WMT - Bridgford Foods: Hidden Value On The Balance Sheet

2024-01-19 07:46:50 ET

Summary

- Bridgford Foods receives a buy rating due to its market price trading below its tangible book value and potential for growth when market headwinds subside.

- The company is going through inflationary pressures that have persisted over the past 2 years materially damaging margins.

- I believe there is hidden value on the balance sheet due to GAAP accounting rules.

- The company has sold assets and used the cash to pay off debt and invest in capacity expansion for a strategic facility.

- I view the high insider ownership as a net positive, along with the fact that majority of the company is owned by the Bridgford Family.

Editor's note: Seeking Alpha is proud to welcome William Walsh as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Investment Thesis

I assess a buy rating for Bridgford Foods Corp. (BRID). BRID is trading at a deep discount, below tangible book value. Additionally, BRID has a real estate portfolio that does not come close to accounting for true market value on their balance sheet, presenting a satisfactory risk-reward opportunity in this microcap stock.

Brief Overview of BRID

Bridgford Foods Corp operates in the United States as a manufacturer, marketer, and distributor of a diverse range of frozen and snack food products. The company is organized into two primary business segments focusing on the processing and distribution of frozen products as well as the processing and distribution of snack food products. The product portfolio encompasses various items such as biscuits, bread dough, roll dough, dry sausage products, and beef jerky.

Bridgford Foods reaches its customers through different channels. For frozen food products, the company serves foodservice and retail clients through wholesalers, cooperatives, and distributors. On the other hand, snack food items are distributed to supermarkets, mass merchandise stores, and convenience retail stores through customer-owned distribution centers and a direct store delivery network.

A significant portion of Bridgford Foods' revenue is derived from snack food products. The company strategically positions itself in the market by catering to both the foodservice industry and retail customers through a wide-reaching distribution network.

{kind=link}

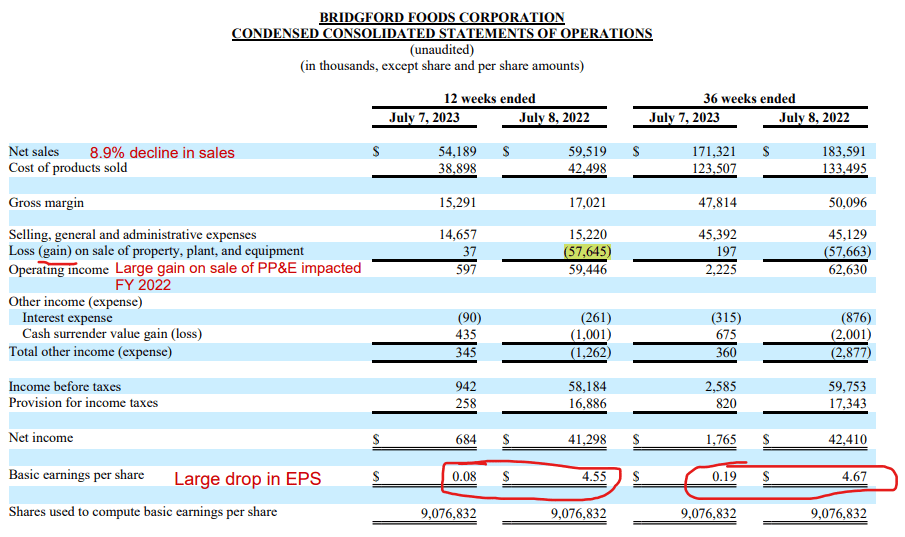

As of the MRQ, the 12- and 36-week period shows some concern from an operational standpoint for BRID. In the 12-week period, sales have declined 8.9% and operating income has dropped by over $58M, resulting in an EPS of $0.08 vs. $4.55. The main reason for the material decline in operations is due to the gain from a sale of one of their properties, which we will explore in more detail later. On a 36-week basis, sales are down by 6.6% with a $60M drop in operating income, resulting in an EPS of $0.19 vs. $4.67. The core reason for the drop in sales was due to a 9% drop in unit volume YoY, which, according to management, is due to a drop in demand because of the inflationary environment changing consumer spending habits.

