BYMOF - BMW: Strong Financial Results And EV Transition But No Growth Prospects

2023-09-14 11:54:04 ET

Summary

- BMW followed up the strong first quarter in 2023 with equally good Q2 results.

- Despite the publicly cautious approach regarding electric vehicles, BMW is a leader in the transition among established auto manufacturers.

- The new Neue Klasse line of electric vehicles looks like a very strong model line-up, but it will only be available in 2025.

- While valuation is low, there is no immediate catalyst for improvement, but patient investors can rely on a 7% dividend yield, and additional returns through buybacks.

- Still, the lack of growth despite billions of capital to be invested in the EV transformation does not warrant a Buy recommendation.

(Note: All amounts in the article are in EUR. At the current exchange rate 1 EUR is around 1.07 USD.)

Investment Thesis

BMW Group ( OTCPK:BAMXF , OTCPK:BMWYY ) achieved the best annual result in the history of the company in 2022 and reported strong Q1 numbers . BMW followed up with equally strong Q2 numbers on August 3. Profit before tax increased 8.3% YoY and deliveries were up 11.3% YoY.

I started my coverage of BMW in May this year. In my first article I gave a Hold rating and said that, while shares are undervalued, investors would need patience as there is no immediate catalyst for a price appreciation in sight. The risks that are keeping the valuation low - mainly the macroeconomic challenges and the uncertainty regarding the EV transformation - will likely stay for a while.

Since then, (ordinary) shares have depreciated by around 7%, and the forward-looking P/E ratio is now below 6 (based on the 2024 EPS consensus of 16.29). (Note - Besides the ordinary or common shares there are also preferred shares, but as I have explained in my first article, those are not a good choice, in my view.)

In addition to the strong financial results, there are some other positive things to note:

- While BMW Group still refuses to give an end date for its ICE production, the EV transition is going well. The share of all-electric vehicles in deliveries increased to 14.1% from 7.2% a year ago.

- Q2 deliveries in China were relatively strong and increased by 11% YoY. This is notable as the other two large German manufacturers, Volkswagen Group ( OTCPK:VWAGY ) and Mercedes ( OTCPK:MBGAF , OTCPK:MBGYY ) did much worse there. Especially Volkswagen is losing market share in China.

- BMW Group raised its full-year guidance for 2023, now expecting an EBIT margin in the Automotive segment between 9% and 10.5% (previously: 8-10%).

While you can certainly do worse than buy BMW shares, I am keeping my Hold recommendation. The Bull case mostly relies on a revaluation taking place and the P/E ratio going back to a value between 7 and 9 - which would be a nice upside. Also, the dividend yield is above 7%, and the dividend looks quite stable to me.

But I do not see a lot of growth potential or even ambition. With some outliers up and down, BMW deliveries have been quite stable around 2.5mn units over the last years, and we should not expect them to increase significantly going forward. It looks like BMW is reinventing itself for the EV age with the Neue Klasse line of electric vehicles, which should come out in 2025. However, the financial promise is mostly that EV production costs will be in line with ICE vehicles, so a continuation of what we have.

I still prefer its German peer and arch-rival Mercedes due to the more ambitious EV strategy and the focus on the luxury segment (I have laid this out in a separate article ).

Q2 2023 results

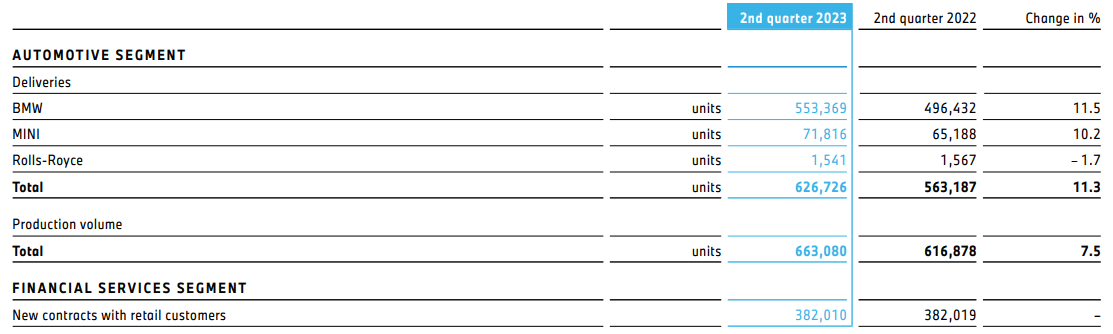

BMW followed up a strong first quarter with equally strong Q2 numbers. Profit before tax increased 8.3% YoY. Revenue was 37.219bn, up 7% YoY, and deliveries were up 11.3% YoY (+6% QoQ).

The increase in revenue was driven by higher volumes and pricing, as well as by the positive impact of currency exchange rates.

The automotive EBIT margin increased to 9.2%, up 100bps from 8.2% a year ago (but down from 12.1% in Q1 2023).

The EBT margin on the group level was 11.3%, unchanged YoY. This includes the Motorcycle segment (which is small compared to the Automotive segment, so that in any discussion on BMW Group financials the Motorcycle segment can be left out) and the Financial Services segment, which is sizeable. Income taxes were up 43% YoY, so EPS was only marginally higher YoY with EUR 4.39 per (common) share versus EUR 4.30 a year ago.

