BNPQF - BNP Paribas: A So-So Q3 Won't Help The Shares

2023-10-27 05:35:15 ET

Summary

- BNP Paribas shares have been pretty flat since my last update just under a year ago, becoming slightly cheaper relative to tangible book value in the process.

- Q3 wasn't a great quarter for the bank. The French retail segment looked particularly weak, though there was an overall bottom line beat driven by lower levels of provisioning.

- The bank remains on course to meet the targets set out in its 2025 strategic plan. Trading at a little over 0.6x tangible book value, its stock remains cheap.

This has been a frustrating year for BNP Paribas ( BNPQY )( BNPQF ) shareholders. The French banking giant continues to tick along as it typically does, yet there is a strong sense that its shares aren't getting the multiple they deserve from the market. Performance since my last update around a year ago sums things up well. Roughly flat in share price, these shares have returned around 8% despite a circa 15% rise in nine-month EPS and 9% year-over-year growth in tangible book value per share. Multiple expansion was a part of my 'Buy' case last time out, so the implied de-rating is clearly a disappointment.

Q3 results won't improve sentiment. Indeed, the shares finished the day 2.6% lower in Paris trading, with the market's negative reaction contributing a large amount to the fairly lackluster returns outlined above. Results actually weren't that bad in terms of the key P&L lines – they were about in line with what analysts had pencilled in – but beneath the surface there were some disappointing numbers, particularly in its domestic retail banking and consumer finance segments. A bottom line beat driven by provisioning is likewise not going to do much for the shares.

Despite some soft notes, the sell-off means that these shares are now largely unmoved versus last time out. Given that implies an even cheaper valuation, I continue to view the bank as undervalued.

A So-So Third Quarter

BNP Paribas released Q3 results early on Thursday. The shares fell around 6% at the open, recovering to finish 2.6% lower at the closing bell.

The main P&L lines were largely in line or slightly above consensus, with revenue (€11.6 billion, up 4% year-on-year), pre-provision income (€4.5 billion, up 5% year-on-year) and return on tangible equity (12.7%, up 130bps year-on-year) not immediately jumping off the page in a bad way. However, beneath the surface there were definitely some soft notes. Global Markets came in on the weak side against a tough comp, with revenue (€1.8 billion) down around 9% year-on-year and operating income (€639 million) down 25%. Global macro trading was the main driver of that, as fixed income, commodities and currency revenue (€1.0 billion)("FICC") fell around 11% year-on-year (Fig 1). That isn't bad relative to European peers like Barclays ( BCS ) (Q3 FICC revenue down 26% YoY), but it does stack up poorly to numbers put out by the big U.S. banks like Bank of America ( BAC ) (Q3 FICC revenue up 6% YoY).

Fig 1. (Data Source: BNP Paribas Quarterly Results Releases) Fig 2. (Data Source: BNP Paribas Quarterly Results Releases) Fig 3. (Data Source: BNP Paribas Quarterly Results Releases)

Of slightly more concern was performance in CPBF, its French retail banking segment. CPBF revenue (€1.6 billion) was down around 3% year-on-year and 7% sequentially. Net interest income (€834 million) was particularly weak, falling 6% year-on-year and 9% sequentially, with that driving a circa 20% year-on-year decline in pre-tax income (Fig 2). French current account balances were down 24% year-on-year to €130.1 billion. Results in its other retail segments, which include other Eurozone markets like Italy, Belgium and Luxembourg, also back up the ongoing theme from European banks that profits have now peaked. The Specialised Business segment (mainly personal finance and auto/equipment leasing) also looked somewhat weak this quarter, with revenue (€2.5 billion) down around €100 million sequentially and higher provisioning expenses eating into profit (Fig 3).

At the group level, reported net income (€2.66 billion) was actually a shade higher than consensus, though it was driven entirely at the provisioning line and that isn't going to earn the stock much kudos. Cost of risk was €734 million, which at around 33bps of total loans remains below management's 40bps medium-term benchmark. Non-performing loans remained flat versus a year ago (~1.7% of total loans), with the bank sitting on a stage 3 coverage ratio of around 70% plus a stock of €5 billion in stage 1 and 2 provisions.

