EDV - Brigadoon

2023-11-08 22:04:42 ET

Summary

- US long bond yields have receded, leading to a bounce in the high beta space thanks to renewed liquidity.

- Yet, "Credit availability" is deteriorating, and employment and PMI indicators are weakening, which does not bode well for 2024.

- There is a potential year-end rally in the cards, as seen in the significant bounce in US High Yield and the improvement in European High Yield.

- There is decentralization coming in the monetary system.

“Nothing in life is to be feared, it is only to be understood. Now is the time to understand more, so that we may fear less.” - Marie Curie

Watching with interest the receding yields in the US long bonds in conjunction with the bounce in the high beta space which were hinted not only by the action price in the crypto space indicative of “renewed liquidity” as well as by our last quote from our previous musing, when it came to selecting our title analogy we reminded ourselves of the term “Brigadoon”, being a place that seems magically transient such as “inflation” for some central bankers such as former Fed “supremo” Janet Yellen. For those who have been following us through our many musings, you know that sometimes we like our titles to have multiple meanings or references. From Websters dictionary a “Brigadoon” is a place that is idyllic, unaffected by time, or remote from reality. In similar fashion one can opine that the period of zero interest rates courtesy of our sorcerer’s apprentices aka central bankers has come to a brutal end. The “Brigadoon” period of ZIRP was unaffected by time given that time was not given any “value”. Of course, this “idyllic” period for anything “beta” was detached from reality. In the urban dictionary a Brigadoon is an alcoholic beverage commonly drank in London East End, which sides effects are: inebriation, vomiting and chatting nonsense. On a side note, Brigadoon refers also to 1954 MGM Musical starring Gene Kelly, where the American heroes on a hunting trip in Scotland happen upon Brigadoon, a miraculously blessed village that rises out of the mists every hundred years for only a day. The movie was inspirational to the Waterboys 1985 classic song “The Whole of the Moon” which uses as well the term “Brigadoon” in its lyrics but we ramble again:

“I was grounded

While you filled the skies

I was dumbfounded by truth

You cut through lies

I saw the rain dirty valley

You saw Brigadoon

I saw the crescent

You saw the whole of the moon” – The Waterboys – The Whole of the Moon, 1985

In similar fashion to the heroes of the 1954 movie, many financial pundits would love to return to “Brigadoon”. Unfortunately, being detached from reality for too long has consequences such as the need for some central banks to seek “recapitalization” but, that is another story. In this conversation we would like to look at the current bounce, which is “liquidity” driven again we think and if it has legs. As well, we see a continuation of the deterioration of “credit availability” in conjunction with a weakening tone in both employment and PMI indicators which does not portend well for 2024.

- Year-end rally in the cards?

