NOA - Bonhoeffer Capital - North American Construction Group: Awash With Competitive Advantages And Barriers To Entry

2023-12-29 05:00:00 ET

Summary

- North American Construction Group is a construction services firm that provides heavy civil and bulk earthmoving services in supply-constrained markets.

- NAC has experienced significant growth in equipment utilization, return on invested capital (RoIC), and return on equity (RoE) over the past decade.

- The company has a strong competitive advantage in the industry, with a large equipment fleet, indigenous partnerships, and a contracted backlog of $3.0 billion.

The following segment was excerpted from this fund letter.

North American Construction Group (NOA)

North American Construction is a construction services firm that provides heavy civil and bulk earthmoving and project and mine site operations services in supply-constrained markets. NAC is typically the first contractor in and the last contractor out of project and mine sites. NAC has over 3,500 employees and over 900 pieces of equipment in its fleet operating at 30 sites. The fleet has a replacement value of over $2 billion.

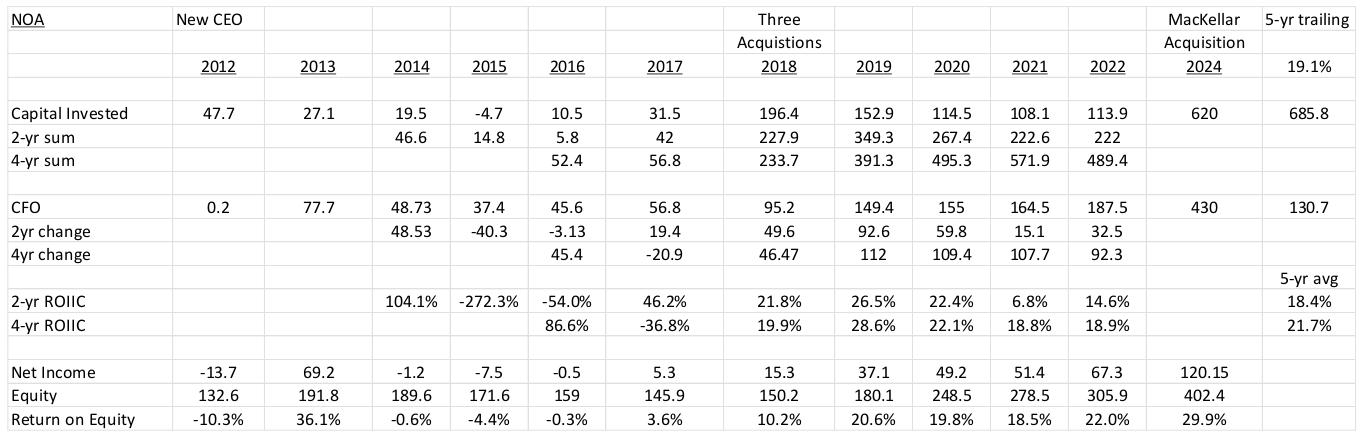

NAC was founded in 1953 as a civil construction firm. NAC has provided earthmoving services in Canada since the 1950s, in the oil sands since the 1970s, and for resources firms since the 1980s. NAC was sold to a private equity firm in 2003 and went public in Canada in 2006. A new CEO, Martin Ferron, was appointed in 2012. His goal was to increase geographic and service offering diversification and to increase return on invested capital (RoIC). In 2012, NAC sold its lower-returning and more cyclical divisions providing pipeline construction and piling-related construction, while retaining its oil sands earthworks business. Later in the 2010s, via acquisitions and partnerships with First Nations and other aboriginal groups, NAC expanded its service offerings and its geographic footprint to other geographies such as the US and Australia. Most of NAC’s invested capital is in large dump trucks and other earthmoving equipment. If NAC could maximize fixed asset utilization, then ROIC would increase. An economies of scale in purchasing and maintenance moat was created by having a highly utilized large fixed asset fleet in remote geographic locations with harsh conditions. Since 2015, equipment utilization has increased from an average of 40%, to 61% in 2023. NAC has a target goal of 75% to 85% by 2024. Since 2012, NAC’s RoIC has increased from -12% to 12%, with a current goal of 15%; and its return on equity has increased from -10% to 22%.

