-price contracts to variable-price contracts. That is precisely the case of two of the so-called Big Four Lithium Companies, Albemarle Corporation ( ALB ), and Sociedad Quimica y Minera de Chile S.A. ( SQM ). This made a lot of sense last year when the lithium market was booming. Much less this year.

Nonetheless, in its Q2 Earnings Call Transcript , on August 03, Albemarle indicated:

“Due to the recent rebound in lithium pricing, our full year 2023 net sales mix is now expected to be 80% index-referenced variable price contracts and 20% spot. There's been no other change to our contract philosophy or structure of these contracts. Our strategy to deliver long-term growth remains on track.”

Note that by August 03, lithium prices were already falling.

But what did all this mean anyway?

First, there was an explicit recognition that 1/5 of their product is sold at the spot price. Second, apart from the 3-month lag incorporated in the price index, the variable price needs to vary relative to something. And, here Albemarle only said that this market index was going to move with the market. The question is again, which market? So, in the absence of a well-developed futures market at the time, it seems plausible to think that Albemarle’s variable-price contracts were also meant to be related to the spot market.

Curiously enough, in its Q3 2023 Earnings Call , Albemarle omitted the word “variable” from its different comments on the evolution and prospects of the lithium price. They only said:

“We have floors on our 80% of our index reference contracts.”

For one thing, variable contracts have very little to do with floors. For another, this confusing approach probably explains why Albemarle was only perplexed as to why the price was where it was by Q3 2023.

Similarly, in its Q2 2023 Earnings Call , on August 17, SQM said:

“Since the majority of our sales contracts are based on price indices that follow market price trends, our realized sales prices moved with the market with some lag, depending on the terms of the contracts. This commercial strategy allowed us to capture the price premiums in the market last year.”

More specifically, in its August corporate presentation , SQM indicated that

“Over 85% of contracts are linked to price indices which follow market price trends.”

Lastly, in a reply to an inquiry at its Q2 2023 Earnings Call, SQM’s CEO clearly stated:

“Yes. Well, as we have explained, we have most of our contracts today following indexes. So, I mean, it's very transparent. Everybody can follow those indexes. We have seen that since the middle of June this year, some negative trends in the Chinese index and later on, followed by also the outside China indexes. So -- but at the same time, we have different lags in the way we adjust our contracts, the way we follow the indexes.”

Likewise, in its Q3 2023 Earnings Call , SQM’s CEO explained once again:

“… the majority of our sales contracts are linked to price indices which move with the market, our realized sales prices have followed the same trend with a small delay and it is reasonable to expect that they should continue to reflect market price dynamics in the upcoming months.”

Why does this matter?

First, SQM explicitly acknowledges that in the market indices that their contracts follow, the Chinese spot market prices are included. Second, the Chilean lithium company also suggests that these prices are followed by other indices outside of China.

Although there is no specific information on Ganfeng and Tianqi’s pricing strategies, it also seems reasonable to assume at this point that they are in some way linked to the Chinese spot market.

All of the above paves the way to propose the following hypothesis.

If the Big Four lithium companies’ pricing mechanisms are related to the Chinese spot prices, it might be plausible to argue that the latter has an important effect on the performance of those companies as measured by their stock prices.

For several reasons, the price of the goods that a company produces and sells might impact the value of its shares. First, a company’s revenue is directly impacted by the price at which its products are sold. If the selling price is high and the business keeps up its volume of sales, it may result in larger revenue and perhaps even profits, which might make the business more appealing to investors and raise the stock price. Second, a company's position in the market may be reflected in the price of its products. A corporation that can charge greater pricing, for instance, would be perceived as having strong branding or better products, which would be favorable for the stock price. Third, if a business can command a high price for its goods, it may indicate that it has an advantageous cost structure (such as low extraction and processing costs), which enables it to generate a sizable profit margin. Investors may find the shares of the firm more enticing as a result.

In this work, I attempt to verify this theory by using Shanghai Metals Market’s lithium chemical and ore prices and Yahoo Finance stock prices for ALB, SQM, Ganfeng Lithium Group Corporation Limited, and Tianqi Lithium Corporation. They are the four largest lithium companies on earth by market capitalization, accounting for about 70% of the world’s lithium production.

Before we proceed, a point of clarification is in order. Besides the price of the goods that a firm produces and sells, many other factors affect the stock price of a given company, as reflected by the play of supply and demand of its shares whereby a higher demand for the stock will result in a higher price, while a lower willingness to sell it will cause a lower price. These consist of:

- Market Sentiment: This is the general opinion of investors toward a specific financial market or investment. Usually, the market price history of a stock, chart patterns, momentum, and trader and investor activity takes care of this. They are also called technical factors.

- Macroeconomic Conditions: These include inflation, interest rates, and changes in GDP.

- Company Performance: A company's profitability, growth pace, and financial stability are all crucial factors to take into account. These are represented by earnings power metrics such as dividends per share, earnings per share ((EPS)), and other metrics. They are also known as fundamental factors because they are reliant on the profits and revenues that a business makes by producing and marketing goods.

- Regulatory Environment: Changes to governmental regulations or policies may impact a company's operations and, consequently, its stock price.

The complete approach utilized in this investigation is described as follows. To begin with, a graphical analysis is performed showing the relationships between each of the Big Four stock prices and domestic spot lithium chemical prices, seaborne spot lithium carbonate and hydroxide prices, and seaborne spot spodumene concentrate prices (Li 2 O: 6%).

Secondly, the correlation coefficients between the Big Four stock prices and 5 different domestic spot lithium chemical prices are estimated.

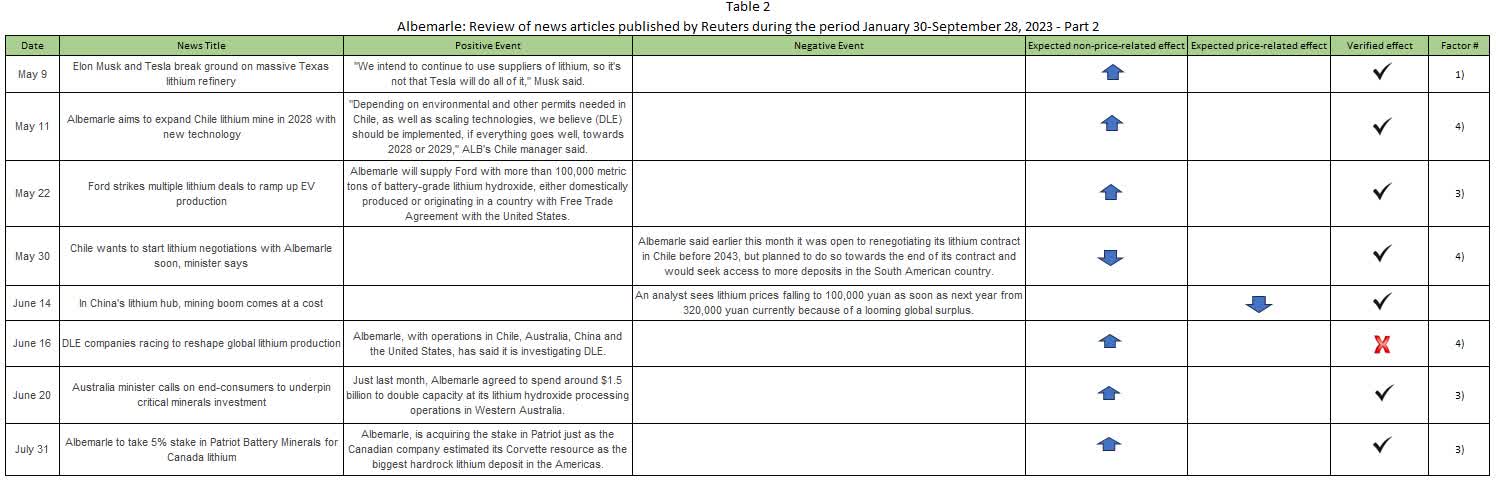

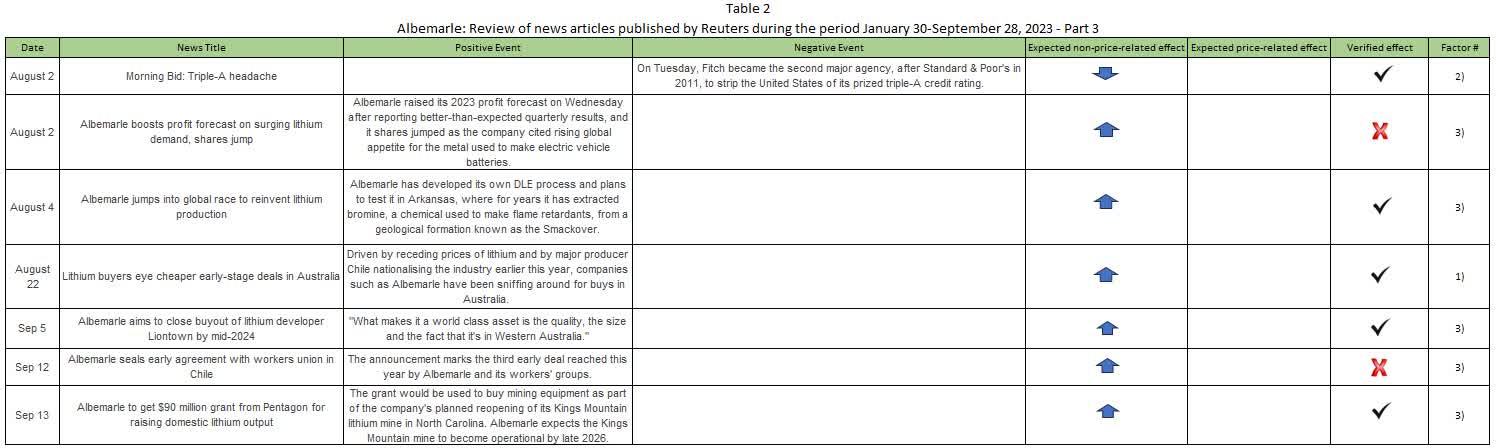

Thirdly, other factors affecting the stock prices of each of the Big Four are examined. To show how important these variables were to determine each Big Four lithium company’s stock prices, the main events that took place during the period under consideration were reviewed. This is described in a table consisting of eight columns. In the first, the date of the news articles is included. In the second, the title of the news stories is incorporated. Next, a summary of the news is placed in the third or fourth column, depending on whether the event is perceived as positive or negative. The fifth column provides a prediction of the direction of the company's stock price taking into account any of the preceding research's elements that are unrelated to the spot price of lithium. The sixth column depicts how the spot price of lithium is anticipated to affect the company's stock price, as stated expressly in the news story. The results are validated or refuted in the seventh column by contrasting the down or up arrows shown in the previous two columns with the actual movement (from one day to another) of each company's shares on the stock market. Lastly, in the eighth column the specific non-price-related factors affecting the company’s stock price are identified, where 1) stands for Market Sentiment; 2) for Macroeconomic Conditions; 3) for Company Performance; and 4) for Regulatory Environment.

