BNTGF - Brenntag: Updating On One Of The Better Chemical Companies

2023-10-13 09:00:00 ET

Summary

- Brenntag is a solid chemical distributor with a stable business model and a strong earnings track record.

- The company operates in both the essentials and specialties segments, providing a unique advantage in the market.

- Despite macro challenges, Brenntag has a diversified customer base and end markets, making it resilient to industry trends.

Dear readers/followers,

Brenntag is a company I have been covering for a few months here at least, but one I've had my eye on for a very long time. I started establishing a position in the company over the past 6-8 months and currently stand at what I view as a very strong cost and yield basis, with a very solid overall upside.

This article is an update on Brenntag ( BNTGF ) ( BNTGY ), specifically the thesis I lay out in this piece right here.

Despite some volatility and some relevant considerations to the medium-term thesis for the company, the performance of this investment has nonetheless been better than the S&P500. My RoR here is 10.57% inclusive of dividends and more inclusive of FX. So, overall, we're having a good performance.

Seeking Alpha Brenntag RoR (Seeking Alpha)

I'm going to give you an update here and show you why this company is perhaps one of the more solid businesses to potentially invest in when it comes to the overall chemical sector. This company, which was once an egg wholesale business, actually has one of the best business models out there and is least affected by macro.

Brenntag: Updating on a solid business

Brenntag is not an "upstream" chemical business. It can be more likened to a midstream or downstream player in the business, as it's a chemical distributor and has been for over 100 years. This industrial player out of Essen, Germany, generates upwards of €13-€15B in annual revenues from the work of 15,000 people at 700 locations worldwide.

The attractiveness of Brenntag is primarily related to its incredible operating stability, by which I of course mean its earnings. If you look at the company's 15-year trends, you see a total of 2 years with negative EPS growth , one in 2016 with -7%, and one in 2021 with -4%. The rest of the years are all positive.

If you think that this does not sound like a chemical company, that is because it isn't, and that is due to Brenntag's business model. The company has made a business out of stability in the chemical sector with relatively low leverage, currently at sub-32% long-term debt to capital. It follows the German tradition of using relatively little debt to fund operations or growth.

Brenntag IR (Brenntag IR)

The company's two core operating segments-essentials and specialties-come with different sorts of business appeal, but what is important to remember is that you do not have another company with this scale in both of these segments. The closest competitor for both would be Univar, but aside from that, no other company even cracks the top three for "both" of these segments.

This is what makes Brenntag the world's most successful specialties and essentials distributor, with an appealing combination of local and global reach, and this one also happens to have an EBITDA CAGR of 9% since the end of the GFC.

Brenntag is a value-adder, working with storage, transport, packaging and labeling, bundling, vendor-managed inventories, and mixing, blending, and formulating. Basically, everything that isn't chemical upstream As you know, I own plenty of chemical producers and upstream businesses such as BASF ( BASFY ) and Evonik ( EVKIY ). These have a vastly more volume-oriented business model with large-scale order sizes, from which Brenntag buys products, which it then packages, value-adds, and ships.

Industry trends are pointing towards specialties and a portfolio focus to decrease the cost of fixed assets-becoming a master of one instead of a master of none. This is exactly what Brenntag is focusing on, and because Brenntag already has the necessary scale, assets, and expertise, it gives Brenntag an incredible moat.

Both of these markets we're talking about have a combined TAM of nearly €300B per year, and these markets, unlike some more cyclical parts of the chemical value chain, are actually expected to grow at 2-7% in the next 2-4 years per year, which gives us appeal here. (Source: 2Q23 Brenntag )

Brenntag IR (Brenntag IR)

