MRSN - bluebird bio: A Risk Worth Taking

2023-07-12 10:45:16 ET

Summary

- bluebird works as a biotech company developing curative gene therapies to save lives.

- Concerns over its cash runway and clinical trials are overblown, with the stock near all-time lows.

- Near-term catalysts from Lovo-cell, Zynteglo, and Skysona are completely overlooked, in my opinion.

- I am initiating on BLUE with a Buy recommendation with a FY23 price target of $5.8, according to my DCF valuation.

Well, sit down at the poker table, my friend, because investing in bluebird bio (BLUE) is much like playing a suspenseful hand of poker - thrilling, unpredictable, and potentially rewarding. When you go all-in with BLUE, you're basically putting your chips on gene therapy - a revolutionary approach in biotech that could hit the jackpot by modifying genes.

The excitement begins in 2024. Will the FDA give the nod to "lovo-cel", BLUE's wonder drug against sickle cell disease? If they do, we could be looking at a windfall. Remember that epic price surge of Mersana ( MRSN ) I covered ? Yeah, we could see that again by Dec-20th this year.

Secondly, I got my eyes on Zynteglo, another ace in BLUE's deck. If it gets its time in the spotlight, lovo-cel could hit a flush, making waves in the market, just as when you've got a strong pair in your poker hand.

Then there's Skysona for CALD - a rare but tough disease. It's the wildcard here. If it takes off, we could rake in peak sales of $50 million. Rare, yes, but remember, it's often the dark horses that win the race.

Now, I'm not calling "All in" on BLUE yet. There's the risk of share dilution, and their pipeline could use some diversifying - kind of like trying to play poker with half a deck. But considering BLUE's undervalued position and the promising hand it's holding, I say let's put some chips on BLUE. I initiate a buy rating on blue and have set a price target of $5.8 for FY23, according to my 10-year DCF valuation, with a 1% terminal growth rate and a 9.5% WACC.

bluebird bio - Overview

Just as a savvy gambler understands the game, it's vital for an investor to know where their money is going. I've provided an overview below - take a look and see if my take aligns with your investment strategy and risk tolerance:

It was in 2010 in Somerville, MA, when bluebird bio ((BLUE)) just got started. They are currently creating one-time, curative gene therapies that could change lives forever. As of writing, BLUE has two FDA-approved products under their belt:

{kind=link}

bluebird bio's product pipeline (www.bluebirdbio.com/our-science/pipeline)

Above is BLUE's latest pipeline. This pipeline is what bluebird bio does, what they have done, and what it will continue to do by developing and commercializing its programs:

- Zynteglo is the first card. This therapy is a potential game-changer for those struggling with transfusion-dependent beta-thalassemia (TDBT). It's like a solid Ace in a poker game.

- Then, there's Skysona , a promising card drawn against cerebral adrenoleukodystrophy or CALD. It's proof of BLUE's commitment to tackling rare and severe diseases.

- Finally, we've got lovo-cel , their late-stage clinical candidate. This therapy is aiming to bring relief to those living with Sickle Cell Disease or SCD. Think of it as another strong card up their sleeve.

These are the key players, the flop, if you will, in BLUE's poker game. When you invest, you're placing your chips on Zynteglo, Skysona, and lovo-vel. You're hoping that the next cards turned (the turn or the river) spell out "commercialization" for any of these three. If an FDA approval comes through, it's like hitting a royal flush. Even a progression from an early-stage to a Phase 1, 2, or 3 program is a win. The faster they make progress, the quicker you could see a return on your gamble.

Investment Thesis

1. The potential FDA approval of lovo-cel

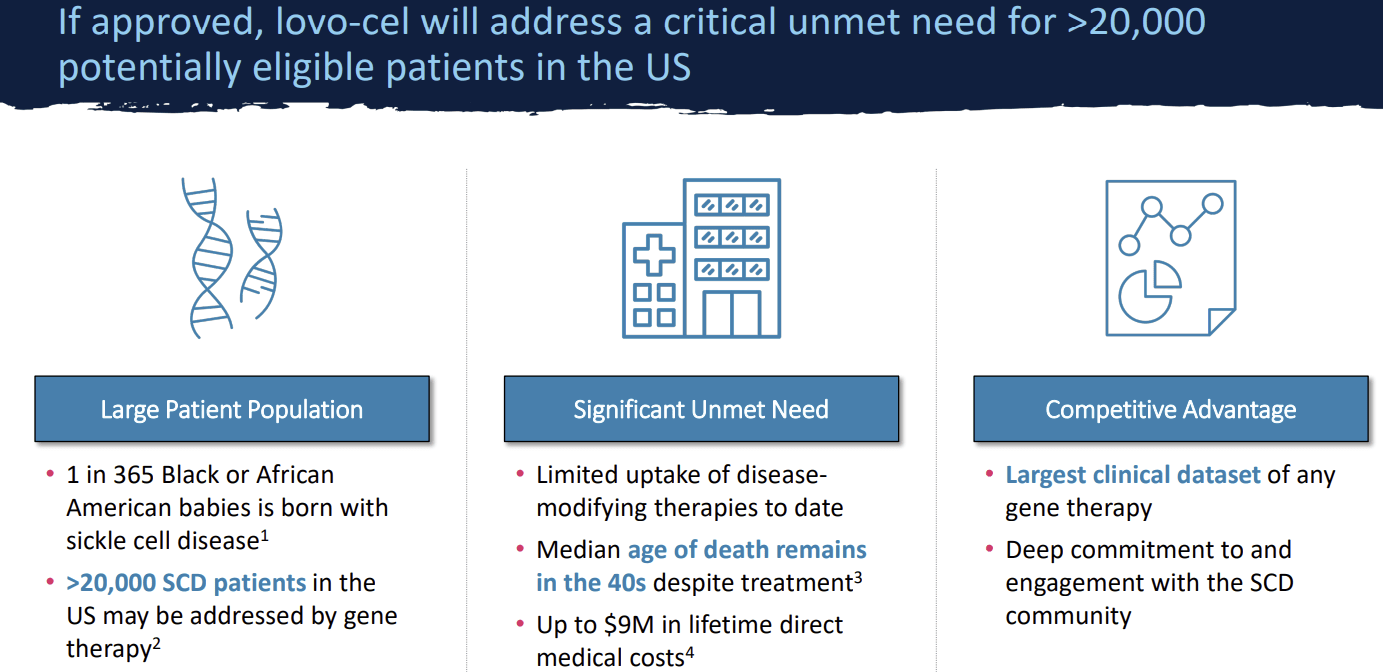

Understanding sickle cell disease or SCD

SCD is a genetic blood disorder where hemoglobin, the protein responsible for transporting oxygen in the body, is affected. In SCD patients, a single nucleotide alteration in the ?-globin gene results in Hemoglobin S (H.b.S), which distorts red blood cells into a sickle shape. This leads to complications like chronic anemia, severe pain, crises, strokes, and some other bad stuff. It is a prevalent disorder, affecting ~100K people in just the US .