Finally, to avoid the situation in which in the previous exercise both valid and invalid outcomes are confounded with the intrinsic relationship between stock prices and lithium carbonate/hydroxide prices and overcome the difficulty of assuming that all effects have the same size, four additional exercises are performed: i) A regression of each company’s stock price on the SMM lithium carbonate 99.5% battery grade and lithium hydroxide (monohydrate) 56.5% battery grade prices, including different combinations of four dummy variables (each one at a time, all four at once, a combined dummy variable of all four, combinations of two, and combinations of three); ii) a regression of each company’s stock price on the SMM lithium carbonate index battery grade and the SMM lithium hydroxide index battery grade prices, including the same combinations of the dummy variables; iii) a regression of each company’s stock price on lithium carbonate 99.5% battery grade CIF China, Japan & Korea and lithium hydroxide 56.5% battery grade CIF China, Japan & Korea prices plus the dummy variables; and iv) a regression of each company’s stock price on spodumene concentrate 6% CIF China price, also including the dummy variables. The five dummy variables are defined as follows. Dummy 1: Market Sentiment; Dummy 2: Macroeconomic Conditions; Dummy 3: Company Performance; Dummy 4: Regulatory Environment; and Dummy Total: The horizontal sum of the other four. To capture the relationships at their plenitude, the dummies were constructed regardless of whether the different news or events resulted in valid or invalid outcomes. The interpretation of these variables is straightforward. A positive and significant relationship between the dependent variable and any of the dummy variables would imply that the type of events or news in question would have led to an increase in the price of the stock, whereas a negative and significant association would mean exactly the opposite.

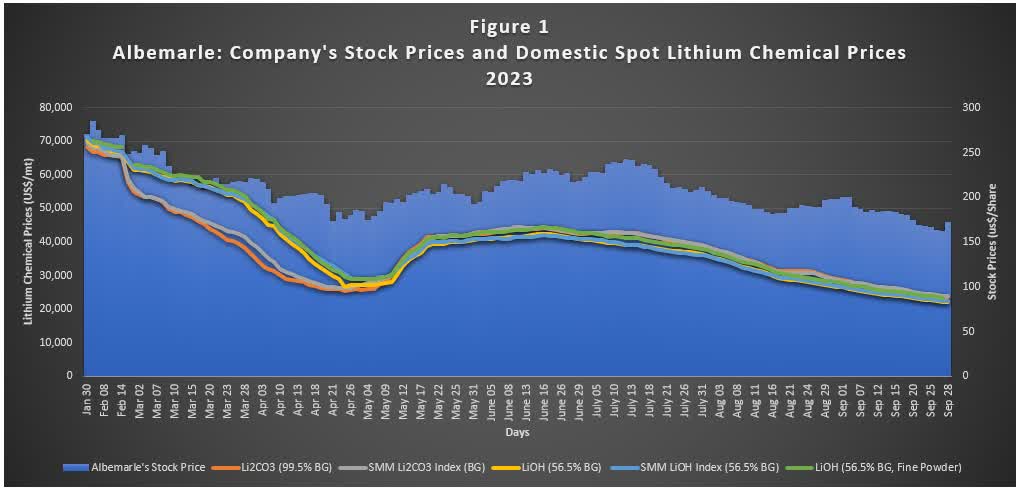

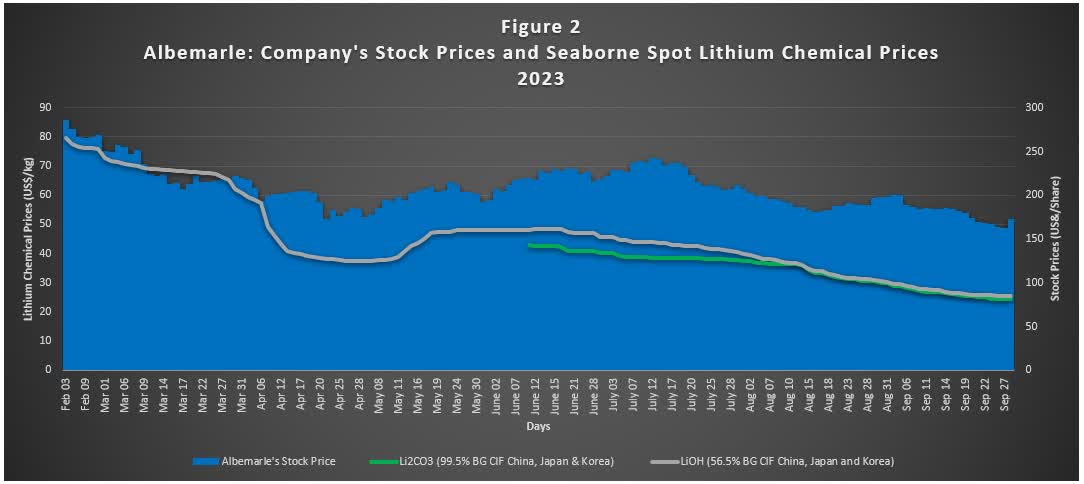

Albemarle

In Figures 1-3, I show the evolution of Albemarle’s stock prices relative to two China domestic spot lithium carbonate battery grade prices, one seaborne spot lithium carbonate battery grade price, as well as three China domestic spot lithium hydroxide battery grade prices, and one China seaborne spot lithium hydroxide price, and one seaborne spot lithium spodumene concentrate (Li 2 O 6%) over the period January 30-September 28. As can be seen, the downward trends are quite similar which is more clearly reflected in the extremely high and positive correlation coefficients reported in Table 1. Note also that these indicators were subject to a two-tailed t-statistic test of significance resulting in all cases in a p-value of less than 0.1%.

{kind=link}

SMM Yahoo.Finance

Sources: SMM , and Finance.Yahoo .

On average, the correlation coefficient for lithium carbonate was 0.89, while the correlation coefficient for lithium hydroxide was 0.83. And the correlation coefficient for SC6% was 0.64. At first glance, this would be consistent with Albemarle’s lithium chemical production mix in 2022 (View slide 10 of Albemarle's most recent presentation , where 50% of its total LCE output was made up of lithium carbonate, 35% of it of lithium hydroxide, and 15% of it of spodumene concentrate). However, as we will see below, how influential the different lithium prices might be on a Li company is probably a much more complicated issue than that.

We would thus be able to determine that Chinese spot prices have a significant impact on Albemarle's stock price performance, which would also explain why Albemarle's existing pricing system is based on Chinese spot prices. Therefore, investors would explicitly consider the Chinese spot prices when considering whether to purchase or sell Albemarle's shares. Last but not least, they would prioritize those prices by the company's mix of chemical and ore production. Hence, for their decision to invest in Albemarle, they would examine the prices of lithium carbonate, lithium hydroxide, and spodumene concentrate, in that successive order. However, another way to look at it would be to see which lithium compound or concentrate would be the most demanded on the international market in which case lithium hydroxide would occupy the first place, followed by lithium carbonate and spodumene concentrate. A third case would be that because the lithium company only produces concentrates, the only relevant price for this company’s investors would be that of the concentrate.

{kind=link}

SMM Yahoo.Finance

Sources: SMM , and Finance.Yahoo .

{kind=link}

SMM Yahoo.Finance

Sources: SMM , and Finance.Yahoo .

But what can we say about other factors affecting Albemarle´s stock prices?

In Table 2, Parts 1-3, we attempt to show how important those other factors were to determine Albemarle’s stock prices by reviewing the main events about Albemarle that took place during the period under consideration.

SMM Finance.Yahoo

Sources: SMM , and Finance.Yahoo .

In what follows, I summarize the findings of this interesting experiment. First, a total of 24 news articles were considered, during the period January 30-September 28, out of which 23 (96%) were non-price-related and 1 (4%) was price-related. A further breakdown of these data shows that out of the 24 news articles, 16 (67%) resulted in valid outcomes, meaning that the expected non-price or price-related effects were validated by the actual movement of the stock prices, and 8 (33%) could simply not be supported by reality. In addition, out of those 16 valid outcomes, 15 were non-price-related and 1 was price-related, and out of those 8 invalid ones, 8 belonged to the first category and 0 to the second. In general, these results can be considered acceptable, providing sufficient credibility to the procedure applied in this research. Second, the 15 non-price-related valid outcomes were subjected to additional scrutiny to reveal what theoretical factors unrelated to the price of lithium affecting stock prices were taken to be the most relevant ones in the specific case of Albemarle. The results in this case were quite interesting: “Company Performance” (6 counts) was perceived to be the overwhelming factor affecting Albemarle’s stock price, followed by “Regulatory Environment” (5 counts), “Market Sentiment” (3 counts), and “Macroeconomic Conditions (1 count).” Third, the price-related valid outcome refers specifically to lithium prices in China and a possible global surplus of the metal. Finally, within the 15 non-price-related valid results no medium or long-term trend formation was perceived and they all seemed to be characterized as having only a short-term impact on Albemarle’s stock price.

