BNPQF - BNP Paribas: We See Light And Shadow

2023-11-16 06:44:19 ET

Summary

- 2025 targets maintained, and BNP Paribas is on track on its targets.

- 85% of its €5 billion buyback program completed with CET1 ratio declining by 20 basis points.

- Higher operating cost and a lower cost of risk. There was a slowdown in top-line momentum, but the bank is still attractive in yield and tangible book value growth.

Our readers know we have a good grip on the EU banking sector. Following Intesa Sanpaolo's (ISNPY) Q3 results comment , we are back analyzing BNP Paribas today (BNPQF)(BNPQY). Cross-checking our banking estimates, we believe that BNP Paribas is lagging behind the sector. Post Q3 results, we decided to lower the Group target price (maintaining a buy rating estimate), and we also provided additional supportive comments to mitigate medium-term headwinds.

Q3 Results and Changes in Estimates

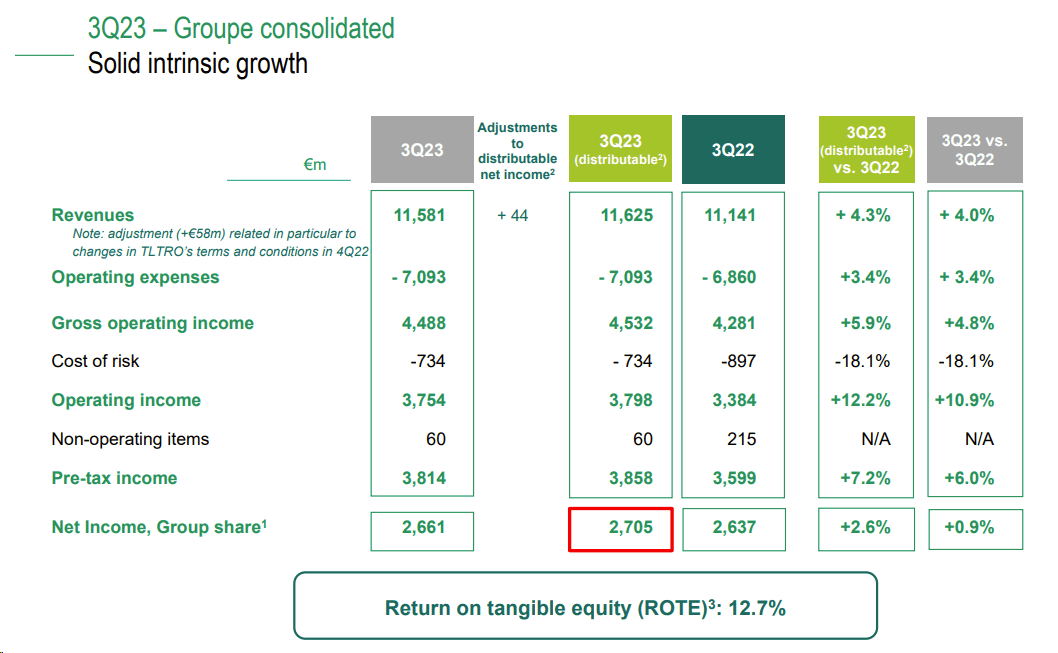

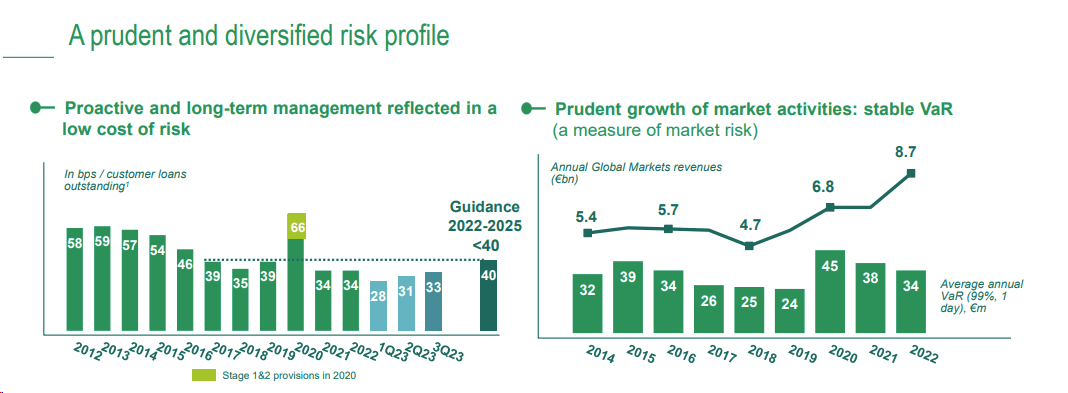

Q3 revenues exceeded consensus expectations and increased by 4% to €11.58 billion (Visible Alpha numbers were at €11.55 billion). More specifically, revenues from trading decreased by over 9%, while those from FICC (fixed income, currencies, and raw materials) fell by 14.3%. However, most of the BNP division showed a slowdown in sales momentum, but the hit from French retail banking was the negative outlier in the quarter and surprised our team. The division reported a 20% decline in net profits, with a loan volume in retail banking almost flat on a quarter-to-quarter basis. After the Q&A session, the company is confident that revenue growth will be sustained in the upcoming quarters. However, we feel the 2023 loan result is lower than previously estimated, and for this reason, we are taking down our internal 