Existing treatments and their limitations

Current Treatments for SCD focus on managing symptoms and preventing the sickling of red blood cells. Many drugs and therapies are used, including Oxbryta, Adakveo, hydroxyurea, folic acid, and antibiotics. Allo-HSCT is the only potentially curative option but carries some big risks due to possible graft-vs-host-disease (G.v.H.D). In my view, there is a clear need for more effective and less risky treatments, and I believe:

Lovo-cel is a promising approach

{kind=link}

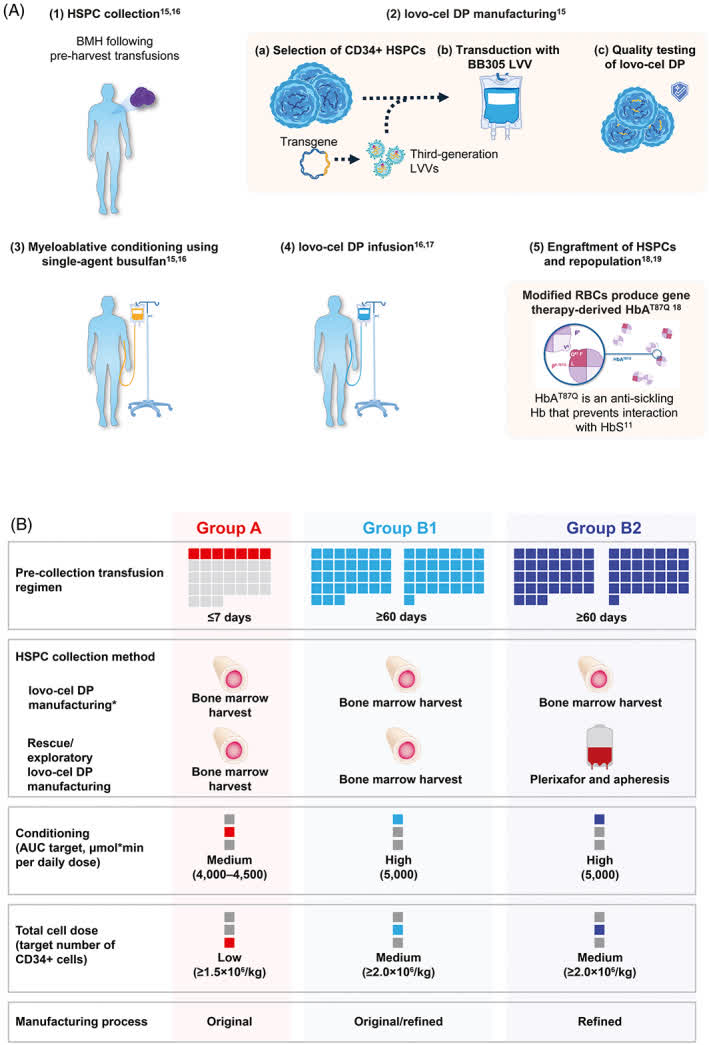

Lovo-cel manufacturing process (American J Hematol. 2022. Lovo-cel gene therapy for sickle cell disease)

As seen above, Lovo-cel, developed by bluebird bio, is a novel gene therapy being investigated for SCD. It uses an autologous hematopoietic stem and progenitor cell (H.S.P.C) therapy where patient-derived HSPCs are altered ex vivo with a BB305 lentiviral vector encoding a modified ?-globin gene, producing normal, non-sickling hemoglobin. The manufacturing process has been iteratively refined to increase yield and transduction efficiency.

Clinical evidence supporting lovo-cel

{kind=link}

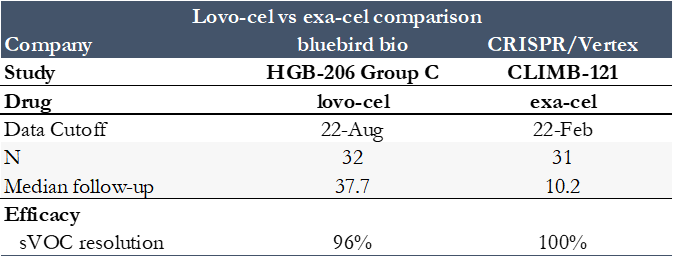

Company Reports

Source: Company Reports

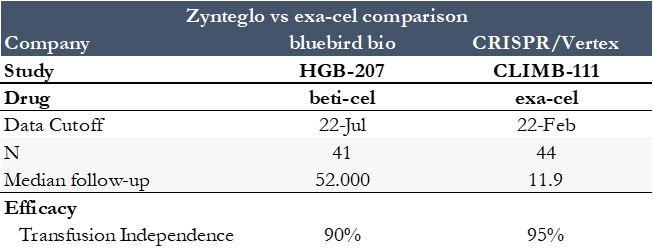

The clinical data for lovo-cel has shown encouraging results, in my view. Among the treated patients, 96% experienced complete resolution of severe vaso-occlusive events after 24 months. The safety profile aligns with expectations for SCD and the busulfan conditioning necessary for transplantation. When compared to competing therapies like Vertex/CRISPR’s exa-cel, lovo-cel has a comparable efficacy and safety profile.