These results should be taken with caution because it was found that when using lithium carbonate as the main independent variable, in 10 cases the verified effect of the non-price related factors coincided with that of lithium prices on Albemarle’s stock price of which 7 resulted in valid outcomes, whereas when utilizing lithium hydroxide as the independent variable 11 times the verified effect of the non-price related factors was the same as that of lithium prices on the company’s stock price in which case also 7 turned out to be valid results. In addition, this method's underlying assumption that all effects have the same size was another flaw in it.

{kind=link}

Reuters

Source: Reuters .

{kind=link}

Reuters

Source: Reuters .

{kind=link}

Reuters

Source: Reuters .

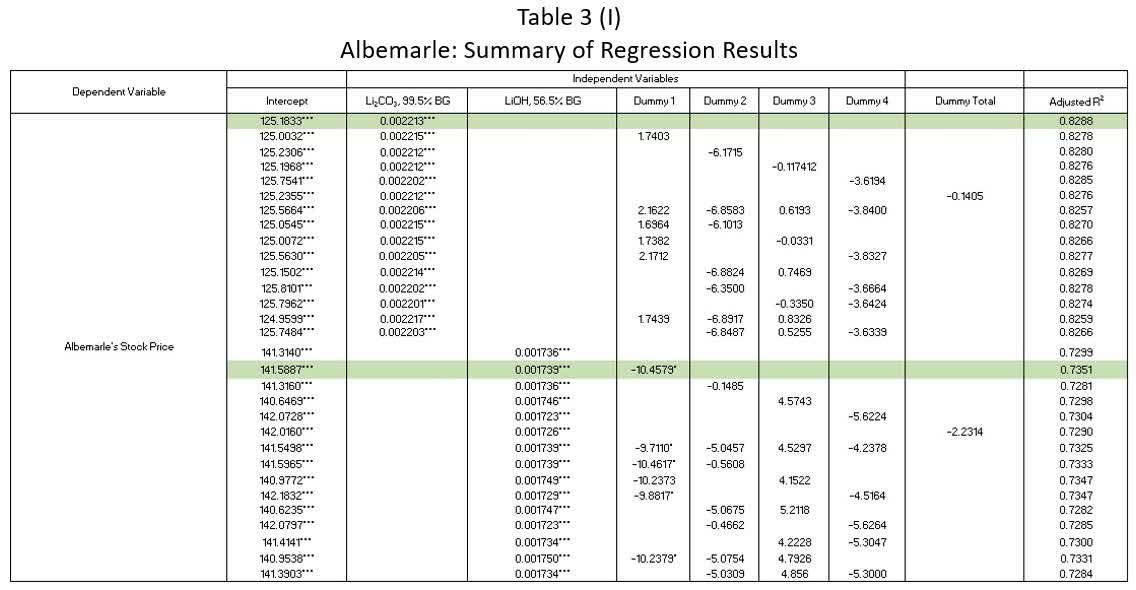

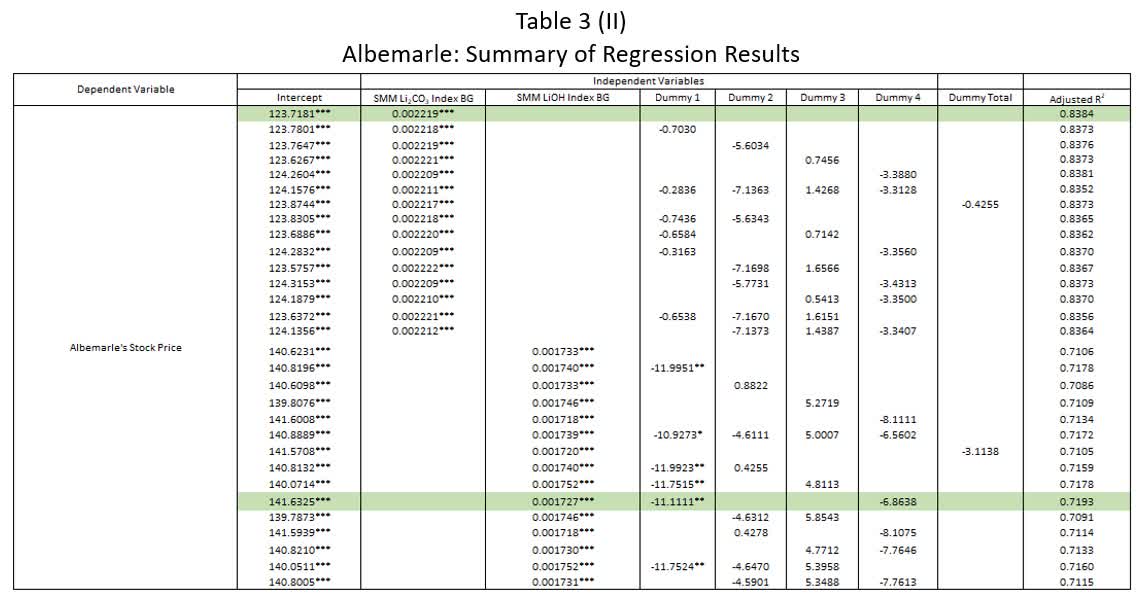

Following the methodology previously described, four additional exercises were performed. In Table 3 (I, II, III, and IV), a summary of the regression results is presented.

As can be seen, a strong relationship between Albemarle’s stock price and lithium chemical prices is confirmed. Note that three different lithium carbonate prices (Li 2 CO 3 99.5% BG, SMM Li2CO3 Index BG, and Li 2 CO 3 99.5% BG CIF China, Japan & Korea) and three distinct lithium hydroxide prices (LiOH, 56.5% BG, SMM LiOH Index BG, and LiOH 56.5% BG CIF China, Japan & Korea) were utilized in this analysis. In the case of Li 2 CO 3 prices , none of the dummy variables, alone or in combination, were found to be pertinent or capable of enhancing the adjusted R 2 as a metric of the regressions' goodness of fit. The situation was slightly different in the case of LiOH prices where dummy 1 and dummy 4 were found to be negative and significant at less than the 10% and 5% level, meaning that market sentiment events, together with the regulatory environment would have had some effect on the decrease in Albemarle’s stock price throughout the study. In sum, we can safely conclude that Chinese spot lithium chemical prices appear to be strongly related to Albemarle’s stock prices with some influence of at least two other non-price factors during the period considered in this research: market sentiment and regulatory environment.

{kind=link}

SMM Finance.Yahoo

Sources: SMM , and Finance.Yahoo .

* Significant at less than the 10% level.

** Significant at less than the 5% level.

*** Significant at less than the 1% level.

{kind=link}

SMM Finance.Yahoo

Sources: SMM , and Finance.Yahoo .

* Significant at less than the 10% level.

** Significant at less than the 5% level.

*** Significant at less than the 1% level.

{kind=link}

SMM Finance.Yahoo

Sources: SMM , and Finance.Yahoo .

* Significant at less than the 10% level.

** Significant at less than the 5% level.

*** Significant at less than the 1% level.

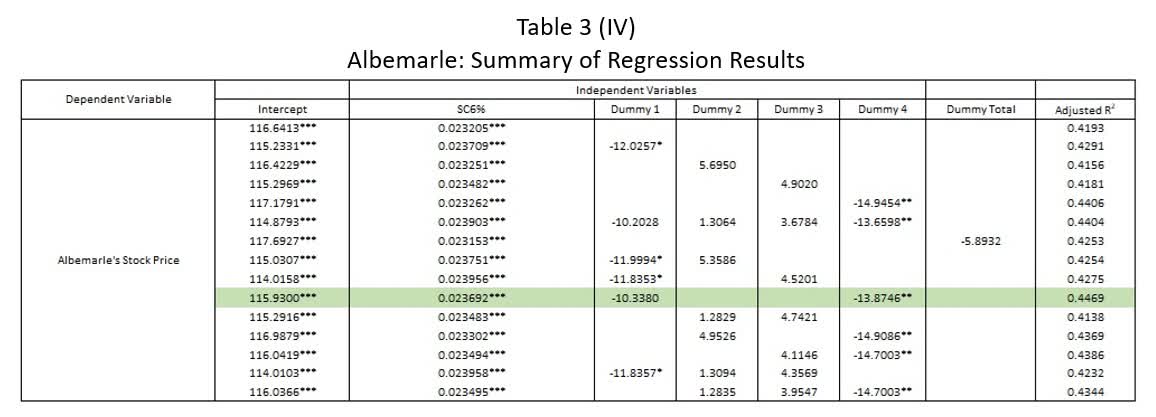

Lastly, a regression of Albemarle’s stock price was run on Spodumene Concentrate 6% (SC6%) price, as well as the four dummy variables and their combinations described above, which ratified the finding that a significant relationship exists between the two prices and the influence of market sentiment and regulatory environment on Albemarle’s stock price.

{kind=link}

SMM Finance.Yahoo

Sources: SMM , and Finance.Yahoo .

* Significant at less than the 10% level.