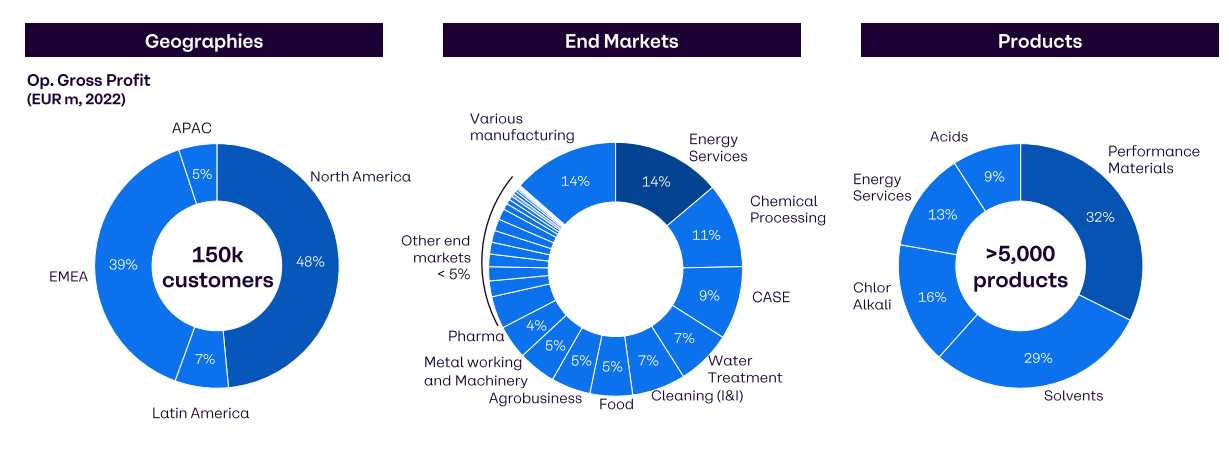

From a fundamental perspective, there is very little argument to be had against Brenntag. We're talking about a globally diversified chemicals business where the industry and product spreads make the businesses extremely resilient to longer-term and shorter-term trends both. The last report cements some of the high-level product and end-market trends somewhat, showcasing essentials here.

{kind=link}

The company has reiterated, recently, its 2026E targets, coming to a very solid organic profit CAGR of 4-6%, together with an EBITDA CAGR of upwards of 8%, lower than historically due to cost and inflation, but still with an EBITA conversion of over 35% and a net annual EBITDA increase of €200 million from modernization.

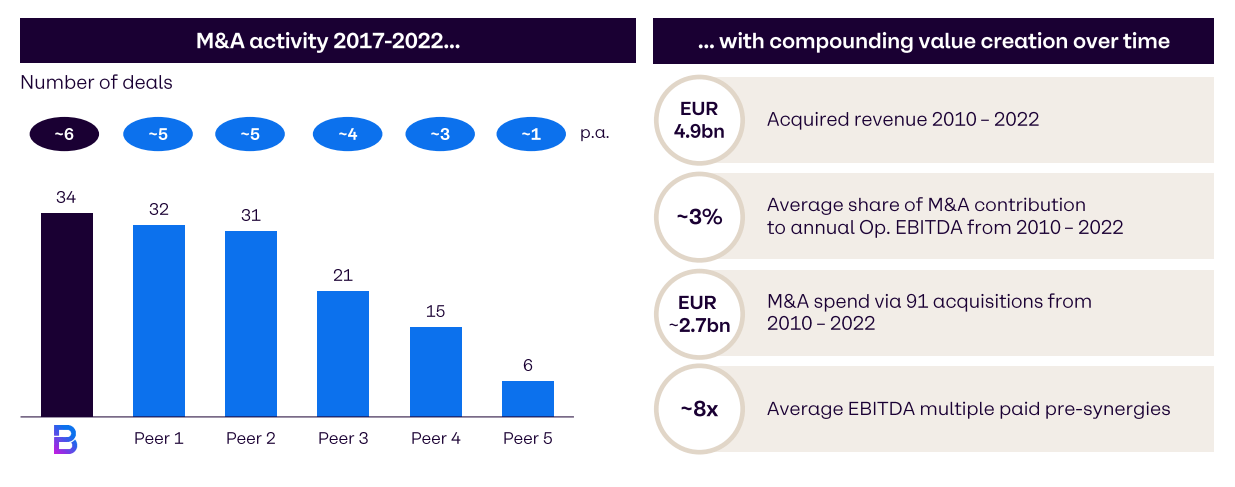

The company is planning to put around half a billion euros on an annual basis into M&A and another €300-€350M into annual CapEx going forward for the next 3 years. We're going to see a combination of inorganic and organic growth for this company-at least, that is what I expect.

The company's high-level specifics make any sort of risk here small. Why?

Because Brenntag has thousands of suppliers , the top 10 accounts for less than 30% of the company's products, and over 180,00o customers, with top 10 being less than 7%. This is the advantage of a chemical distributor as opposed to an upstream business like BASF. The company has over 10,000 products it sells to these customers, and it's not a Germany-focused business either. Less than 10% of sales are in Germany, and the company's end markets are some of the most diversified in the entire chemical sector.

The largest end market?

Food, at 14%.

Try making the argument that food chemicals are going down in a more urbanized/developing world for a company that's not focused on EMEA. Brenntag is also the leading consolidator in this industry, speaking to M&A's for a second.

{kind=link}

My investments in Brenntag do in fact reflect the thesis I hold for the company long-term. I am already heavily invested in the business, and I am very open to buying even more shares at cheap prices if such prices should present themselves.

2Q23 was a bad quarter, no doubt about it. The company's sales, gross profit, EBITA were down. However, EPS and FCF were up, and its new operating model was introduced, and Brenntag is now specifically guiding for an annual EBITA of €1.3B - €1.4B for the full year.

The reason for what could be described as lackluster performance is macro. Less cyclical does not mean "immune" to cycles, because Brenntag certainly is not that. The macro is challenging and geopolitical challenges are causing impacts here. Continued destocking and sluggish end markets are impacting order flows. The impact is far higher for upstream and more cyclical companies.

I currently forecast an adjusted EPS decline for Brenntag of about 7-10% for the 2023E period - no more than that.