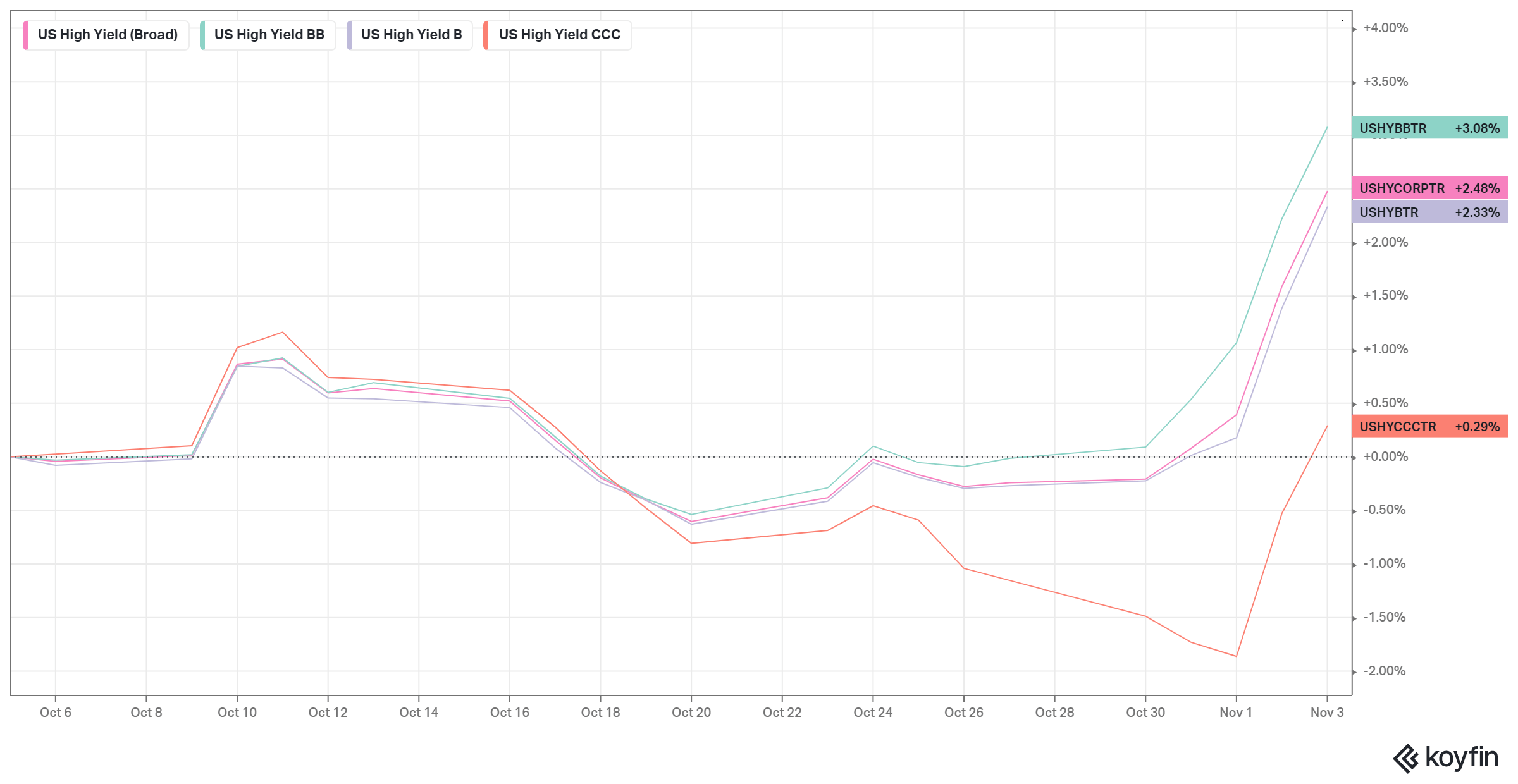

Thanks to a sudden drop in US yields, we have seen a significant bounce in the “high beta” space like in US High Yield (1 month chart):

{kind=link}

-

- Graph source Macronomics - KOYFIN

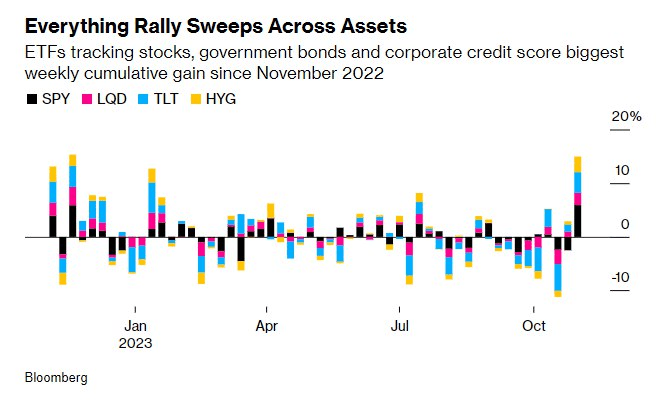

Bloomberg as well points towards a similar bounce across assets:

