BLRDY - Billerud: One Of The More Undervalued Forestry Business Out There

2023-09-13 06:18:43 ET

Summary

- Despite recent decline, the author remains convinced of Billerud's long-term investment potential for conservative investors.

- Billerud is facing industry-wide pressure due to customer inventory destocking, impacting sales prices and finances.

- The company's profitability and positive cash flow, along with its efficiency program and low debt, make it an attractive investment opportunity.

Dear readers/followers,

I've been covering Billerud (BLRDF) for a number of years, and I've started establishing positions in the company both commercially and personally in the past few months. A few of the positions are the result of assigned put options, a few are straight buying of common shares.

Despite the company seeing decline since both my bullish, recent articles , I remain firmly convinced of the company's deep attraction as a long-term investment. In this article, I'll show you why that is, and why I believe that over time, Billerud can actually deliver high double digit or low triple digit alpha for conservative investors.

Updating on Billerud after 2Q23 - The appeal is still there

Despite covering the company only sporadically, I've been investing in Billerud for years. This is the sort of cyclical company that declines in downcycles, making it a superb buy, but it also requires you to recognize overvaluation, and actually sell at around 130-145 SEK/share. This has been a profitable approach for Billerud for several years.

Remember, Scandinavia in general is a geography you want to look at if you like timber/wood/fiber/paper/carton investments, and I invest in most of these. I don't just invest in Billerud, but companies like UPM (UPMKY), Enso (SEOJF), Huhtamäki (HOYFF). I also wrote options on how many of these businesses were possible.

Billerud has been and continues to be under share-price-related pressure. The reasons for this pressure are obvious. All of the industry is under the trend of customer inventory destocking, which is softening the end market demand. Sales prices are "okay" and relatively stable with some exceptions - inventory trends are not, and reevaluations of said inventory is impacting finances as well.