2024 forecast. In number, net interest income was down by 6%. In addition, the bank costs increased by 3.4% to €7.09 billion yearly. Going down to the P&L account, the bank's net profit fell 4% year-on-year to €2.66 billion and was also below the consensus estimate of €2.72 billion. On a positive note, the bank credit losses reached €734 million (Fig 2) and were 10% below consensus with a cost of risk at 33 basis points (higher than ISP, which got 28 basis points). Looking at BNP (the Italian branch), the division recorded an intermediation margin up 1.2% to €660 million, with an interest margin growing by 4.2%. This was supported by stability on margin deposits, partly counterbalanced by increased refinancing costs.

BNP Paribas Q3 Financials in a Snap

{kind=link}

Source: BNP Paribas Q3 results presentatio n - Fig 1

{kind=link}

Fig 2

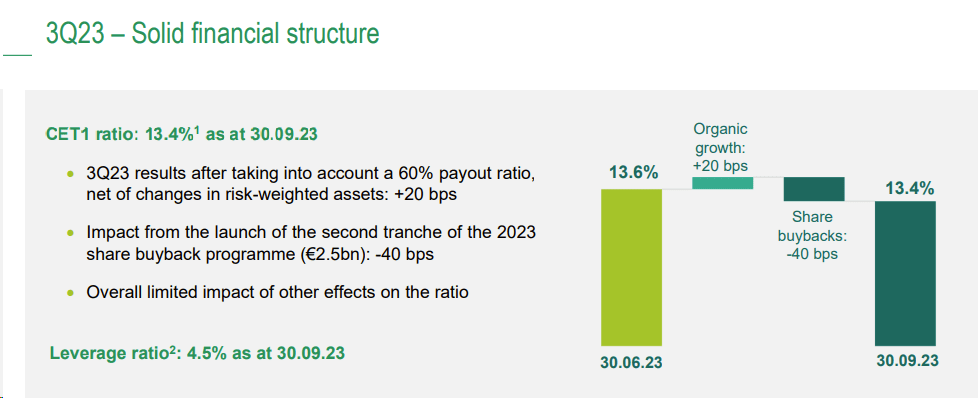

Furthermore, on the capital front, as of September-end, BNP Paribas' CET 1 ratio reached 13.4%, ten basis points lower than expected and down twenty basis points compared to the previous quarter. Including dividend accrued and profit of the period, there is a change in risk-weighted assets, which led to an increase of 20 basis points in the CET 1 ratio evolution (Fig 3). The ongoing buyback offset this. In detail, purchases of treasury shares were a negative detractor from the CET1 waterfall analysis and signed a minus 40 basis point. At the Lab, we were surprised that the bank has already completed over 85% of its €5 billion program. This is equivalent to around 7% of its market capitalization. As a reminder, proceeds from the sale of Bank of the West, BNP's former US retail subsidiary, entirely financed the operation. BNP's leverage ratio was flat at 4.5%, and the liquidity coverage ratio reached 138%.

