ACR - Blackstone Mortgage Trust: Hardly Ever You Get Such An Attractive Combo

2023-03-07 13:55:49 ET

Summary

- With the Fed's terminal rate now at ~5.6% and "higher for longer" narrative, Blackstone Mortgage Trust, Inc.'s 100% floating-rate portfolio is poised to earn a lot more (all else equal).

- Only during the COVID peak panic did Blackstone Mortgage Trust offer a higher yield than the current ~12%, but today the dividend coverage is far better.

- We see an upside potential of 30%+ versus a downside risk of about 15%. This attractive >=2:1 ratio doesn't include dividends.

- Slowing economic growth, surely a recession, may lead to more prepayments and non-accruals, perhaps even to a couple of defaults; however, Blackstone Mortgage Trust, Inc.'s portfolio is set to weather such headwinds.

Personal Touch

Before we do some more in-depth analysis of Blackstone Mortgage Trust, Inc. ( BXMT ), let us say in a very direct way: we have traded this company's equity and debt for so many years that even if we don't look at the company's portfolio at all - we're still comfortable trading in and out of BXMT solely based on our long-term, intimate relationships with the company's securities.

With that in mind, we have two things to say:

1. Switching Debt for Equity

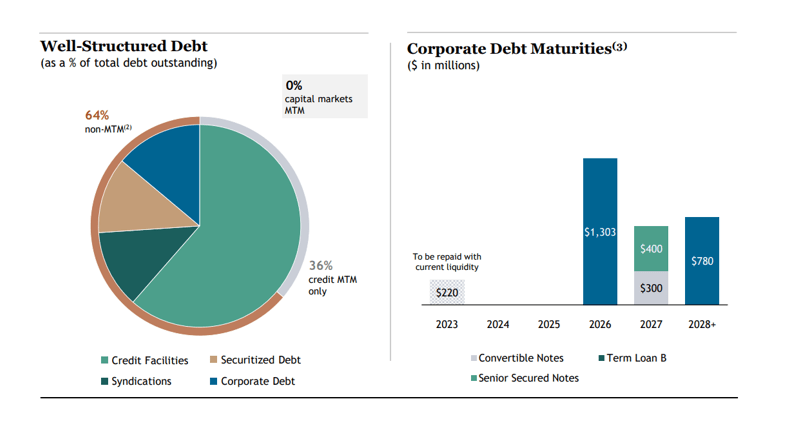

In exactly two weeks, the BXMT debt that we bought in April 2020 is maturing (that's part of the $220M which is due in 2023 per the below chart). So, in a way - we replace the debt exposure with an equity exposure.

[That's not to say that a BXMT debt purchase isn't going to happen on top... it's certainly on our agenda/radar, too.]

BXMT Q4/2022 Earnings Presentation

{kind=link}

2. Low 20s for BXMT? We take it!

Not only this is almost halving (ok, not from the 52-week high but) from the pre-COVID high, but history shows that buying BXMT in the 20s and selling in the 30s is a pretty reliable trade.

Y-Charts, Author

Over the past decade, buying when BXMT crossed above the 200-DMA and selling when it crossed below the 200-DMA was a profitable trading pattern. Therefore, it might be safer to wait for the stock price to cross above the 200-DMA again. Perhaps. However, we believe that at $20 (and a change), the opportunity is big enough for us not to wait a while longer to take advantage of it.

At this point, even if you don't read further, you understand that the above is enough for us (and perhaps for you to) to buy BXMT. Yet, we will walk the extra mile (just for you) and try to show you that not only long-term technicals but also (and perhaps mostly) fundamentals support this decision.

Btw, short-term technicals aren't too encouraging, with the stock potentially en route to test the lower end of the channel, around $17-$18. That's a downside risk that we should take in consideration. Nonetheless, we believe that the upside (expected distributions + potential appreciation) is far greater and worth taking the risk.

Y-Charts, Author

Q4 and FY 2022 Earnings Report ("ER")

Ok then. Let's take a closer look at BXMT now and why we believe it's a good buy right now.