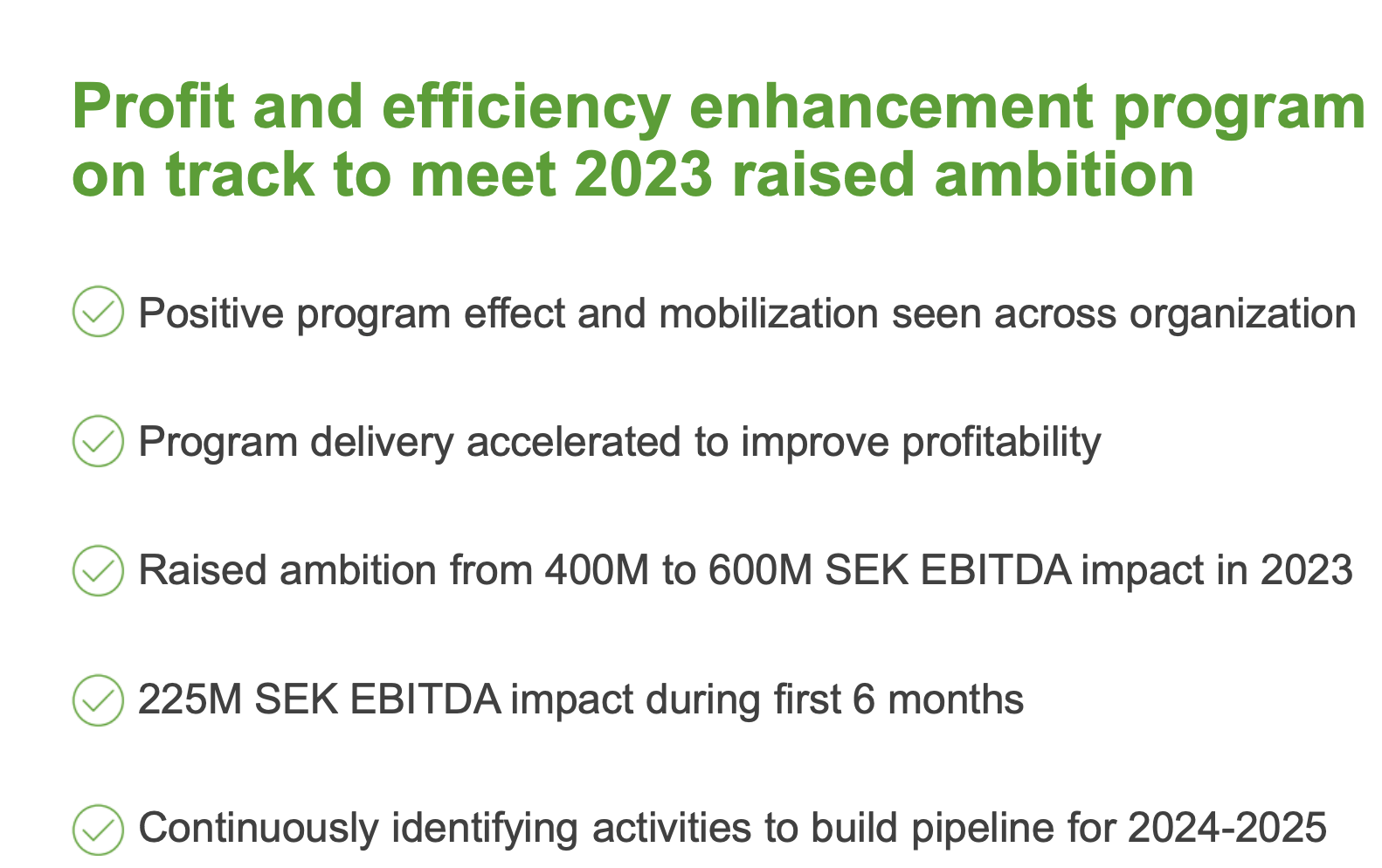

However, Billerud remains profitable and manages positive cash flow on a quarterly basis despite this, with tight inventory control, pushing quality and sales, and working its efficiency program for all it's worth, with a new annual target of 600 MSEK.