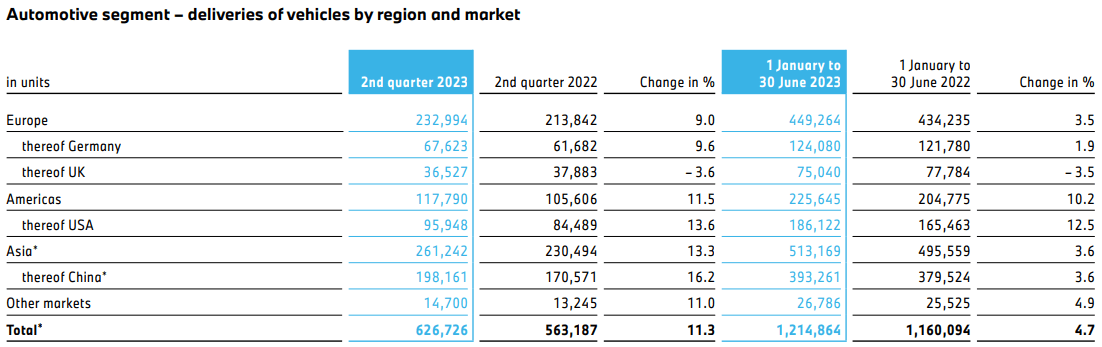

Deliveries were strong across all regions

Automotive deliveries were up 11.3% YoY to 626,726 units, while in Q1 they had been almost flat YoY with a nominal -1.5%. The positive development was visible in all regions, except the UK (which accounts for only a small part of sales).

Automotive deliveries 2nd quarter 2023 versus 2nd quarter 2022 (Source: BMW Group)

{kind=link}

The percentage increase was highest in China, which is notable as other German manufacturers are struggling there. China accounts for almost one-third of BMW automotive deliveries to customers. Across H1 11% of deliveries in China were fully electric vehicles, which is in line with the global ratio and much better than arch-rival Mercedes is doing with only 2.6%. (Note - BMW Group and Mercedes are not disclosing those numbers. The German newspaper Handelsblatt calculated them based on Chinese insurance registrations. BMW Group numbers include the MINI brand besides BMW.)

Last year, BMW took over its Chinese JV, with a significant one-time accounting profit of 8bn. But it made a long-term commitment with a production contract until 2040 (you can find more details on this in my previous article). So, it is good to see BMW do well in China.

Guidance for 2023 and beyond

BMW's guidance for the automotive EBIT margin is a conservative 8-10% - in line with the previous years.

The company changed the forecast for 2023 deliveries from " slight increase " to " solid increase " after the Q2 results. BMW does not give a target number. To me, this seems just an acknowledgment of the strong second quarter and not a promise of further increases. BMW's automotive deliveries have been around 2.5 million units per year for several years now (with some minor ups and downs), and it does not look like the company has the ambition to change this.

In general, I do have the impression that BMW's ambition is to keep things as they are. The upcoming Neue Klasse electric vehicles, despite the huge investment, can also be characterized from that perspective.

Neue Klasse and EV transformation

BMW recently presented the prototypes of its Neue Klasse line-up at the IFA in Munich. This is a matter of taste, but I think the cars look gorgeous, and I am pleased that they are immediately recognizable as BMWs. I deplore that nowadays most cars look very much the same, whether they are made in China, Europe, or elsewhere - but the Neue Klasse prototypes look like a modern tech version of BMW's groundbreaking cars from the 1960s and 1970s.

BMW Neue Klasse (Source: BMW Group)

{kind=link}

Unfortunately, the first Neue Klasse cars will not be delivered to customers before 2025. The specifications, like a range of 800 kilometers (497 miles), look best in class now. But they will likely not be that anymore in 2025. Mercedes, for example, talks about models with a range of 1000 kilometers.

A key promise of the Neue Klasse is that the cars will be at least as profitable for BMW as the current ICE models. BMW is one of the last holdouts among auto manufacturers and refuses to give a date for phasing out petrol and diesel. BMW CEO Oliver Zipse calls this technology openness. He criticizes in frequent interviews that the EV transformation is going too fast and says that BMW wants to keep its options, investing in electric vehicles, but also still in ICE models and hydrogen technology.

The reality though is that BMW is a front-runner regarding electric vehicles among established auto manufacturers. Arch-rival Mercedes wants to be fully electric in 2030, but in Q2 2023 the BEV share of deliveries was just 12% compared to 14.1% for BMW - and the gap is not closing, but widening: in Q1 2023 the numbers were 10.3% for Mercedes and 11% for BMW.

