BXC - BlueLinx: This Time Looks Different

2023-10-05 02:28:13 ET

Summary

- BlueLinx is a prominent player in the building materials distribution industry in the US, serving a wide range of customers in residential and commercial construction projects.

- The company has improved its financials and balance sheet, with higher gross margins, strong shareholder equity, and ample liquidity.

- Despite potential short-term risks from a slowing housing market, BXC's long-term outlook is favorable due to its focus on repair and remodeling, which has demonstrated lower cyclicality compared to new construction.

I have been a homeowner for two years and there are a few things I have realized in these two years. There are expenses that you do not foresee, some expenses that you foresee but still cannot hold off on, and expenses that actually save you money. Spending money when you don't want to, especially in this economy is never a pleasurable thing to do. Since I am an equity investor, I try to be an opportunist here. Aren't many people in the same boat? Is there any way I can benefit from this? Going down this rabbit hole, I landed on a long list of stocks in the home-building space. Investing in this space in the current environment can be tricky but there are a few names on my radar that I thought exhibited strength and would be ready to jump on at the right opportunity.

In this write-up, I will talk about BlueLinx ( BXC ) and how this company stood out to me.

The Business

BlueLinx is a prominent player in the building materials distribution industry in the United States. Their core business involves the distribution of a wide range of construction-related products, including lumber, structural panels, roofing, siding, insulation, and more. They serve an extensive customer base consisting of dealers, retailers, and industrial manufacturers engaged in residential and commercial construction projects.

With an efficient logistics and warehousing network with strategically located distribution centers across the country, they are able to streamline operations and serve customer-specific needs. What bothers me about the business is how cyclical it can get and how worse the stock performs when the economy is not doing well. Multiple market participants are calling for a soft landing or a no landing but this looks highly unlikely given the conditions we are in (Yield curve inversions are a time-honored recession signal)

So it is prudent that we understand its past behavior and the conditions of the company during that time and what has changed from then.

Rewinding to pre-GFC Vs. Now

Our last recent memory of a big financial crisis that was borne out of the housing market was the time period between 2007 - 2009. Around that time period, the stock lost more than 85% of its price and an investor holding through this drawdown would be in a precarious position indeed. In fact, the highs reached by the stock pre-GFC have still not been reached 18 years later. I understand that many stocks undergo vicious drawdowns during times of market stress and that does not necessarily mean much for long-term investors if the company is still sound. Patience would be key for investing in the long term. But you wouldn't be able to say that the company was in the best shape if you looked at it before it headed to the recession.

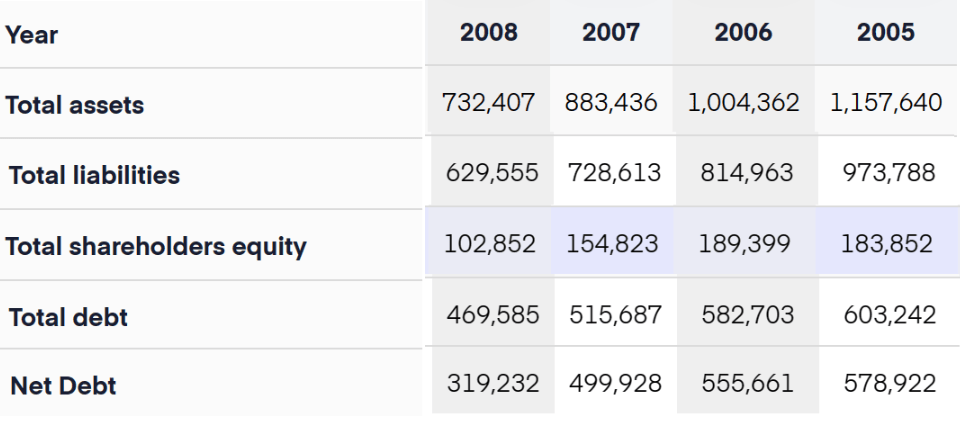

In 2005, the company had its highest revenues ever (which it still has not been able to beat). But underneath the surface, things looked different . Gross margins were low and the balance sheet needed work. Against the total assets of $1.15 B, its total liabilities were $973M giving us a low shareholders equity. Its total debt-to-equity ratio stood at approximately 3.3.

{kind=link}

{kind=link}

Fast forward to now, the revenues are definitely lower and for LTM it is $3.5B. The last quarter alone saw a huge drop in QoQ sales and net sales decreased by 34% to $816M (Profitability has also dropped accordingly). But the difference in margins and the balance sheet is remarkably different between then and now.