Beginning in 2018, management acquired businesses to expand NAC’s geographic reach, scale, and functional capability (including equipment repair services). From 2018 to 2022, NAC acquired five firms that increased the firm’s equipment utilization from 46% to 61% by 2023. The return on equity also increased to the 20%s from single-digits before 2018, and free cash flow conversion increased from breakeven to almost 40% in 2022. The business acquisitions were financed primarily by debt, which was paid down from cash flow generated from the acquired firms. Over the past five years, management has acquired six firms—three in mining services and three in equipment maintenance. The resulting unlevered RoIIC (see calculation below) has been around 19%, which includes returns from both organic growth initiatives and acquisitions.

NAC has four levers for cash flow growth: 1) buying a firm in their core or adjacent market; 2) expanding within existing markets; 3) paying down debt; and 4) distributing excess cash as dividends or buying back shares. The acquired firms generate cash flows in excess of what is needed to modestly grow the firm, which are used to purchase firms in its target or adjacent markets. If no firms can be found that meet management’s operational and valuation criteria, then management will buy back shares, as the shares have typically traded at modest valuations reflecting modest organic growth. NAC currently spends about 60% of operational cash flow on capital expenditures, leaving 40% for buy-backs and mergers and acquisitions. As NAC continues to grow, free cash flow conversion should increase.

The business sector in which NAC competes is subject to economies of scale from purchasing, maintaining, and selling of equipment and have route density characteristics in the provision of earthmoving and other mining services. NAC’s recent acquisition of an Australian firm should expand these economies of scale to Australia.

Earthmoving and Mining Services

NAC competes in the earthmoving and mining services markets in Canada, the United States, and Australia. NAC’s services are provided to four markets. First, NAC provides earthmoving services in the oil sands region to five large investment-grade clients which generated 50% of NAC’s 2022 operating income. In the oil sands region, as the largest third-party services provides, NAC moves about 7% of the total volume, so the earthmoving TAM is still quite large in the oil sands. The majority of the remaining earthmoving is provided by in-house operations. Oil sands operations are expected to have a remaining life of 50 years.

Second, NAC provides services to other mining and construction operations in Canada which generated 30% of NAC’s 2022 operating income. Canada currently has 200 operating mines, with an average remaining mine life of about 20 years. About 125 mines are expected to open in Canada over the next 10 years.

Third, NAC provides civil construction services and US mining services which generated 20% of NAC’s 2022 operating income. This includes the Fargo-Moorehead river flood diversion project. NAC is a joint venture partner with D&B, an international construction firm. NAC is planning on bidding with its joint venture partner on future projects in Australia.

Finally, with the purchase of MacKellar, NAC provides earthmoving and mining services in Australia. MacKellar will add an additional 40% to NAC’s operating income. MacKellar provides additional geographic and mining end-market diversification, adding to coal mining exposure, as well as new end markets such as gold mining. MacKellar was purchased for C$395m and was financed by internal cash and new debt, as well as vendor financing. The purchase price was about 2.75x expected EBITDA.

Mining and civil construction demand is driven by mega-projects, which have become more numerous due to increased commodity and energy demand and US, Canadian, and Australian government infrastructure spending. Oil sands production has increased over the past 10 years and is expected to continue to grow as new pipelines are completed in British Columbia. Electric vehicles and the electrification infrastructure is expected to boost metals and mineral demand over the next decade. NAC is expected to have a project backlog of $3.0 billion by year-end 2023. This is over three years of projected run-rate revenues.

