VET:CC - Birchcliff Energy: Dividend Yield Falls Peyto And Whitecap Make More Sense

2024-01-19 09:31:15 ET

Summary

- Birchcliff Energy cut its dividend by 50%, disappointing investors who were attracted to the high yield and large reserves.

- The company's production guidance for Q4-2023 and 2024 was also lowered, indicating potential issues.

- We tell you why you should have seen this coming a mile away and why other plays still make more sense, despite the drop.

With the era of mergers and acquisitions firmly upon the energy space, it is tough to find smaller plays that one can get behind. Birchcliff Energy Ltd. ( BIR:CA ) appeared to be one such residual company, and investors had a clearly defined story alongside a nice dividend.

Birchcliff January Presentation

They key things to like here were the high yield and a rather large set of 2P reserves.

Birchcliff January Presentation

{kind=link}

36 years is fairly uncommon outside of the oil sands, and the modest market capitalization meant that you had the potential for decent upside. You also got paid to wait, a fairly decent chunk, as the dividend in 2023 was 80 cents a year and that worked out to a nice double-digit yield. That dream was shattered yesterday as the company cut its dividend by 50%. We look at what went wrong and why the cut was not the only thing you should focus on.

What Happened To The Growth?

The first thing that investors paid attention to after they recovered from the dividend cut news, was the production guidance . Q4 2023 was estimated to be in the range of 76,000-77,000 barrels of oil equivalents, also known as BOE, a day. This is a big, big miss versus where consensus stood (and management had allowed to stand). At 81,000 BOE. Growth stories have hiccups and this one could be chalked to just that, but then Birchcliff also cut its 2024 numbers.

Birchcliff January Presentation

{kind=link}

We are now looking at numbers that are below even the low Q4 2023 numbers, with an identical budget. There are a couple of ways to look at the guidance cut. The first being that it is time to dump the stock and look elsewhere for growth. That can certainly be a valid interpretation in case of a growth story gone bad.

But from our view, a lot of the Canadian gassy plays were just unattached to the reality that the pricing was not there for unlimited growth. Only one company really has the potential to grow rapidly in natural gas and that is Tourmaline Oil Corp ( TOU:CA ) with its really low cost structure. The rest, by growing production, were simply adding to the problem of chronic oversupply and chronically low prices. Birchcliff's withdrawal from this appears sound to us. Of course, the bigger question is whether this was dictated by gas price or geology.

Birchcliff Energy's Dividend Cut

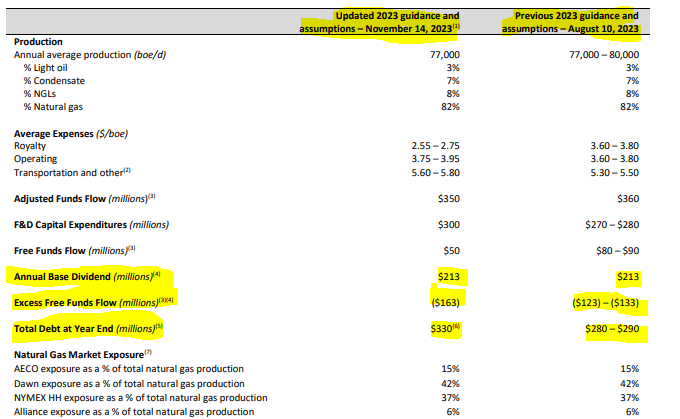

If you missed the possibility, nay, the strong probability of a dividend cut, you really have to only blame yourself. This was the outlook in November 2023 from the company at the time of the Q3 2023 results . Just look at how horrific their free cash flow ("FCF") was projected to be. Even earlier in August 2023, the company was expecting to incur $128 million (midpoint) of debt just to pay their income guys.

Birchcliff Q3-2023 Financial Report

{kind=link}

By November, this had ballooned to $163 million. The company was in essence doubling its debt from 2022 year end to 2023 year end, just to pay the dividend. In addition, even that amount was not guaranteed. The company had waltzed into the situation with zero hedges.

The Corporation's average realized sales price in Q3 2023 was $25.96/boe, a 45% decrease from Q3 2022. The decrease was primarily due to lower benchmark oil and natural gas prices, which negatively impacted the sales prices Birchcliff received for its production in Q3 2023. Birchcliff is fully exposed to increases and decreases in commodity prices as it has no fixed price commodity hedges in place.

Source: Birchcliff Q3 2023 Financial Report .

Compare that with Peyto ([[PEYUF]], PEY:CA ), another high dividend payer. While that one has also had issues in the past with sustaining the dividend, it seems to know that a strong price is worth locking in.

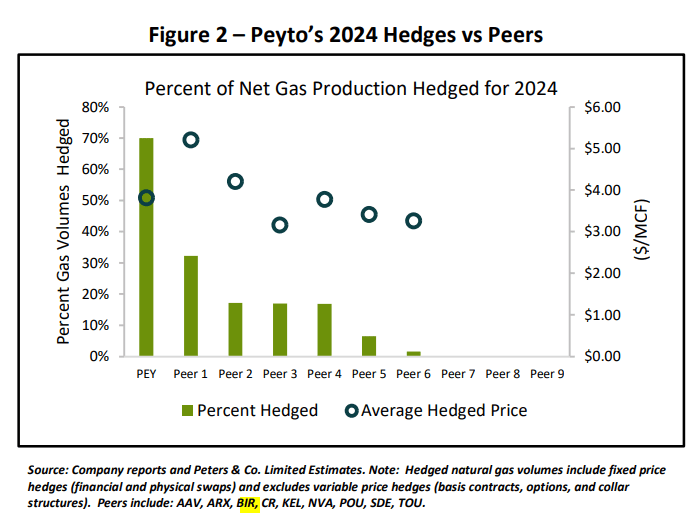

While gas producers hope a major blast of winter brings higher prices, 'hope' is not a strategy. To the contrary, Peyto's prudent risk management that includes a mechanistic hedging program and market diversification is a strategy that has us well-protected through 2024 and even 2025. We have hedged (or fixed) pricing for approximately 70% of our forecasted gas volumes for 2024 at a price just under $4/mcf (see Figure 1) which is far better than the current strip. And we have also hedged about a third of our 2024 forecasted condensate and pentanes volumes. The current fixed revenue for 2024 is enough to pay for our contemplated 2024 capital program and our dividend. Couple that with our industry leading cash costs, means Peyto has insulated itself from very low prices, if that is what is in store for 2024.