1. Gross margins have taken off and are currently close to 17%

2. Has total shareholder equity of $622.8M and net debt of $153M, and has a debt-to-equity ratio of 0.47

3. Cash on Hand of $418M which suggests plenty of liquidity and no material outstanding debt maturities until 2029

The difference between these metrics in 2005 and now is night and day. The focus now seems to be more on strengthening the company as opposed to just being focused on the top line. Certainly, they look better prepared for a recession in the last few years than at any other time during their 20-year history.

{kind=link}

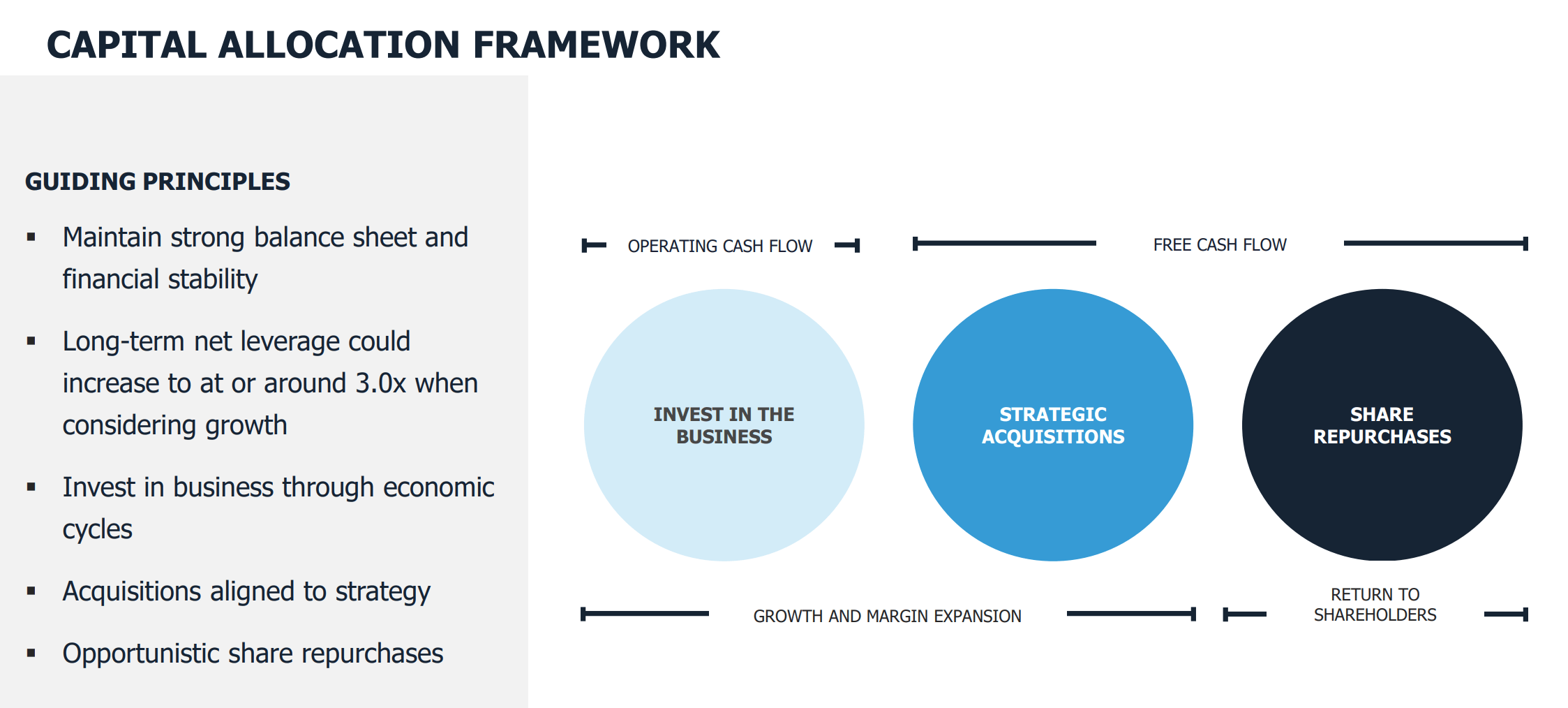

Vision

I believe their excellent management of the company in the last few years sets them up really well against companies that are weak and could be vulnerable in a downturn. They see an addressable market of $40B and a competition that is highly fragmented. With their superior capital allocation strategy they could pick up troubled companies in the face of a downturn and beef up their offerings. This could create a nice flywheel effect of accelerating growth through acquisitions, optimizing their operations, creating value, and eventually moving on to the next target (This strategy has been demonstrated well if we look at the last acquisition as an example. The company acquired Vandermeer Forest Products and its other assets for $67M and the entire transaction was funded through cash on hand)