{kind=link}

Fig 3

Levers to pull to mitigate headwinds and Valuation

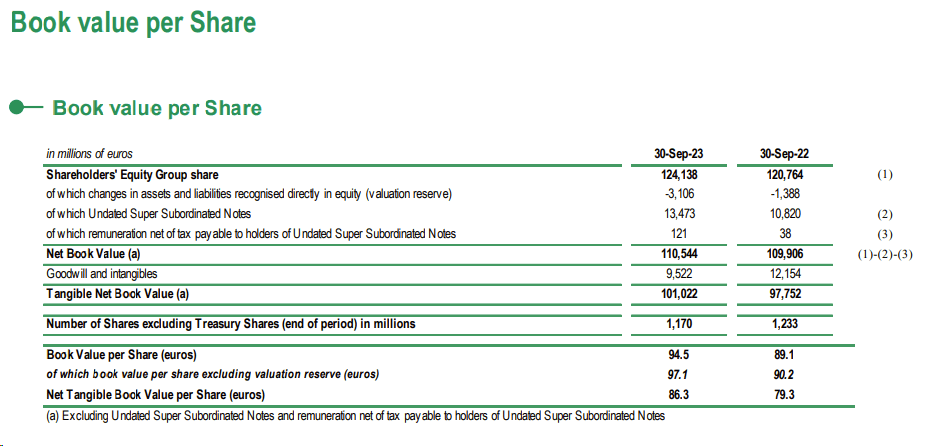

Post Q3 and in line with the management indication, we estimate a cost-saving target of 2%, and we forecast a loan loss at 33 basis points (below the 40 basis points target by the management). This is a supportive factor that will likely favor BNP Paribas' earnings. Here at the Lab, we anticipate a CET 1 ratio of 13.4% in 2024. This leaves the bank ample space for capital distributions. BNP is a solid institution, and the management reiterated a payout of 60% on profit. There is also €5 billion in reserves available for distribution. BNP already canceled 70 million shares or approximately 7% of its share capital in the year. Looking at the net income evolution, we now forecast a DPS of €4.6/4.7/5.3 in 2023/2024/2025. Therefore, we predicted a dividend yield of 8%, and including a potential buyback, we arrived at a total yield of 10%. Weaker revenues negatively impacted our internal estimates and price target, down from €80 to €75 per share. BNP Paribas recorded solid profits, and we appreciated the lower cost of risks. In addition, we positively forecast a tangible book value growth estimated at 8% per year until 2025. The specialized business division with Arval & leasing Solution and Wealth Management strength supports this. Still, we believe these numbers are insufficient to justify a higher target price as we performed in Intesa Sanpaolo. In numbers, the bank is on track to reach 1 billion more in profit vs. the 2022 results vs. players that already achieved €2 billion in higher net profit in the 9M.

Intesa Sanpaolo net income evolution

{kind=link}

Source: Intesa Sanpaolo Q3 results

The company is also well positioned to achieve the 2025 objective with a net profit up 9.5% annually compared to over +9% of the yearly target and RoTE at 12.7% compared to a target of over 12%. The bank is tracking ahead of its targets, but other banks offer a better entry point with better yield and capital upside opportunity. Regarding the target price, the leading French bank is trading at 0.65x of tangible book value with a 2024 EPS of 6.0x vs. a European bank average of 0.8 P/TB and a P/E of 6.4x. Even applying conservative estimates and considering a TBV up by 8% for 2024, BNP is still a buy, and valuing the bank in line with EU peers, we arrive at a €75 target price (down from €80 per share ).

BNP Paribas Book value per share

{kind=link}

Fig 4

For further details see:

BNP Paribas: We See Light And Shadow