BLND - Blend Labs Focuses On Consumer Banking As Mortgage Industry Woes Continue (Rating Downgrade)

2023-11-30 07:26:27 ET

Summary

- Blend Labs has reported Q3 2023 financial results, beating revenue and matching earnings estimates.

- The company provides software to financial institutions for modernizing customer interfaces and mortgage application processing.

- My near-term outlook is bearish due to the company's declining revenue and heavy losses, although management has made some progress in reducing the company's cost structure.

A Quick Take On Blend Labs

Blend Labs (BLND) reported its Q3 2023 financial results on November 7, 2023, beating revenue and matching consensus earnings estimates.

The firm provides software to financial institutions seeking to modernize their customer interfaces and mortgage application processing.

I previously wrote about BLND with a Hold outlook on declining revenue and high operating losses.

With cutbacks throughout the company amid continued heavy losses, it will be difficult for the team to generate any meaningful total revenue growth in the near term.

So, my outlook on BLND is Bearish [Sell] for the near term.

Blend Labs Overview And Market

California-based Blend has developed a suite of lending, credit card and deposit account interfaces that enable legacy banks to present a modernized look to their service offerings.

The company's revenue model is not a standard SaaS revenue model; rather, it charges for completed transactions and doesn't charge for abandoned or rejected applications.

BLND is led by co-founder and Head of Blend, Nima Ghamsari, who was previously employed at Palantir Technologies.

The firm's primary offerings include white-label interfaces for:

-

Mortgages

-

Home equity loans

-

Home equity lines of credit

-

Vehicle loans

-

Personal loans

-

Credit cards

-

Deposit accounts

Blend also provides title insurance procedures and other related closing and settlement services.

Blend seeks customer relationships with financial institutions via a direct sales and marketing process targeting customers from the largest banks to smaller community lenders.

According to a 2023 market research report by Mordor Intelligence, the global financial services application market was an estimated $130 billion in 2023 and is forecast to reach $240 billion by 2028.

This represents a forecast CAGR of 13.13% from 2020 to 2025. The primary reason for this expected growth is the need by financial institutions to modernize their infrastructure stack to remain competitive for younger demographic users. Also, the industry needs improved business intelligence solutions as competitive pressures increase from newer fintech firms.

Major competitive or other industry participants include:

-

MeridianLink

-

Tavant Technologies

-

LenderLogix

-

RealKey

-

Neofin

-

Roostify

-

Kiavi

-

Truework

-

SimpleNexus

-

Major consulting firms

-

Systems integrators

-

Institutional financial software companies

Blend Labs' Recent Financial Trends

Total revenue by quarter (blue columns) has continued to fall; operating income by quarter (red line) has remained heavily negative, but losses have been reduced somewhat in recent quarters:

Seeking Alpha

Gross profit margin by quarter (green line) has improved recently; selling and G&A expenses as a percentage of total revenue by quarter (amber line) have remained high but have dropped in recent quarters:

Seeking Alpha

Earnings per share (Diluted) have remained substantially negative:

Seeking Alpha

(All data in the above charts is GAAP.)