Growth Flywheel (Investor Presentation)

{kind=link}

Valuation

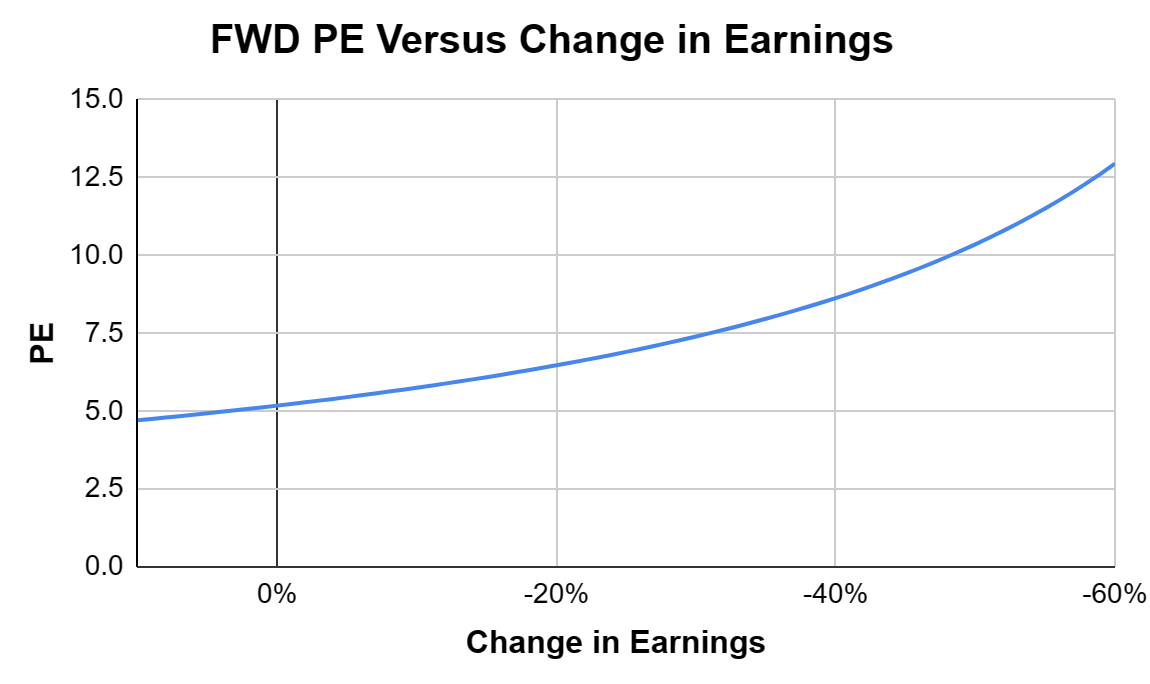

On a Price-to-Earnings basis, the company looks quite undervalued at 5.4x (Sector median 18.6x). Even on an OCF basis with the company making $450M in LTM, the P/CF ratio is also quite low at 1.5x (Sector median 12.5). But what matters more here is their forward metrics. Although the company did not provide guidance, diluted EPS has been declining YoY. This combined with the fact that we are going into a slowing Housing industry and an uncertain economy means earnings could get a lot lower from here. In such situations, it would be wiser to model the forward multiples under a range of scenarios.

Author Computed from Company data

{kind=link}

If we look at the worst-case scenario and expect the EPS to drop by more than 60% we see PE inflating beyond 13x. Even though it looks like it is less than the sector median for now, in a recessionary environment the sector median could come down and be a lot lower than 13x. In fact, in the worst of the recession, the company reported a loss and the metric would not even be comparable to the sector median. The difference this time is as we saw the company's management has put in significant effort to strengthen the company by its foundations and has a lot more confidence that they can survive the worst-case scenario.

Warning Signs

A slowing housing market and a recession can introduce severe drawdowns on the stock price. Many cyclicals tend to exhibit this behavior during such environments and BlueLinx would be no exception. According to their 2022 annual report, approximately 40% of the annual sales come from residential new construction. Most of the factors highlighted in their annual report are currently flashing warning signs that could potentially affect the stock price.