Regulatory pathway and potential approval

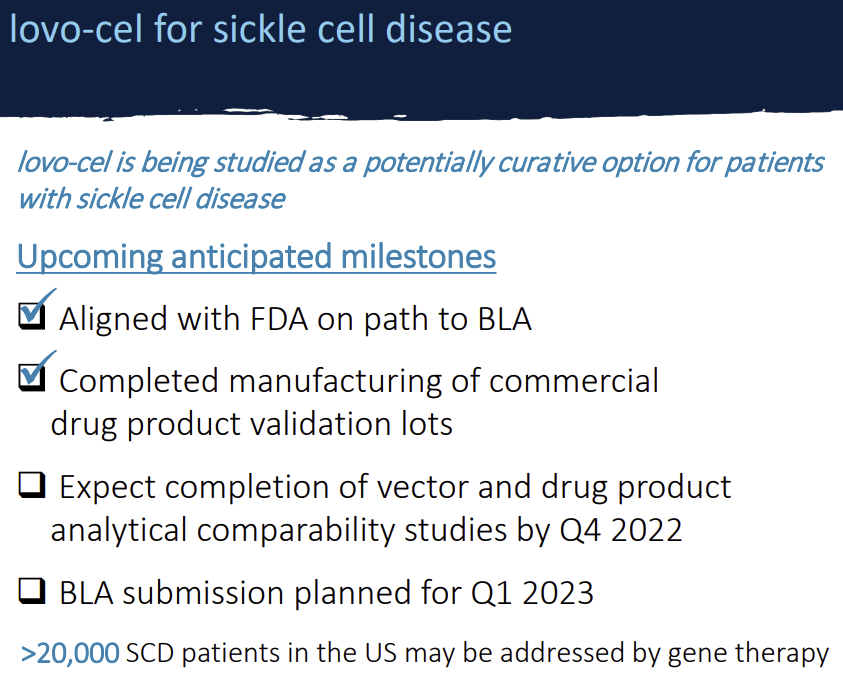

{kind=link}

Investor Presentation (Sep-2022)

Bluebird bio submitted a Biologics License Application (B.L.A) for lovo-cel in April 2023. If things go as planned, we could see FDA approval by the end of 2023 and a commercial launch in early 2024. There is a general sense of optimism around the regulatory review process, with no requests for additional clinical data by the FDA.

Physician enthusiasm and market demand

Surveyed hematologists express high excitement for a gene therapy/editing candidate like lovo-cel for SCD, with 84% showing moderate to high interest. The potential for a curative treatment option has generated significant buzz in the medical community. However, there are some adoption barriers, like hospital bed availability and patient awareness, which need addressing.

Market forecast and commercial potential

According to JPM, lovo-cel could make a significant splash in the market, estimating peak sales of around $400-$600 million in the US. If approved and launched by 2024, it will likely increase steadily in market penetration, potentially capturing 3-5% of the market in the next 10-15 years.

{kind=link}

Investor Presentation (Sep-2022)

Lovo-cel is a priority for the FDA this year

Given the recent news of the FDA granting priority review for BLUE's BLA for lovo-cel, the company's potential for success seems upward. Notably, the FDA's action underlines the potential of this innovative gene therapy and brings us closer to its approval and subsequent commercial launch. The FDA has set a regulatory action date of December 20, 2023.

Bottom line , an FDA green light for lovo-cel will spur a revival for BLUE's stock from its present all-time lows. I do not believe this is just a roll of the dice but a challenge to the prevailing bearish sentiment in the share price and potentially a turning point in SCD treatment.

2. Zynteglo for ?-thalassemia

Brief overview on ?-thalassemia

Beta-thalassemia’s are a group of inherited blood disorders caused by reduced or absent production of the beta globin protein, which is essential for the formation of functional hemoglobin. The most severe form, ?-thalassemia major or Cooley’s anemia, often requires lifelong transfusions and can lead to a shortened lifespan. The condition affects around 1,500 people in the US and is characterized by symptoms such as severe anemia, bone deformities, cardiac diseases, growth delays, and splenomegaly. Understanding this is crucial for the next few parts of the catalyst.

{kind=link}

Investor Presentation (Sep-2022)

?-thalassemia’s current treatment landscape

Treatment options include regular red blood cell transfusions, iron chelation therapy, and bone marrow transplants. The bad thing is that these treatments can lead to complications such as chronic iron overload and organ damage. There is also the challenge of finding suitable bone marrow donors. Currently, FDA-approved treatments include deferoxamine and deferasirox for iron overload and Reblozyl for adults who require regular red blood cell transfusions. The existing treatments, while helpful, still leave patients dealing with serious complications, signifying a clear need for a more effective option. With that in mind, the next few parts of the catalyst will explain my rationale for why I think Zenteglo is like one size fits all:

Zynteglo: mechanism and manufacturing

{kind=link}

Investor Presentation (Sep-2022)

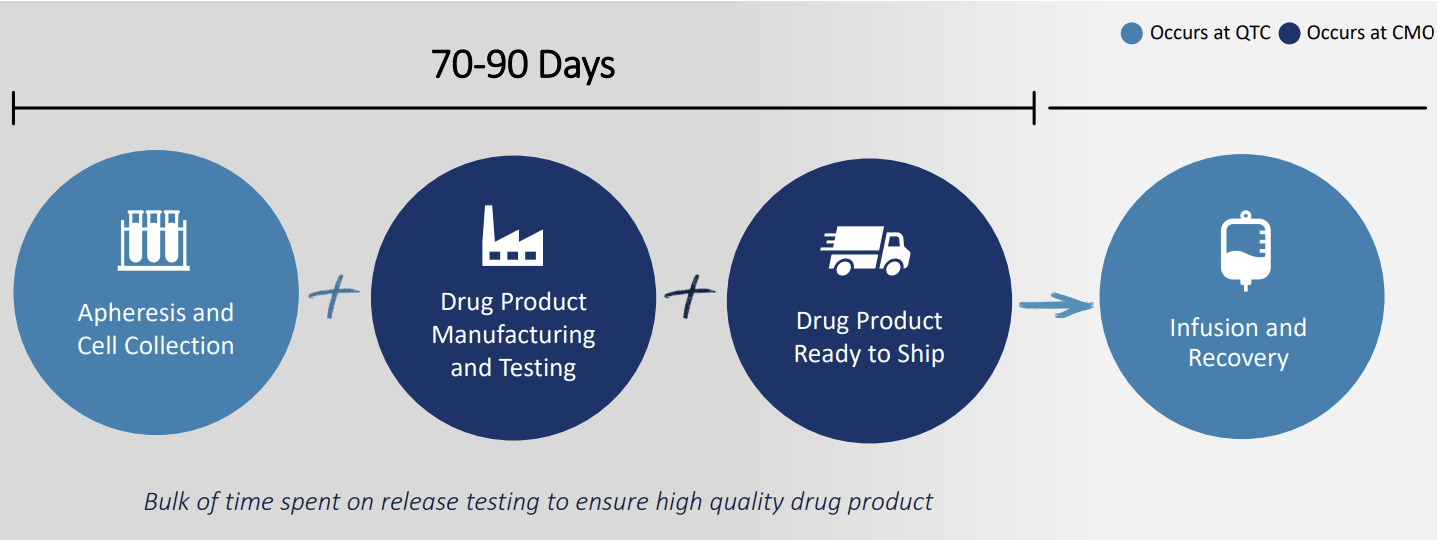

Zynteglo, developed by bluebird bio, is a gene therapy that provides a functional copy of the modified ?-globin gene via transduction of autologous CD34+ cells using a self-inactivating BB05 lentiviral vector. The manufacturing process involves the collection of peripheral-blood hematopoietic stem cells, isolation, activation, and transduction of CD34+ cells, which takes about 70-90 days. This to me shows that Zynteglo’s innovative gene therapy approach has the talent and potential to provide a more targeted and enduring solution for patients suffering from ?-thalassemia.