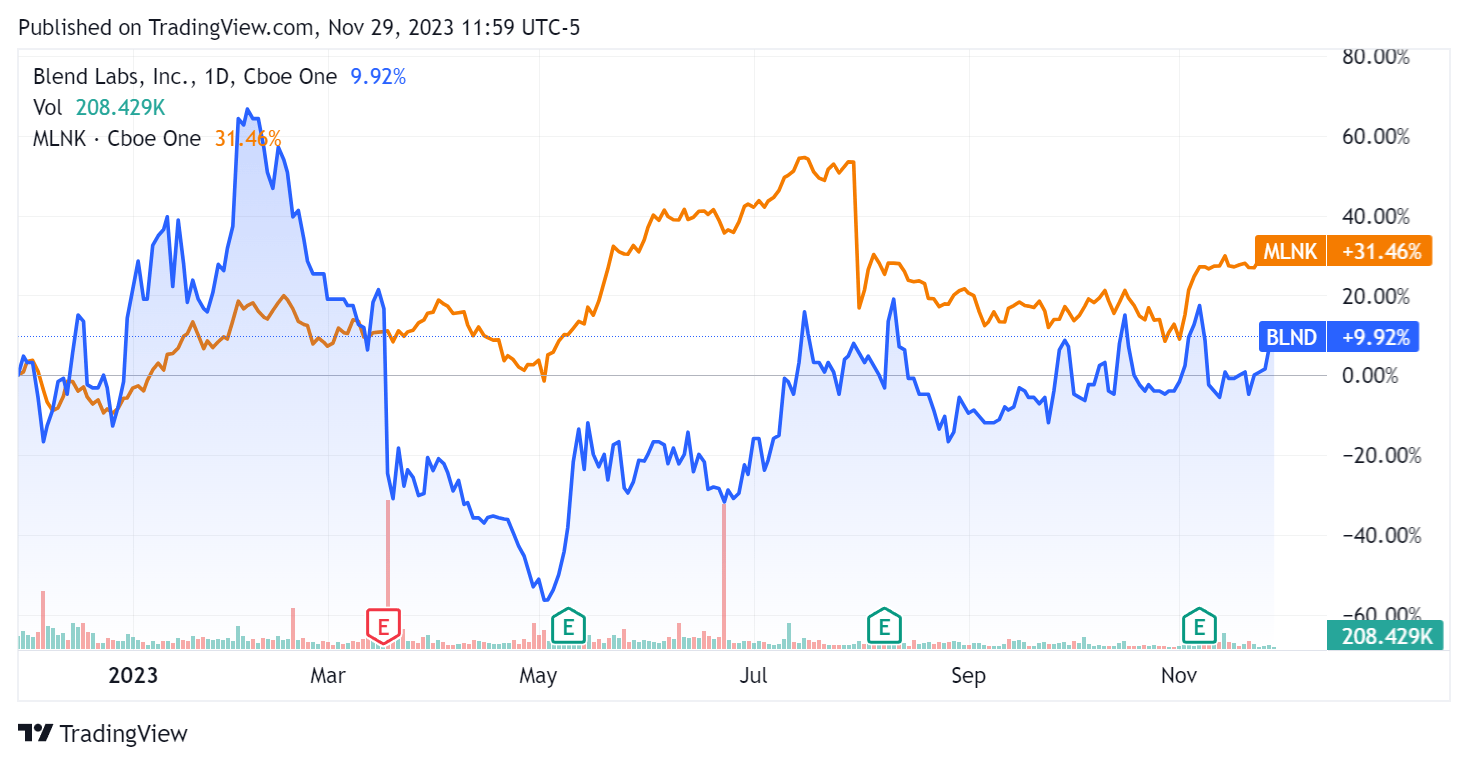

In the past 12 months, BLND's stock price has risen by 9.92% vs. that of MeridianLink's ( MLNK ) gain of 31.46%:

{kind=link}

For balance sheet results, the firm ended the quarter with $245.0 million in cash, equivalents and short-term investments and $219.0 million in total debt, all of which was long-term.

Over the trailing twelve months, free cash used was a whopping $155.1 million, during which capital expenditures were only $1.0 million. The company paid $68.0 million in stock-based compensation in the last four quarters.

Valuation And Other Metrics For Blend Labs

Below is a table of relevant capitalization and valuation figures for the company:

| Measure (Trailing Twelve Months) |

| Amount |

| Enterprise Value / Sales |

| 2.1 |

| Enterprise Value / EBITDA |

| NM |

| Price / Sales |

| 1.9 |

| Revenue Growth Rate |

| -40.2% |

| Net Income Margin |

| -140.0% |

| EBITDA % |

| -110.2% |

| Market Capitalization |

| $317,690,000 |

| Enterprise Value |

| $348,920,000 |

| Operating Cash Flow |

| -$154,260,000 |

| Earnings Per Share (Fully Diluted) |

| -$0.99 |

| Forward EPS Estimate |

| -$0.21 |

| Free Cash Flow Per Share |

| -$0.64 |

| SA Quant Score |

| Hold - 2.73 |

(Source - Seeking Alpha)