We believe demand for residential new construction is driven by a myriad of factors including, but not limited to; mortgage rates, which recently reached multi-year highs; lending standards; home affordability; employment conditions; savings rates; the rate of population growth and new household formation; builder activity levels; the level of existing home inventory on the market; and consumer sentiment

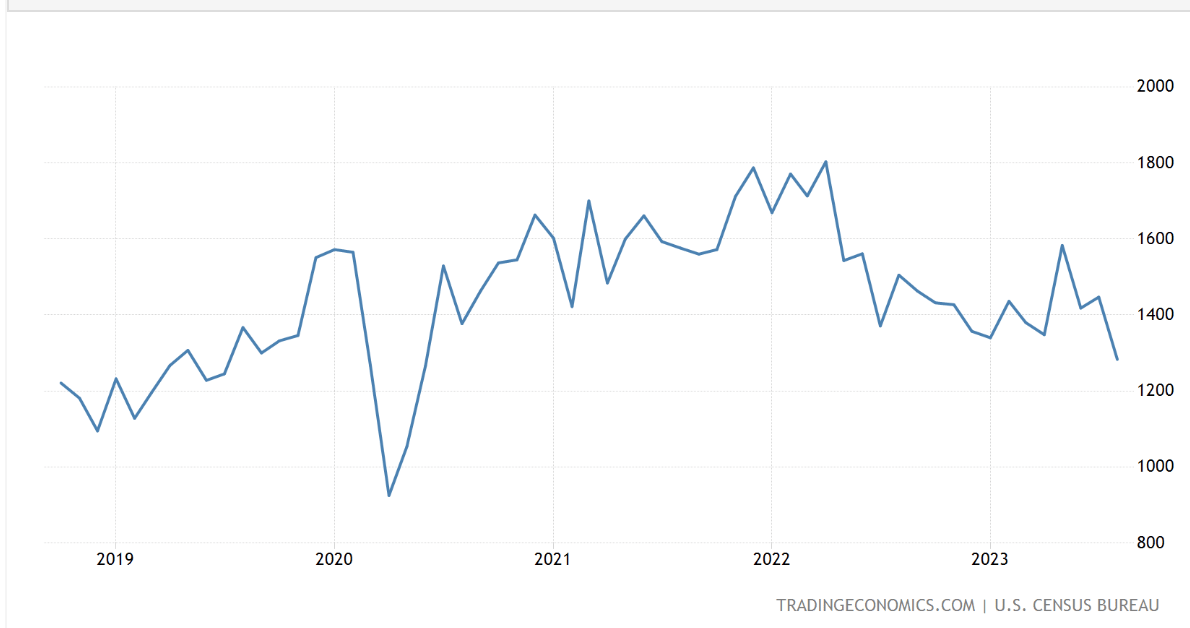

Recent data for Housing starts show that the downtrend started in 2022 and continues to head down. Till some of the factors mentioned above ease up, potential investors can expect the stock price to take a hit based on how bad it gets.

US Housing Starts (Trading Economics)

{kind=link}

In August 2023, housing construction activity in the United States took a notable downturn, marking an 11.3% month-over-month decline. This decline brought the seasonally adjusted annualized rate of new housing starts to 1.28 million, a level not seen since June 2020 and falling significantly short of the anticipated 1.44 million. Construction of single-family homes saw a decrease of 4.3% to 941K units, while multi-unit buildings of five or more units experienced a substantial 26.3% drop. Therefore, it is prudent that an investor considers the short-term risks associated with this stock.

Why is this a long-term hold?

1. Everything we have talked about so far has indicated strength from the company and the company will come out relatively stronger compared to its peers as we go through this economic cycle

2. Their vision means we can expect this company to grow quite well in the next decade

3. More importantly the long-term outlook is favorable due to Residential repair and remodeling taking a big role in their business (accounting for 45% of the annual sales in 2022) and will only get better going forward.

Demand conditions for repair and renovation have demonstrated a relatively lower degree of cyclicality compared to the residential new construction market. This is especially notable for exterior products that are exposed to environmental elements and involve maintenance that is less prone to extended deferral periods. The owners of existing homes that are discouraged by high interest rates may stay longer especially if they have secured a lower interest rate which could mean more repair and renovation.

The average age of housing stock in the United States has seen a notable increase in the median age which has advanced from 23 years in 1985 to 39 years in 2019. Furthermore, approximately 80 percent of the current housing inventory was constructed before 1999. The thinking is that the ongoing trend towards older homes, among the roughly 142 million existing residences in the country, will continue to propel the demand for repair and remodeling projects.

I believe over the longer term this stock will still be a winner going forward as this time it's different.

For further details see:

BlueLinx: This Time Looks Different