{kind=link}

- Graph source Bloomberg

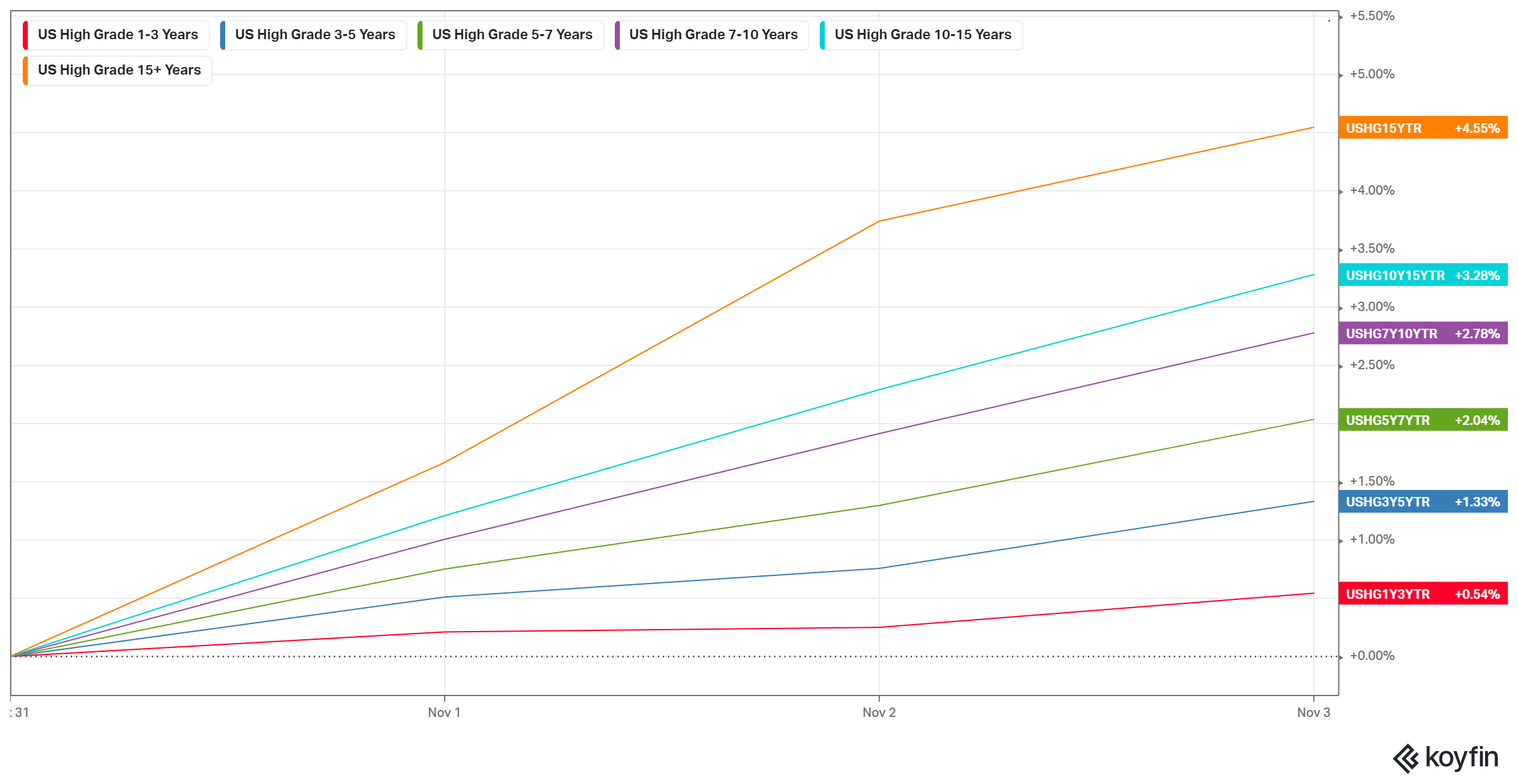

Of course as we pointed out in our last conversation Convexity had indeed starting to bite in US Investment Grade but since the beginning of the month, US Investment Grade has bounced significantly and particularly the long end, no real surprise there given the fall in yields in the long end of the US Yield curve ((MTD)):

{kind=link}

-

- Graph source Macronomics – KOYFIN

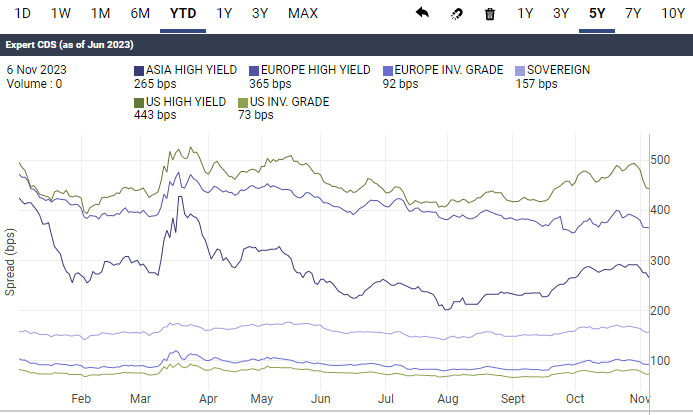

Credit risk wise 5 years CDS spreads have significantly receded since our previous conversation (YTD chart). Since our last conversation US High Yield CDS gauge is tighter by 40 bps. European High Yield as well is improving:

{kind=link}

-

- Graph source Macronomics – Datagrapple.com

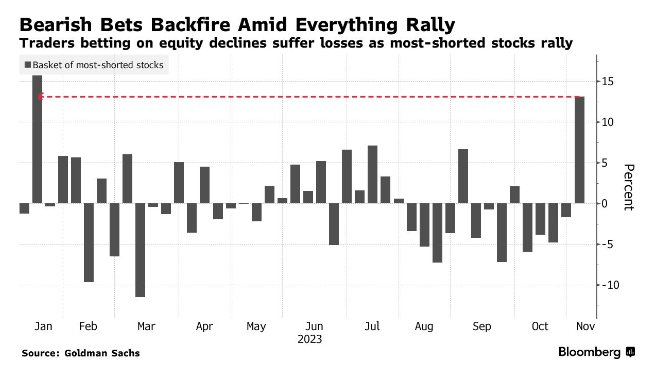

The “risk reversal” caught many traders to cover there “shorts” given the sudden burst with this rally:

{kind=link}

-

- Graph source Bloomberg

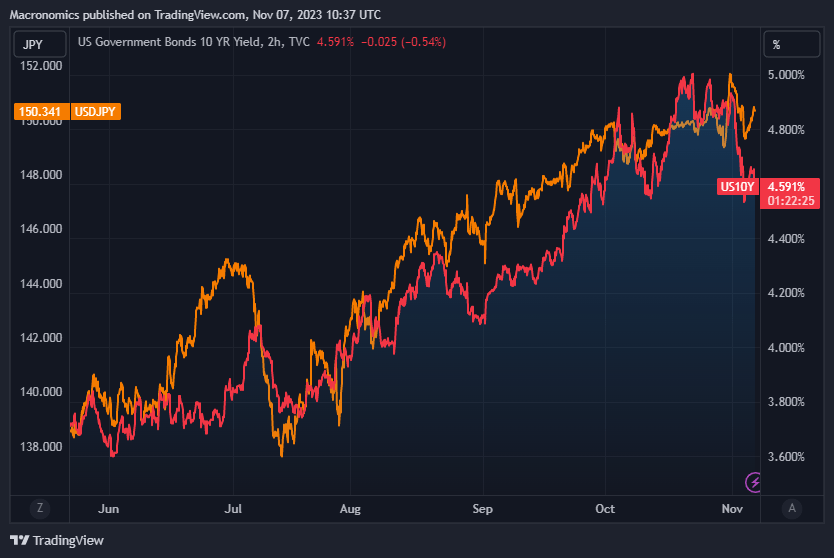

As you know by now, we have highlighted on many occasions that we have been tracking the Japanese yen depreciation in synch with the rise in US Treasury 10 year yields (6 months chart):

USTs 10 year yield vs USD/JPY 6 months (Macronomics - TradingView)

