APRN - Blue Apron: Recipe For Financial Turnaround Looks Good But Growth Still Missing

2023-08-10 18:05:53 ET

Summary

- Blue Apron has made progress in narrowing its losses and aims to achieve profitability by next year.

- Deal with "FreshRealm" to outsource meal kit fulfilment provides a path to profitability through stronger margins.

- The company's outlook has improved but poor sales trends remain a concern.

Blue Apron Holdings, Inc. ( APRN ) has been challenged amid a difficult consumer spending environment and intense competition within the meal-kit home delivery space. The company just reported it latest quarterly results with another decline in sales and recurring losses which have likely been frustrating to investors.

We last covered the stock with a critical article in 2022 citing the poor trends and an ongoing cash burn as representing " significant risks " to the outlook. Indeed, ARPN has significantly underperformed over the past year, failing to regain operational momentum.

That being said, we can now cite some encouraging developments including a strategy shift into an "asset-light" model. Blue Apron has made progress in narrowing its losses with management now guiding for a path to profitability by next year. While it may be a bit too early to buy APRN with conviction, we believe the outlook has at least improved while acknowledging ongoing uncertainties. The stock deserves to be on the radar of more traders.

APRN Earnings Recap

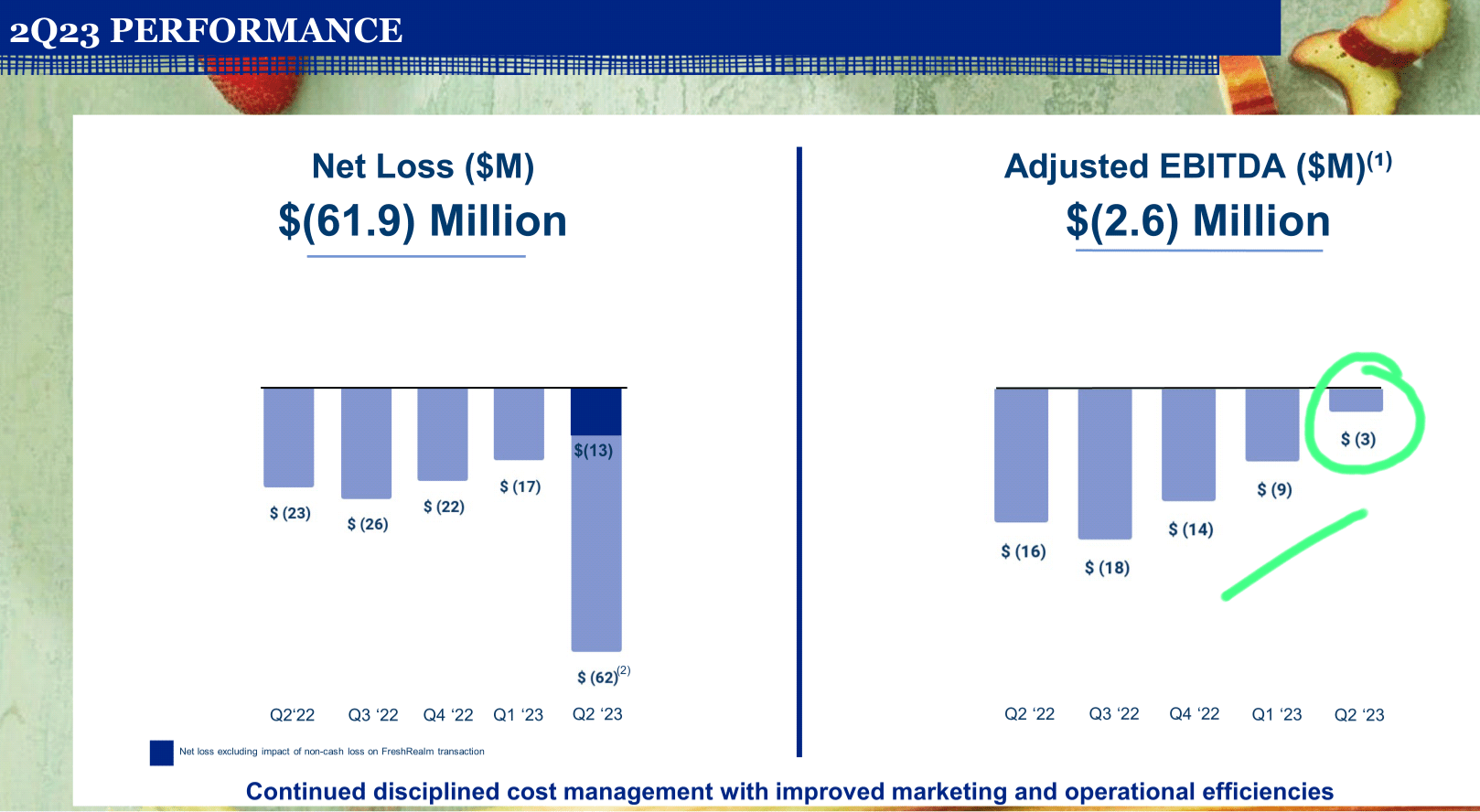

Blue Apron reported a Q2 EPS loss of -$9.52 , although this figure includes a large non-cash restructuring charge related to its deal with " FreshRealm", which we discuss below. Excluding this amount, the adjusted net loss of -$13 million compares to -$17 million in the prior quarter, and -$23 million in Q2 2022.