Shares Remain Cheap Relative To Tangible Book Value

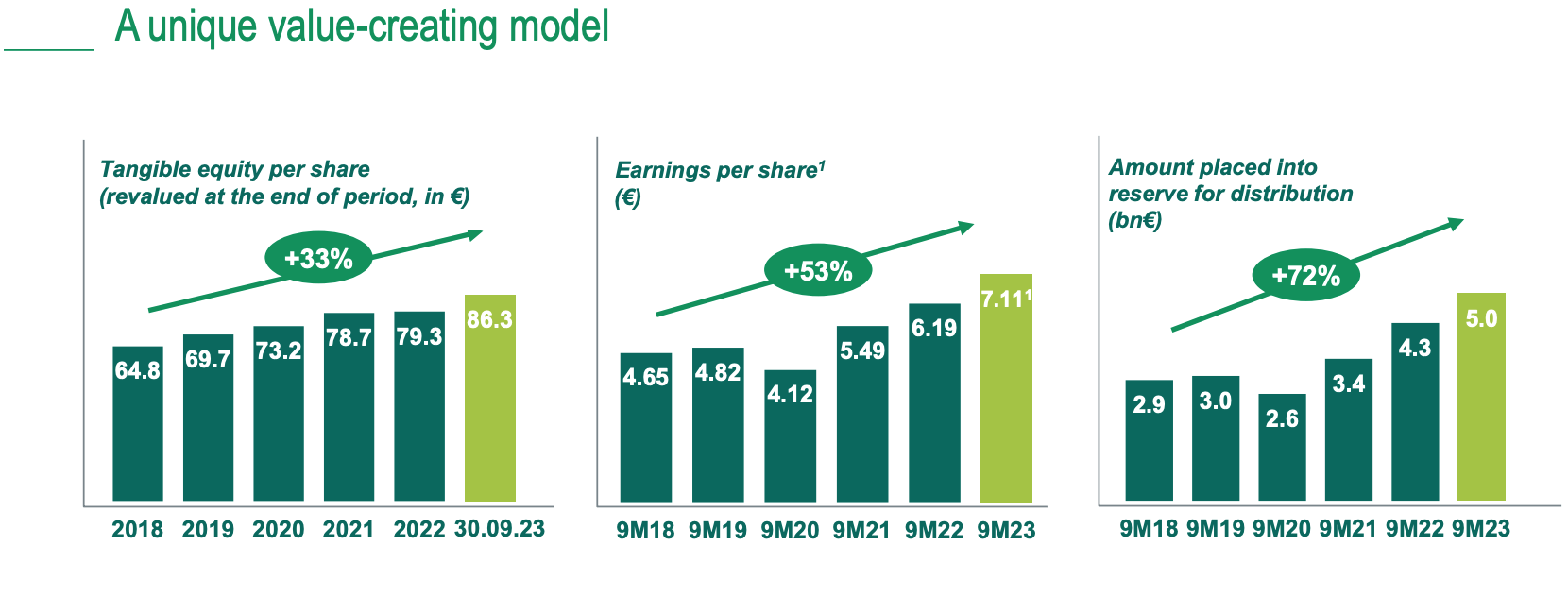

Cheap-looking European banks are not in short supply right now, and I would not exclude BNP from that category despite a very mixed quarter. The shares closed out the day at €54.72 in Paris trading ($ 28.74 per 'BNPQY' ADS), roughly the level they were at when I covered them in Q4 of last year. Tangible book value per share ("TBVPS") has increased by around 9% in that time to €86.30 (~$40.99 per 'BNPQY' ADS), meaning these shares have actually become cheaper on a P/TBVPS basis. They trade at just 7.7x 9M'23 EPS.

Fig 4. (Source: BNP Paribas Q3 2023 Results Presentation)

{kind=link}

The bank's return on tangible equity isn't stellar at this point in the cycle, but it is still comfortably above 10%. I would also note that BNP Paribas is probably one of the least interest rate sensitive names in its peer group. If you view the current Eurozone interest rate environment as unsustainable, which current market valuations of European banks seem to imply, then this may be a name to consider.