{kind=link}

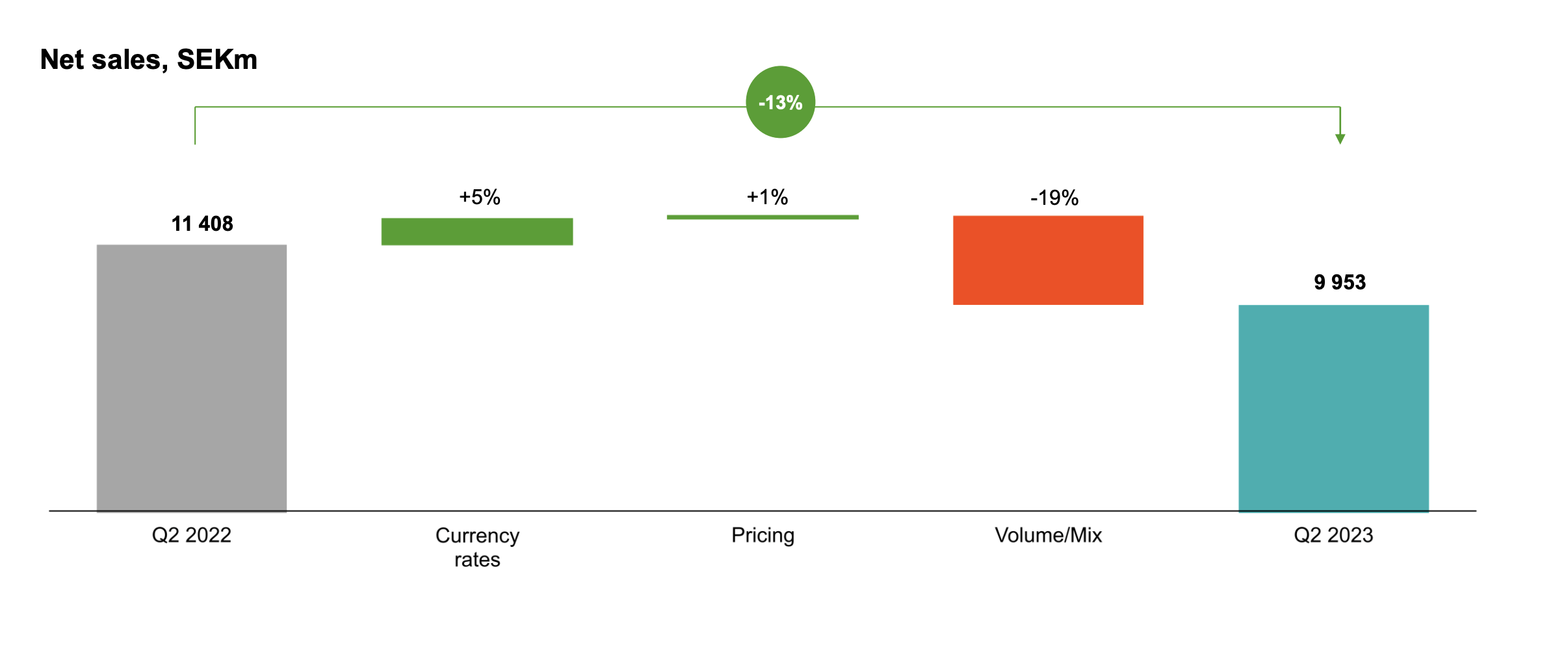

However, in the end, nothing the company can do can make up for what you see here, or in terms of adjusted EBITDA. Impacts like volume, inventory recalculations, maintenance, and other factors have pushed down from a record level of 2.2B SEK in 2Q22, to less than 200M SEK in 2023 for 2Q23. Obviously a massive impact, with significantly challenging marketing conditions, and no improvements expected going into 3Q23. That makes this a much longer-term play than it has been for some time - but also a profitable one, if entered into at the right price.

The company is doing some housecleaning. A new reporting structure is in place as of this quarter to make sure to capture some of the efficiencies in the company. It's important to recall that this company is one of the better players in the entire industry, despite the current results, with an annual production capacity of almost 5M tonnes an annual basis, working with a product like liquid packaging board, cartons, containers, kraft, sack paper, pulp, graphic and specialty.

The trends we see at this time require the company to work with curtailment in most of the mills, and suffer a negative sales mix from relative pulp sales, without being able to push pricing beyond the levels needed to sustain the profits we've seen for the past year.

The one trend that's going to help to go into 3Q is lower input costs , meaning cost advantages for chemicals, energy, and stable logistics costs. Fiber costs are up - the price for pulp and timber hasn't declined as much as we might expect, so that's an important trend to be aware of.

Operating cash flow trends are nonetheless positive, and this latest year or two of sales has helped put the company in a very advantageous position in terms of debt. The company's net debt/EBITDA is currently at a sub-1.5x level, which is to be put into the context of the company's own 2.5x target. The company, as such, has plenty of cash on hand, as well as a new credit facility of 5.5B SEK. Compare this to an expected base CapEx of 2B.

The focus should, for the time being, be on the company's efficiency program, on track to meet the company's 2023 targets.

{kind=link}

The company is also back to normal production in the Escabana Mill, and the matter has been closed with a total impact of around 85MSEK for 2Q23. Other critical projects for the company are well on track. The Frövi boiler will start well ahead of time, and this is despite a national cement crisis and years of COVID-19 disruption. The company deserves praise for this - and the USA transformation project is chugging along well.

This part of the project involves a new carton board machine, a new wood yard, a new BCTMP plant, upgrades for the mill, and other cost efficiencies. The company is being supported here by the state government of Michigan.

On a high level, Billerud continues to focus on the retaining or transformation of critical infrastructure and production, while continuing to divest non-core assets. One of those divestments was Managed Packing back in July, as well as Billerud ownership of Kezzler AS, with only a marginal impact.

Unlike other companies, and this is perhaps the one part of the strategy that I do not agree with, the company is still seeking to divest over 9,000 hectares of forest land in Sweden. Even if some of this might be considered non-core by the company, I am personally in favor of keeping and working with whatever land the company has - expanding it whenever possible. I believe future valuation of forest land cannot be overstated given what we're seeing on the market here.