Clinical data

{kind=link}

Company reports

Source: Company Reports

A phase 3 trial involving 41 patients showed that 90% of them achieved transfusion independence, with the longest follow-up to 8 years after treatment. The tolerability profile of Zynteglo was consistent with myeloablative conditioning. In other words, the clinical trial for Zynteglo was impressive by showing the therapy’s high effectiveness.

Commercial strategy and expectations

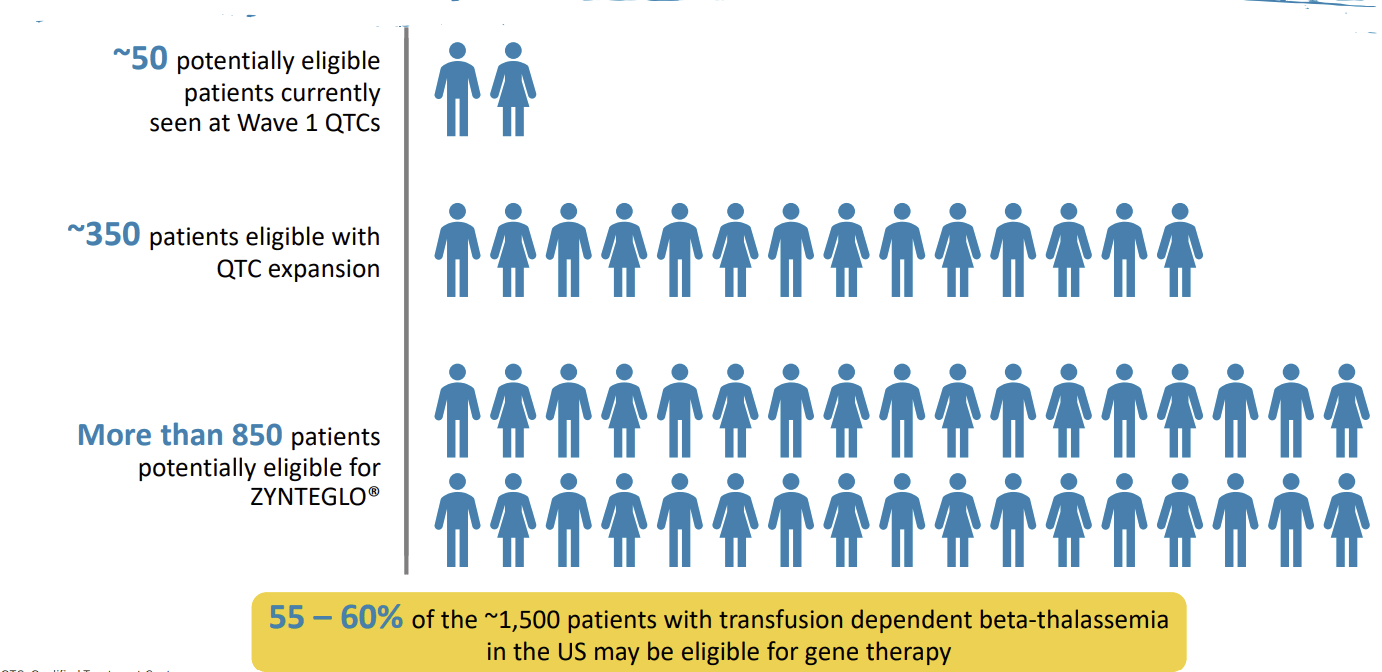

BLUE estimates that about 850 patients in the US are eligible for gene therapy. They plan to expand to about 40-50 qualified treatment centers by the end of 2023 to facilitate the Zynteglo launch. The therapy is priced at $2.8 million upfront, with a contingency of up to 80% rebate if patients do not achieve transfusion independence within two years. Basically, BLUE’s strategy to expand treatment centers and their flexible payment plan makes Zynteglo accessible to a larger number of patients.

Survey highlights

Surveyed physicians highlighted transfusion dependence, iron overload, noncompliance with iron chelation therapy, and end-organ damage as key areas of unmet need. Eligibility for stem cell transplant depends on control of the underlying disease, patient health, and compliance with iron chelation therapy. Challenges to the adoption of Zynteglo included myeloablative conditioning, cost, and access to payer coverage. Overall, the survey results, to me, underline the pressing need for better treatments and confirm that Zynteglo can address these key issues currently faced by ?-thalassemia patients.

Market projections

Following the launch in 2023, Zynteglo is projected to achieve a market penetration of about 25% by 2028, with peak sales nearing $400 million in the US. This suggests a promising future for the therapy, benefiting both patients and BLUE.

The point is , should Zynteglo receive FDA approval, this makes for another reason we could witness BLUE making a major comeback from its lows. Backed by robust clinical trial results and a well-charted commercial strategy. To me, this isn't just about betting against the odds but a stand against the bearish status quo, potentially opening a new chapter in the story of ?-thalassemia treatment.

3. Skysona for CALD

Cerebral Adrenoleukodystrophy (C.A.L.D.) 0verview

CALD is a pretty deadly genetic disorder that impairs the ability of the body to break down very-long chain fatty acids (VLCFAs). This inability leads to a harmful accumulation of VLCFAs, which damages adrenal and nervous tissues, and is especially severe in the case of CALD, as it affects the central nervous system. Point is, bluebird’s Skysona targets a disease with a significant unmet need, positioning it as a potential game-changer in CALD treatment and a major win for the firm.

CALD’s current treatment

Before Skysona , the primary treatment was a specialized type of stem cell transplant, but only if a genetic match was available, otherwise patients were left to merely manage the symptoms. So, by having an effective treatment option for CALD, irrespective of the need for a genetic math, I see Skysona filling an important gap in the treatment landscape, thus, signifying a significant market opportunity for bluebird.

Skysona early launch

Skysona works by using a lentiviral vector to modify a patient’s own stem cells to produce a protein that can counteract the effects of CALD. Early data showed us that most patients treated with Skysona survive w/o major functional disabilities, and it has already been approved and launched in the US. I like this because it is an innovative treatment approach, combined with attractive early results, thus, reinforcing bluebird’s position as a leader in the field, which I believe should enhance investor confidence and share value.

