MRTX - Bristol-Myers' Mirati Takeover: Pharma Is Either Buying Crown Jewels Or A Dud

2023-10-09 12:00:33 ET

Summary

- Bristol-Myers Squibb has announced its acquisition of Mirati Therapeutics and its lead drug candidate KRAZATI for a potential value of $5.8 million.

- BMY paid a 52% premium to Mirati's share price with other Pharmas - e.g. Sanofi - rumored to be interested.

- The acquisition allows BMY to bolster its oncology portfolio and potentially expand the label of KRAZATI into first-line lung cancer and colorectal cancer.

- As one of only two approved KRAS targeting drugs, KRAZATI has enormous potential, but recent disappointments in the clinic also imply it might be a dud.

- The buyout covers other assets including another KRAS inhibitor. BMY will hope it can use its substantial R&D resources to revive a pipeline that once commanded a >$15bn valuation.

Over the weekend Bristol-Myers Squibb ( BMY ) announced that it would acquire Mirati Therapeutics ( MRTX ) and its KRAS targeting lead drug candidate KRAZATI in a deal whose value could reach $5.8m.

BMY paid a 52% premium to Mirati's 30-day traded share price to get the deal done, amid speculation other Pharmas would bid for Mirati - but is the bigger Pharma under, or over-paying? I discuss the deal and its prospects in depth in this post.

Investment Overview

Back in November last year I covered Mirati Therapeutics in a note for Seeking Alpha, titled "Is There A Big Pharma Buyout In Play And What's The Price Tag?".

Mirati is a San Diego based biotech, best known for succeeding where countless other biotechs and drug discovery companies could not, and developing a drug candidate - MRTX849 - capable of targeting the Kirsten rat sarcoma virus, or KRAS.

KRAS is part of the RAS/MAPK pathway, where it is involved in signalling and cell proliferation, and can often become mutated - as stated in Mirati's Q2 2023 10Q submission (quarterly report):

The RAS family of genes is the most commonly mutated oncogene and mutations in this gene family occur in up to approximately 25% of all human cancers. Among the RAS family members, mutations most frequently occur in KRAS (approximately 85% of all RAS family mutations). Tumors characterized by KRAS mutations are commonly associated with poor prognosis and resistance to therapy.

MRTX849 is a "commercially available, selective, specific, potent and orally available KRAS G12C inhibitor, designed to directly inhibit KRAS G12C mutations", the 10Q continues, and in December last year the drug was approved under the brand name KRAZATI, for use by adult patients with KRAS G12C-mutated locally advanced or metastatic Non Small Cell Lung Cancer ("NSCLC"), as determined by an FDA-approved test, who have received at least one prior systemic therapy.

Prior to the approval, there had been speculation that Mirati was a potential takeover target for a Big Pharma concern - as I wrote in my last note:

Bloomberg News has reported that management has been considering a sale for some time, and the suggested bid price could be as high as $185 - $200 per share, according to JPMorgan analysts, with pharma giants Merck ( MRK ), Pfizer ( PFE ), Bristol-Myers Squibb ( BMY ) and AstraZeneca ( AZN ) all interested.

Nevertheless, Mirati's approval date arrived, KRAZATI secured a historic approval as only the second KRAS targeting drug to make it to market - after Amgen's ( AMGN ) LUMAKRAS - and no formal bids were made for the company.

When the hype around a KRAS targeting drug was at its peak, back in mid-2021, when Amgen and Mirati were racing to the approval finish line, Mirati stock traded at >$235 per share, valuing the company at >$15bn.

Doubts around the efficacy, durability, and versatility of either of Amgen or Mirati's KRAS drugs began to surface, however, primarily centered around the drugs duration of response, and also about their ability to work as a first line therapy or in combo with Merck's legendary, >$20bn per annum selling immunotherapy Keytruda, with clinical studies delivering uncertain results that did not suggest a "best-in-class" profile in any indication outside of 2nd line NSCLC - a population of ~7k patients.

By the time the FDA's "PDUFA" approval decision date of December 12th arrived, and the agency granted KRAZATI an accelerated approval, Mirati stock had shrunk to a low of $45 per share - down >80% from its former highs.

Why Has Bristol Myers Moved For Mirati?

Last week, rumors were circulating that French Pharma giant Sanofi ( SNY ) was considering a bid for Mirati, but with a small oncology division that generated only ~$1bn in annual revenues in 2022, it certainly seems to make more sense that Bristol-Myers Squibb ultimately had a bid of $58 per share accepted by Mirati, given BMY markets and sells 12 cancer drugs, that generated a combined ~$28bn of revenues in FY22.

