BXC - BlueLinx: Weathering The Lumber Market Storm

2023-08-02 05:15:02 ET

Summary

- BlueLinx Holdings missed analysts' estimates, causing a 7% premarket drop in the stock.

- Despite the miss, I see BlueLinx as a profitable company with a strong balance sheet and small capital return program.

- The current softness in the lumber market is cyclical, and lumber prices are expected to bounce back.

- While revenue growth rates have been challenging, H2 2023 is anticipated to show improvement as comparables become easier.

Investment Thesis

BlueLinx Holdings ( BXC ) missed analysts estimates on the top and bottom line and the stock is down premarket by around 7%. However, I don't believe this set of results is all that bad.

There's perhaps some commitment bias on my part, but when we look through BlueLinx we see a company that is clearly profitable, with a strong balance sheet, together with a small capital return program. Given how soft the lumber market has been in 2023 compared with 2022, I don't believe that this is the right point in time to call it a day on this stock.

The lumber market is cyclical and together with many other commodities, right now it's in the doldrums. But lumber prices will bounce back sooner or later, particularly if we see a soft landing in the economy. Stay the course with BXC.

Key Drivers for BlueLinx

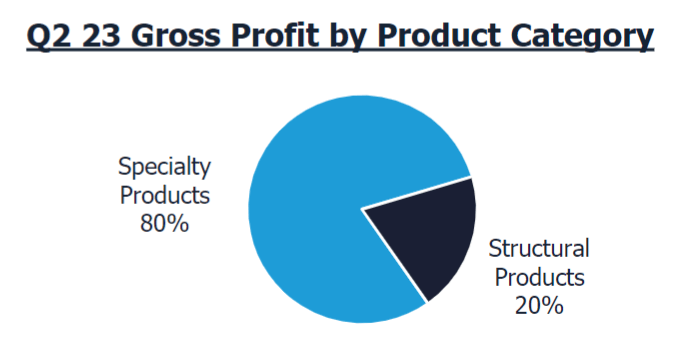

In the graphic that follows, we can see a breakdown of BlueLinx's gross profits by category. I believe this is helpful to provide readers with context.

{kind=link}

The bulk of BlueLinx's operations are tied to its Specialty Products, which include, products such as engineered wood, siding, and millwork.

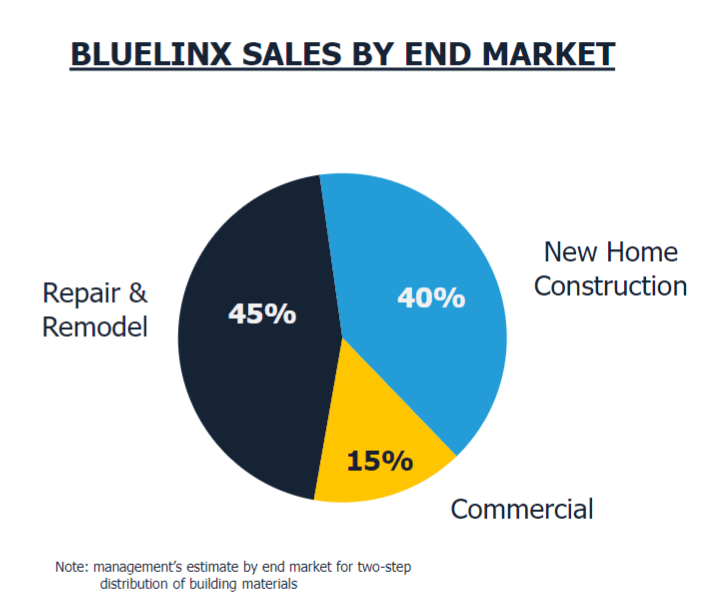

However, with approximately 40% of its revenues tied to new home construction, and with single-family housing starts falling during the first 6 months of 2023, there's little that BlueLinx could do to thrive in this quarter.

{kind=link}

What's more, as you'd expect, this far into the work-from-home period, any households that wanted to do any renovations on their property will to a large extent have already completed these projects. Meaning that there was little to stimulate lumber prices during Q2, and by extension BlueLinx's revenue growth rates.