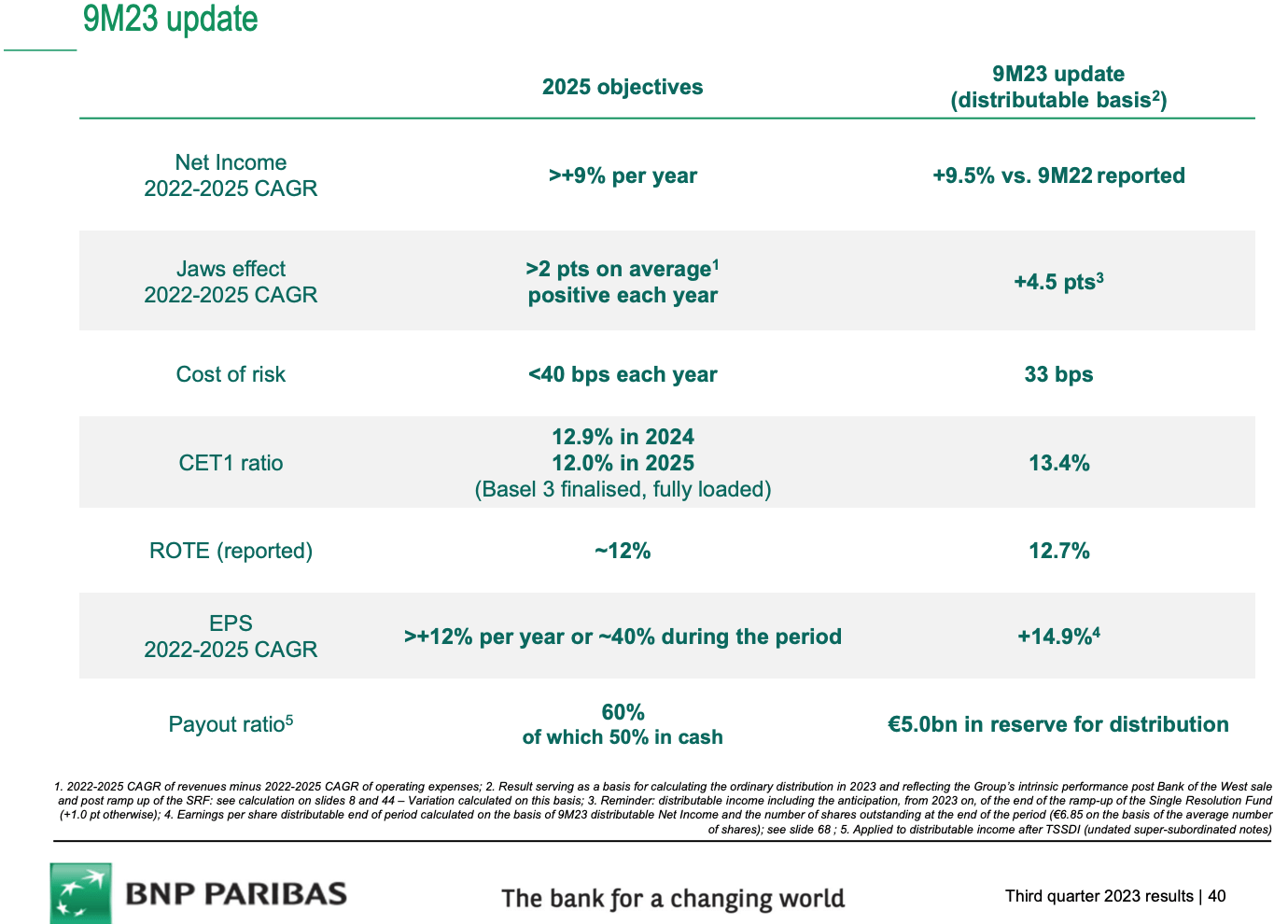

Regardless, BNP Paribas remains on track to meet the goals set out in its 2025 strategic plan. These include 9% per annum net income growth (relative to a 2022 base), 12%-plus per annum EPS growth and a 2025 reported ROTE of approximately 12%. Cost of risk is still seen below 40bps in each year, unchanged from last time.

Fig 5. (Source: BNP Paribas Q3 2023 Results Presentation)

{kind=link}

Given the above, quick math implies 2025 TBVPS of around €91.25. I maintain the view from previous coverage that a 0.9x multiple is pretty undemanding given the bank's through-the-cycle ROTE profile, and that gets me to a 2025 price target of around €82 per share ($ 43.28 per ADS) . Capital returns are guided at 60% of net income, of which 50ppt is allocated to the annual dividend. Even on a flat multiple of TBVPS (~0.63x currently), that would be good for circa 13% annual returns over the next couple of years, with the share price tracking TBVPS growth and dividends growing in line with EPS. A mixed bag of results in Q3 hasn't helped the investment case here, but BNP Paribas shares remain attractively valued, and I affirm my previous 'Buy' rating.

For further details see:

BNP Paribas: A So-So Q3 Won't Help The Shares