NAC has three competitive advantages. First, NAC is the low-cost operator of earthmoving equipment. 90% of equipment maintenance is performed in-house and NAC provides maintenance services to third parties. NAC also rebuilds equipment components and has access to low-cost components. NAC has 14 equipment bays, providing over 170,000 square feet of maintenance and rebuild capacity. Over 50% of NAC’s equipment has telematics capabilities, which increase fleet efficiency. Second, NAC has indigenous partnerships, which generate over 90% of the projects in NAC’s pipeline. Finally, NAC has a large contracted backlog of $3.0 billion.

NAC also has many barriers to entry including:

- the scale/cost of NAC’s equipment fleet, the largest in North America, provides purchasing and maintenance cost advantages;

- one of the largest equipment maintenance capabilities in North America, which provides cost advantages and third-party equipment maintenance opportunities;

- indigenous partnership opportunities, which are limited in number (NAC has two) and are required to be competitive on many Canadian large earthmoving/mining projects;

- harsh operating environments where NAC’s services are provided reduces the number of profitable scaled competitors for available projects; and

- in the medium term, long lead times and scarcity of new equipment.

As described above, organic growth in these segments is expected to be 7% annual growth rate [1] with any other growth coming from identified growth projects, acquisitions, or share repurchases.

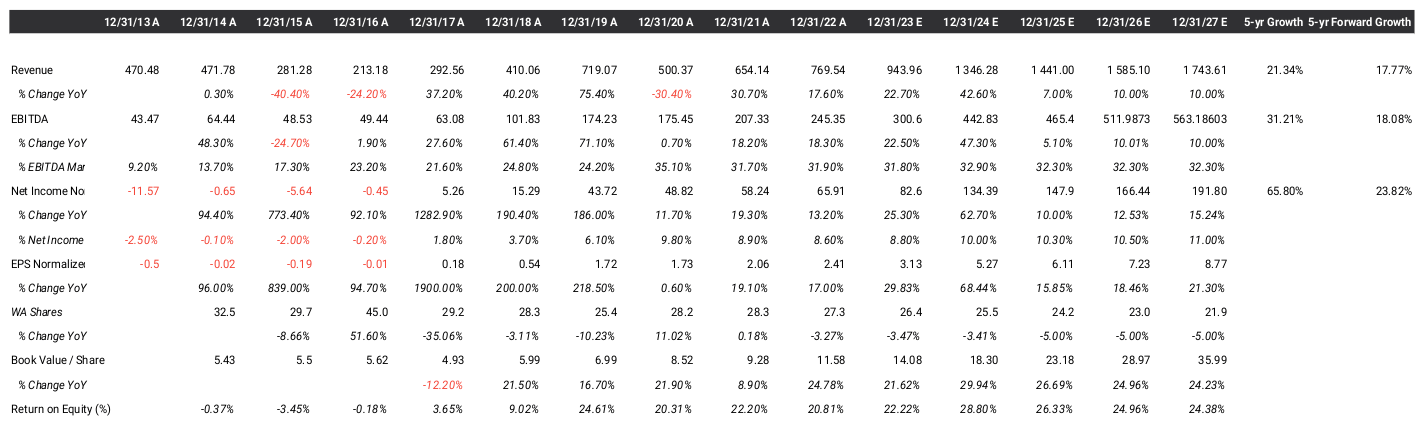

NAC operations have become better over time, as Martin Ferron and then Joe Lambert implemented a value-added acquisition strategy utilizing economies of scope and operations density and increased the efficiency of the core earthmoving operations. The return on equity has increased from about breakeven in 2014 to 2017, to 22% in 2022 and is expected to increase to 30% by 2024 with the purchase of MacKellar. Free cash flow conversion also increased from break-even in 2014-2017, to about 40% in 2022. The drivers included increases in net income margins from 5.2% in 2017, to 9.4% in 2022, and increases in asset turnover from 0.76x in 2017, to 0.86x in 2022. Leverage also declined from 2.2x to 1.8x EBITDA.

The incremental return on invested capital over the past five years is close to 20%, which has increased NAC’s RoIC over the past five years. See the calculations below.