BLND's most recent unadjusted Rule of 40 calculation was negative (106.9%) as of Q3 2023's results, so the firm has performed poorly in this regard, although improving from an even worse result in Q1 2023, per the table below:

| Rule of 40 Performance (Unadjusted) |

| Q1 2023 |

| Q3 2023 |

| Revenue Growth % |

| -26.7% |

| -40.2% |

| Operating Margin |

| -126.0% |

| -66.7% |

| Total |

| -152.7% |

| -106.9% |

(Source - Seeking Alpha)

A publicly-held direct competitor to Blend would be MeridianLink. Below is a comparison of major metrics for the two companies:

| Metric (Trailing Twelve Months) |

| MeridianLink |

| Blend Labs |

| Variance |

| Enterprise Value / Sales |

| 5.1 |

| 2.1 |

| -58.2% |

| Enterprise Value / EBITDA |

| 33.4 |

| NM |

| --% |

| Revenue Growth Rate |

| 6.4% |

| -40.2% |

| --% |

| Net Income Margin |

| -6.2% |

| -140.0% |

| --% |

| Operating Cash Flow |

| $62,840,000 |

| -$154,260,000 |

| -345.5% |

(Source - Seeking Alpha)

Commentary On Blend Labs

In its last earnings call (Source - Seeking Alpha ), covering Q3 2023's results, management's prepared remarks highlighted the double-digit year-over-year growth for its Consumer Banking segment.

Its pipeline expanded from 40 to 60 opportunities sequentially across both its Consumer Banking and Mortgage segments. Management noted its gross margin growth despite a continuing decline in the mortgage origination market.

While the mortgage industry is navigating significant challenges due to high interest rates relative to high home prices, management is clearly focusing more of its new business efforts on the Consumer Banking segment.

The leadership said it is ahead of its cost savings targets it set last year.

In the earnings call, I tracked the frequency of various terms and keywords used by management and analysts:

Seeking Alpha

The frequency of negative terms such as 'uncertain', 'challenges[ing]', 'headwind', 'macro', and 'drop' is quite high and indicates the difficulties the firm and its mortgage segment client base are facing in the current mortgage environment.

Analysts asked leadership about its new product development and shifts in its revenue mix. Management explained that it is focused on developing deeper new product functions as a priority since it drives more revenue per customer. However, the company will likely expand into one new product area per year.

Leadership expects to see increasing diversification of its revenue mix over time across its product lineup.

Total revenue for Q3 2023 dropped by 26.7% year-over-year while gross profit margin rose by 16.3%, likely due to a mix shift.

Management did not disclose any customer or revenue retention rate metrics.

Selling and G&A expenses as a percentage of revenue fell 20.5% YoY, a positive trend, and operating losses were reduced by 59.0% but remained heavy at $27.1 million for the quarter.