The market

Even though CALD is rare, Skysona’s unique treatment approach could lead to peak sales of around $50 million in the US marke t. So, with a high barrier to entry, no clear competitors, and potential for strong sales, Skysona could deliver steady revenue streams and continue to drive shareholder value over time.

Bottom line , with Skysona's approval, this makes for my third reason that I'm calling the bluff on BLUE's current lows. It's not merely about riding the wave of uncertainty but challenging the bearish undercurrents and possibly setting a new standard in CALD treatment while contributing to sustained shareholder value.

Valuation

Cash Runway Through 2024

With ~$318 million in cash & equivalents and no debt outflow or inflow projected in the coming years, the street forecasts a cash outflow of $182 million for FY23 and another $183 million cash outflow in FY24.

Combined, this means that BLUE will be financing around $365 million over the next two years, and still in need of ~$50 million more to do so. This could be done by issuing additional debt, which is unlikely, or by diluting shareholders again, which will likely happen sometime in 2024. This is never a good sign and just another reason why I did not rate this company a "strong" buy.

However, with my optimistic look on the company, I believe that another small share dilution in 2024 will only dilute shares by a little bit, given that I see this company trading at over $800 million by 2024.

Discounted Cash Flows Analysis

{kind=link}

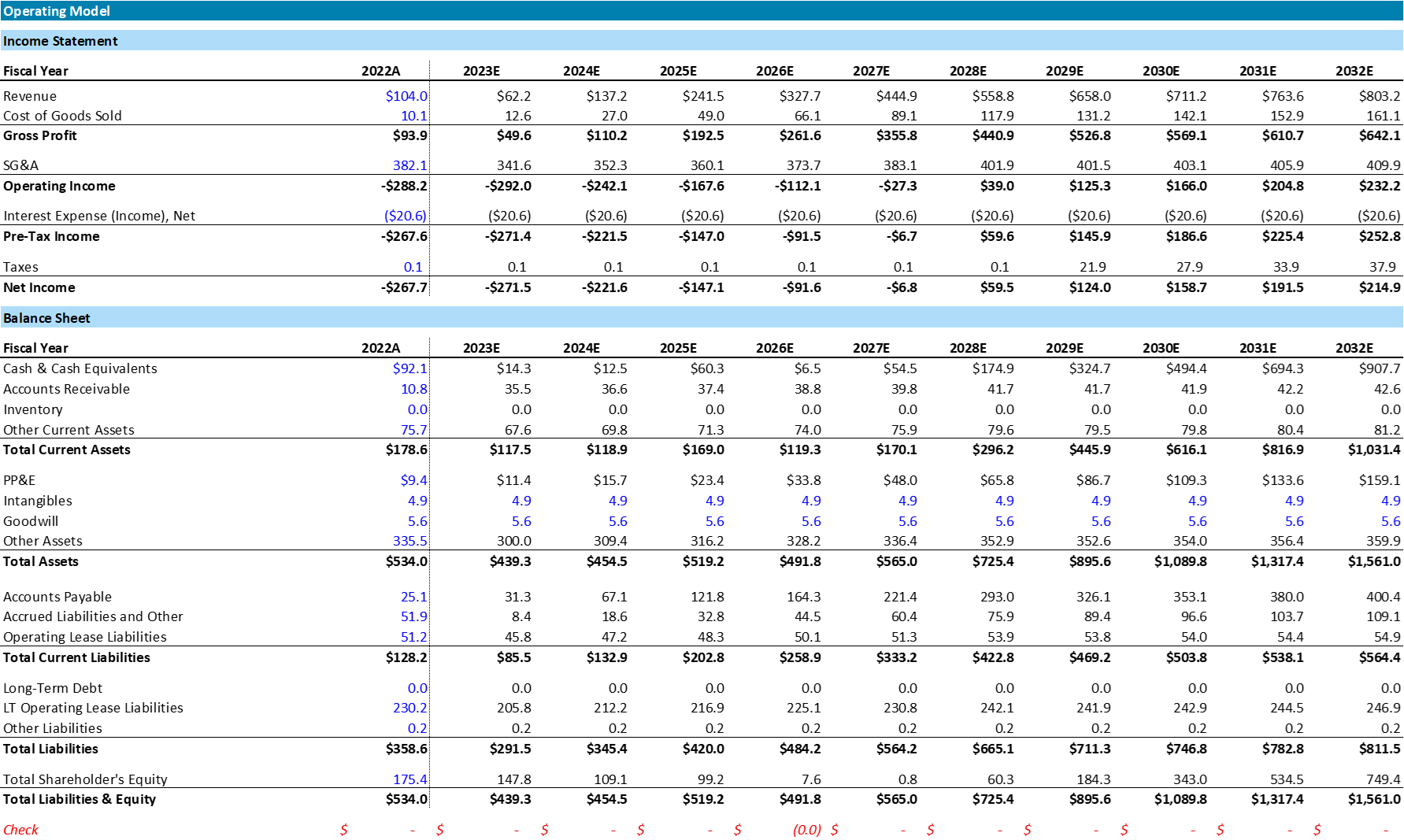

Income Statement and Balance Sheet Assumptions (Author's Data)

