IHTA - BMN: A Defensive 5% Yielding Muni CEF

2023-11-15 12:08:25 ET

Summary

- BlackRock 2037 Municipal Target Term Trust is a target term fund with the objective of returning $25 at its termination date in 2037.

- The BMN closed-end fund is a defensive Muni CEF option owing to its lack of leverage (subject to change), duration profile and term structure.

- BMN has a decent chance of hitting its $25 NAV target in 2037.

In this article we discuss the BlackRock 2037 Municipal Target Term Trust (BMN) - a relatively new Municipal closed-end fund, or CEF. The fund trades at a 5% yield and an 8.2% discount.

Fund Snapshot

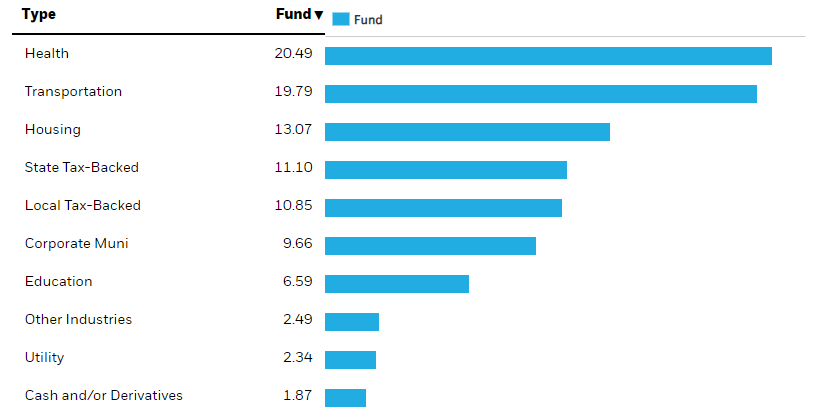

The BMN portfolio is allocated primarily to 15-20Y bonds, favoring revenue bonds over GO, i.e., general obligation bonds. Its sector overweights are Health and Transport.

{kind=link}

Its credit allocation is fairly typical, with around 20% in sub investment-grade and unrated bonds.

{kind=link}

It has a duration of 7.9, which is fairly modest within the CEF sector where many funds have double-digit duration. This is largely due to its lack of leverage.

It has a management fee of 0.55% - on the low side in the sector - with additional expenses of 0.17% for a total of 0.72%. The yield-to-worst of the portfolio is 5.2%.

Target Term Structure

The fund's allocation profile is not particularly unusual. What is unusual is its target term structure. Recall that a target term CEF is one that not only has an expected termination date but also hopes to return the original NAV to investors at termination.

Let's discuss these two features in turn. The basic attraction of a term CEF is that it can deliver discount amortization into the termination date. For example, a term CEF trading at a 5% discount which then terminates will deliver a 5% price gain relative to the NAV as the discount on termination has to be zero by definition.

The term structure leads to a lot of misconceptions, such as the view that the term CEF must terminate. The reality is very different. Specifically, a term CEF is not like a bond with a defined maturity.

As an investment vehicle, a term CEF can make decisions. One of these decisions is whether to terminate or not. Many CEFs that were term CEFs at inception continue to exist well past their term date such as DMO, BSL and many others. A fund whose management doesn't really want to terminate the fund can easily put an extension or a conversion to a perpetual fund to a shareholder vote as has been done in the past.

The basic rule of thumb that we follow is to assume that a Nuveen term CEF will likely either terminate or offer investors a tender offer at NAV - the same economic outcome. A term CEF that is not issued by Nuveen should not be assumed to terminate. Other managers such as Eaton Vance and Invesco have terminated their term CEFs, but this is a point where investors have to tread carefully with their assumptions.

Another important point which has come up recently is that a terminating fund could suffer NAV decay during the process of unwinding its portfolio. We saw this recently with the Invesco High Income 2023 Target Term Fund ( IHIT ). IHIT has a sister fund, Invesco High Income 2024 Target Term Fund (IHTA), which is very similar to IHIT but holds slightly longer-maturity assets. For this reason, IHTA has been a somewhat higher-beta CEF than IHIT.

However, as the chart below shows, IHIT's NAV collapsed relative to IHTA during its termination, which arguably cost it close to 10% in NAV. This is highly unusual as many other CEFs have terminated with very little, if any, additional cost. The likely reason for such a poor result for IHIT is its allocation to a fairly stressed and illiquid CMBS sector. A high-quality Municipal fund like BMN is unlikely to suffer a similar experience.

Systematic Income

Finally, it's worth highlighting how a target term CEF differs from a term CEF. A target term CEF hopes to deliver the fund's NAV at inception - $25 in case of BMN.

{kind=link}

This objective is a kind of hope rather than any legal mandate, of course. Given most of the bonds in the BMN portfolio will mature after the termination date, there is no certainty around whether or not the fund can hit the $25 target.