I hope Brenntag declines more, but I also believe that the market, or atleast Brenntag investors are very aware of the fact that this company is moving up eventually. I expect and forecast double-digit potential growth not only for 2024, but for 2025-2026E.

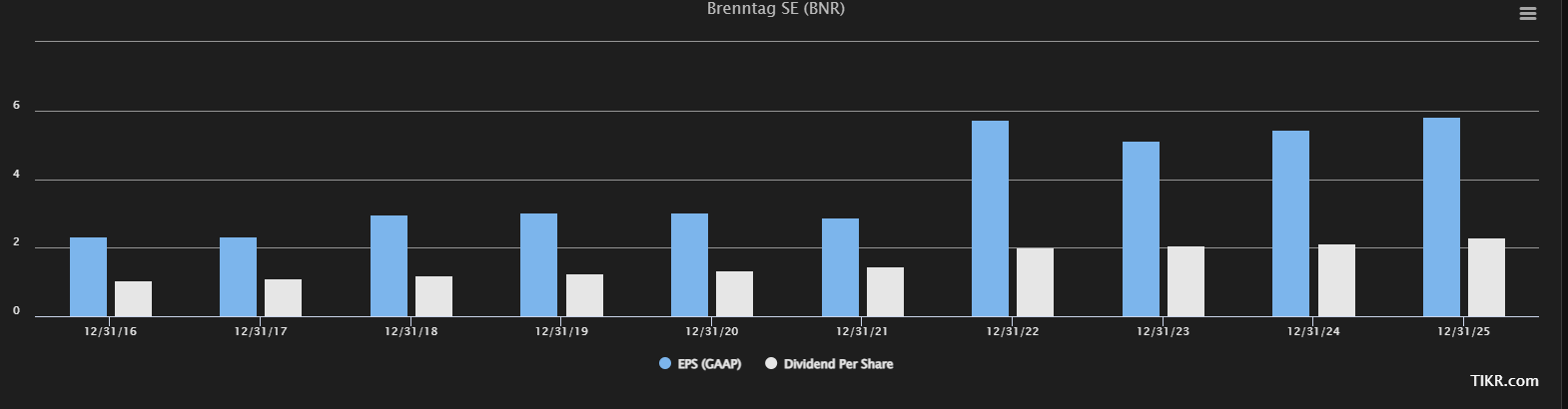

Here are current S&P Global forecasts.

Brenntag EPS/Dividend (S&P Global/Tikr.com)

{kind=link}

And I remind you, this is a chemical distributor, not some consumer goods player. The EPS and dividend stability you see here is substantial.

My own YoC is over 3.2% on the company, having bought it lower. It's now at 2.8%.

Let's look at company valuation.

Brenntag - The valuation still "works"

It is unfortunately no longer possible for me to call the company "cheap". The reason is that the company no longer has a 15% upside to a conservative multiple, which in this case I would say would be around 15x, despite a 5-year normalized premium of around 18x, which I actually consider to be somewhat indicative for this business.

I would see, based on current estimates of a €6.2/share EPS for the 2025E period, a 34% upside to a 15x P/E, which brings us to just below 15% per year on an annualized basis. Because I consider the premium to be relevant here, I do believe the company is still a "BUY", but I don't view it as a "cheap" business any longer.

Based on 18x P/E (at a premium) for that EPS, we're able to see a 22%+ annualized rate of return to a total of almost 63% until 2025E. I don't consider this easily achievable, but Brenntag has made a business out of hitting estimates and does so more than 50% of the time even with a very low margin of error (Source: FactSet).

S&P Global analysts consider Brenntag, at €72/share to be undervalued. The average PT from these is €85/share, which implies a double-digit upside of 17.9%, with 11 out of 17 analysts either at a "BUY" or a equivalent, positive rating. The low here is €71, and the high is €99/share. For the 2025E, I consider a conservative €90/share to be the least that Brenntag should be worth. This is not my current PT, but I'm bumping my conservative PT from €75/share to €77/share based on the next few years, despite the current estimated earnings drop this year.

Here is my thesis for Brenntag.

Thesis

- Brenntag is a world leader in chemical distribution. No other player offers the same sort of diversity of operations and products and is as well integrated as Brenntag. The company is an excellent complementary investment to a basic materials portfolio and, at the right price, should be considered a must-own due to its double-digit return potential based on extremely attractive exposures and trends as we move forward.

- I give Brenntag a conservative PT of €75/share. That's as low as I can go, and that's with impairing earnings 15-20% and going as low as 12x P/E on a forward basis, despite believing that the company is really worth 14-15x P/E, implying a share price close to triple digits.

- For now, I rate Brenntag as a "BUY". I have a strong position in the company, and it's one I slowly will continue expanding here.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansions/reversions.

The company is no longer cheap here, but it does fulfill all other of my demands.

For further details see:

Brenntag: Updating On One Of The Better Chemical Companies