{kind=link}

Downside Protection

NAC’s risks include both operational leverage and financial leverage. Operational leverage is based upon the fixed vs. variable costs of the operations. There are some moderate economies of scale in terms of purchasing and maintenance and local economies of scale, as the business is primarily clustered in the oil sands region of Alberta, the mining regions of the Northwest Territories, Nunavut, and Western Australia and Queensland.

Financial leverage can be measured by the debt/EBITDA ratio. NAC has an average net debt/EBITDA of 2.0 versus other earthmoving contractors (like Aecon, Badger Infrastructure Solutions, Bird Construction, Granite Construction, and Sterling Infrastructure) and versus NAC’s history. The history and projected financial performance for NAC is illustrated below.

{kind=link}

Management and Incentives

NAC’s management team has developed an M&A engine and an operationally efficient firm in profitable niches of the earthmoving and mine management industry. They perform M&A when targets are available at the right prices partially financed by debt, pay down debt, and return capital via buybacks when there are not opportunities to invest organically or via M&A.

The base compensation for the management team (the top five officers) ranges from C$2.1 million per year for the CEO to C$600k per year for the VP of HR. Over the past year, the top five management folks’ total compensation was about C$5.4m per year—about 5% of net income per year. The CEO and the chairman of the board (the previous CEO) currently hold 2.79 million shares and options (worth C$60.1 million), which is more than 30 times their 2022 salaries and bonuses. The CEO’s compensation is structured to include a C$575k base pay and up to a C$1.5 million performance bonus. Short-term management incentive pay is based upon meeting stretch EBIT and EBIDA targets and is paid in cash. Long-term management incentive paid in RSUs has two parts: 40% time-based and 60% performance-based vesting. The performance-based vesting is based upon relative total shareholder return (TSR) to a peer group and three-year target EBIT, free cash flow, and return on invested capital.

Board members have a significant investment in NAC. Martin Ferron, who was the previous CEO, owns 2.4 million shares, and the board owns 3.15 million shares, about 12% of shares outstanding. Option grants, provided to management and employees, were equal to 1.7% per year of the shares outstanding over the past three years.

Valuation

{kind=link}

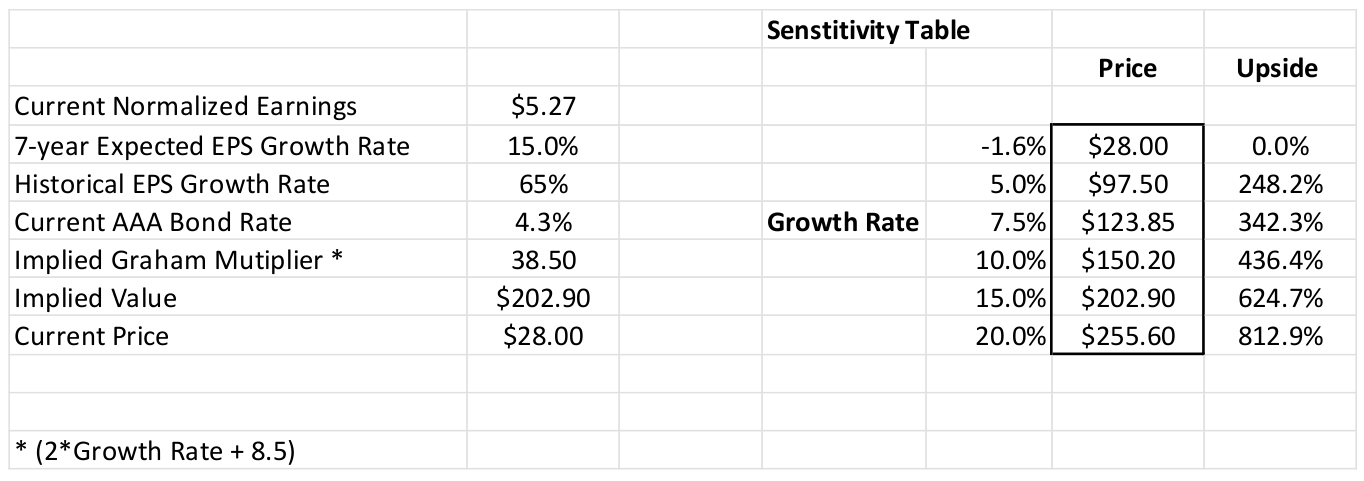

The key to the valuation of NAC is the expected growth rate. The current valuation implies an earnings/FCF increase of -1.6% in perpetuity using the Graham formula ((8.5 + 2g)). The historical fiveyear earnings growth has been 68% per year including acquisitions and the current return on equity of 26%.