{kind=link}

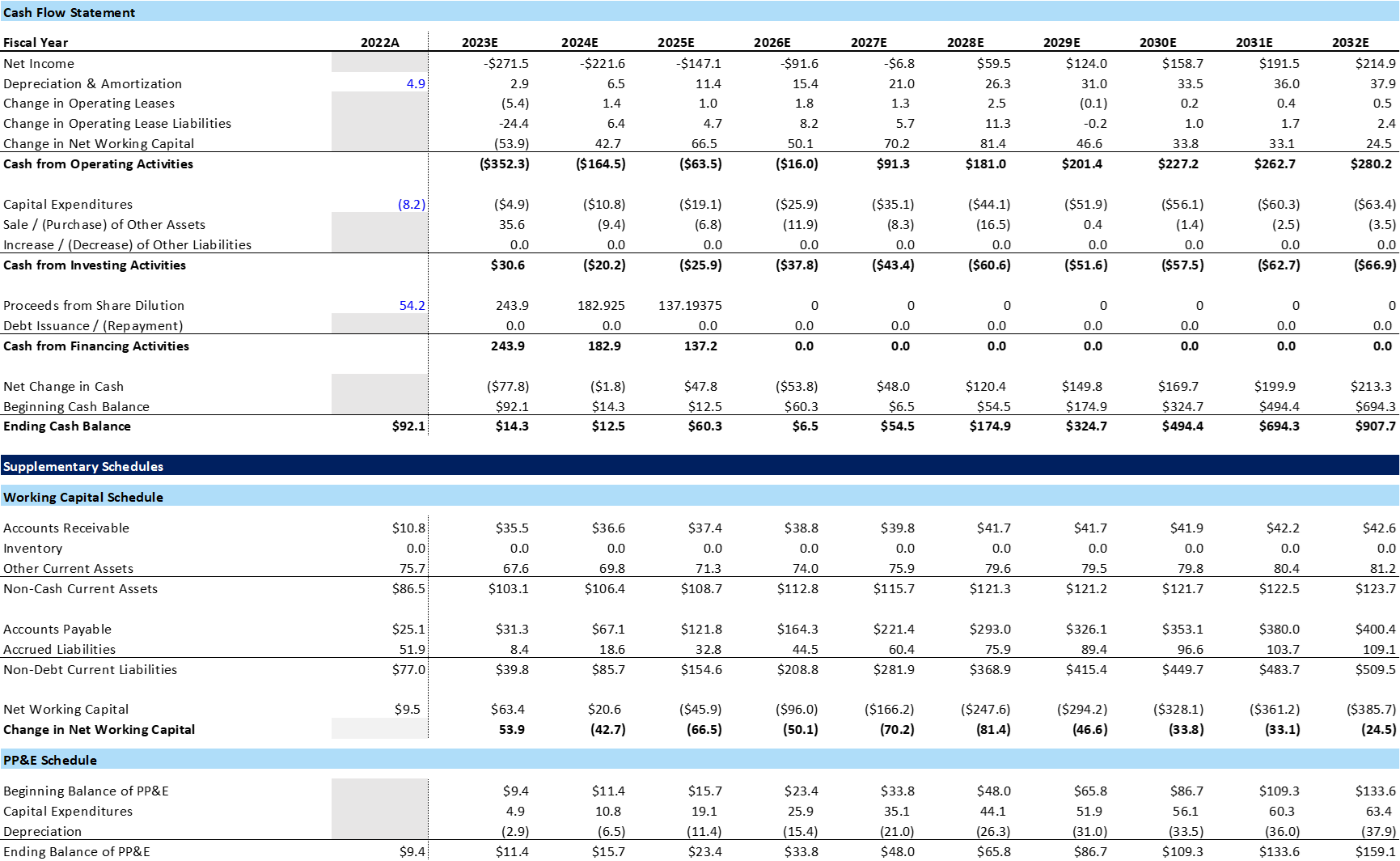

Cash Flow Statement, Working Capital, and PP&E Schedule Forecasts (Author's Data)

{kind=link}

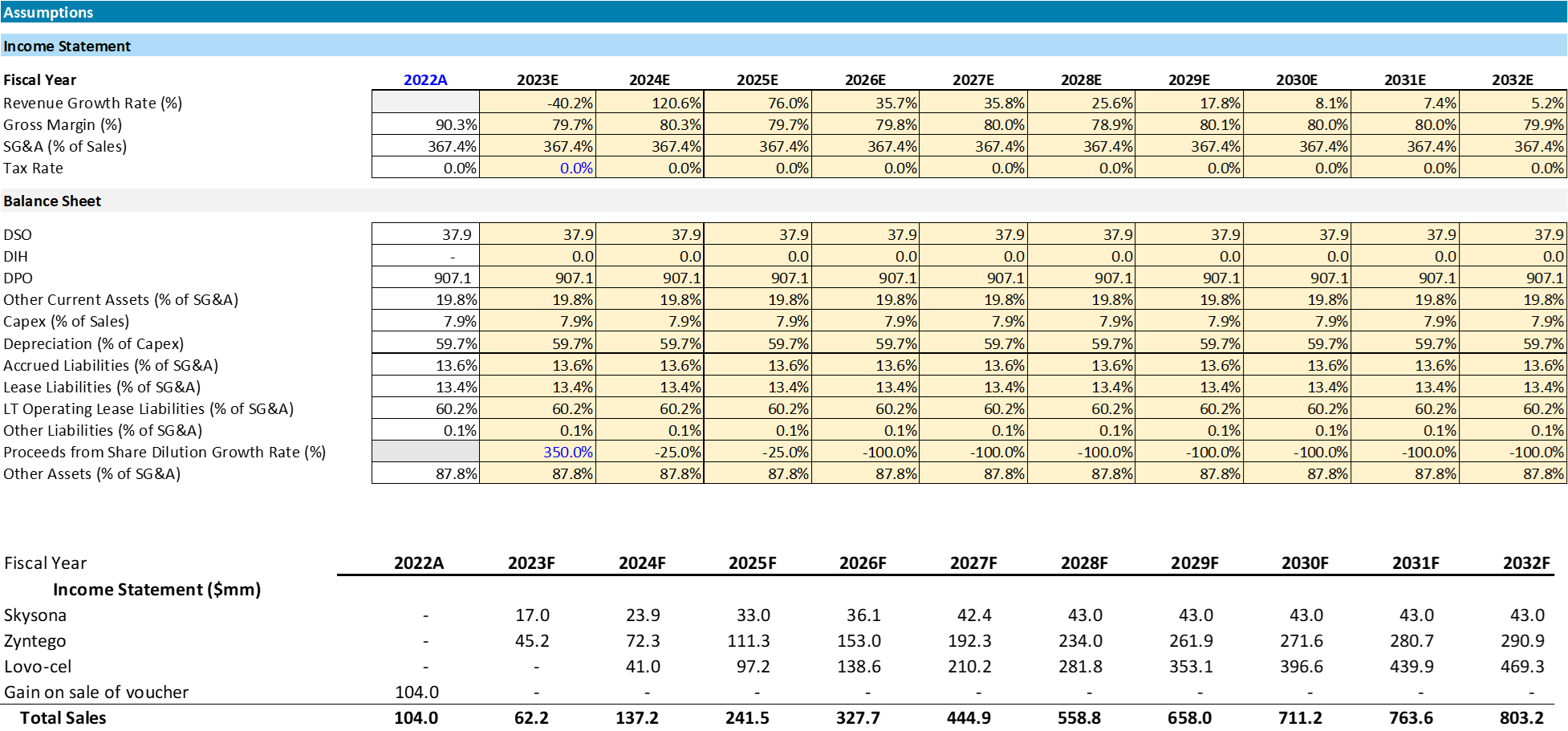

Operating Model Assumptions (Author's Data)