Source: Peyto January 2024 Commentary .

Interestingly enough, even Peyto showed everyone that Birchcliff probably would cut the dividend with the current strip by bringing attention to their zero hedges.

{kind=link}

Of course, these peers were not lined up alphabetically, but it should have caused you to investigate. In case you still missed it, Birchcliff let you know after the cut as well.

Birchcliff January Presentation

{kind=link}

Outlook

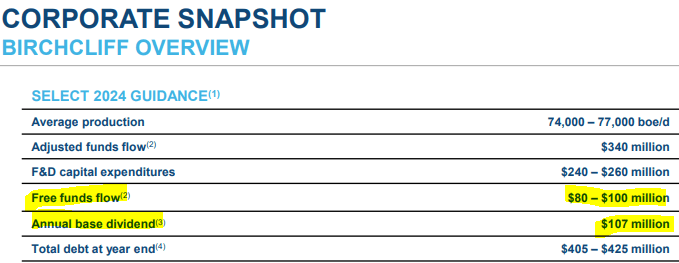

No growth is fine with us when conditions dictate one to exercise caution. The company won't lose brownie points on that account from us. There are still two major issues here that investors should think about before jumping into the 7.7% dividend yield. The first being that even the current dividend is not funded out of free cash flow. It is right there on the first slide.

Birchcliff January Presentation

{kind=link}

Using midpoints of the numbers, Birchcliff's debt expands, once again. Even that forecast is based on Henry Hub and Dawn holding up at these levels.

Birchcliff January Presentation

{kind=link}

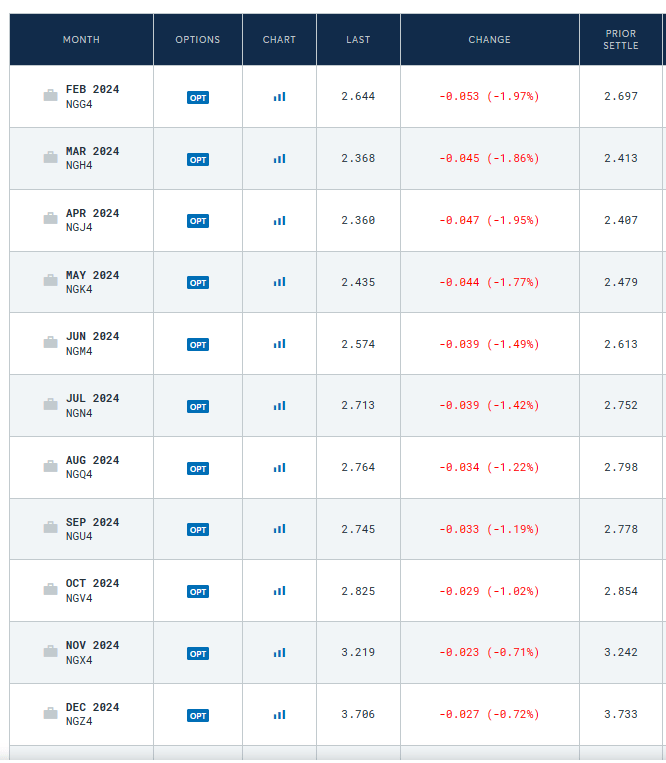

Actually, the current strip is already below $3.00 on Henry Hub, so you will need to increase to get where Birchcliff is estimating.

{kind=link}

So they are in a bit of a pickle here if they don't want to have to cut again. The relatively good part is that the projected increase in net debt this year is modest. So they could soldier through it, if 2025 holds some better luck for prices.

The second issue we have is that Birchcliff is relatively expensive here if you are aiming to get natural gas exposure. The company trades more expensive to Peyto, and both have a similar level of natural gas production as a percentage of the total (86% for Peyto, 82% for Birchcliff).

Tough sell, right? It gets even worse on a relative valuation basis. Whitecap Resources Inc. ([[SPGYF]], WCP:CA ) and Vermilion Energy Inc. ([[VET]], VET:CA ) are trading unbelievably cheap on a relative basis.

Yes, the two are about 40% and 50% natural gas weighted, respectively. But that is an advantage here when the gas side is collapsing. Instead of giving the oil weighting a premium, the market is pricing it poorly.

Verdict

The Birchcliff Energy's valuation is just too rich here to merit a buy. If you want a pure gas play, then Peyto makes more sense. If you want gas exposure, then there are several gas weighted medium-sized companies that are cheaper today, even after Birchcliff's drop. Whitecap would be an alternative here for quality inventory depth and good management.

The one reason that we could have a bullish slant on Birchcliff is for the value of the reserves. The company holds more gas per dollar of enterprise value than anyone else. So, this might put some sort of a floor here. It might also get someone to buy them with a modest premium. Hence, we would not get too bearish here. But outside of a sale, this has some downside to catch up with almost all of its peers on cash-flow based valuation metrics.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Birchcliff Energy: Dividend Yield Falls, Peyto And Whitecap Make More Sense