{kind=link}

-

- Graph source Macronomics – TradingView

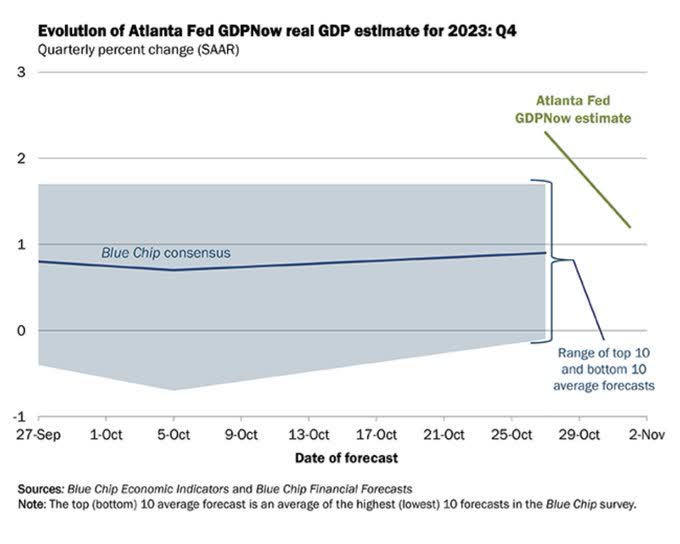

What is of interest to us is that coincidence or not, the reversal of the US 10 year US Treasury notes yield came around the same time of the release of the Atlanta Fed GDPNow forecast on the 1 st of November pointing towards a real GDP Growth in Q4 2023 of 1.2%:

{kind=link}

-

- Graph source Atlanta Fed – X/Twitter

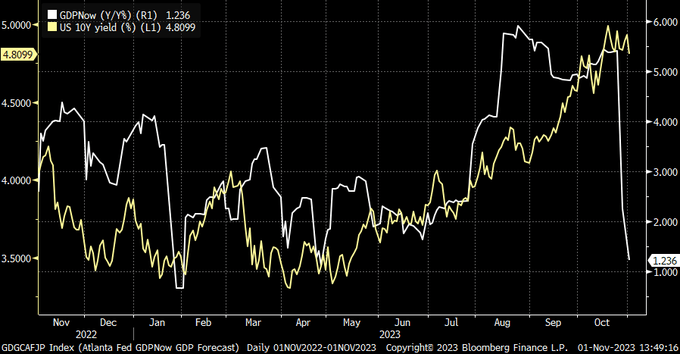

As pointed out by @Marcomadness2 on the first of November on our X/Twitter feed there was indeed somewhat a “trigger” in the rapid fall in the US 10 year yield:

“The Wiley-GDPNow-Coyote Effect”

US 10 year yield vs GDPNOW (@Marcomadness2 – Bloomberg – X/Twitter)