What will drive this are two factors: 1) its distribution relative to its underlying net yield; and 2) what happens to rates from now to its termination date. Its distribution on NAV of 4.7% is fairly modest, so after fees there shouldn't be much overdistribution, if any.

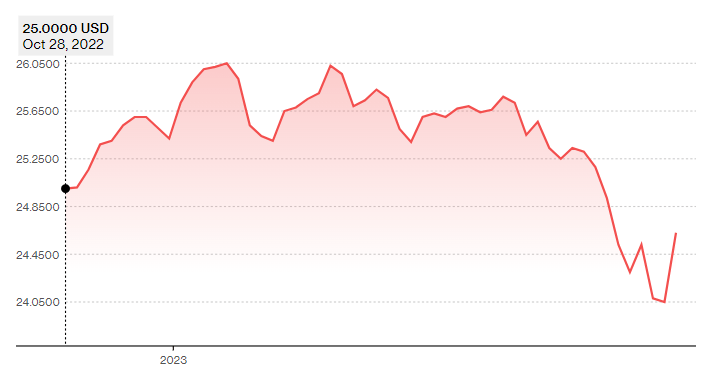

And as far as rates, the fund had good timing on the launch as Muni yields were not much below current levels and its NAV rose up to $26 early in 2023. Since then, however, rates have taken a toll and the NAV moved towards $24 before recovering somewhat in the latest bond rally.

At some point over the next 14 years, the Fed has a good chance of getting inflation down to 2%, at which point rates are unlikely to remain where they are which, together with its distribution, gives the fund a good shot at keeping the NAV around $25, barring credit losses.

Takeaways

Overall, BlackRock 2037 Municipal Target Term Trust is a fairly defensive option in the sector for several reasons. One, as a target term fund it is unlikely to reshuffle into longer-duration bonds as time goes on, meaning its duration will fall over time as its holdings get closer to maturity. Perpetual funds will tend to rotate into longer maturities over time to keep duration exposure within a range.

Two, it has no leverage at present. This will likely change given the prospectus talks about achieving leverage of up to 33% of total assets and using preferred shares within 6 months of launch. Since it's been a year since launch it's possible they reconsidered this and may carry on without leverage or add leverage only when it makes sense to do so, i.e., when the Muni yield curve re-steepens.

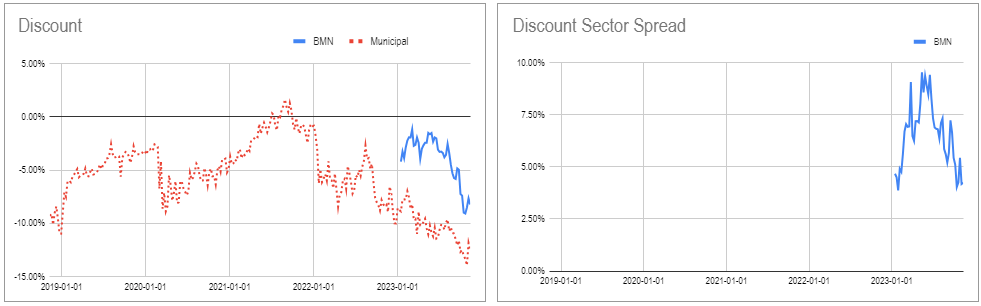

Three, as a target term fund, discount volatility will likely remain more constrained. We can already see this working already as the discount of the fund remains significantly tighter than the median fund.

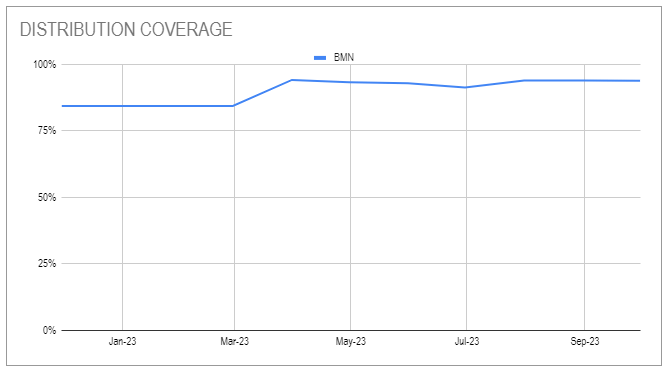

The fund's coverage is not miles from 100% and has been stable - driven by its lack of leverage and fixed-rate assets.

{kind=link}

While its discount is tighter than the sector average, this is normal for a term CEF. What's interesting is that the gap between its discount and the sector is relatively low - around 4% at present, which offers attractive upside / downside whatever happens with regard to its termination.

{kind=link}

For further details see:

BMN: A Defensive 5% Yielding Muni CEF