MAIN - BlackRock TCP Capital: Potential To Be A Major Player In The BDC Space Post-Merger?

2024-01-08 07:00:00 ET

Summary

- BlackRock TCP Capital announced a merger with BlackRock Capital Investment that is expected to create long-term value for shareholders.

- The merger could lead to cost synergies and enhanced scale, giving TCPC better access to capital and driving long-term growth.

- TCPC has posted strong earnings and has a decent balance sheet but faces risks such as rises in PIK income and non-accruals.

- The BDC currently trades at a discount to its NAV and could reward shareholders in the foreseeable future if the merger is successful.

- Additionally, TCPC has seen its NAV price decline despite out-earning its dividend, a likely reason for the discount.

Introduction

As a dividend investor, Business Development Companies are some of my favorite stocks to invest in. And with the banking crisis that happened in early 2023, I think the sector ( BIZD ) will only become more attractive over time. I have my favorites that I hold but I'm always looking out for others in the space that I think have long-term potential as well. One of those that comes to mind is BlackRock TCP Capital ( TCPC ). The BDC recently announced a merger and that peaked my interest, prompting me to do an analysis on the company. In this article, I discuss whether TCPC has the potential to be a major player in the space post-merger.

Overview

BlackRock TCP Capital is a BDC that invests in the debt of private, middle-market companies with enterprise values typically between $100 million and $1.5 billion. Like many others in the sector, they typically invest in first-lien loans.

They are externally-managed and in August 2018, merged with and into a wholly-owned subsidiary of BlackRock ( BLK ). As an investor in the space, I typically prefer internally-managed BDCs like Capital Southwest ( CSWC ).

Being internally-managed gives these companies some advantages as their values usually align more with shareholders. Furthermore, they sometimes pay out more in special & supplemental dividends. One reason is there are less fees associated with being internally-managed, and this extra income can be distributed to shareholders in the form of dividends.

Recent Merger

Back in September, TCPC announced they entered into an agreement with BlackRock Capital Investment ( BKCC ) for them to merge into a wholly-owned indirect subsidiary of TCPC. In connection with this, their advisor BLK agreed to reduce its base management fee rate. They also agreed to waive their fee if TCPC's adjusted NII per share falls below $0.32 in any of the first four fiscal year quarters. This is expected to close in the first quarter of this year.

The merger is expected to create long-term value for shareholders as the combined company is expected to benefit from cost synergies and enhanced scale. With the merger, I think the BDC does have a lot of potential but the question remains, will it come to fruition? Will they successfully grow and the share price reflect it?

One potential advantage is it should give them better access to capital, including the potential to access debt financing on more favorable terms. TCPC is expected to have total assets of approximately $2.4 billion and net assets of approximately $1.1 billion.

This drives long-term growth and is something you want to see from a company. Especially when they are smaller in size & scale and looking for sustainable growth. The transaction is also expected to be accretive to net investment income through reduced fees, lower combined operating expenses, and opportunity for portfolio growth, which I think will benefit the BDC in the foreseeable future.

Why The Merger Could Boost Investor Confidence

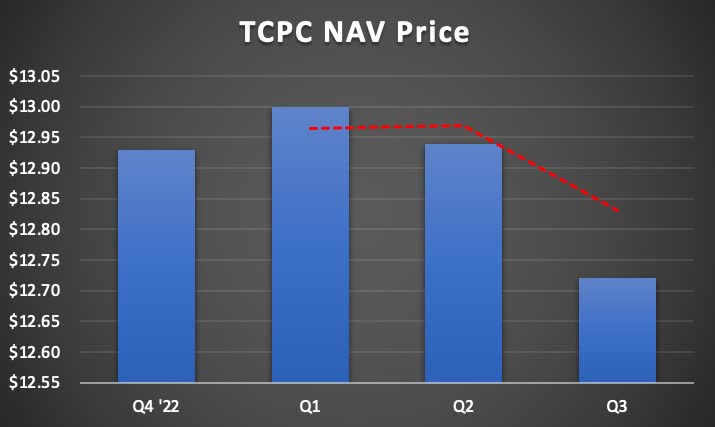

The management fee is expected to be reduced from 1.5% to 1.25% for assets equal to or below 200% of net (asset) value. Speaking of NAV, despite strong earnings this fiscal year and out-earning the dividend in all 3 quarters, TCPC's NAV has continued to decline quarter-over-quarter. This is likely one reason the stock currently trades at a discount to its NAV price of $12.72. In the chart below you can see since the start of rate hikes in March of 2022, the BDC is down nearly 12%.