{kind=link}

-

- Graph source @Marcomadness2 – Bloomberg – X/Twitter

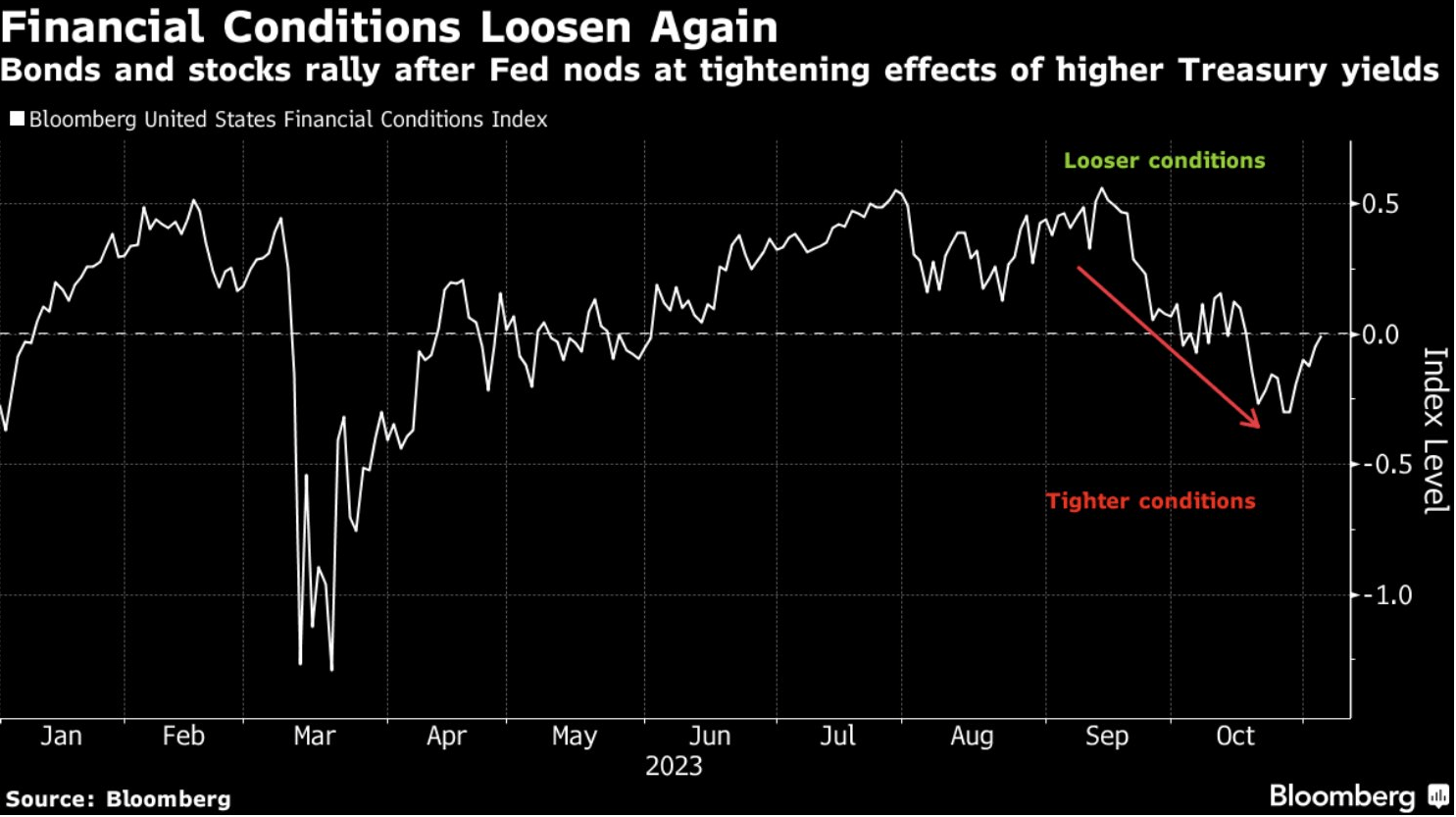

No wonder last week saw the largest YTD rally in “everything”, somewhat a return to the “Brigadoon” of financial euphoria, thanks to loosening of “financial conditions”:

{kind=link}

-

- Graph source Bloomberg

As we pointed out in our conversation “ Springtime of Nations ” published on the 24 th of October, we indicated that we were looking at BitCoin as a “liquidity” indicator. We told you that the very recent jump in the price of BitCoin in conjunction with President Xi Jinping’s recent surprise visit to the People’s Bank (PBoC) was probably tied to some sort of “unleashing” of a significant amount of additional stimulus. Both ETH and BTC jumped very significantly on the 23 rd of October based on an ETF driven movement, on the anticipation surrounding ETF spot approval which propelled BTC around the $35K level, its highest level since May 2022.

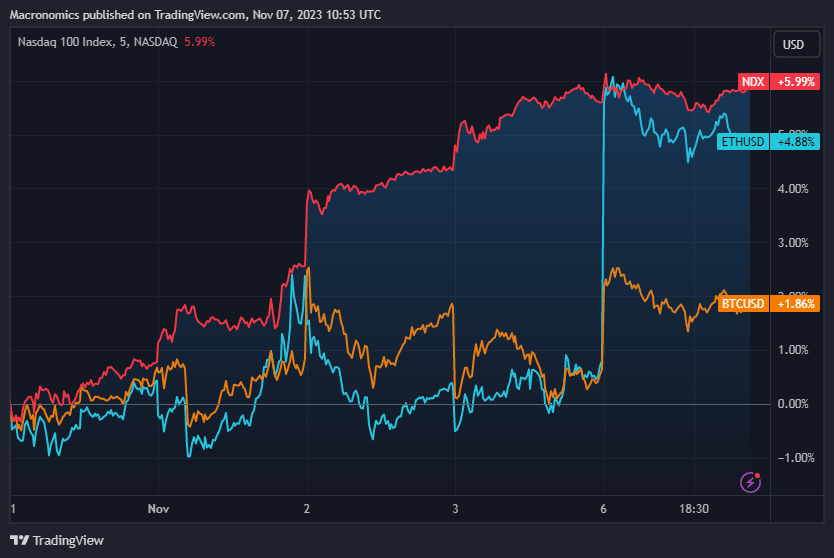

In the last 5 days, following the rally in crypto, we have seen again a correlation with Nasdaq leading to a significant rise in the index:

{kind=link}

-

- Graph source Macronomics - TradingView

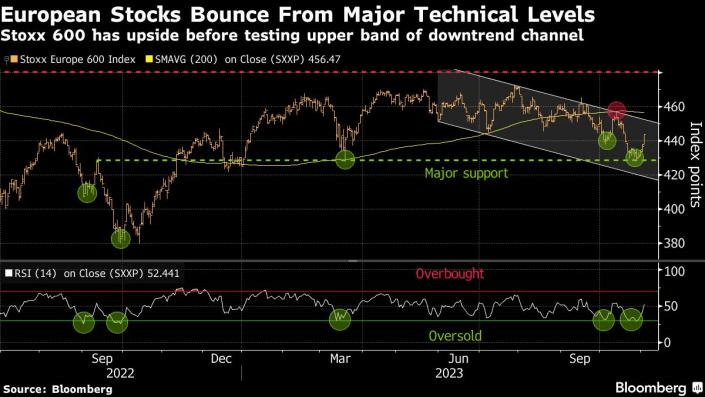

As well, European stocks joined the rally in US equities:

{kind=link}

-

- Graph source Bloomberg

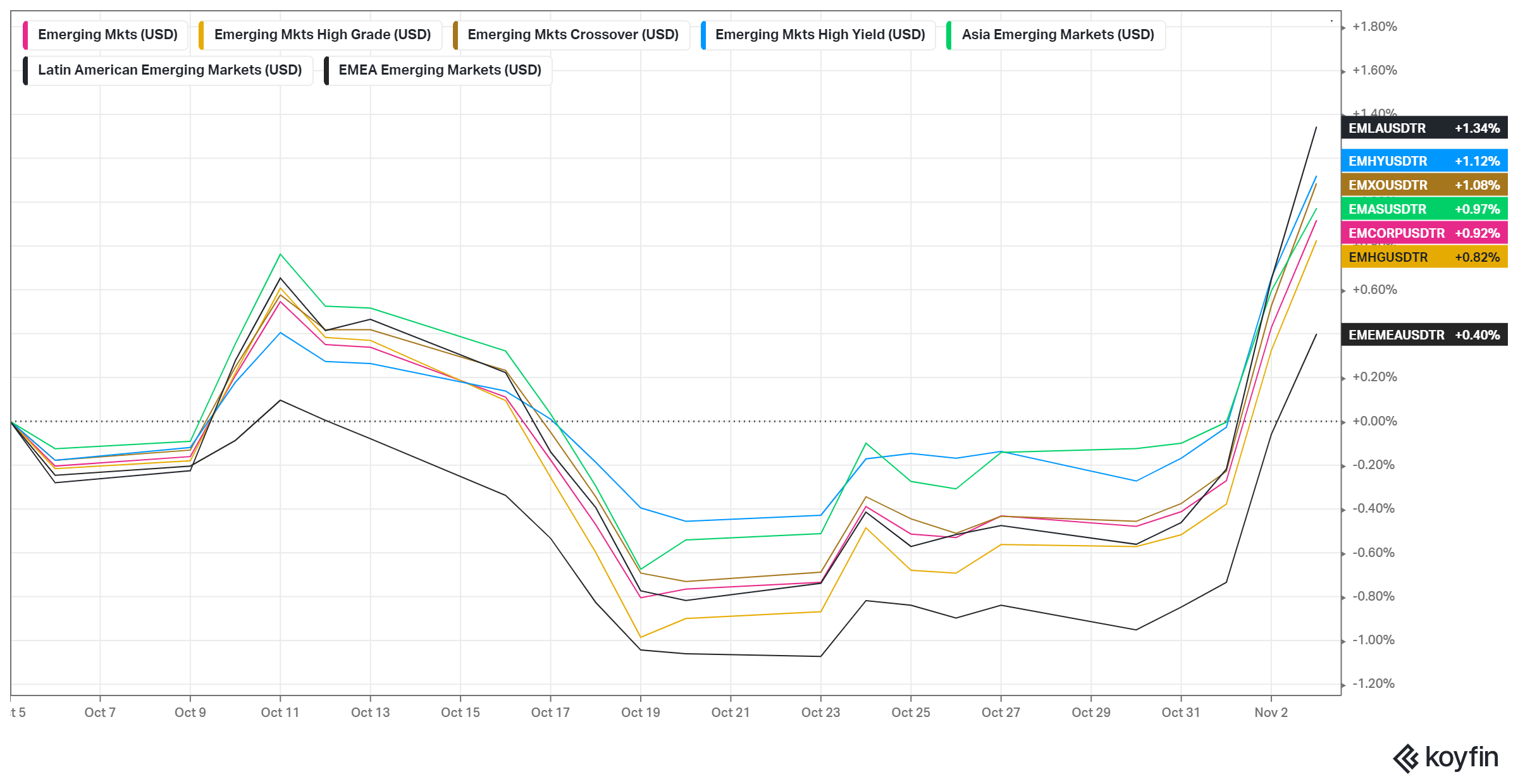

As far as Emerging Markets are concerned, what is of interest to us is that relative to US Investment Grade and US High Yield, it displays far less volatility and less “beta” (1 month chart):

{kind=link}

-

- Graph source Macronomics – KOYFIN

This is interesting because, as we have joked with other financial pundits in recent times it seems to us that more and more Developed Markets ((DM)) government bonds are trading more and more like Emerging Markets ((EM)) bonds as shown by Joe Consorti in our X/Twitter feed:

“Liquidity in the US Treasury market, as measured by average yield errors, is more stressed than the COVID meltdown in March 2020. Ample liquidity is a hallmark of the ~$23 trillion US Treasury market. Not good.” – Joe Consorti

US Treasury Market Liquidity (Joe Consorti – Bloomberg -X/Twitter)

{kind=link}

-

- Graph source Joe Consorti – Bloomberg -X/Twitter

As a reminder from our previous conversation “ Gambit ”:

“The US fiscal trajectory is unsustainable because of Quasi Fiscal Deficit in the US. (For more on QFD issues we highly recommend watching Geoffrey Fouvry quick take on Graph Financials, part 1 and part 2 ). US Treasuries seems to be more and more trading like Emerging Market bonds when it comes to “volatility”. – Macronomics, September 2023