The company published its ER on Feb. 8:

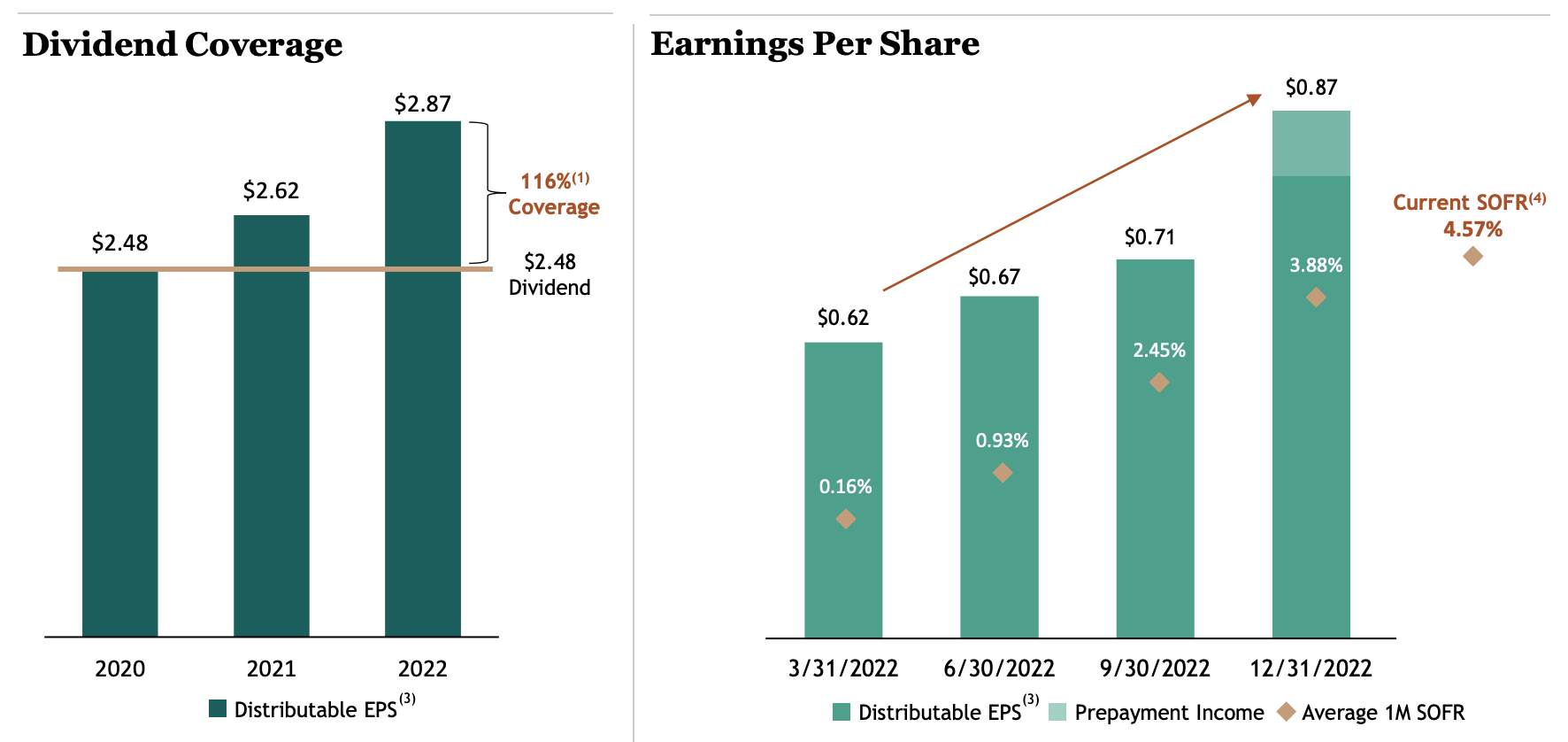

- Q4 Distributable EPS ("DE") of $0.87, exceeding the average analyst estimate of $0.72, climbed from $0.71 in the third quarter.

- It should be noted, however, that the higher than normal profitability in Q4 includes a (non-recurring) prepayment fee of about $0.07 per share. Excluding this fee, BXMT weighted DE of $0.80 per share is still up 13% from Q3 and 21% from the equivalent metric in Q4 of last year, reflecting the significant beneficial impact of rising rates on the portfolio.

- GAAP loss in Q4 of $0.28 per diluted share (down from a gain of $0.76 a year earlier) stemmed from a $189M buildup in the company's expected credit loss reserve ("CECL"), up from less than $10M in the year-ago quarter.

- FY 2022 distributable EPS of $2.87 provides a 116% to the $2.48 annual distribution.

BXMT Q4/2022 Earnings Presentation

{kind=link}

There are a few advantages for investing in BXMT; some are time-bound (mostly relevant for the current time) and some are longer-term in nature (reflecting the company's nature over the year).