Several others in the sector have outperformed over the same period, with Main Street Capital ( MAIN ) up nearly double-digits in price return. Ares Capital ( ARCC ) is the only one in the red but barely at just -0.17%. This time frame is from the day before the first rate hike in March of 2022 until the time of writing, January 4th.

{kind=link}

In my opinion, the discount is because of the NAV decline quarter-over-quarter and year-over-year. Currently, they trade at a near 7% discount to NAV. In the chart below, you can see TCPC's NAV declined more than 2% from Q1 and 1.65% from Q4 2022. If you're a believer in the merger and growth outlook, then the stock may be a buy now.

{kind=link}

This was due to the unrealized markdown in six positions, reflecting general market volatility and isolated performance challenges. But after the merger closes during the first quarter 2024, if the company can manage to grow its NAV steadily in the coming quarters while out-earning its dividend comfortably, I think the share price will likely follow.

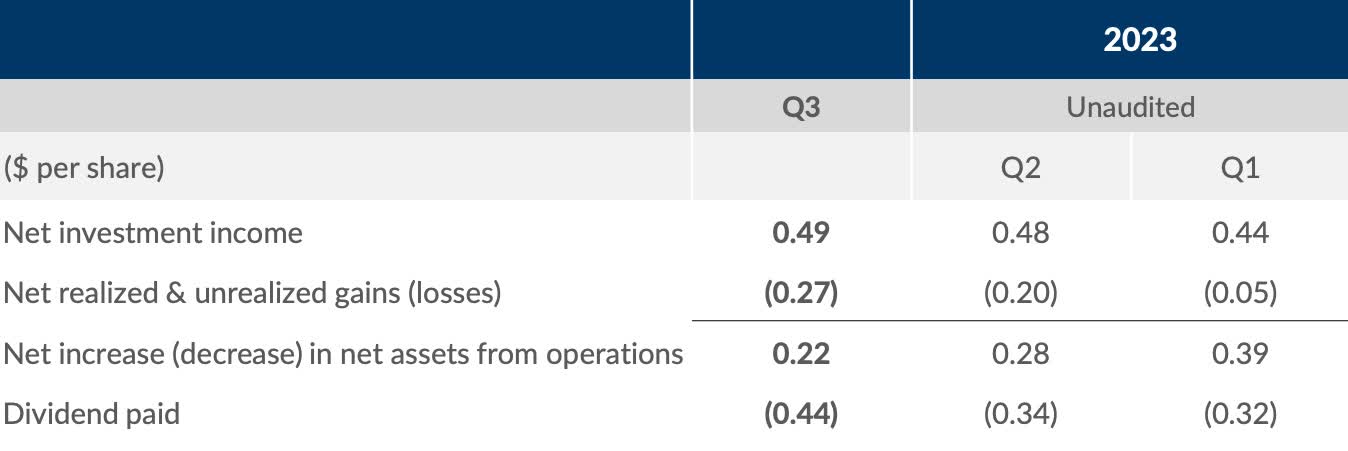

Strong Earnings Support The Dividend

As I previously mentioned, BlackRock TC Capital has posted some strong earnings this fiscal year. Both net investment and total investment income grew quarter-over-quarter. NII grew from $25.373 million to $28.320 million while TII grew from $50.3 million to $54.2 million over the same period.

{kind=link}

The BDC paid out a total of $0.59 at the end of last month when you included the $0.25 special dividend they declared. Although the company comfortably out-earned its dividend during the fiscal year, it would have been nice to see them roll this extra income over into the next year in preparation for rate cuts.

I'm sure shareholders in the company will disagree with me but with 95% of their debt investments floating rate, it's best to be proactive and not reactive. Furthermore, the company could have used the extra income to make future investments and grow its portfolio. Since the start of the FY, TCPC has not added any additional portfolio companies with 143 total , the same amount they started with in Q1.

To be fair, it has been a challenging environment for a lot of companies, and you want to see businesses making smart investments, not making acquisitions just for the sake of growing. This will be advantageous because of the increased size & scale of the company going forward, especially with better access to capital. Management addressed this in Q3 , stating they continued to pass on the substantially less attractive number of opportunities coming to market.