A bottom-up analysis (based upon market growth rates of NAC’s markets’ (i.e., earthmoving in the oil sands and mining) results) was used to estimate an organic growth rate of 7% for NAC. This is based upon analysts’ estimates of 7% and five-year historical organic revenue growth of 16%. This does not include any future acquisitions. If we include 8% growth for acquisitions, then the base EPS growth rate is 15%. Historically, NAC’s EPS growth rate was 65% per year, driven by six acquisitions over five years. If we assume half of the number of acquisitions over the next seven years and a forward return on equity of low-20s declining from the current rate of 26%, retaining 85% of earnings, then the incremental 8% growth per year is conservative. Using a 15% expected growth rate, the resulting current multiple is 39x of earnings, while NAC trades at an earnings multiple of about 5x. If we look at construction comparables, which are larger but have slower growth prospects, they have an average earnings multiple of 18x. If we apply 18x (see details below) earnings to NAC’s estimated normalized 2023 earnings of $5.27, then we arrive at a value of $95 per share, which is a reasonable short-term target. If we use a 15% seven-year growth rate, then we arrive at a value of $202.90 per share. This results in a five-year IRR of 49%.

Growth Framework

{kind=link}

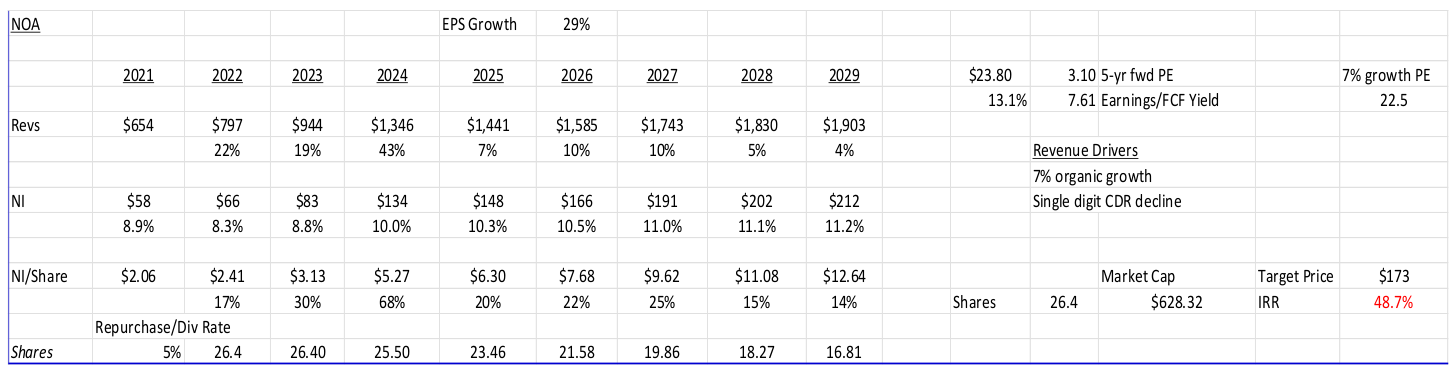

Another way to look at growth and the valuation of companies is to estimate the EPS five years into the future and see how much of today’s price incorporates this growth. Using the same revenue described above results in a 2027 EPS of $9.62, or 3.1x the current price. If we assume a steady-state average growth rate from 2027 on of 7%, then this results in a fair value Graham multiple of 22.5x, or $173 per share, similar to the five-year-forward valuation above of $202.90 per share.