1) Portfolio C onstruction

First and foremost, BXMT's 100% floating rate portfolio is obviously very suitable for the rate environment we're in right now.

Floating-rate loan portfolio continues to benefit from rising rates; a further 100 bps increase in base rates from the 4Q average would generate $0.05 per share of incremental earnings quarterly

We continue to see rising rates as a tailwind for our business, but 100-basis-point increase in rates from 4Q levels generating around $0.05 per share of incremental quarterly earnings all else equal.

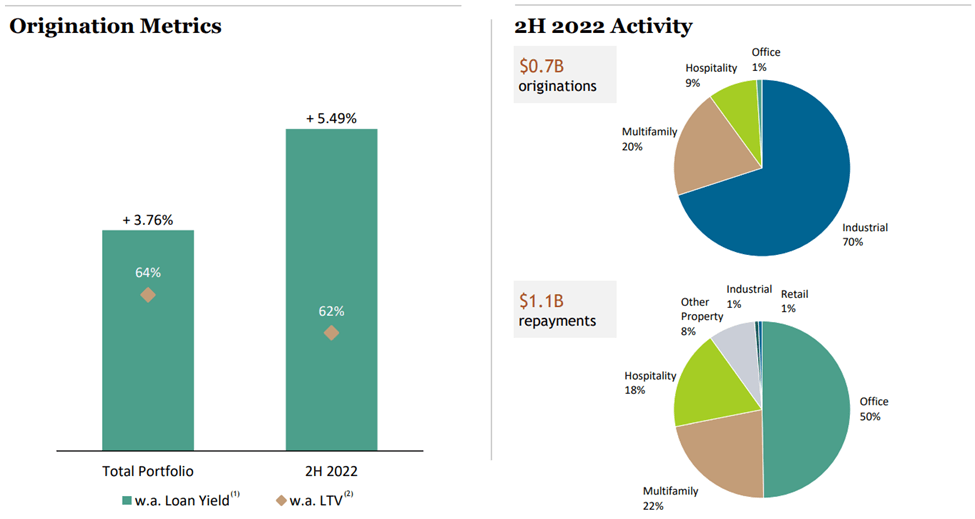

Loan originations were $700M for the back half of 2022, while repayments were $1.1B.

Portfolio value rose to $26.8B from $26.1B at the end of Q3.

97% of the loan portfolio is performing. BXMT collected $3.7B of repayments in 2022, nearly 50% of which were on office loans. Borrowers contributed $675M of incremental equity, continuing to invest in their assets.

BXMT continued to collect 100% of all interest due under all loans and the vast majority of loans (97%) remain fully performing and recognizing income as usual. Although loan repayments remained muted, BXMT did collect $648M of repayments in Q4, roughly in line with the company's $690M of loan fundings.

2) Stable Book Value ("BV")