Even as net revenue of $106 million declined by -15% year over year, or -6% sequentially from Q1, the bigger story was significant cost cutting measures including on lower marketing spend to better balance the reality of the operation. The improvement at the margin is evident as the adjusted EBITDA loss of -$2.6 million has now narrowed for three consecutive quarters.

{kind=link}

source: company IR

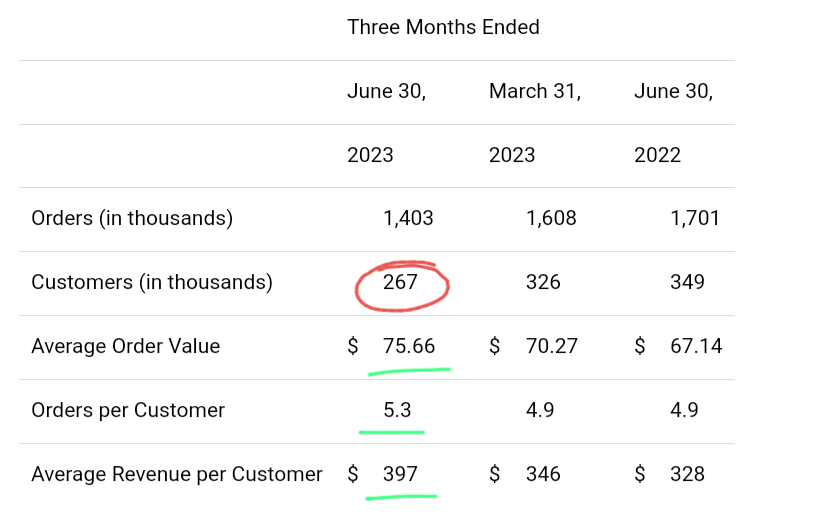

Management focused on performance metrics highlighted by a climb in average revenue per customer, and higher orders per customer during the quarter. Our interpretation here is that while the total number of customers on the platform are down, loyal subscribers are sticking with the service which is a good reflection of engagement and member satisfaction.

Still, while these metrics are edging higher in the right direction, they aren't quite enough alone to move the needle on the bottom line in terms of earnings. We say this because the next step for Blue Apron will be to expand the pie of customers in an attempt to regain growth. 267k customers down from 349k in the period last year is more concerning.

{kind=link}

source: company IR

As mentioned, a key development in the quarter was the announcement of a deal with FreshRealm national provider of fresh cooked meals to major retailers. Blue Apron has sold its logistical operation to FreshRealm which will now be responsible for all meal kit fulfilment.

In consideration of up to $50 million including an immediate $25 million cash payment, the idea here is for Blue Apron to transform into an asset light model, avoiding capital intensive infrastructure to instead focus on direct to consumer brand marketing. In other words, the strategy now is to center efforts on what Blue Apron believes to be its core strengths while outsourcing the major cost driver.

With that restructuring, the other benefit is a significantly streamlined operation allowing it to reduce its corporate headcount by 20%, expected to lead to a $7 million in annualized savings. Through the deal proceeds, Blue Apron ended this quarter with a balance sheet cash position of $30 million and zero long term financial debt. This aspect provide some flexibility and buys the company time until liquidity becomes a concern again.