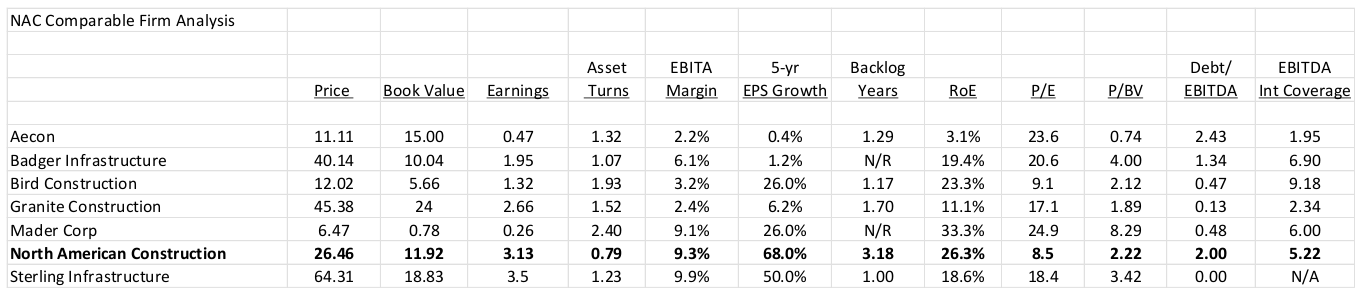

Comparables and Benchmarking

Below are the construction and specialized construction firms located in the United States, Canada, and Australia. Most of NAC’s competitors are private firms. Compared to these firms, NAC has debt on the high end of the range with adequate coverage and has better growth prospects and a below-average multiple. NAC also has the one of the highest RoEs and the highest five-year growth rates.

{kind=link}

Risks

The primary risks are:

- slower-than-expected acquisition growth (currently projected to be 50% of the historic acquisition growth rate);

- lower-than-expected growth in NAC’s end markets offset by the small market share NAC has in its markets; and

- a lack of new investment opportunities (mergers and acquisitions) coupled with higher stock prices making buybacks less accretive.

Potential Upside/Catalyst

The primary catalysts are:

- higher-than-expected acquisition growth;

- faster growth in NAC’s end markets or higher penetration into these markets; and

- increased local scope or purchase of local scale in new markets.

Timeline/Investment Horizon

The short-term target is $95 per share, which is almost 75% above today’s stock price. If the continued acquisition/consolidation thesis plays out over the next five years (with a resulting 15% earnings per year growth rate), then a value of $188 (midpoint of the two methods described above) could be realized. This is a 46% IRR over the next five years.

Footnotes[1] Based upon analysts’ estimates of 7% and five-year historical organic revenue growth of 16%. The total five-year revenue growth rate has been 21%. DisclaimerThis letter does not contain all the information that is material to a prospective investor in the Bonhoeffer Fund, L.P. (the “Fund”). Not an Offer: The information set forth in this letter is being made available to generally describe the philosophies of the Fund. The letter does not constitute an offer, solicitation or recommendation to sell or an offer to buy any securities, investment products or investment advisory services. Such an offer may only be made to accredited investors by means of delivery of a confidential private placement memorandum, or other similar materials that contain a description of material terms relating to such investment. The information published and the opinions expressed herein are provided for informational purposes only. No Advice: Nothing contained herein constitutes financial, legal, tax, or other advice. The Fund makes no representation that the information and opinions expressed herein are accurate, complete or current. The information contained herein is current as of the date hereof but may become outdated or change. Risks: An investment in the Fund is speculative due to a variety of risks and considerations as detailed in the Confidential Private Placement Memorandum of the Fund, and this letter is qualified in its entirety by the more complete information contained therein and in the related subscription materials. No Recommendation: The mention of or reference to specific companies, strategies or instruments in this letter should not be interpreted as a recommendation or opinion that you should make any purchase or sale or participate in any transaction. |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Bonhoeffer Capital - North American Construction Group: Awash With Competitive Advantages And Barriers To Entry