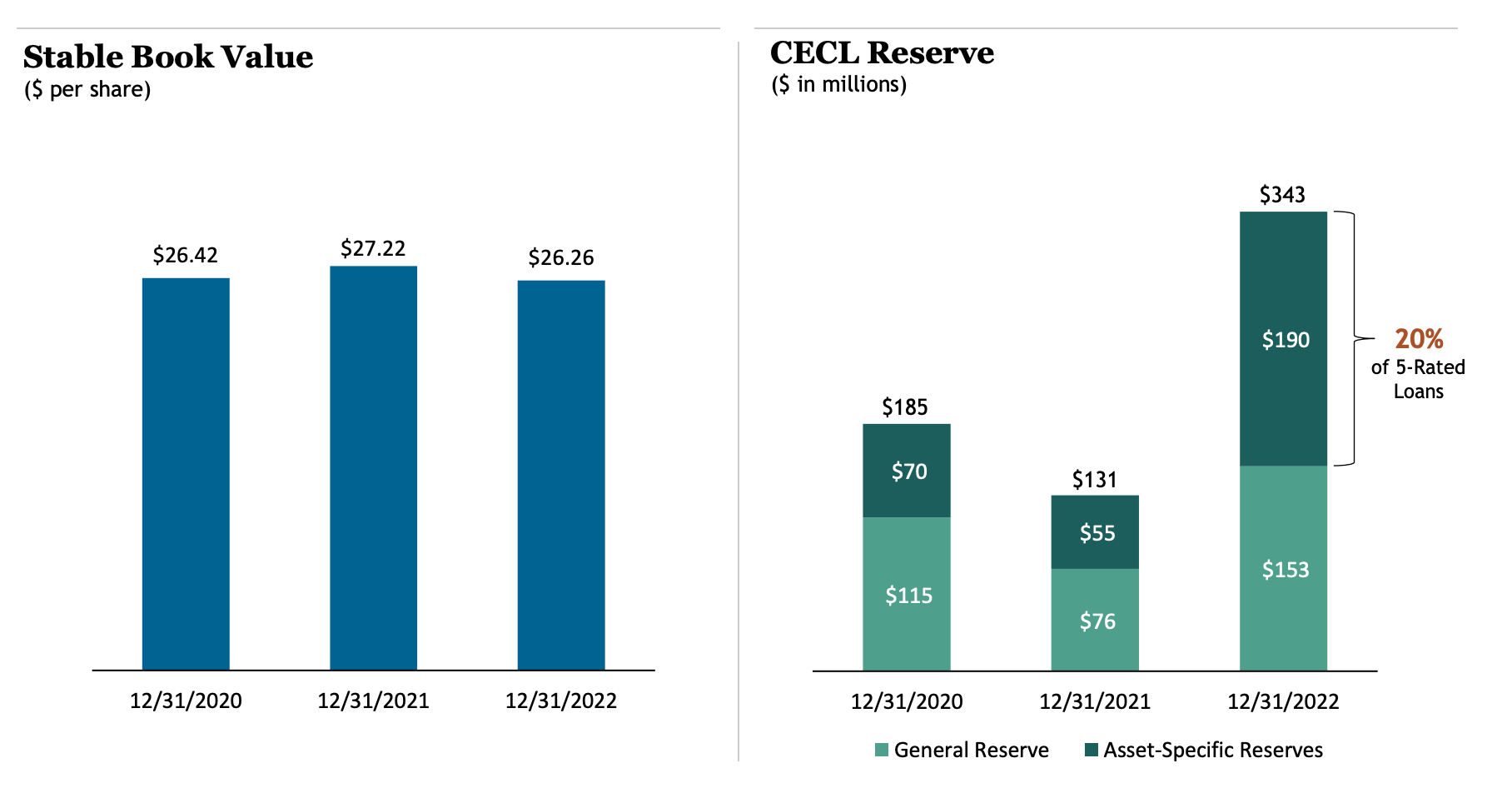

Book value per share was $26.26 at Dec. 31, 2022, versus $27.20 at Sept. 30, 2022. Not only such a 3.5% quarterly decline is very rare for BXMT, but it's still smaller/better than what many other mREITs have/will post/ed.

Now, let's not forget:

- The main reason for this decline was the significant increase in the CECL.

The snapshot of this quarter’s earnings comes down to two key numbers, $0.87 per share, our distributable earnings, an all-time record for BXMT and $0.94 per share, our net change to book value reflecting the impact of our CECL reserve increase given the more challenging credit environment.

- BV is down <1% from the past two years ago, despite this huge addition to the reserves; that is the prudence we like to see, even though it may not even be needed.

Book value per share of $26.26 as of December 31, 2022, which is net of a $1.99 cumulative CECL reserve, and is within 1% of our book value of $26.42 as of December 31, 2020, despite an increase of $171.6 million in our CECL reserve since that time.

BXMT Q4/2022 Earnings Presentation

{kind=link}

It's a kind of magic (and a beauty) to see an mREIT that has lost only 5.7% of its BV over the past 5 years.

How rare is this? Judge for yourself:

- Past 5 years.

[Comparing BXMT Ares Commercial Real Estate Corp ( ACRE ), Starwood Property Trust Inc ( STWD ), Ladder Capital Corp ( LADR ), Apollo Commercial Real Estate Finance Inc ( ARI ), Arbor Realty Trust Inc ( ABR ), Rithm Capital Corp ( RITM ), Granite Point Mortgage Trust Inc ( GPMT ), PennyMac Mortgage Investment Trust ( PMT ), ACRES Commercial Realty Corp ( ACR ), MFA Financial Inc ( MFA ), Chimera Investment Corp ( CIM )]

Y-Charts

- Past 10 years

[GPMT (doesn't exist so long) replaced by AG Mortgage Investment Trust Inc ( MITT ).]

Y-Charts

And the above charts are also doing a favor to names like Ellington Residential Mortgage REIT ( EARN ) or Western Asset Mortgage Capital Corp ( WMC ) that have lost most of their BV over the past decade.

3) Dividend Yield and Coverage

On one hand, BXMT hasn't increased its quarterly distribution for about eight years.