None of these quarterly trends that we're seeing here are encouraging - but those quarterly trends do not take away from what I view as immense positives here, including a market-leading percentile of 50%+ gross margin, and net margins at almost 10% for a company like this. Billerud is without a doubt a market leader. These companies have somewhat different mixes and foci - which is also why I can see the appeal of many of them, and why I continue to own shares in all of the ones I mentioned. Some are focused more on specialty papers and luxury packaging. Some are focused more on biofuel and the timber/raw material side of things. Some are focused on an appealing mix of it all. But with Russia out of the game in terms of much of the import/export, Scandinavia has become an even more critical part of the global supply of paper, cartons, and related products - and investing in those sorts of critical dependencies is something I am very happy to do - especially with the current non-Swedish FX being so unfavorable in terms of non-Swedish investments.

Let's look at valuation and see what we have here.

Billerud - Plenty to like about the low valuation - The upside is high

Billerud is a very volatile company to invest in, of this there is no doubt. Earnings can cycle negative for several years, and you're collecting 4-6% dividends but very few positive returns otherwise. Then, there's a sudden demand spike, and the company is able to deliver earnings in the billions, turning your RoR into triple digits - but usually only temporarily. That's why I sold Billerud back in 2021 and only started buying back shares fairly recently.

Estimating the company on a forward-looking basis, we find a possibility of annualized returns of 25.9%, to a total RoR of 70% on a forward 3-year basis - and this is only when considering a forward P/E of 15x. If we go by the 5-10 year normalized P/E, then those returns start inching up towards the triple digits, with a 106.8% total RoR for the company at an 18.5x P/E, which is the 5-year average.

There's plenty of volatility to Billerud - no doubting or discussing that. But the fundamental upside when you're buying the company at a valuation that implies a P/S of less than 0.5x, a P/B of less than 0.8x - that's a pretty damn good upside.

And remember - my own way of investing in Billerud is taking advantage of the volatility and writing CSPs with significantly lower strikes - usually in the low to mid-70s, which puts these multiples at even lower levels. I've been able, using this strategy, to ensure annualized RoR in the range of 15-20% at most, and usually around 8% at the very least. At 70-75 SEK, I'm very willing to "BUY" the company even in this sort of downcycle. I know the company, when things turn around, is going to see RoR putting it to the 110-140 SEK/share, which will then enable attractive rotation with, once again, very good returns.

S&P Global targets for this company range between 75 SEK on the low side to 110 SEK on the high side, and for once I'm mostly in agreement with the low PT. At anything around 75 SEK PT, this company becomes a "STRONG BUY". In an upcycle, we're looking at less than a 125-130 SEK, which is the PT I've also held for Billerud - but I believe it will take time for the company to recover to this level.

So, for the time being, the "right" way to go for Billerud remains cash-secured PUTs whenever those are available. I've already seen a few assignments here for the company, which means I actually own common shares in the company as well. At my cost basis, this in no way bothers me.

Going forward, I will continue to write attractive options and keep an eye on Billerud's operations, as I do with other companies in the same sector. I use a very similar strategy for most of the aforementioned companies in the same sector.

Thesis

- Billerud is a very solid packaging/forestry company with assets and sales in both NA and Europe. It's top-tier in terms of margins and profitability, and after its recent M&A, I believe it's in a position than ever before. At the right price, the combination of packaging resilience and dividend payouts makes Billerud an absolute "must-have" to me.

- My current PT comes to a conservative 10-12x P/E, which implies a 125-130 SEK share price - I go to 127.5/share.

- That makes the company a "BUY". I already own a large stake, but I'm buying more, and I'm not shifting my price target at this time. It's 127.5.

Remember, I'm all about : 1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company therefore fulfills every investment criteria I currently hold and I give it a "BUY" here.

For further details see:

Billerud: One Of The More Undervalued Forestry Business Out There