BLND - Blend Labs: Q2 2023 Could Be The Sign That Revenue Growth Is Turning Around

2023-09-13 04:13:15 ET

Summary

- Blend Labs has developed a streamlined platform for mortgage lenders and borrowers, offering simple and convenient digital services.

- Despite recent revenue declines, BLND showed improvement in 2Q23 and has potential for growth in FY24 and FY25.

- I think it is better to wait 1 or 2 more quarters to confirm that the current trend is sustainable.

Investment action

Based on my current outlook and analysis of Blend Labs ( BLND ), I recommend a hold rating despite the attractive upside. I think it is prudent to wait for 1 or 2 more quarters to confirm that the underlying trend we are seeing in 2Q23 sustains (i.e., revenue decline decelerates) and that profitability continues to inch upwards.

Basic Info

Mortgage lenders and borrowers alike can benefit from BLND's streamlined platform and streamlined application process for the home-buying process. To address the many systemic problems plaguing the massive mortgage lending sector, BLND has developed a platform that streamlines and automates the origination process, allowing banks to provide their customers with simple and convenient digital services.

Review

It has been a rough period for BLND over the past few quarters as it lapsed high revenue base and also the tough interest rates environment which dampened mortgage demand. Nonetheless, I believe it is appropriate to write about the situation at this time because the business appears to be turning around. To give context, starting in 3Q22, the business has been seeing significant declines in revenue (38% in 3Q22, 47% in 4Q22, and 48% in 1Q23). However, the acceleration in decline finally flipped to an improvement of 34% decline in 2Q23. While still negative, this is a positive trend that has surprised the market as 2Q23 revenue, gross profit, and EBIT all beat consensus expectations. BLND's 2Q23 revenue of $43 million was higher than the expected $40 million, the company's gross profit of $24 million was higher than the expected $18 million, and the company's adjusted EBIT loss of $18 million was significantly lower than the expected $26 million loss.

I anticipate a slowing in the rate of revenue decline and a strong year for BLND in FY24 due to favorable comparisons with FY23 and the possibility of interest rate easing (which would boost demand for mortgages). On a more micro level, I think there are a lot of new mortgage customers that BLND can win over and use to increase its market share. Since it only serves 47 of the top 100 mortgage originators as of now, BLND has a lot of room to expand. The second layer that could drive BLND growth is revenue per customer. The high Blend Income attachment rate BLND is experiencing, in my opinion, is proof that the company can successfully introduce new offerings and cross-sell to existing clientele. Because of this, I also think highly of the Blend Builder environment. Blend Builder's release at the beginning of the year allowed BLND to increase its use cases with existing customers and provide faster service to customers. In my opinion, this is a necessary first step for BLND to take in order to create additional solutions in the future to drive further increases in average revenue per user. To put it another way, this has opened the door for BLND to upsell more solutions in a more efficient way.

Yeah, absolutely. Well, I think again, we haven't shared the attach rate very specific to Blend Income, but what you're able to see is the follow-through of Blend Income and also what we do, for example, with clothes and some of our other solutions, the ability to actually allow those to attach to what we do in terms of renewals with our existing mortgage customers, it's those two outcomes together that are actually driving an increase in our funded loan rates and into the first part of your question. 2Q23 call

The massive losses being experienced by BLND must be mentioned in any article about the company. Investors should be very wary of BLND because the company has lost money for every dollar it has ever earned in the past. The good news is that BLND is getting close to breakeven, and I don't think the recovery of the mortgage industry will have any bearing on how quickly they reach EBITDA breakeven. Notably, BLND has announced a reorganization that will save the company $33 million per year. This amount is equivalent to avoiding a loss in EBITDA at the run rate of 25% in 2Q23. With solid cost management support and rising revenue per funded loan, BLND should be able to reach breakeven by FY25. Consensus is expecting a -$17 million EBITDA loss in FY24 on revenue of $181 million. If FY25 grows as I expected (refer below), the incremental revenue will be $54 million. Using the same gross margin expected in FY24 ($104 million / $181 million = 56%), it implies an incremental gross profit of $30 million, which will bring the EBITDA level from a loss of -$17 million to a $13 million profit.

Valuation

Author's work

I believe BLND can grow its revenue back to FY21 levels as revenue growth accelerates, boosted by a recovery in the mortgage environment, revenue per funded loan, and customer wins. Considering that BLND still has a very small revenue base as compared to the large mortgage industry, my expected growth pace is certainly possible. While I am optimistic about the growth prospect, I am certain that the valuation will continue to trade at a discount vs. peers like Alkami Technology (which provides digital banking solutions for smaller banks) and Upstart (a usage-based AI lending platform), as they are in a much better profitability position and are expected to grow way faster than BLND. Nonetheless, at a 1.6x forward revenue multiple, the stock can provide an attractive upside to investors. That said, I am recommending waiting one more quarter or two just to make sure that the trend we are seeing in 2Q23 continues.

Risk and final thoughts

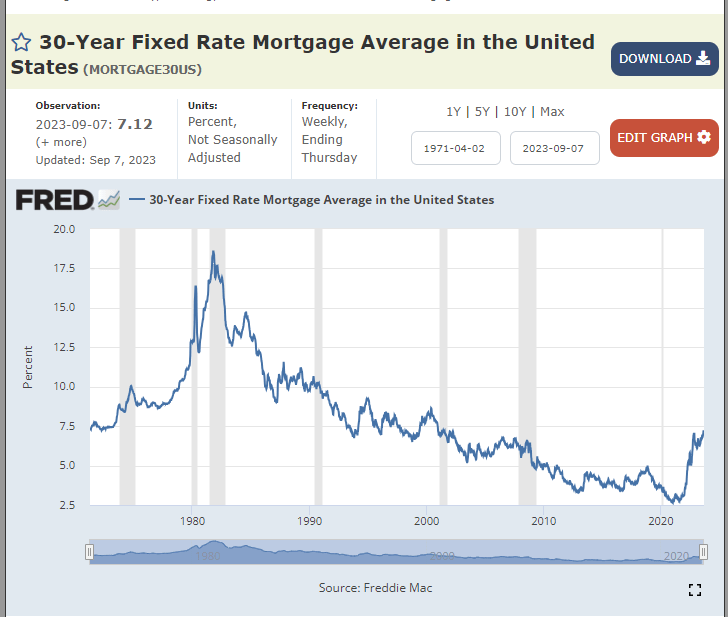

The major risk is that mortgage rates continue to go up. While I expect rates to come down, if we look at the history of US 30-year mortgage rates, we are nowhere near the peak, and there is certainly plenty of room left to increase. Naturally, this will significantly impact demand for the BLND solution.

{kind=link}

I recommend a hold rating for BLND despite the appealing potential for growth. The recent trends in 2Q23 have shown signs of improvement, with the revenue decline decelerating. However, it's prudent to wait for one or two more quarters to confirm if this trend continues and profitability continues to rise. The main risk lies in the potential for mortgage rates to rise further, impacting demand for BLND's solution. Monitoring this factor is essential for a well-informed investment decision.

For further details see:

Blend Labs: Q2 2023 Could Be The Sign That Revenue Growth Is Turning Around