Y-Charts

On the other hand, with the exception of the COVID (temporary) peak, yield has never been as high and well covered as it is now.

With a dividend coverage of 116%, we expect the company to announce either a dividend increase (finally), or (at least) a special dividend.

4) Conservative Approach

Retention of $66 million of excess Distributable Earnings in 2022 supported book value stability despite 161% increase in CECL reserve due to a more challenging credit environment.

CECL reserve increased $1.10 per share in 4Q; specific CECL reserves cover 20% of aggregate 5-rated loan balance

BXMT Q4/2022 Earnings Presentation

{kind=link}

Keep in mind that tightening monetary policy (rising rates) has had two, conflicting, outcomes on (floating-rate focused) lenders:

On one hand, it requires higher allocation to credit (potential loan loss) reserves.

On the other hand, it's pushing profitability a lot higher and a lot quicker thanks to the magnitude (number of hikes) and pace (frequency of hikes).

The two are integrally related. The primary factor pressuring credit performance is also driving record income for our business and that is the precipitous rise in short-term interest rates, 425 basis points over the course of 2022, the status tightening cycle in 50 years.

5) Attractive Price to Book Value ("P/BV")

In-spite of BXMT's BV being only 5.7% off its (5-year) peak, the stock price is trading at nearly half its peak level.

BXMT's P/BV is now <0.8, a rarely low level; only early 2020 offered a lower ratio than that for a brief period.

6) Valuation

Based on the current size and composition of the portfolio, BXMT is capable of making well over $3/share a year, if no major credit losses are due.

Assuming that some loan losses will come BXMT way, let's assume that BXMT running, sustainable, EPS is somewhere in the $2.50-$3.00 area.

Y-Charts, Author

At the top end ($3/share) that is good for a multiple of ~7x (when the stock price is ~$21), which is a lot better than BXMT's norm.

Y-Charts

Over the past three years, when the stock traded a lot higher than the current market price, the TTM P/E ratio was a lot higher than today's forward multiple.

Y-Charts, Author

Sure, the macro landscape and economic environment are currently pressing the stock price down, however, the point we're making is that if we look beyond the short-term (say, next 12 months), BXMT deserves to trade a lot higher based on its current multiples.

At the very minimum, BXMT deserves to trade at no more than a discount of 5%-10% to BV; about $23.63-$24.95 using the end of 2022 BV.

Under a reasonable-case scenario, we would pick one of the following:

- EPS of $2.75 (=midpoint of the EPS sustainable range) and a multiple of 10x >>> This implies a stock price of $27.50

- Dividend yield of ~8.9% = ~3% lower spread (compared to B-rated spreads) >>> This implies a stock price of ~$27.87.

Y-Charts, Author

Indeed, from the current level of $21 we see an upside of 30%+.

How to Play This?

With BXMT trading sub-$21, we believe that the stock is a straight BUY here.

Nonetheless, if you wish to play this even more safely - selling PUTs provides even more protections, i.e., limiting the downside.

Implied annual volatility on BXMT options today is approaching 40% which is, as you can see below, quite an elevated level.

Y-Charts, Author

This means that this is a good time to be a seller of options.

How do we suggest playing this?

- SELL (to open) BXMT 07/21/2023 20.00 PUT @ $1.40

- SELL (to open) BXMT 07/21/2023 21.00 PUT @ $2.00

- SELL (to open) BXMT 01/19/2024 20.00 PUT @ $2.40.

The risk is that we're using too-low strikes and the options won't get assigned to us. In other words, if BXMT won't remain under $21 (and we don't expect it to), we won't become shareholders through selling these PUTs. In such a case, BXMT can run higher without us, and we will be left out only with the premiums we collect by selling the PUTs.

What we are creating is a ladder of multiple purchases that will build a (bigger) BXMT position. with an average net price that is near the upper end of the downside ($17-$18) area.

| PUT option sold |

| Premium |

| Net Price* |

| BXMT 07/21/2023 20.00 |

| $1.40 |

| $18.60 |

| BXMT 07/21/2023 21.00 |

| $2.00 |

| $19.00 |

| BXMT 01/19/2024 20.00 |

| $2.40 |

| $17.60 |

| *If the option gets assigned to us |

| Average price: |

| $18.40 |

And if BXMT falls further - rest assured we will be selling more PUTs.

For further details see:

Blackstone Mortgage Trust: Hardly Ever You Get Such An Attractive Combo