{kind=link}

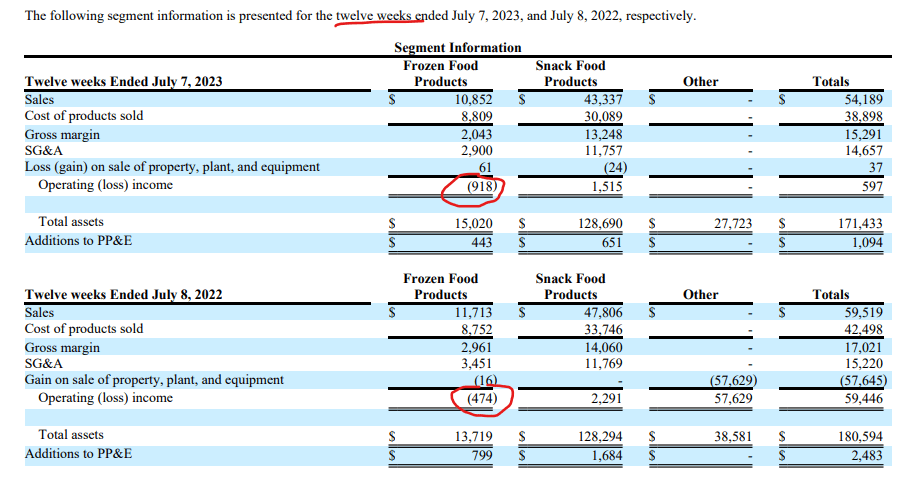

As we delve deeper into the details, we see a tale of 2 segments at BRID. The snack food products segment contributed 80% of the $54M in revenue BRID generated, along with $1.5M in operating income at a 3.5% margin. The frozen foods products segment is a different story. This segment operated at a $918K loss on $10.9M in revenue. Historically, the majority of BRID's revenue and profit has come from the snack foods division as noted above, and with management self-describing these products as "impulse buys", the current macro environment is likely the main cause of pressure on the company's performance.

These inflationary headwinds and lower consumer demand are likely temporary. However, the tenet of my investment thesis is based on data we can't see, regardless of company performance metrics.

Tangible Book Value Analysis

When looking at the MRQ , the Tangible Book Value ((TBV)) is $14.11 while at the time of this writing the market price is $11.09. This represents a 21.4% discount to TBV, which can be seen as a proxy for liquidation value. In my opinion, when looking at an investment based on TBV it is important to verify the quality of the assets and determine if there are any off-balance sheet liability arrangements.

{kind=link}

BRID's current assets make up 52.3% of its total assets. A quarter of those current assets is inventory, which consists of $26M of finished goods that have a relatively long shelf-life due to the dehydrated and frozen products of the business. The remaining $17M is in commodity inventory and work in progress, which likely could be made into finished products if need be. This indicates that in a liquidation/bankruptcy scenario $89M could be generated swiftly to satisfy the creditors of the company, with plenty left over for shareholders.

{kind=link}

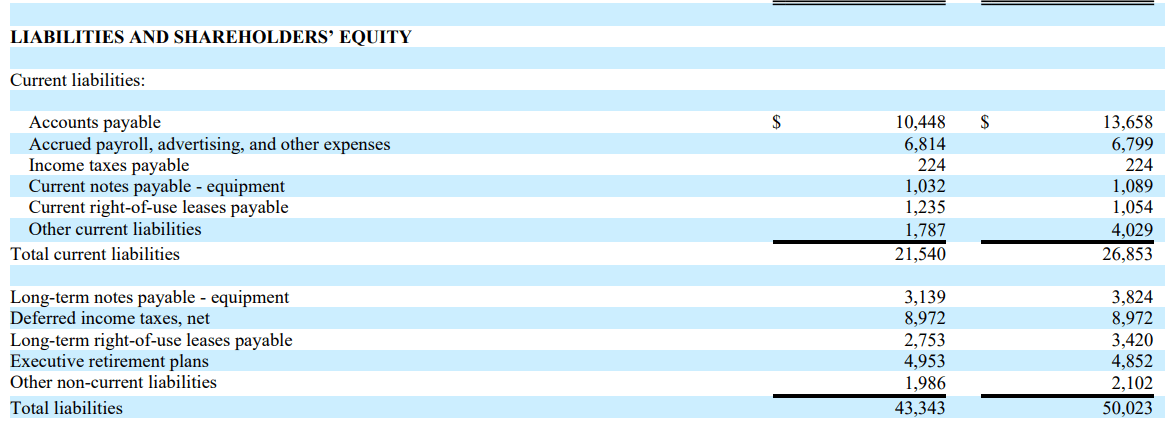

As of the MRQ the company had $43.3M in total liabilities with 24%/$10.4M in the form of payables. The debt/equity ratio is a paltry 6.5% thanks to management paying off substantially all their debt with the proceeds from the sale of one of their Chicago processing facilities.

{kind=link}

With highly liquid assets and virtually no liabilities, I am comfortable with the TBV of $14.11, representing what we as investors can expect to receive in a liquidation scenario for BRID. The current price of $11.09 represents an inherent margin of safety.