** Significant at less than the 5% level.

*** Significant at less than the 1% level.

SQM

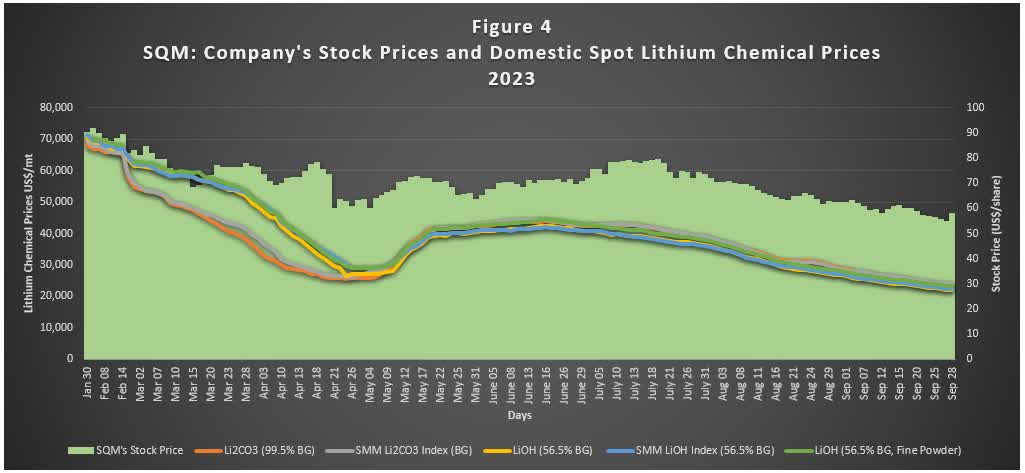

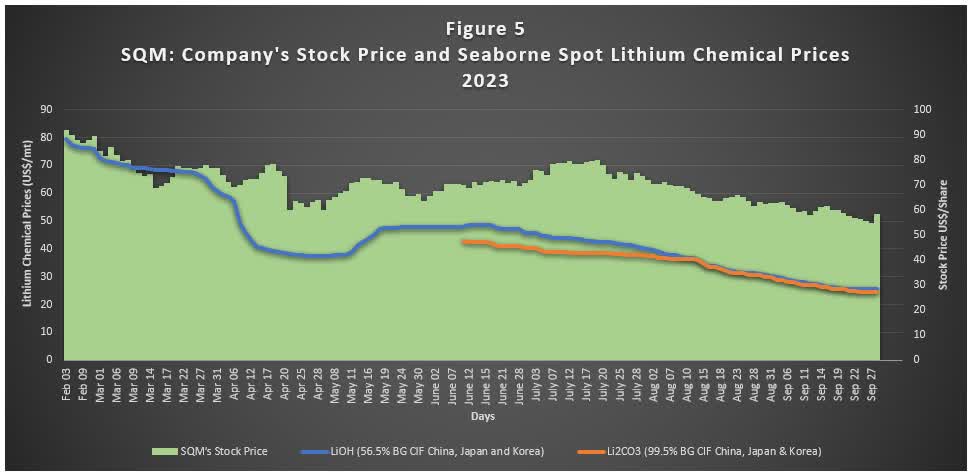

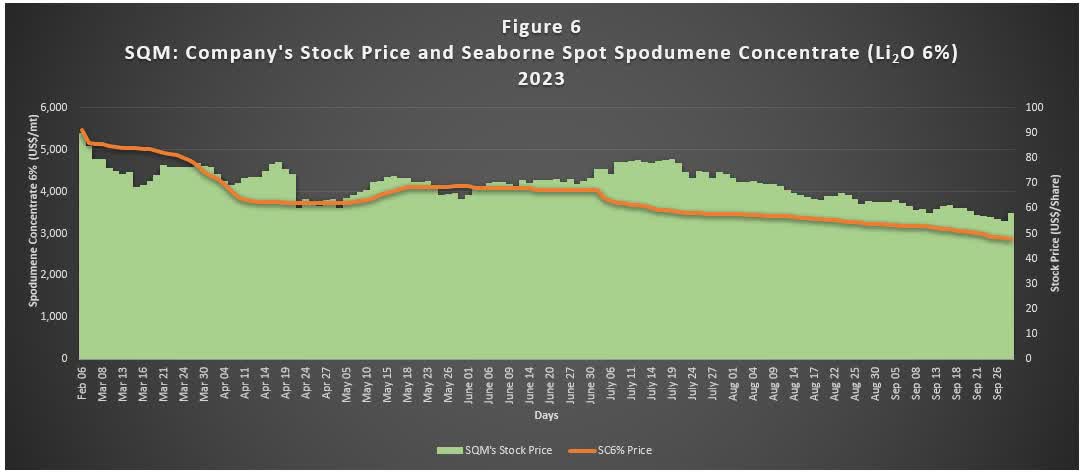

As in the previous analysis, Figures 4-6 depict the changes in SQM's stock price throughout the study concerning two domestic spot lithium carbonate battery grade prices, one seaborne spot lithium carbonate battery grade price, three domestic spot lithium hydroxide battery grade prices, one seaborne spot lithium hydroxide price, and one seaborne spot lithium spodumene concentrate (Li 2 O 6%) in China. The exceptionally high and positive correlation coefficients shown in Table 4 further demonstrate how comparable the declining trends are. Take note also that these indicators were subjected to a two-tailed t-statistic significance test, resulting in a p-value of less than 0.1% in each case.

On average, lithium carbonate's correlation coefficient was 0.84, whereas lithium hydroxide's correlation coefficient was 0.82. Additionally, SC6% had a correlation value of 0.63. This is consistent to some extent with the mix of lithium chemicals produced by SQM 2021 (see slide 6 of SQM's presentation in August 2022) showing that 85% of their total LCE output was made up of lithium carbonate and 15% was lithium hydroxide.

{kind=link}

SMM Finance.Yahoo

Sources: SMM , and Finance.Yahoo .

{kind=link}

SMM Finance.Yahoo

Sources: SMM , and Finance.Yahoo .

{kind=link}

SMM Finance.Yahoo

Sources: SMM , and Finance.Yahoo .

Therefore, we may conclude that Chinese spot prices have a substantial influence on SQM's stock price performance, which also explains why SQM's current pricing model is dependent on Chinese spot prices. Investors will thus probably expressly take the Chinese spot prices into account when deciding whether to buy or sell SQM's shares. Not least, they would give priority to those prices based on the company's mix of mineral and chemical output. Hence, they would look first at the prices of lithium carbonate and lithium hydroxide, which SQM currently produces, and then at spodumene concentrate, which SQM expects to start producing beginning in 2024.

SMM Finance.Yahoo

Sources: SMM , and Finance.Yahoo .

What can we, however, say about additional variables - besides lithium prices - influencing SQM's stock prices?

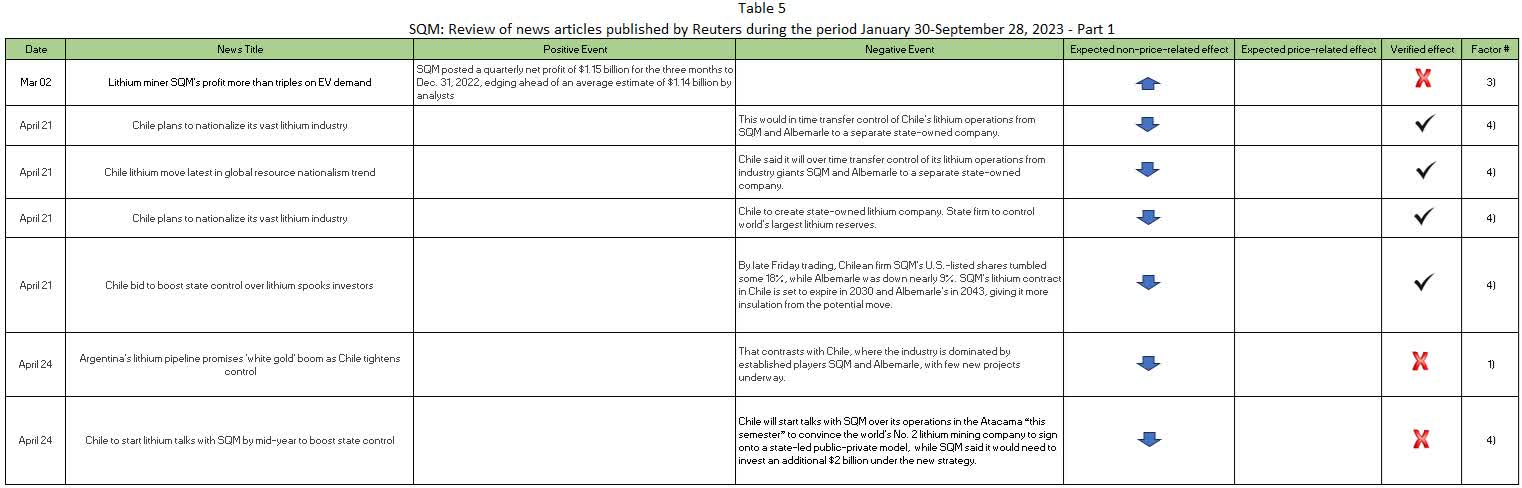

By examining the major events that occurred during the period under discussion, utilizing the same methodology as in the previous instance, we attempt to demonstrate in Table 5, Parts 1-3 how significant those other elements were in determining SQM's stock values.

{kind=link}

SMM Finance.Yahoo

Source: Reuters .

{kind=link}

SMM Finance.Yahoo

Source: Reuters .

{kind=link}

SMM Finance.Yahoo

Source: Reuters .

What follows is a summary of the findings. First, a total of 24 news stories during the period of January 30 to September 28 were considered, of which 23 (96%) had nothing to do with prices and 1 (4%) did. Out of the 24 news stories, 16 (67%) produced valid results, meaning that the anticipated non-price or price-related impacts were backed by the actual movement of the stock prices, and 8 (33%) could not be supported by reality. These data were further broken down as follows. Of the 16 valid outcomes, 15 were unrelated to price and 1 was, and of the 8 invalid outcomes, 8 belonged to the first category and 0 to the second. These results generally are acceptable as long as the methodology used in this study is given enough confidence. Second, the 15 non-price-related valid outcomes were further examined to determine which theoretical variables that have nothing to do with lithium prices and impact stock prices were deemed to be the most significant ones in the particular example of SQM. The outcomes in this example were extremely intuitive: "Regulatory Environment" (11 counts), followed by "Market Sentiment" (4 counts) were seen to be the major factors influencing the price of SQM’s shares. Neither "Company Performance" nor "Macroeconomic Conditions" were found to affect SQM’s stock prices. Third, the price-related valid result alludes to an increase in SQM’s stock prices due to an uptick in Chinese spot lithium prices.

As in the case of Albemarle, because it was found that there was frequently confusion between valid and invalid findings and the inherent correlation between stock prices and lithium carbonate/hydroxide prices, these results should be interpreted cautiously. Specifically, it was discovered that when either lithium carbonate or lithium hydroxide was used as the primary independent variable, the verified effect of the non-price related factors on SQM's stock price occurred in 19 cases, of which 11 produced valid results. This method's underlying assumption that all effects have the same size was another unresolved issue.