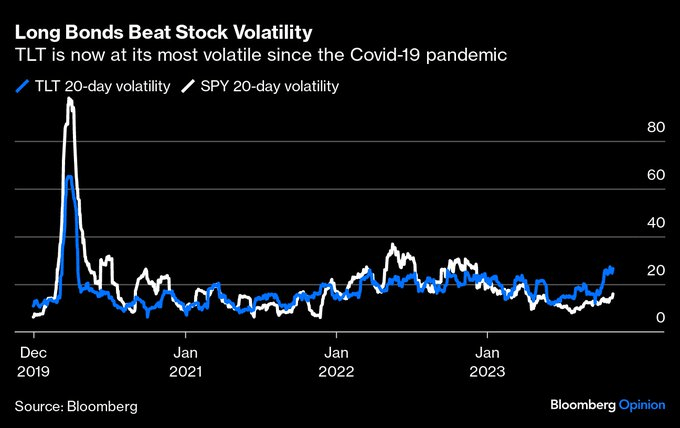

Also there has been a significant rise in bonds volatility than can be ascertained from ETF TLT volatility over the S1P500 20 day volatility, indicative of the on-going destabilization process of the much vaunted 60/40 portfolios in recent times:

"Volatility of iShares 20+ Year Treasury Bond ETF ( TLT ) now exceeds that of the SPDR S&P 500 ETF Trust (SPY). The ICE BofA MOVE Index, which tracks price swings on US bond options, has had an average reading of 124 over past year, almost double its measure over previous decade"- Ali-Khan Satchu

{kind=link}

-

- Graph source Bloomberg

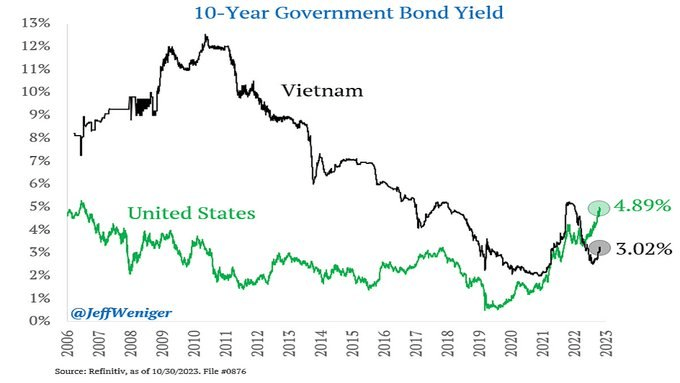

This change in the volatility pattern gives more ammunition to our opinion about the fact that DM bonds are more and more trading like EM bonds:

{kind=link}

-

- Graph source Jeff Weniger – X/Twitter

Where is safety today? This brings us to our next bullet point.

- On the road to a decentralized monetary system?

Other recent months we read with interest the conversations relating to “dedollarization”. On one side you have the “dollar can never be replaced as a reserve currency” camp and on the other side you have other financial pundits discussing that the rise of BRICS+ will lead to the creation of a new “reserve” currency. If globalization went hand in hand with “dollarization”, we believe that “deglobalization” should lead to further “decentralization”. While going through the few macro letters we read on a regular basis, Charles Gave from Gavekal made the argument that we were not moving back towards a Bretton-Woods-type system but what he call a messy environment based on multiple bilateral agreements. Both Geoffrey Fouvry and ourselves find us in agreement with Charles Gave. We think that a multipolar world will not lead to a new reserve currency but most likely to a system that prevailed pre 1922 (Genoa conference). The advent of floating currencies following August 1971 Fed gold decision led to the emergence of powerful central banks which corresponded to more globalization as well as more centralization. One could argue that the Great Financial crisis of 2008 marked the top of “financialization”.

Prior to 1873, the financial system was decentralized with Bills of Exchange being used and the system was a lot more resilient and stable. The first attempt at centralization was the gold standard demonetizing silver which had a catastrophic outcome and led to the great depression of 1873.

What most people do not understand is there is more “stability” in “chaos”.

Dylan Grice formerly with Société Générale wrote a great piece in June 2012 called “The Illusion of Safety”:

“Developments in traffic engineering show that measures aimed at making roads safer (such as road signs, traffic lights) actually make roads less safe. They signal to drivers that it’s OK not to think through the risks of their behaviour. Is that so different to the recent problems caused by over exposure to sub-crime mortgages or eurozone sovereign debt? Didn’t regulators say such securities were “risk free” and reward heavy ownership of them? Today’s crisis has been dubbed a crisis of capitalism. A crisis of regulation is more accurate.” – Dylan Grice – Popular Delusions, June 2012

Given the current trajectory of the financial system as a whole towards “decentralization” and our fondness for physics and biology analogies in our various musings (our Marie Curie quote is not by happenstance), we thought that it would be important for us to revisit this time piece from Dylan Grice because it makes perfect sense from an analytical perspective:

“Traffic is a complex system. It self organizes at a macro level by drivers or pedestrians following a simple algorithm at the micro level. That rule is something like “avoid collisions by keeping a safe distance from whoever is in front” and from it springs a cohesive and spontaneous system-wide order. Intricate networks of paths are created allowing individuals to reach one location from any other location, and to do so simultaneously. The non-linearity of the system is apparent when one considers the consequences of a traffic interruption somewhere. The answer is it depends which path is blocked, when and what type of traffic is in the vicinity of the interruption. So it might have no effect on traffic flow, or it might have a paralyzing effect. Finally, there is no central command to such a traffic system. One will spring up wherever there are people and no higher intelligence is required to build one.