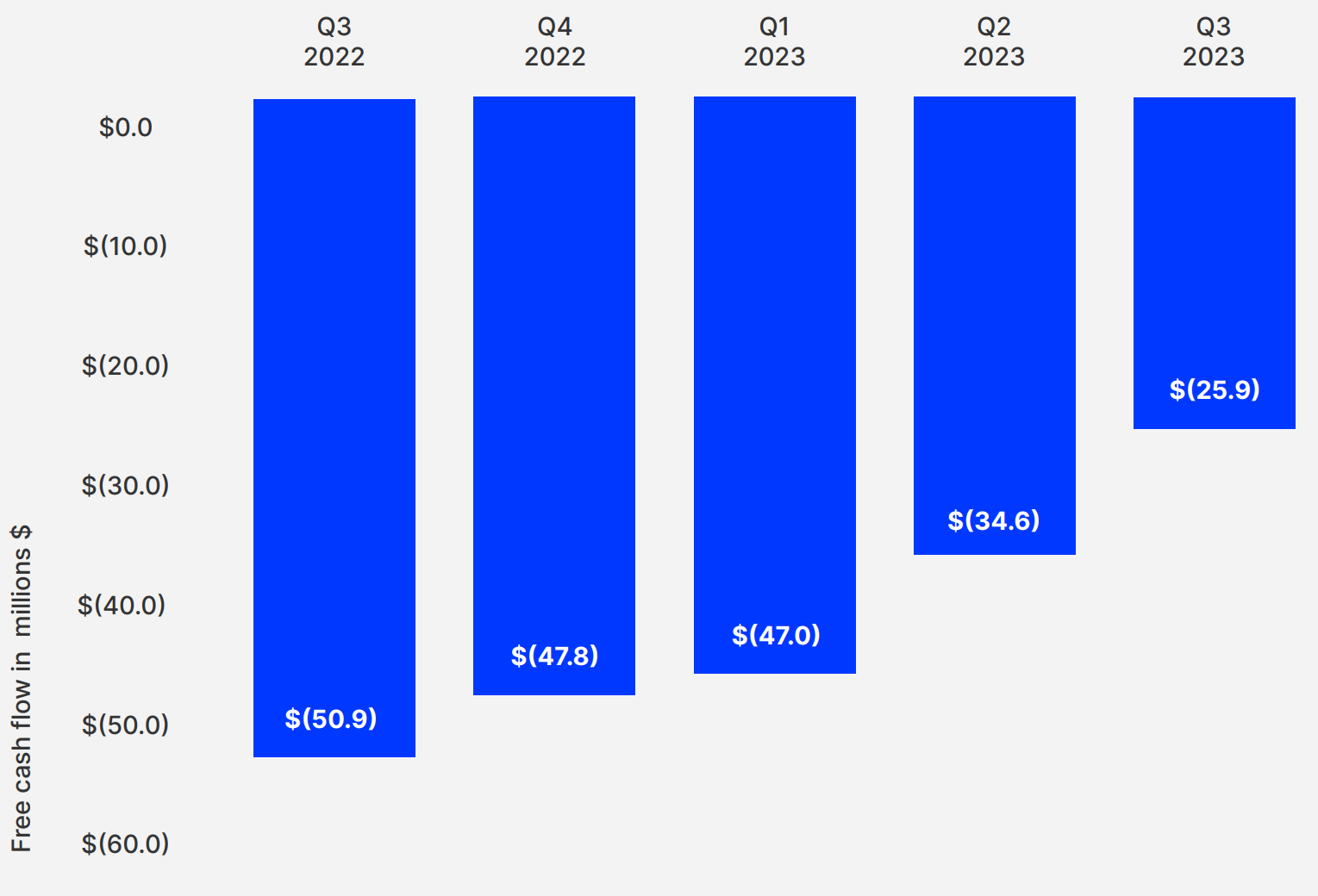

The company's financial position is uncertain since it has slightly more cash than debt but has used a high amount of free cash flow in the past twelve months, although its cash use has been trending lower each quarter, per the quarterly free cash flow chart below:

{kind=link}

BLND's Rule of 40 performance has been quite poor, although it has improved from Q1 2023's very poor result.

Looking ahead, total revenue consensus estimates for 2023 suggest a decline of 33% versus 2022.

In the past twelve months, the firm's EV/Sales valuation multiple has increased by a net of 226%, as the chart from Seeking Alpha shows below:

{kind=link}

While the company's focus on its Consumer Banking segment is understandable given the terrible shape the U.S. mortgage industry is in, most of its revenue base is from its mortgage segment.

So, management will need to really ramp up the growth in its Consumer Banking segment to stay even.

With cutbacks throughout the company amid continued heavy losses, it will be difficult for the team to generate any meaningful total revenue growth in the near term.

So, my outlook on BLND is Bearish [Sell] for the near term.

For further details see:

Blend Labs Focuses On Consumer Banking As Mortgage Industry Woes Continue (Rating Downgrade)