{kind=link}

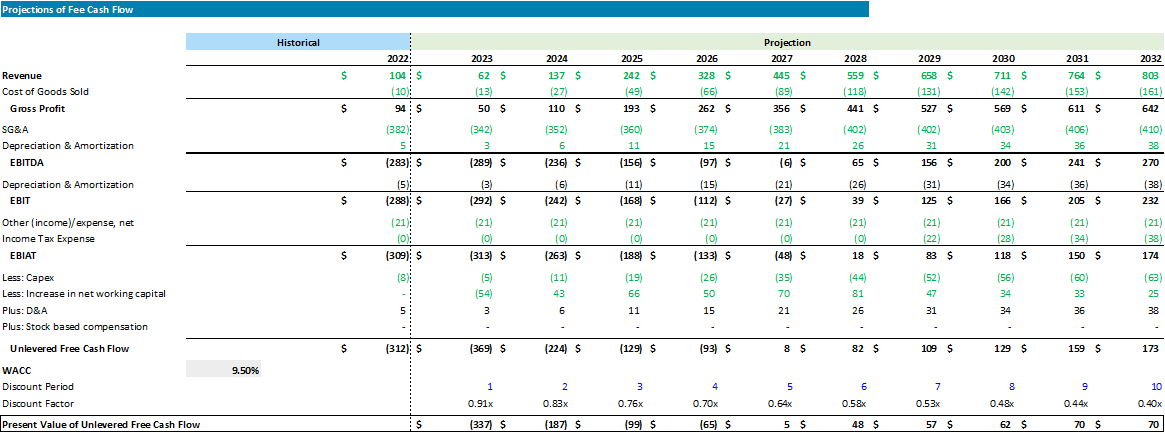

Discounted Cash Flows Analysis (Author's Data)

{kind=link}

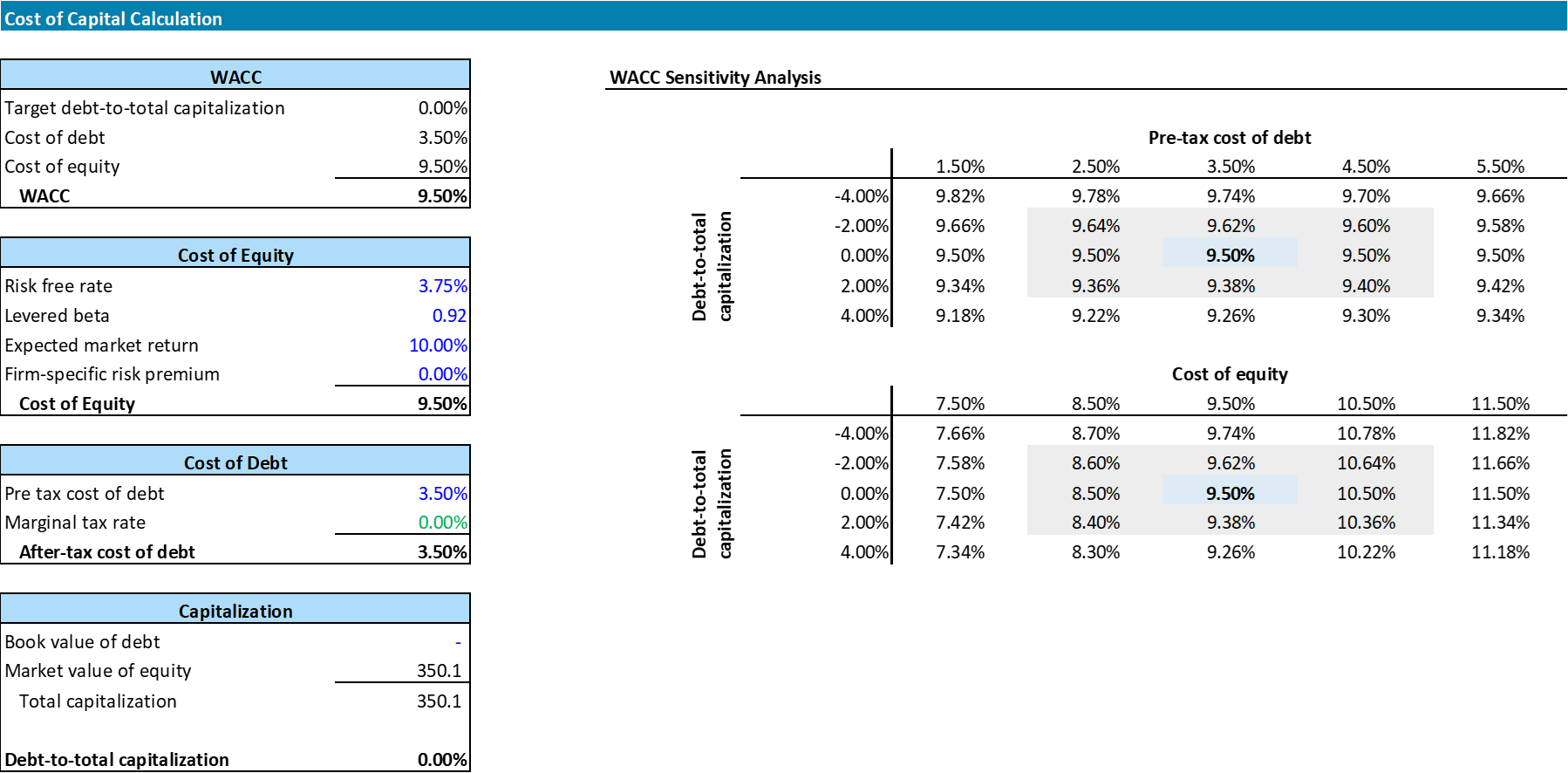

WACC Calculation (Author's Data)