Adequate Balance Sheet

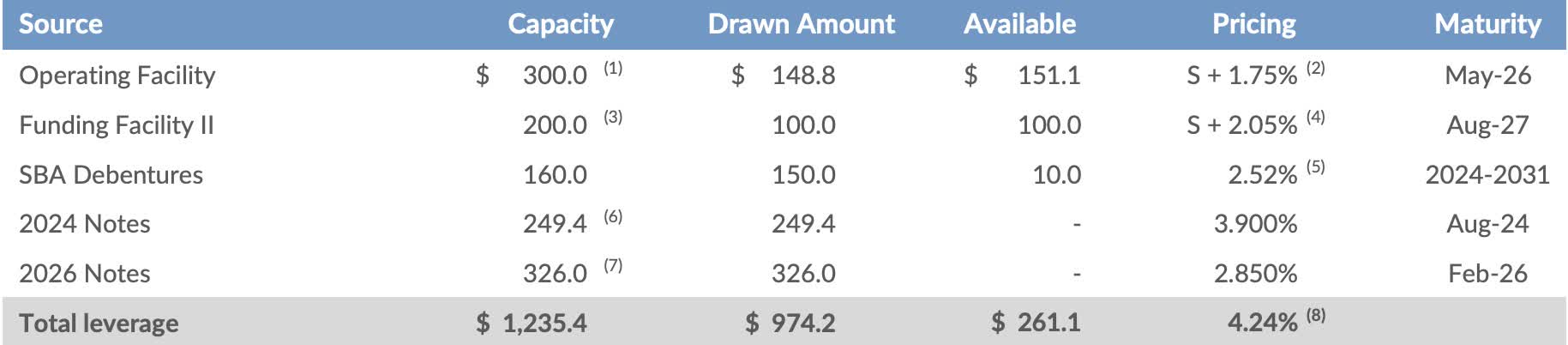

TCPC does have a decent balance sheet with a BBB- credit rating from Fitch and Moody's. The BDC has also been increasing its liquidity. In Q3, this grew to $353 million from $333 million in Q2. This includes leverage of $261 million and cash of $92 million.

Additionally, they have some notes due this coming August for roughly $250 million but no additional debt maturities due until 2026. They've also been focusing on deleveraging. This declined to 1.12x from 1.17x in Q2, well below management's target range of 2.1x. This is also in comparison to peer SLR Investment Corp.'s ( SLRC ) 1.21x. So, the company's balance sheet remains strong, and seeing how they've increased their cash, the BDC is well-prepared for challenging times ahead.

{kind=link}

Risk Factors

Two huge risks that have been plaguing BDCs are rises in PIK income and non-accruals. TCPC saw an uptick in both of these. Non-accruals rose to 1.1% of total investments at fair value, up from just 0.3% a year ago. Furthermore, PIK income of $3.5 million was more than 6% of total investment income, up from roughly 4% in Q3 of 2022.

And although rates are expected to decline this year, this is still something to keep an eye on in the coming quarters. Another risk the company faces is a steep fall in interest rates. With three cuts expected this year, TCPC could see NII fall quarter-over-quarter as 95% of their debt investments are floating rate.

If so, this would likely place pressure on dividend coverage, which could cause a further decline in NAV. This would also cause the share price to decline as well. As previously mentioned, it would have been nice to see the BDC carry over the extra income which they could have used if dividend coverage became tight because of suppressed earnings. For now, non-accruals are manageable but with TCPC being on the smaller side, they could see a potential rise in loan defaults from less credible portfolio companies.

Conclusion

BlackRock TCP Capital has performed well out-earning the dividend and growing their net investment and total investment income quarter-over-quarter. Despite that, their NAV price has declined over the same period, indicating why the stock may be trading at a near 7% discount to NAV. This has also caused the stock to underperform its peers in the sector, who've all mostly fared well during the high interest rate environment.

Furthermore, the company announced a merger with BKCC which is expected to close in Q1 2024. This is expected to create long-term value as the merger is expected to benefit from cost synergies and enhanced scale. If the BDC can successfully merge and continue growing earnings while growing its NAV over time, it may become a major player in the space in the foreseeable future. For now, I rate the stock a hold as I wait to see what the BDC does over the next few quarters.

For further details see:

BlackRock TCP Capital: Potential To Be A Major Player In The BDC Space Post-Merger?