Hidden Value on the Balance Sheet

The company has net PP&E assets valued at $69.5M on their balance sheet. To briefly go over accounting for those who have no background in accounting, the net PP&E is where the value of property plant and equipment are located on the company's balance sheet, minus the depreciation expense the company has taken over the useful life of the assets up until the current reporting period. Any appreciation in value of the land or the facilities is NOT accounted for under existing GAAP rules.

The point I am trying to convey, is that real-estate assets can be worth more than the value it is carried at on company's balance sheet due to limitations of GAAP accounting rules.

The reason I briefly went over this accounting lesson is because of the following: in the July FY 2022 quarter, the company sold a parcel of land including an approximate 156,000 square foot four-story industrial food processing building located at 170 N. Green Street in Chicago, Illinois for a purchase price of $60M!

Why is that important? Well look at the list of the existing properties from the company's FY 2022 10-K below.

{kind=link}

The company still has 7 processing and distribution facilities it owns, including the facility at 44th Street in Chicago, which has 21K more SQFT than the 170 N. Green Street that sold for $60M. Now ask yourself, is the value of the properties listed under PP&E really only worth $70M? I would argue there is a lot of value not captured on the balance sheet due to accounting rule limitations. And yes, I know interest rates have increased dramatically since the date of the sale, and the real estate market is still being impacted on a commercial level. I would still argue that these properties are worth much more than $70M. Not to mention that PP&E includes the processing and manufacturing equipment the company owns, which likely has some salvageable value.

Here is a video overviewing their updated Chicago facility that primarily handles their meat processing operations. I recommend all to watch this so they can get a visualization of one of Bridgford's key assets and what a typical day of operations looks like at this facility.

The hard part for us as investors is to try and find the true market value of these properties. One Seeking Alpha contributor estimates the potential value of these properties could be $200M . If that is true, the TBV/share should be $36.13, a 226% upside. But let's be a little realistic/conservative and say this contributor is half right, where the total of the properties is worth roughly $100M, only $40M more than the sale of that ONE property. That would put the TBV/share at $25.12, a still hefty 127% upside. There are also no material off-balance sheet liabilities that were disclosed in their MRQ 10-Q. Investors can see that there is a deep discount in the company's stock which, in my opinion, presents a high risk to reward ratio.

Risks to the Thesis: Invert Always Invert

The depressed stock price does have merit due to the headwinds BRID is facing right now. As stated previously, MRQ sales have declined 9%, a third consecutive quarter in a decline of sales growth. The company disclosed that sales growth has slowed down because of a drop in unit volume due to a decline in demand from the inflationary environment on consumer habits for both the Frozen Food and Snack Food segments. Management has also described their snack division as "impulse buys." Not exactly the most resilient company if a recession does occur.

{kind=link}

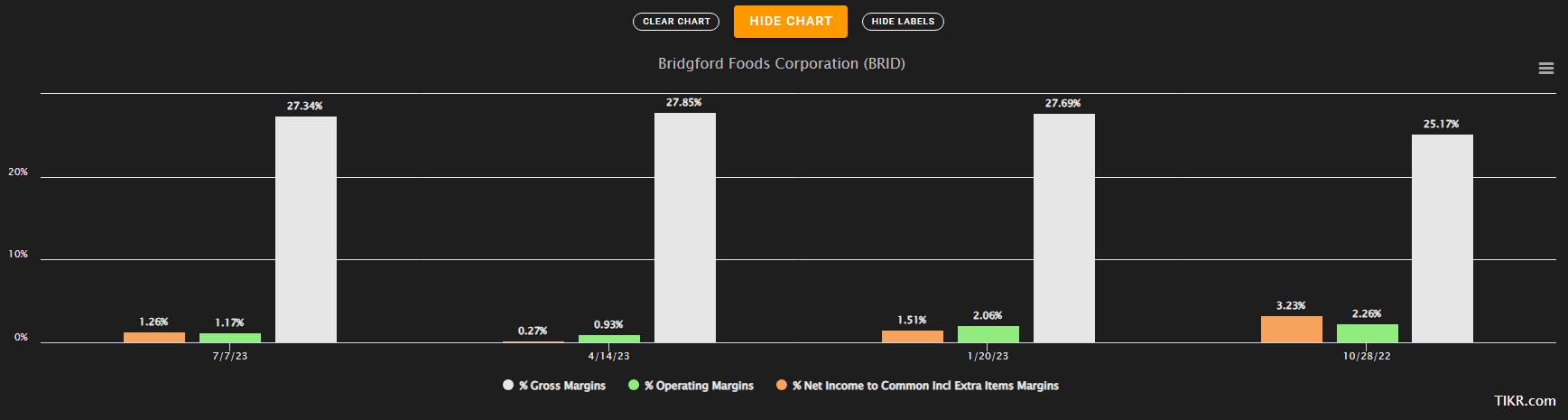

While sales have declined, the company has done a relatively decent job in maintaining gross margins over the TTM period.