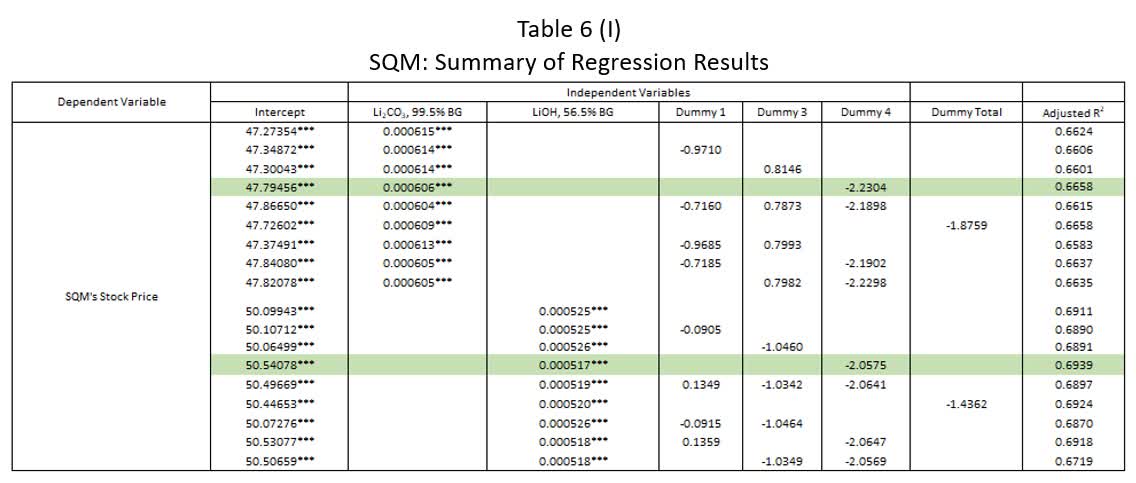

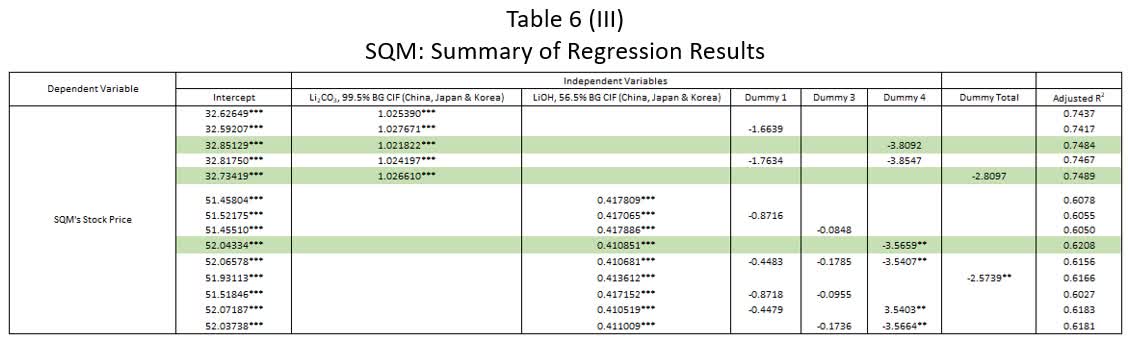

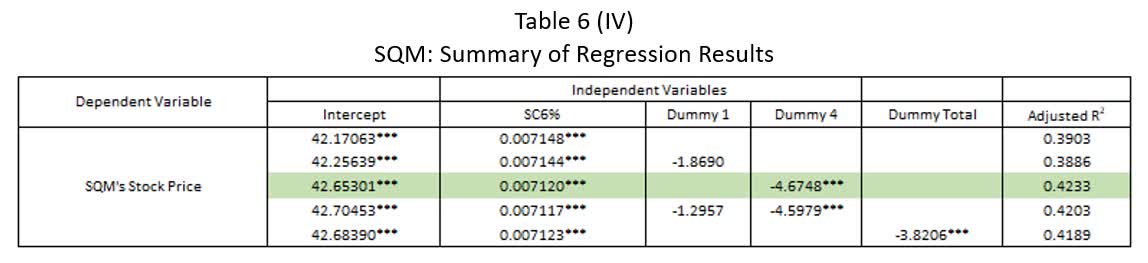

Following the methodology used to analyze the previous case, the same four sets of regressions were run including the different combinations of only three dummy variables: Market sentiment, company performance, and regulatory environment. The results of these exercises can be found in Table 6 (I, II, III, and IV).

A strong association between the price of lithium chemicals and SQM's shares was established. None of the dummy variables, either separately or in combination, were determined to be significant, albeit in some cases, dummy 4 was able to improve the adjusted R 2 , a measure of the regressions' goodness of fit, in the instance of Li 2 CO 3 pricing. However, the results were different for LiOH prices since in all cases dummy 4 was found to be either significant at less than 10 and 5% level or to improve the adjusted R 2 . Finally, when relating SQM’s stock price and SC6% price, a strong influence of dummy 4 (at less than the 1% level of significance) was also revealed.

{kind=link}

SMM Finance.Yahoo

Sources: SMM , and Finance.Yahoo .

* Significant at less than the 10% level.

** Significant at less than the 5% level.

*** Significant at less than the 1% level.

{kind=link}

SMM Finance.Yahoo

Sources: SMM , and Finance.Yahoo .

* Significant at less than the 10% level.

** Significant at less than the 5% level.

*** Significant at less than the 1% level.

{kind=link}

SMM Finance.Yahoo

Sources: SMM , and Finance.Yahoo .

* Significant at less than the 10% level.

** Significant at less than the 5% level.

*** Significant at less than the 1% level.

{kind=link}

SMM Finance.Yahoo

Sources: SMM , and Finance.Yahoo .

* Significant at less than the 10% level.

** Significant at less than the 5% level.

*** Significant at less than the 1% level.

Ganfeng

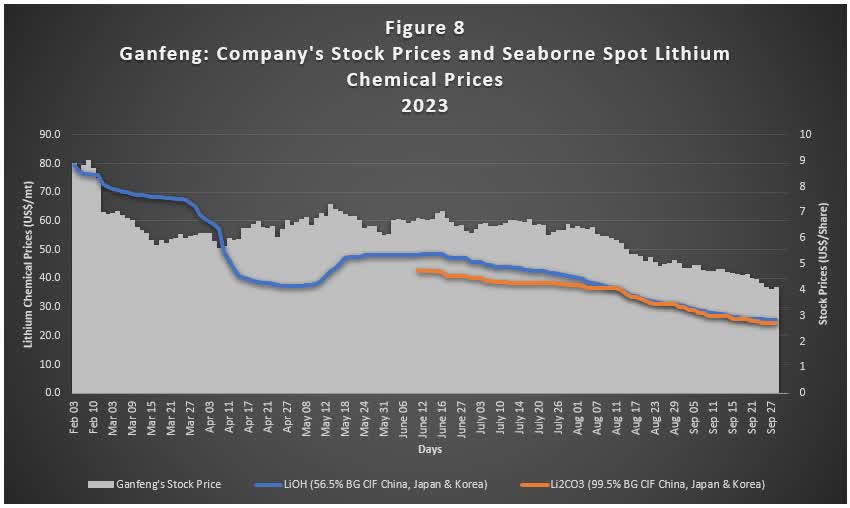

The behavior of Ganfeng’s stock price over the study period is exposed in Figures 7-9, which also show the evolution of three domestic spot lithium hydroxide battery grade prices, two domestic spot lithium carbonate battery grade prices, one seaborne spot lithium hydroxide price, and one seaborne spot lithium spodumene concentrate (Li2O 6%) price in China. Table 7's extraordinarily high and positive correlation coefficients provide more evidence of how similar the dropping patterns are. Also be aware that a two-tailed t-statistic significance test was performed on these indicators, and the results showed that in every case the p-value was less than 0.1%.

{kind=link}

SMM Finance.Yahoo

Sources: SMM , and Finance.Yahoo .

{kind=link}

SMM Finance.Yahoo

Sources: SMM , and Finance.Yahoo .

{kind=link}

SMM Finance.Yahoo

Sources: SMM , and Finance.Yahoo .

SMM Finance.Yahoo

Sources: SMM , and Finance.Yahoo .

The average correlation value for lithium carbonate was 0.84, whereas the average correlation coefficient for lithium hydroxide was 0.68. Note, however, that the carbonate number appears to be inflated by the seaborne indicator obtained from a limited database. Furthermore, the correlation value for SC6% was 0.63. This is somewhat counterintuitive. Following the reasoning applied in the case of Albemarle and SQM, one would expect a greater correlation between Ganfeng’s stock price and lithium hydroxide prices than between the Chinese company’s stock prices and lithium carbonate mainly because Ganfeng produces way more hydroxide than carbonate (See slide 4 in Ganfeng’s 2022 presentation). However, the fact that this is not the case should only call our attention to other not-so-obvious factors or variables that may have to do with this outcome.

So, we are in a position to say that Chinese spot prices may have a significant impact on the direction of Ganfeng’s stock prices but the relatively high correlation coefficient found between stock prices and spot lithium carbonate prices is perhaps picking up some recent developments by the Chinese company in the lithium brine sector, particularly in Argentina. Likewise, the overall relatively lower correlations between those variables may be an indication that Ganfeng, unlike Albemarle and SQM, when it comes to prices, may be relying more on medium and long-term relationships rather than on short-term quotes from the Chinese spot market.