Of course, today many such networks are centrally planned, particularly road networks, which is why the traffic light example is so interesting. They are planned by a central agency. And behaviour on them is regulated by that central agency too, in the form of systems of traffic signs, speed bumps, bollards and traffic lights. All are intended to make the roads safer for users of the roads. The problem is that they don’t.

The pioneering demonstration of this was by a traffic engineer called Hans Monderman who I think should be a household name. In 2001, he redesigned the landscape of the small town of Drachten in the Dutch province of Friesland by removing all traffic controls. There are no traffic lights, no traffic signs, no traffic islands and no arrows pointing people in the direction they’re supposed to be moving in. At the town’s main four-way intersection, the Laweiplein (picture on front page), only the minimum legally required traffic indicators remain. In a fascinating article Tom Vanderbilt recalled meeting the man in Drachten:

“As I watched the intricate social ballet that occurred as cars and bikes slowed to enter the circle (pedestrians were meant to cross at crosswalks placed a bit before the intersection) Monderman performed a favorite trick. He walked, backward and with his eyes closed, into the Laweiplein. The traffic made its way around him. No one honked, he wasn’t struck. Instead of a binary, mechanistic process – stop, go – the movement of traffic and pedestrians in the circle felt human and organic.”

It may be counterintuitive, but the finding in Drachten has been that since it dispensed with such road safety measures the traffic system has become far more efficient. Traffic flow has doubled while the number of fatal road accidents has fallen (by 100%, to zero). Moreover, similar results have been reported wherever such schemes have been tried across Europe – in Germany, Sweden, the UK. Broadly speaking, traffic speeds have declined, the incidence of traffic accidents have fallen and traffic flow has increased.” – Dylan Grice, Popular Delusions, June 2012

Indeed complex systems such as “ traffic lights ” and banking regulations as well when it comes to “ratings” for sovereign risk give you the “illusion of safety” (SVB debacle anyone?).

In his 2012 time piece Dylan Grice asked the right questions:

“But what would have happened if banks had never been given capital ratio targets? What if they’d been told that if they got into trouble they’d go bankrupt, like any other business? Wouldn’t they have been more careful about what they were buying? Wouldn’t they have paid more attention to the price they were taking? I’m quite sure they wouldn’t have let their guard down so easily. Behaviour at the micro level would therefore have remained more consistent with robustness at the macro level because individual banks would not have been seduced by the illusion of safety. Just as the residents of Drachten do today, they would have felt less safe, and been safer for it.

"Risk free" - US Treasury (Dylan Gryce, Popular Delusions, SG Cross Asset Research)

-

- Graph source – Dylan Gryce, Popular Delusions, SG Cross Asset Research

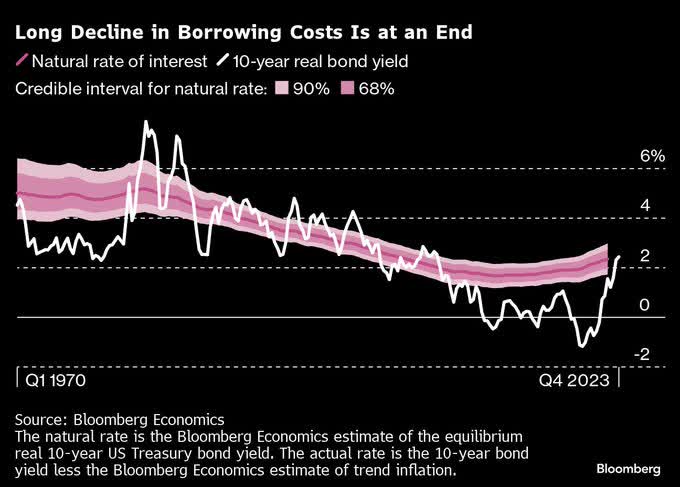

Sure, you might find solace in thinking that “risk free” still exists in “Brigadoon”, but, good luck in finding the village of “Brigadoon” again:

End of long decline in borrowing cost (Bloomberg - X/Twitter)

{kind=link}

-

- Graph source Bloomberg – X/Twitter

As we posited earlier in our conversation, when it comes to the “Brigadoon” period of ZIRP, “risk free” was not challenged given that time was not given any “value” by our sorcerer’s apprentices aka our central bankers. Not anymore. For instance, Bloomberg estimates that at the end of last month, estimated annual interest payment on US government debt topped $1 trillion. This amount has doubled in the past 19 months and is equivalent to 15.9% of the entire federal budget for the fiscal year of 2022.

But returning to the case for multiple currencies in a growing multipolar world, surprisingly most financial pundits do not take into account “gold arbitrage” (akin to “variation margin” we find in futures trading we think). The gold flow due to trade deficit dictates FX movements, regardless of fixed parity or not. Interest rates differential are a secondary factor in such a floating currency system.

Many people look at the Gold spread between New York and Shanghai are somewhat puzzled. For those living in books, it’s actually a standard feature of pre-gold standard local currency trading with the discharge of Bills of Exchange. It would be evidence that local currency trading has started again (the discharge creates the spread), we use the extract from the book of Henry Thornton in 1802, discussing local currency trading, bills of Exchanges, and trade deficits forcing a discharge and creating a Gold spread. The situation is interesting because the situation is similar to today in many ways (the UK is on fiat in 1802)

“One never notices what has been done; one can only see what remains to be done.” - Marie Curie

For further details see:

Brigadoon