{kind=link}

The company's biggest commodity expenses are beef, pork, and flour. While they purchase flour domestically, the Russia-Ukraine war is interrupting international trade and increasing flour prices, hurting margins compared to previous years. Beef and pork have had wild swings over the past few years, so investors should expect some volatility in commodity costs, especially since the company does not engage in any hedging activities.

SG&A expenses have all come down YoY for the MRQ. Insurance expenses and Other SG&A (which is just a catch all metric that includes pension income, vehicle repairs, and consulting fees) slightly increased.

{kind=link}

For the YTD numbers we saw a double in outside storage expense from $519K to $1,165K. This could be a sign that the company overproduced or does not have sufficient storage facilities that would require CapEx investment in the future. Management also decided to cut their credit line from $15M to $7.5M, lowering their liquidity position. On top of that they disclosed that they are willing to mortgage their properties in order to satisfy cash needs. This is puzzling to me: why mortgage the properties, a collateralized senior loan vs. using lines of credit already available? I would assume lower interest expense, but this should be monitored carefully by investors.

I believe the mortgaging of properties is the biggest downside risk to my investment thesis . If the company decides to mortgage some of these properties to improve their liquidity position, the banks will be higher than us equity holders in the capital stack, and in a liquidation scenario, investors will no longer have claims to the real estate assets the company mortgaged. This act could eliminate the inherent margin of safety of the current market price, and meaningfully impact the tangible book value of BRID. I reiterate, this must be monitored carefully.

The company also has concentration risk for their sales and receivables from WMT and DG. If either of these major retailers have their own financial issues or decide to drop BRID products, this will materially impact the revenue and the operating cash flow of the business.

{kind=link}

On top of all this, BRID has not generated operating cash flow over the past 2 years and has not generated FCF since FY 2017. FCF has suffered as the company invested in CapEx for their snack foods division, which does account for over 78% of sales for the YTD results, and contributed materially to the sales growth of $167M in FY 2017 to $265M in FY 2022, a 9.7% CAGR.

Growth Potential

While there are existing headwinds, there is still a potential growth story here. The company has not been sitting idly by as they go through this macroeconomic event.

As we saw above, BRID is managing costs well considering the macro environment. They are trying to return to profitability in the frozen-food section by shutting down the long-haul fleet for that division, while also taking 4 price increases in the foodservice division, the first time this has happened. They currently have 4 of the largest school districts in the USA as customers, and are in the negotiating process with the 3 other biggest school districts to grow sales of the foodservice segment. It is important to note that school districts count for over 25% of foodservice revenues. The foodservice division should return to profitability as input costs come down, and they did restructure some of their bread processing facilities to cut costs.

WMT is allowing new bread items in stores in FY 2023, with their monkey bread being the top seller. BRID is also gaining market share in Kroger's and Target's distribution network. BRID is now in 19 out of 20 Kroger distribution centers and in over 2K Target stores, with more than $1.6M in Target sales vs. $60K last year. Management stated on the most recent virtual investor presentation that they were able to land Kroger as a customer because of their strong performance during Covid. By strong I mean their supply chain was not shut down like many of their competitors during that time.

Management stated in their investor day that their focus is on cutting expenses, eliminating people who do not produce, and getting in front of customers to generate sales. Nothing matters if they do not sell anything.

The expansion at the 44th street Chicago facility is doing well with capacity expansion and efficiency initiatives. This could mean lower outside storage costs in the future. BRID is also focusing on improving their production schedule so they do not overproduce, lowering inventory costs.

Lastly, they have been seeing good growth in their snack foods division, especially around their jerky products. The company entered the convenience store market less than 3-years ago, and have grown sales from $0 to $8M, and have the 6th highest rated jerky brand. The company also has been sponsoring an angling team and is entering the college sports market to help spread brand awareness.

As I stated in the beginning of this article, I believe the headwinds BRID is now facing are temporary and management is taking appropriate action for the long-term viability of the business.

Conclusion: BRID is Still a Buy

With the above initiatives and the skilled management that consists mostly of Bridgford family members, who also own over 80% of the company, I think there is an ability for the company to continue to grow sales, albeit at a slower rate. Regardless, with the market pricing the company below TBV/liquidation value and the "conservative" potential $100M in real estate value hidden on the balance sheet, I reiterate my thesis that BRID is a buy and may be worth a risky business play in a risk tolerant investors portfolio.

For further details see:

Bridgford Foods: Hidden Value On The Balance Sheet