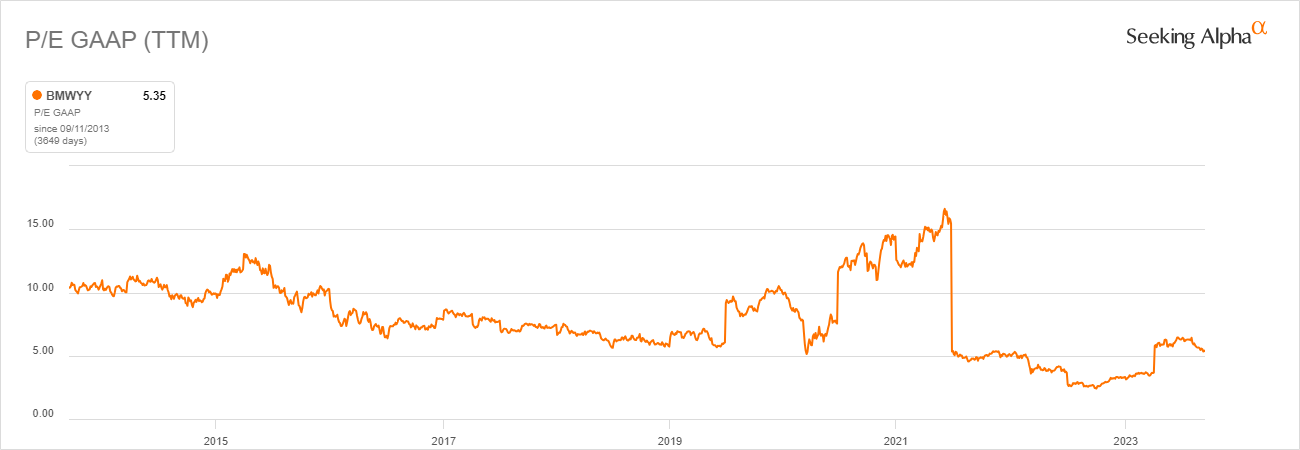

Valuation

BMW ordinary shares have a forward-looking P/E ratio under 6, based on the 2024 average EPS consensus of 16.29. Estimates range from 13.06 to 19.85 and have generally been revised upwards after BMW announced the Q2 2023 results.

This is not expensive and also below the historic average:

BMW Group GAAP P/E ratio (Source: Seeking Alpha)

{kind=link}

Of course, if you think that BMW profits will go down due to either macroeconomic conditions or the EV transformation, you could see this as a value trap. But I do not think so.

Like many other German companies, BMW has only one dividend payout per year, usually around April/May. This year the dividend was 8.50 euros per share, 2.70 euros more than in the previous year. 2022 profits had a one-time element because of the consolidation of the Chinese JV, but I expect at least 7 euros for 2023, so at the current share price, the yield would be around 7.3%.

BMW Group completed a share buy-back program in June with a total value of 2bn euros (3.63% of the capital) and started a new one with the same volume, which is scheduled to run until 2025. So we are looking at a nice annual shareholder return of around 9-10% from dividends and buy-backs, in addition to the low valuation.

BMW is therefore not a bad stock to hold. But I assume it will trade sideways in a range between 90 and 120 euros. Currently, I do not see a runway above that. If BMW could demonstrate that it can grow unit sales and keep profit margins at least stable, that would change my mind.

Balance sheet and debt

One topic that I did not cover in my previous article, is the question of BMW's debt. BMW Group features on some lists of the most indebted companies in the world, as do other auto manufacturers with a large financial services segment. This is nonsense as the debt is in the financial services segment, and banks do have a lot of debt. This is their business. The larger a bank, the more debt it has.

The topic also regularly comes up in the comments section here on Seeking Alpha and I have covered this in an article on Volkswagen in more detail. Most of what I am saying there about Volkswagen also applies to BMW.

Through BMW Bank, BMW owns a banking license in Germany. More than 1/2 of its deliveries to customers are financed by the Financial Services segment, which contributes almost 1/5 to the total group profits.

BMW Group KPIs (Source: BMW Group)

{kind=link}

The Automotive segment itself is debt-free and has financial assets of more than 18bn euros.

BMW Group debt in the Automotive segment (Source: BMW Group)

Risks

The ability of BMW Group to execute the transition to electric vehicles is an obvious risk that needs mentioning. However, I do think this is priced in, and as I have said, BMW is doing well here in my view.

BMW is also doing much better than its German peers in China. But with China accounting for around 30% of deliveries, anything bad that happens there will significantly affect the company.

There has also been a lot of talk recently about Chinese manufacturers gearing up in Europe, and specifically Germany which is a key market for BMW. I think it is not hard to imagine a world where Germans also are sitting in Chinese cars like the Chinese are sitting in German cars now. While I do not think this is a major concern for the likes of BMW and Mercedes with their focus on the premium and luxury segments, it is a headwind for future growth. The lack of significant growth potential is what makes me stay with a Hold recommendation despite the good financial results.

Conclusion

As I said in my last article, I think that BMW will come out fine through the EV transformation. BMW shares have a low valuation, but I am keeping my Hold recommendation. The Bull case mostly relies on the valuation going back to historic averages and does not rest on financial improvements on the company side. For a Buy recommendation, more would be needed here - in my view - than to keep the status quo after billions of capital investments into the EV transformation.

For further details see:

BMW: Strong Financial Results And EV Transition, But No Growth Prospects