Since BMY shares hit an all-time high of $81 in November last year, they have performed poorly, for 2 main reasons. The first is patent expirations - BMY's revlimid, which earned revenues of $12.8bn in 2021, lost its patent protection last year, meaning generic versions of the drug can be sold and marketed by other companies.

This inevitably drags down the price and sales volumes of the original drug - revlimid generated revenues of $10bn last year, but in 1H23, only $3.2bn. The only drug that contributed more towards BMY's total revenues in 2022 - the blood thinner eliquis, which earned $11.8bn, is also due to lose its patent protection after 2026.

The second reason is the Inflation Reduction Act ("IRA") introduced by the Biden administration last year, which allows the Centers for Medicaid and Medicare ("CMS") to participate in drug pricing negotiations for the first time. The CMS and Department for Health and Human Services ("HHS") recently announced the first ten drugs it will begin participating in pricing discussion for, and eliquis is top of the list , given it accounts for the highest Medicare spend of any drug - ~$16.5bn divided between ~3.7m enrolled members.

Rumor has it that the CMS will likely select BMY's cancer drug opdivo on its next list of 15 drugs subject to price negotiations, and opdivo generated $8.2bn of revenues for BMY last year, or ~18% of its total revenues. The CMS will be determined to drive down the prices charged by BMY for both eliquis and opdivo, with the net effect being that profit margins may slide at the company, and shareholders' profits will decrease.

Thanks to its mega-money acquisition of Celgene in 2019, and its late stage product portfolio, BMY has been able to develop an entirely new product portfolio, consisting of 9 drugs that management believes can drive >$25bn of revenues by 2030, offsetting any losses from falling sales of Eliquis, revlimid, opdivo and other patent expired drugs such as one-time >$3bn p.a. selling pomalyst.

In a p revious note on BMY for Seeking Alpha I have shared product by product revenue forecasts for BMY's assets, and used forward income statements and discounted cash flow analysis to suggest that BMY stock ought to be worth ~$90 per share today based on its potential 2030 revenues.

In reality, however, the risk that one or two assets fail to achieve their peak sales expectations, or that several late-stage pipeline assets - including a NSCLC therapy, reprotectinib - fail to make it to market, is high, and therefore BMY was always likely to want to make further M&A deals in order to derisk its current portfolio, and reassure investors.

What Can BMY Achieve With Mirati's Approved, Clinical, and Preclinical Stage Product Portfolio?

As mentioned, BMY is an oncology powerhouse that is looking to reinvigorate a portfolio suffering from new pricing controls and patent expiries, so in that sense the acquisition of Mirati is a great deal for the Pharma.

KRAZATI is already approved and earning revenues, and the good news is that the drug appears to be performing well in the second line NSCLC market since launch, with Mirati reporting at the end of Q2 2023 that:

Net KRAZATI® product revenue for the three and six months ended June 30, 2023 was $13.4 million and $19.7 million, respectively

Amgen's Lumakras - which was approved in May 2021, 18 months before KRAZATI - earned $285m of revenues in FY22, but KRAZATI sales have outperformed analysts' expectations, while Lumakras' sales have flatlined, falling 2% year-on-year in Q2 2023 in the US to $51m, and rising just 4% in new territory Europe, to $26m.

Last week, an FDA panel was critical of Amgen's confirmatory study results for Lumakras - as a reminder, a confirmatory study must be completed after an accelerated approval is awarded by the agency, and if this trial does not succeed, the product risks being withdrawn from the marketplace. The committee voted 10-2 that data from Amgen's CodeBreak 2000 trial "could not be reliably interpreted.

This may therefore hand a significant advantage to KRAZATI, although it should be noted that KRAZATI itself has an accelerated approval only, and that the drug was recently rejected for approval in Europe. Nevertheless, BMY has acquired a drug that is growing revenues faster than expected, that fits in nicely with its oncology portfolio, and may have blockbuster (>$1bn revenues per annum) potential.

The bulk of BMY's cancer drugs - opdivo, CTLA-4 blocker Yervoy, and LAG-3 blocking opdualog - are immunotherapies, whilst KRAZATI is a targeted drug, like reprotrectinib, whose approval decision data arrives at the end of next month, in NSCLC, providing an opportunity for BMY to establish a significant share of the largest cancer therapy market.