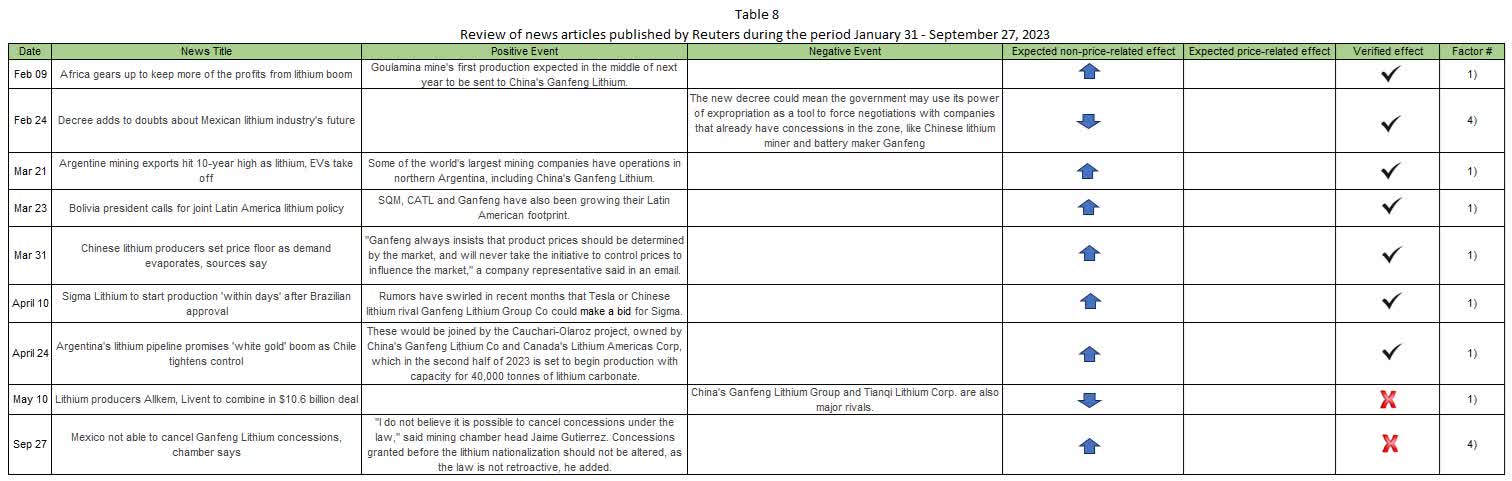

We are now ready to move to the next level of analysis to see how significant other non-price-related variables were in the determination of Ganfeng’s stock prices. In line with the methodology previously applied, in Table 8, a review of news articles published in the period of analysis is shown.

{kind=link}

Reuters

Source: Reuters .

As can be seen, a total of 9 news articles were considered, all of them being unrelated to spot prices. 7 events produced valid results (78%) and 2 (22%) invalid ones. The 7 valid outcomes were then reviewed to find out what other variables besides spot prices influenced Ganfeng’s stock prices. Only two other variables were seen to play a role here, “Market Sentiment” and “Regulatory Environment.” Unlike the other cases, “Market Sentiment” generated 6 out of the 7 valid outcomes, and “Regulatory Environment” produced only one valid result. Lastly, in only one case a valid result also coincided with the type of relationship found between stock and spot prices and the two invalid results matched the lack of association between spot and stock prices.

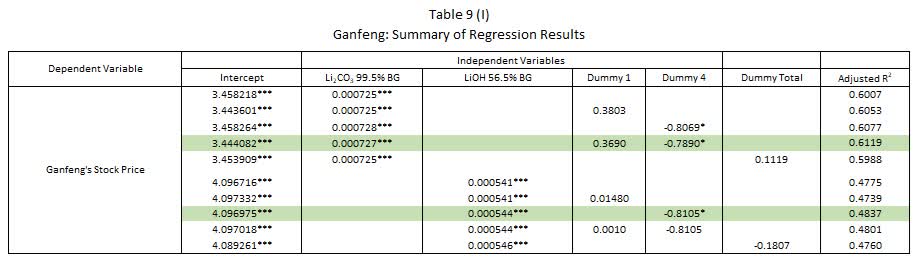

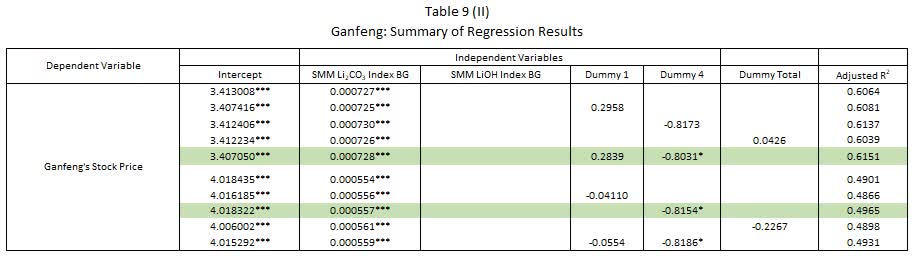

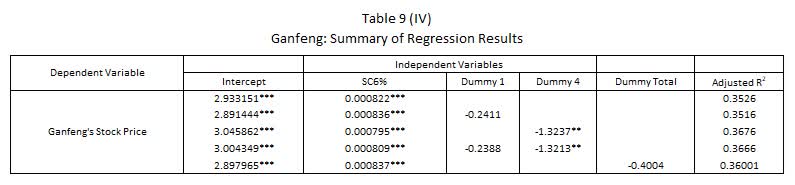

The same four sets of regressions, incorporating various combinations of just two dummy variables—market sentiment, and regulatory environment—were conducted following the general framework utilized to examine the earlier cases. Table 9 (I, II, III, and IV) presents the outcomes of these activities.

The price of lithium compounds and Ganfeng’s stock have a significant relationship. The same appears to be the case with Ganfeng’s stock price and spodumene concentrate 6% price.

{kind=link}

SMM Finance.Yahoo

Sources: SMM , and Finance.Yahoo .

* Significant at less than the 10% level.

** Significant at less than the 5% level.

*** Significant at less than the 1% level.

{kind=link}

SMM Finance.Yahoo

Sources: SMM , and Finance.Yahoo .

* Significant at less than the 10% level.

** Significant at less than the 5% level.

*** Significant at less than the 1% level.

{kind=link}

SMM Finance.Yahoo

Sources: SMM , and Finance.Yahoo .

* Significant at less than the 10% level.

** Significant at less than the 5% level.

*** Significant at less than the 1% level.

{kind=link}

SMM Finance.Yahoo

The dummy variable 4 (Regulatory Environment) was the only significant non-price variable in most regressions, although in some cases dummy 1 (Market Sentiment) was seen to improve the adjusted R 2 . Hence, despite in the previous examination, we found more news articles relating to market sentiment than the regulatory environment affecting Ganfeng’s price, the regression analysis established exactly the opposite. This points to the danger of using that methodology in this type of study.

Tianqi

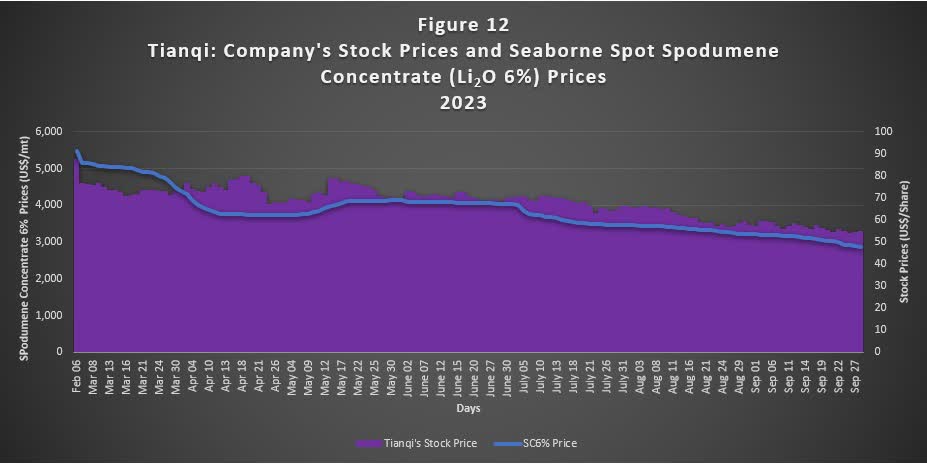

Figures 10-12, which also depict the evolution of the lithium compound and concentrate prices, previously presented for the other three cases, show the behavior of Tainqi’s stock price over the study period. The significantly high and positive correlation values in Table 10 offer more proof of how similar the downward trends are to one another. Also be aware that these indicators were subjected to a two-tailed t-statistic significance test, and the findings indicated that the p-value was always less than 0.1%.

The average correlation value for lithium carbonate and lithium hydroxide was 0.80, whereas the correlation value for SC6% was 0.78. At first sight, the relevant correlation number would be that of SC6% since Tianqi essentially only produces that product despite some failed attempts to diversify its production. However, given the insignificant difference between correlation coefficients, there is nothing much more to be said about it.

{kind=link}

SMM Finance.Yahoo

Sources: SMM , and Finance.Yahoo .

{kind=link}

SMM Finance.Yahoo

Sources: SMM , and Finance.Yahoo .

{kind=link}

SMM Finance.Yahoo

Sources: SMM , and Finance.Yahoo .

SMM Finance.Yahoo

Sources: SMM , and Finance.Yahoo .

Based on the above results, we ratify a strong relationship between the Chinese spot prices and Tianqi’s stock prices with the correlation between SC6% and stock prices reflecting the highest value of the Big Four. The latter result makes a lot of sense considering that Tianqi’s main product is SC6%. Another important outcome is that the lower overall correlation coefficients than those found for Albemarle and SQM may be pointing to the fact that, just as in the case of Ganfeng, Tianqi would also rely more on contractual agreements rather than the spot prices for the commercialization of its lithium.