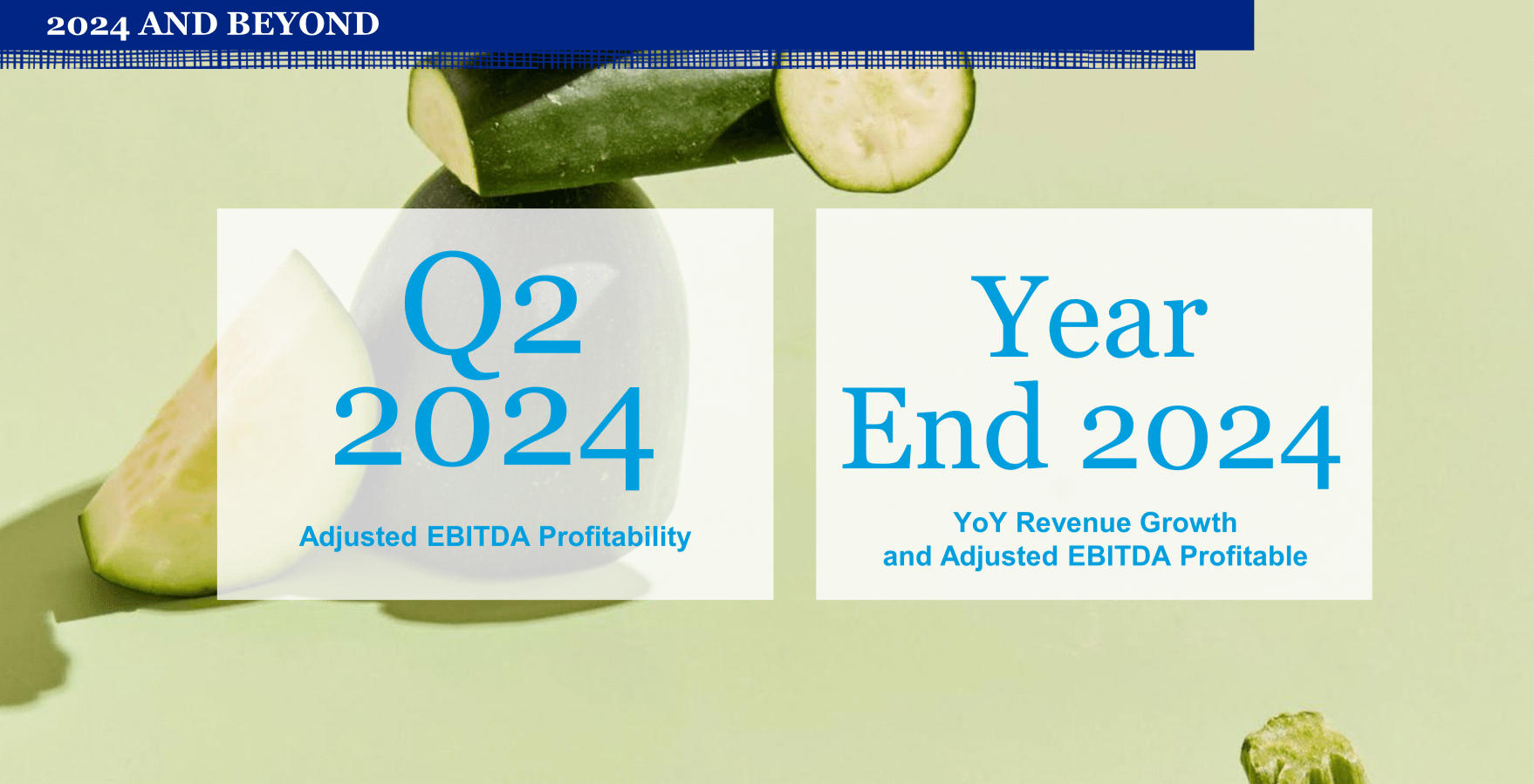

According to management, the setup here is for the company to reach adjusted EBITDA profitability by this time next year with a return to annual year over year revenue growth for the full year 2024. Again, this is a good target but it's also not the first time Blue Apron has set out a lofty ambition.

{kind=link}

source: company IR

What's Next For APRN Stock?

The story with Blue Apron is about financial engineering and squeezing out operating efficiencies. That's a good first step but what will be more important is a return of top line growth and finding success in expanding the customer base. On this point, Blue Apron has a lot of work to do in terms of standing out from other meal kit options in what has evolved into a crowded space. By this measure, the next few quarters will be crucial to confirm this new strategy is paying off.

The upside here is that the stock could be rewarded by the market looking ahead to 2024 if we get in a situation where the company is growing and on track to generate positive cash flow.

Until then, our baseline here is for shares to remain volatile with plenty of reasons for the market to remain skeptical with plenty of work to be done on the part of management and the company to deliver at least a sense of stability and greater financial clarity.

{kind=link}

Seeking Alpha

Final Thoughts

We rate APRN as a hold implying a neutral view over the near term. The bullish here is that Blue Apron captures something of a brand resurgence with the addition of new customers helping sales and earnings to even outperform expectations.

On the other hand, the risk is that any new marketing initiatives fail to kick start a new wave of growth which would mean continued financial losses and a recurring cash bleed. Here, Blue Apron remains exposed to macro conditions with weaker trends towards consumer spending undermining the operating environment. Weaker than expected results would open the door for a deeper leg lower in the stock and force a reassessment of the long term outlook.

For further details see:

Blue Apron: Recipe For Financial Turnaround Looks Good, But Growth Still Missing