{kind=link}

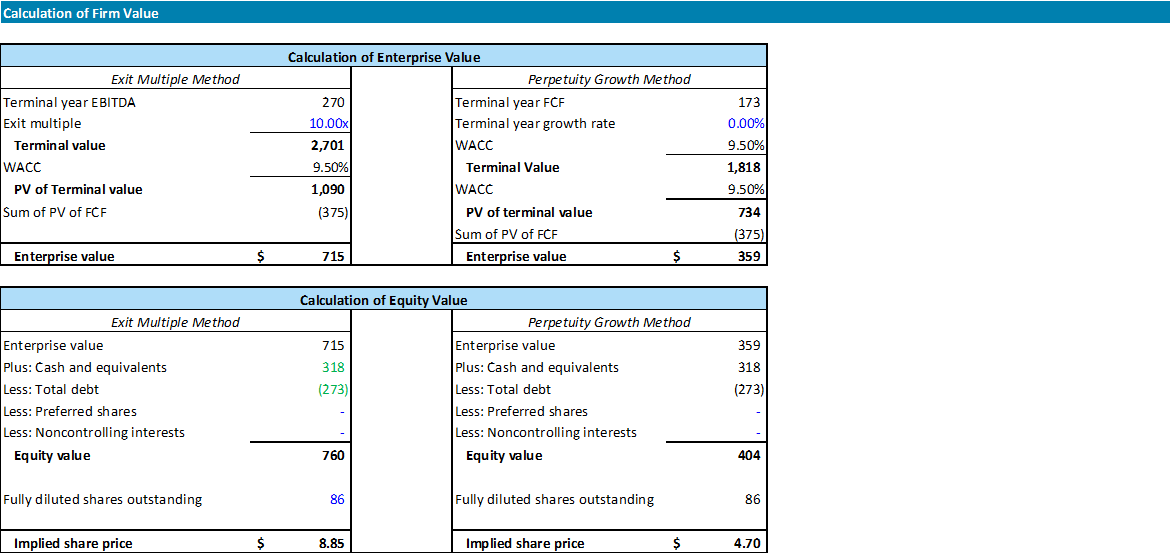

DCF - Price Target Calculation (Author's Data)

{kind=link}

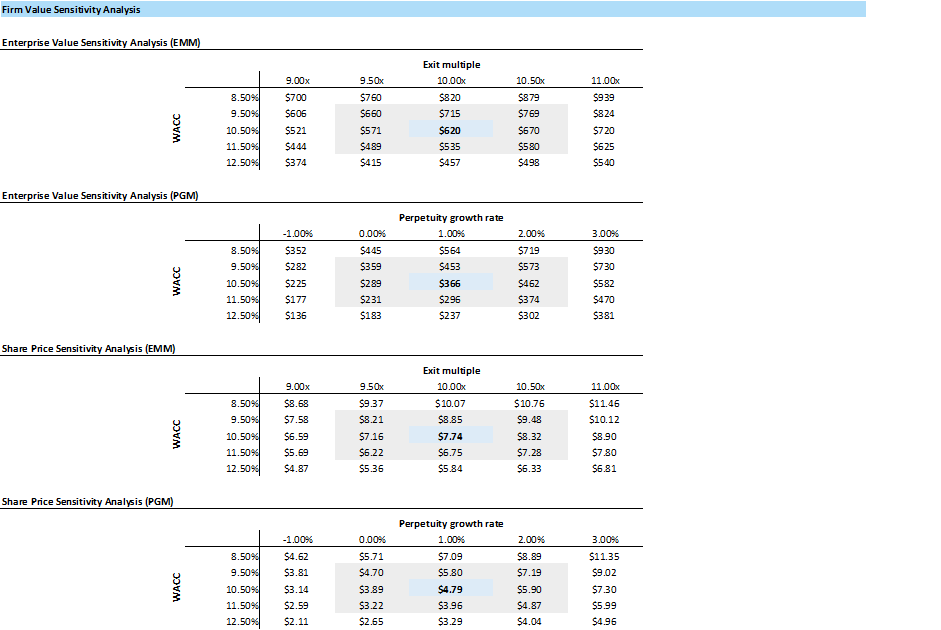

Price Target Sensitivity Analysis (Author's Data)

As an investor, doing this in-depth DCF analysis on a biotech firm like BLUE kinda feels similar to dealing a poker hand - I have to weigh each card carefully and make strategic adjustments to the game plan. I used the consensus (Capital IQ) projections for BLUE over the next decade while taking some liberty to shuffle the deck a bit. I have lowered sales estimates for 2023 and 2024 to allow for FDA timing, but I am also upping the ante with higher sales expectations for lovo-cel from 2025 onward.

With a conservative 0% perpetuity growth rate and a calculated 9.5% WACC, I'm dealt a price target of $4.7. Now, if I switch gears and use a 10x EBITDA multiple, the price target skyrockets to $8.86. But keep in mind, playing the EBITDA multiple cards depends heavily on 2032's EBITDA, which is like trying to predict a royal flush - highly unpredictable. For small biotech companies like BLUE, it's safer to stick with the perpetuity growth methodology.

Still, the price target is completely sensitive to the terminal growth % and WACC %. Even a slight uptick to a 1% growth rate sends the share price climbing to $5.8, while a 2% growth rate catapults it to over $7. Considering BLUE's current share price hovers around $3.3, hitting near all-time lows, I'm calling the bluff and maintaining a buy-under $4.7 price target for FY23 (assuming 0% growth rate). My overall price target for FY23, with a more ambitious 1% growth rate, lands at $5.8 - that's over a 70% upside to today's prices. However, if Lady Luck graces us and the price surges past $6-7 in the next year, I'd recommend cashing in some of those chips and taking profits.

Risks to rating and price target

First off, it's like BLUE's drawn three of a kind. Not bad, right? But what if we only have three cards in the deck? With just three programs under development, the company's pipeline isn't as diversified as I'd like , which puts it at greater risk of clinical trial failures. The ongoing clinical trials for their programs treating CALD, TDBT, and SCD are akin to the unfolding rounds of a poker game - any misstep could sour the pot.

But the game isn't solely in BLUE's hands. The 'dealer', in this case, the FDA , has grown stricter over time , and they can upend the table without warning. Any delays or unexpected requests from the FDA might put BLUE's chips in a shaky position. Again, it’s a situation where a more diversified hand (or, in this case, pipeline) could soften any potential blow.

Then we have the financial risk - the chips on the table, if you will. As it stands, BLUE has around $270 million in cash, and in January of this year, they raised ~$130 million in proceeds from secondary public financing. Now, the company has around $318 million in cash available, and the street forecasts ~$365 in cash outflows for the next 24 months. This will likely result in the company requiring additional capital to fund operations to commercialize their programs sometime in 2024. However, I do not see this as such a big risk, as it is already priced in, and I have a more optimistic look on where the company will be trading at by the time they dilute shares again.

The final notable risk I see is patent litigation - the bluff of the biotech poker game. BLUE holds a handful of patents, but it's always possible someone could challenge their claim.

The bottom line

I'm confident that the market has exaggerated worries about BLUE's clinical trials and financial reserves. It's time we shift the narrative. With three potent candidates in the pipeline, I'm not just recommending a buy; I'm betting on BLUE's comeback. I'm setting a target price at $5.8, a healthy 76% uptick from the current $3.3, as of writing.

Looking forward to your comments - drop a note below with your thoughts on BLUE, any tips for enhancing my articles, or your opinion on the poker analogy I used in my summary and in the risks. Your feedback is very valuable to me.

For further details see:

bluebird bio: A Risk Worth Taking