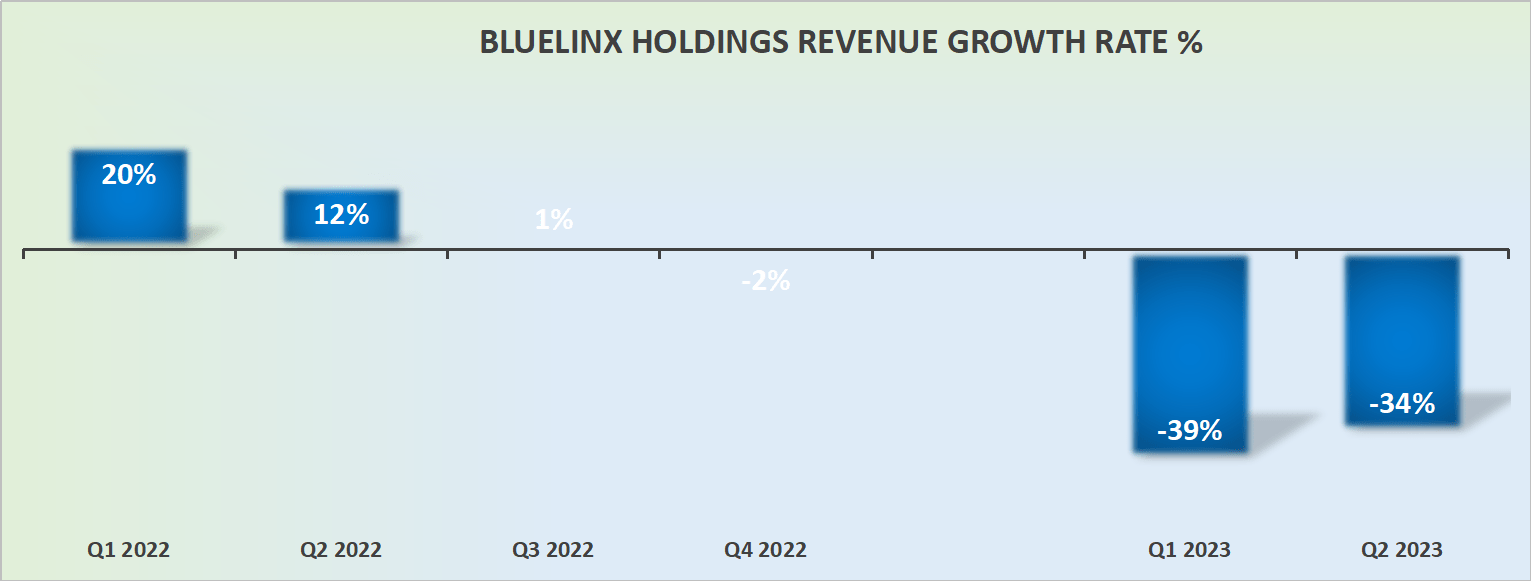

Revenue Growth Rates Struggle

{kind=link}

Anyone following the housing market will have been surprised by the dynamics that have unfolded this year. The housing market has remained a lot more resilient than many would have believed was possible at the start of the year.

That being said, this hasn't stopped BlueLinx from delivering two very negative back-to-back quarterly reports.

That being said, H2 2023 should see BlueLinx delivering slightly better revenue growth rates compared with H1 2023, as the y/y comparables become easier.

Profitability Profile Doesn't Entice Much

The guidance we are given thus far into Q3 looks unappetizing. For context, Q3 of last year saw its specialty products segment delivering 21% gross margins, while this time around its gross margins points to around 19% at the midpoint.

On the other hand, its structural products segment last year in Q3 reported 11%, while this time around it points to around 12% to 13%, an improvement of around 150 basis points at the midpoint.

However, given what we've already discussed above, the bulk of BlueLinx's gross profits are derived from its specialty products, meaning that any compression in that segment has an overreaching impact on BlueLinx's overall profitability.

Altogether, I suspect that around $2.90 of EPS could be on the cards for BlueLinx's upcoming Q3 period.

Meaning that for 2023, around $11 to $12 of EPS looks likely. This leaves this cyclical lumber company priced at approximately 8x this year's EPS. A figure that I don't believe is unreasonably stretched.

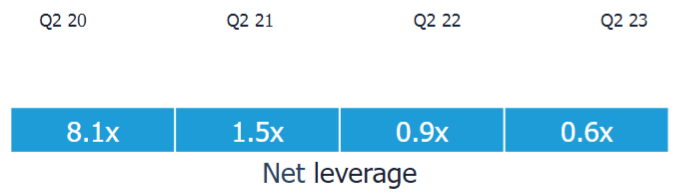

Particularly when we consider that BlueLinx's balance sheet is in a strong position with net leverage of 0.6x.

{kind=link}

As you can see above, BlueLinx's balance sheet is now at a multi-year low. This leaves this cash flow generating company very well positioned, despite overall weakness in lumber prices.

The Bottom Line

I don't consider these results to be all that bad. BlueLinx is a profitable company with a strong balance sheet and a small capital return program.

While the lumber market has been soft in 2023 compared to the previous year, it's important to remember that the lumber market is cyclical and prices will likely bounce back.

The bulk of BlueLinx's operations are tied to its Specialty Products. With approximately 40% of its revenues tied to new home construction and housing starts falling during the first half of 2023, revenue growth rates have been challenging.

However, H2 2023 is expected to show better revenue growth as the y/y comparables become easier. The profitability profile may not look enticing currently, but EPS for the upcoming Q3 period could be around $2.90, leading to a likely EPS range of $11 to $12 for the full year.

Considering the company's strong balance sheet with net leverage of 0.6x, BlueLinx is well positioned despite the weakness in lumber prices.

For further details see:

BlueLinx: Weathering The Lumber Market Storm