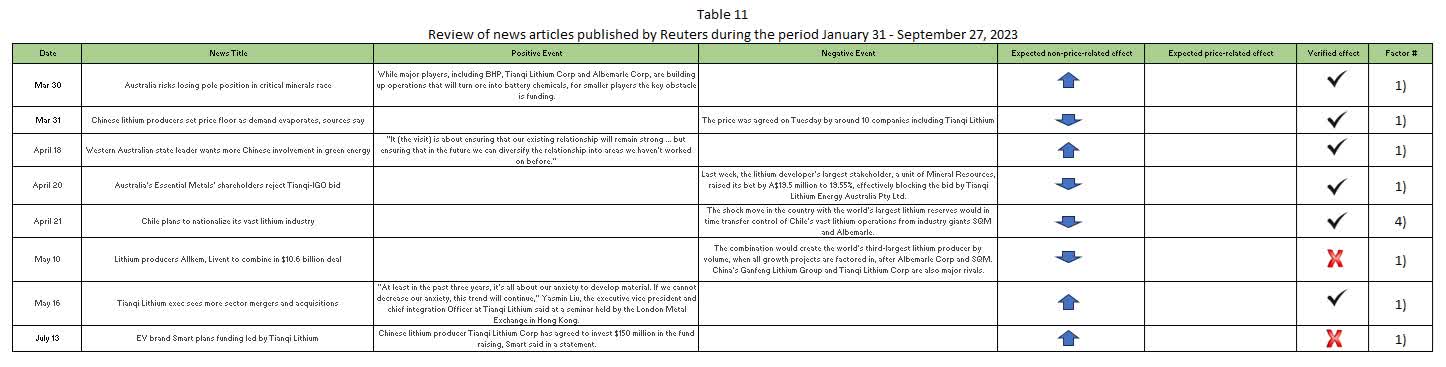

We may now go to the next stage of the investigation to find out how important factors unrelated to price were in determining Tianqi's stock prices. According to the previously used technique, a review of news stories released during the analysis period is displayed in Table 11.

{kind=link}

Reuters

Source: Reuters .

As is evident, eight news items in total—all unrelated to spot prices—were taken into consideration. Two events (25%) yielded invalid outcomes, whereas six events (75%), valid ones. The six valid results were then examined to determine if Tianqi's stock prices were impacted by factors other than spot pricing. As with Ganfeng, only "Market Sentiment" and "Regulatory Environment" were considered to be significant additional elements. Note that, "Regulatory Environment" yielded just one valid result, whereas "Market Sentiment" gave five of the six possible results. Finally, two invalid findings matched the absence of a correlation between spot and stock prices, and in three cases, a valid result also matched the kind of link discovered between spot and stock prices.

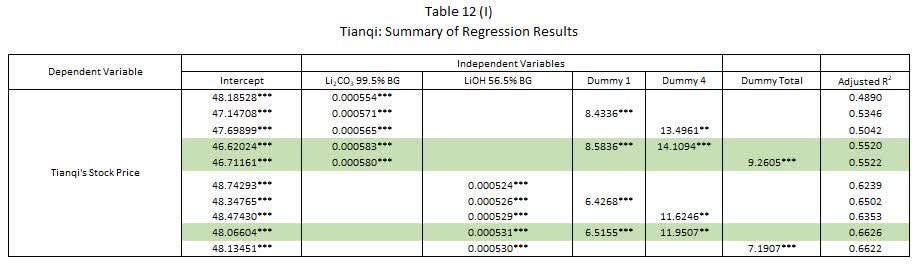

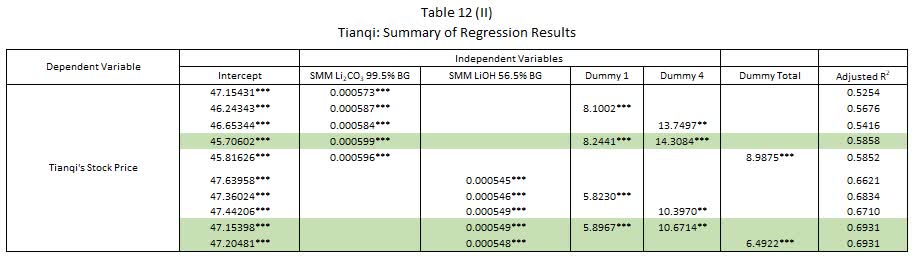

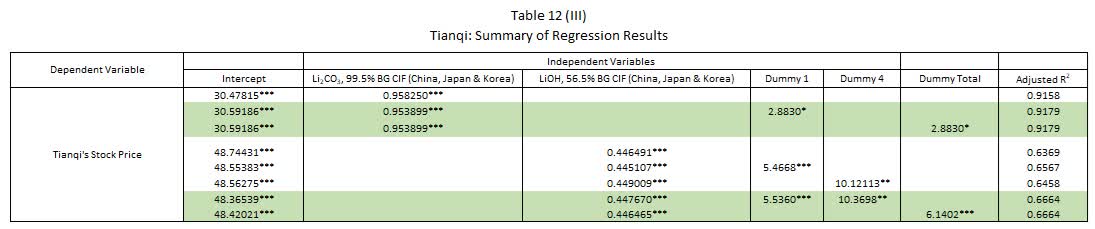

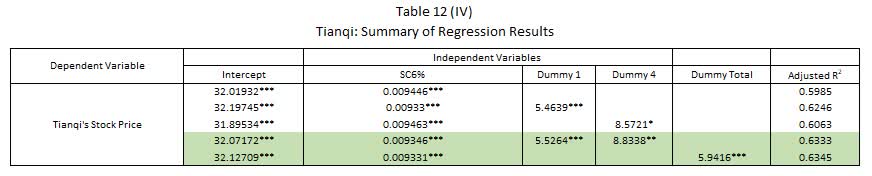

Following the basic framework used to analyze the previous examples, the same four sets of regressions were carried out, combining different combinations of just two dummy variables: market sentiment and regulatory environment. The results of these efforts are shown in Table 12 (I, II, III, and IV).

A substantial correlation exists between the price of lithium compounds and Tianqi's shares. It looks like the price of spodumene concentrate (6%) and the stock price of Tianqi, are also highly correlated.

{kind=link}

SMM Finance.Yahoo

Sources: SMM , and Finance.Yahoo .

* Significant at less than the 10% level.

** Significant at less than the 5% level.

*** Significant at less than the 1% level.

{kind=link}

SMM Finance.Yahoo

Sources: SMM , and Finance.Yahoo .

* Significant at less than the 10% level.

** Significant at less than the 5% level.

*** Significant at less than the 1% level.

{kind=link}

SMM Finance.Yahoo

Sources: SMM , and Finance.Yahoo .

* Significant at less than the 10% level.

** Significant at less than the 5% level.

*** Significant at less than the 1% level.

{kind=link}

SMM Finance.Yahoo

Sources: SMM , and Finance.Yahoo .

* Significant at less than the 10% level.

** Significant at less than the 5% level.

*** Significant at less than the 1% level.

Both dummy variable 1 (Market Sentiment) and dummy variable 4 (Regulatory Environment) were significant in most regressions. The only exception was Li 2 CO 3 , 99.5% B.G. CIF (China, Korea & Japan), although this was because there were no news events over the period for which data for this variable were available. In general, these results are consistent with the news articles analysis where market sentiment and regulatory environment were also found to be important in explaining the evolution of Tianqi’s stock price. However, one strong word of caution is in order here regarding the results for dummy 4.

As shown in Table 11, there was only one news article concerning the regulatory environment for Tianqi. It appears to be too risky to draw any strong conclusions about the dummy variable’s effect in this scenario. There are at least three reasons for this. One is limited variability because, with only one “1” in more than 140 data points, the dummy variable has very low variability which makes it challenging to reliably estimate its impact. Another is potential overfitting because the model might be overfitting to this single outlier point, leading to a significant but potentially misleading coefficient for the dummy variable. Lastly, a third one is uncertainty in prediction, because the model’s ability to predict stock prices accurately when a regulatory event occurs (i.e. when the dummy variable is 1) is highly uncertain, as it’s based on extrapolation from a single data point. All of this explains why, in contrast with all the previous results, the coefficient of dummy 4 was significantly positive.

Summary and Conclusions

In this article, it is argued that two types of factors drive the stock prices of the Big Four lithium companies. One refers to the price of lithium chemicals and ores that these corporations produce and sell which is the most obvious one. Here a clear positive relationship is expected. That is, as the prices of chemicals and ores of lithium go up, the price of the stocks also increases and vice versa. The other pertains to non-price related variables such as Company Performance, Market Sentiment, Macroeconomic Conditions, and Regulatory Environment. In this case, the effects are likely to be not only variable but temporary. As a first approximation, a review of events (as described by news articles) that took place over the period under consideration was performed to see whether a given event had an immediate effect on the stock price. As argued in the study, there are two problems with this approach. First, in several cases, the verified effect of the non-price related factors may coincide with that of the spot lithium prices on the given company’s stock prices. And, second, this method implicitly assumes that all effects are of the same size. To address these challenges, a regression analysis has been applied using stock prices as the dependent variable and the different lithium prices, together with dummy variables for each of the non-price related factors mentioned above, as the independent variables.

A summary of results and some general conclusions follow.

- A highly significant positive association between stock and spot prices is confirmed for all Four Big Lithium companies, using both correlation and regression analysis. The fact that the linkage is much stronger for Albemarle, SQM, and Tianqi than for Ganfeng may be an indication of the different influence of the spot market on the sales strategy of lithium companies. Note that taking the 7 lithium prices included in this analysis into consideration, the respective average correlation coefficients were: 0.83, 0.80, 0.80, and 0.73. As mentioned above, in their Q2 Earnings Call, both Albemarle and SQM declared that between 80 and 85% of their contracts were variable and that they specifically sold between 15 and 20% of their products in the spot market. As I have argued elsewhere ( See my post on X ), chances are those variable contracts are likely to be related to spot prices. So, if they show the strongest relationship between stock and spot prices, it is essentially because they have incorporated the spot prices into their marketing strategies. Note however that in their Q3 Earnings Call, they no longer talk about variable contracts which may be a way to hide the explicit recognition of the danger that this kind of strategy entailed. As for Tianqi, we don’t have much information on where this company sells its products but we can presume that its relationship to the China market in general and the Chinese spot market in particular is significant. Lastly, Ganfeng’s relatively lower average coefficient of correlation may point to the fact that it relies more on contractual arrangements than on the Chinese spot market to sell its chemicals. Be aware that Ganfeng has probably been over the years the most important supplier of lithium to Tesla.

- The relationship tends to be stronger when using lithium carbonate prices rather than lithium hydroxide prices in the case of Albemarle and Ganfeng, whereas the opposite holds for SQM and Tianqi. This finding is a bit puzzling. As a first approximation, one could think that this might be related to the product mix of each of the Big Four. That only seems to work for Albemarle. Not for Ganfeng, which produces almost no lithium carbonate. Neither does for SQM or Tianqi which either produce very little lithium hydroxide or none. Another possibility is that investors consider the most representative product of the market as the one to look at for their decisions to invest. But this again would take us nowhere to the extent that what is highly priced in one market may not be in another. However, we could give this a twist. Lithium carbonate is the chemical of choice in China nowadays, whereas lithium hydroxide is more demanded ex China. This would explain why despite Ganfeng producing mostly lithium hydroxide, its stock price would be more correlated with lithium carbonate. In the case of Albemarle, the reasoning would be that even though the company has a lithium operation in Chile, its partnership with Tianqi in Australia would not only be much greater in size but also more integrated into the Chinese market. Likewise, despite SQM not producing much lithium hydroxide, within its radius of action, this compound would be more highly valued than carbonate. Lastly, although Tianqi essentially produces spodumene concentrates, its stock price would be more correlated with lithium hydroxide prices because it has already built a lithium hydroxide plant in Australia. For that reason, Tianqi would be more related to the market outside of China than to the Chinese domestic market.

- Except for Tianqi, spodumene prices generate a much weaker relationship with stock prices than either carbonate or hydroxide. In fact, in the case of Tianqi, lithium carbonate prices do not seem to count much for investors; only hydroxide and spodumene concentrates do, for the reasons explained above and as per its correlation coefficients with the company’s stock prices.

- Regulatory Environment (Dummy 4) appears to be by and large the most important non-price related factor affecting the stock prices of the Big Four. However, it was found to be relatively more relevant for Ganfeng and SQM (in this order) than for Albemarle, while it was not possible to draw any conclusion regarding the impact of this variable on Tianqi’s stock prices. This discovery is quite revealing. Even though both Ganfeng and SQM did seem to have been hit by the regulatory environment, investors appear to have picked up this effect in a different way. For instance, the nationalization of lithium in Mexico would have been terrible news for Ganfeng given that its $400M investment in the Sonora Lithium Project would be at serious risk of loss let alone any possibility of generating profits for the company. As for SQM, the threat of the Chilean government to SQM to take control of the company even before the conclusion of SQM’s contract affecting the viability of SQM has no doubt had a significant impact on investors’ decision to buy more SQM’s shares in the stock market. Lastly, Albemarle seems to be the least affected company by the regulatory environment of the Big Four, presumably because, unlike SQM whose contract to extract lithium from Salar de Atacama ends in 2030, it holds a contractual arrangement for lithium production with the Chilean state until 2043.

Why I am Bullish on SQM

If we agree that to a great extent, the stock prices of the Big Four Lithium Companies are heavily dependent on the spot lithium prices, given the spot price trend identified until September 2023, not substantially modified to the present day, at first sight, it would be extremely risky to be bullish on those stocks. However, I resist adding myself to the list of analysts who are now claiming that we will have to wait until 2028 or later to see a general lithium price rebound in China and elsewhere. Based on the results of this study, this clueless view of the lithium market would condemn the Big Four to failure in the coming years. As I have suggested in several posts on X.com over the last four weeks or so, a price rebound may take place in the following months only followed by a price stabilization at a slightly higher level than the current one until around 2025 with an expected increase to and subsequent stabilization at twice as high that level between 2026 and 2030. These prices could suffice to guarantee the viability of any good lithium project. Hence, I declare myself bullish on SQM, the stock that I consider is better suited to face the turbulent times we anticipate in 2024 and beyond.

What makes SQM the best investment option in the lithium space nowadays?

As of today, SQM is not only the world’s largest lithium company by market capitalization but also the one with the best performance year-to-date. For one thing, with the recent rally for SQM shares following the recent announcement about inking a Memora ndum of Understand ing ((MOU)) with CODELCO for the development of Salar de Atacama from 2025 to 2060, SQM’s market capitalization rose to $17.20B surpassing Albemarle’s number that now stands at $16.96B. So now SQM is the world’s largest lithium company as measured by market capitalization. For another, as shown in Figure 13, despite all Big Four’s stock prices falling throughout 2023, SQM’s shares decreased relatively less than those of the other three lithium companies.

Valuation, Growth, and Profitability

In what follows I compare three sets of indicators about criteria of valuation, growth, and profitability for SQM and Albemarle to find out which stock provides the best results. This is shown in Tables 13-15. This comparison is plausible to the extent that these two companies have similar market capitalization. Note that SQM performs better than Albemarle in two sets of indicators (Valuation and Profitability) and worse in one (Growth).

How would we rank these sets of indicators to assess the stocks?

Since the significance of these indicators varies depending on our investing goals, risk tolerance, and chosen investment strategy, there is no one "correct" ranking for them. But first, let's break down each signal and see how our viewpoint could affect how important they are concerning one another:

Valuation:

Meaning: Evaluates the current price of a stock concerning its underlying, fundamental value. Price-to-Earnings (P/E), and Price-to-Book (P/B) analysis are examples of common valuation measures.

Pros: Offers value investors points of entrance and exit by assisting in the identification of stocks that may be overpriced or undervalued.

Cons: Depending on the assumptions and techniques of valuation, there is a chance that future growth potential may not be fully captured.

{kind=link}

Reuters

Source: Reuters.com.

Growth:

Meaning: Assesses the possibility of future increases in revenues and earnings for a business. The growth ra tes of revenue and earnings per share ((EPS)) are important growth metrics.

Pros: Attracts growth investors looking for substantial returns from businesses with room to develop.

Cons: May ignore present profitability and be vulnerable to changes in the economy or other external variables.

Profitability:

Meaning: Measures a company's ability to generate profits from its operations. Common profitability metrics include net income margin, return on equity ((ROE)), and operating cash flow.

Pros: Provides insights into a company's operational efficiency and ability to generate sustained returns, especially relevant for income investors.

Cons: May not reflect future growth potential and can be impacted by accounting practices or temporary fluctuations.

As argued above, we would now make some ranking considerations, based on our investment objectives, our risk tolerance, and our investment horizon.

Seeking Alpha

Source: Seekingalpha.com ( SQM ), and SeekingAlpha.com ( ALB ).

In terms of our investment objectives, we could have three different strategies.

- Value investor: Prioritize Valuation, followed by Profitability and then Growth.

- Growth investor: Prioritize Growth, followed by Valuation and then Profitability.

- Income investor: Prioritize Profitability, followed by Valuation and then Growth.

As we can see, in two of these strategies, Growth would be the least important factor to be considered which would provide support for our view that SQM might be a better investment option than Albemarle.

Likewise, in terms of our risk tolerance, we would favor Growth with higher risk tolerance, while lower risk tolerance might favor Valuation and Profitability. Hence, again, according to this perspective, SQM could be seen as well as a better investment option than Albemarle.

Lastly, in terms of our investment horizon, in general, long-term investors might weight Growth higher, while short-term investors might focus more on Valuation and Profitability. Once more, since in this case, we are interested in our top 2024 pick, we might be inclined to select SQM over Albemarle.

Seeking Alpha

Source: SeekingAlpha.com ( SQM ), and SeekingAlpha.com ( ALB ).

Risks

Of course, there are some risks involved in this kind of perspective. One is that the slight price rebound I advocate could not take place and that rather prices deepen into a further decline to reach a US$10,000/t LCE level mainly due to what I have denominated a lithium battery overcapacity and a lithium oversupply. However, under the current state of lithium technology and with the prevailing market conditions, I doubt this would be sustainable leading inexorably (and relatively soon enough) to an upward price correction. This implicitly assumes that the much-hyped direct lithium extraction (DLE) technologies will take some time to take hold contributing to a significant improvement in lithium recovery and efficiency, with positive effects on costs and prices.

Another is that the ongoing slowdown in demand for EVs gets worse particularly in China also pushing lithium prices down to the above-mentioned level or lower. Although this is entirely possible not only in China but also in other parts of the world, it could be ameliorated or reversed by what I have called a positive EV demand shock whereby the two leading EV makers (BYD and Tesla) launch mass-produced low-cost EVs to the market to generate a significantly increased demand for those cars and consequently for lithium batteries and lithium. Note that BYD’s Seagull introduced into the Chinese market a few months ago could have already started this new EV wave with Tesla following suit fairly soon.

Finally, as we have seen in the first part of this article, the regulatory environment (i.e. the threat of the Chilean government to SQM to take control of the company even before the conclusion of SQM’s contract affecting the viability of SQM) is relatively important in determining SQM’s stock prices. However, this threat has been taken care of with the MOU because under its terms there is no considerable risk that the new agreement could affect negatively the viability of SQM. On the contrary, it could benefit SQM by providing it with security of access to the richest lithium resources in the world for another 30 years while expanding significantly the quota of production to guarantee SQM’s competitiveness in the lithium market. In this context, we could think now of the risk that, for some reason, the MOU signed by CODELCO and SQM does not materialize into a final contract. While this would have devastating effects on SQM, we have at least two reasons to believe that there is very little chance this could occur. First, the MOU is very advantageous to Chile because it establishes that, beginning 2031, in addition to the taxes and royalties currently paid by SQM, under the new joint venture (JV), the country will have access to profits as well, considerably increasing its total revenue from lithium. Second, although some indigenous communities have questioned the MOU because they were not consulted, the mining minister has recently declared that dialogue continues and that before the final contract is signed those peoples will be consulted.

Based on all the arguments above, SQM is my top 2024 pick and I highly recommend buying this stock in the coming year.

Seeking Alpha

Source: SeekingAlpha.com ( SQM ), and SeekingAlpha.com ( ALB ).

Editor's Note : This article was submitted as part of Seeking Alpha's Top 2024 Long/Short Pick investment competition , which runs through December 31. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

Big 4 Lithium Stocks And Spot Lithium Prices - Why I Am Bullish On SQM