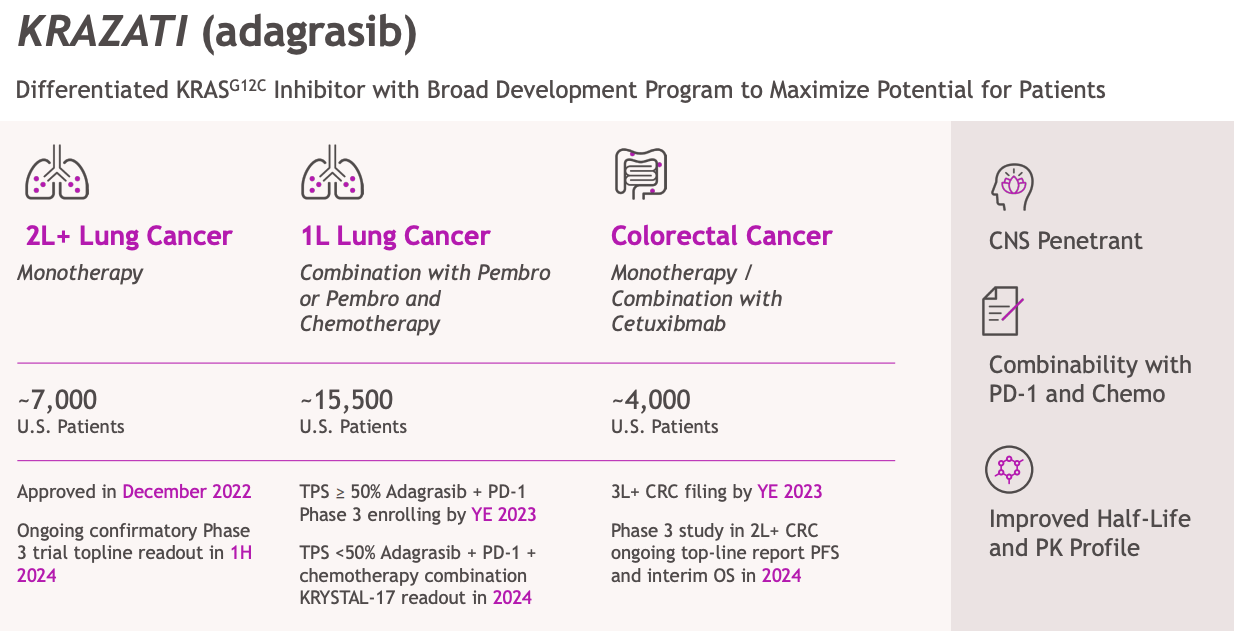

{kind=link}

As we can see above in this slide released by BMY as part of its Mirati offer presentation, BMY believes it can expand the label of KRAZATI into first line lung cancer, and colorectal cancer.

An expansion into first line NSCLC will triple the drug's current addressable market, although it's interesting to note that BMY's slide discusses doing this as part of a combo therapy alongside pembrolizumab - Merck's Keytruda, which happens to be the key rival of BMY's opdivo, which has the same mechanism of action, being a PD-1 targeting immunotherapy. Perhaps, BMY will try to make KRAZATI work alongside opdivo also.

Regarding the rest of Mirati's portfolio, MRTX1719 is a potentially exciting prospect, being a PRMT5 inhibitor that is indicated for MTAP deleted tumors. Like KRAS, MTAP deletions are commonly expressed in a wide range of tumors, and the drug is already in early studies - both as a monotherapy and in combo with other drugs - in NSCLC, melanoma, cholangiocarcinoma, and mesothelioma.

As part of the takeover deal, BMY has pledged a non-tradeable contingent value right ("CVR") for each Mirati share, worth $12, related to MRTX1719 - if the drug secures approval in either later stage locally advanced or metastatic NSCLC within seven years of the takeover, the CVR will convert, and Mirati shareholders will divide a windfall of ~$1bn between them.

Finally, Mirati has a second generation KRAS inhibiting drug candidate, MRTX1133 in Phase 1 studies, again as both monotherapy and combo, indicated for pancreatic, Colorectal cancer ("CRC"), NSCLC and potentially others besides these, and an SOS1 inhibiting candidate in Phase 1 studies in solid tumor cancers.

Concluding Thoughts: Assessing Value Of Deal For Mirati & BMY Shareholders - Better For BMY In My View

In my July note on BMY titled "Back In The Doldrums - Or Just Pausing For Breath?" I expressed some concerns around BMY's prospects for growth being dependent on a large number of newly approved, or late stage drug candidate with peak sales expectations between ~$2 - $4bn to replace falling sales of 2 drugs in eliquis and revlimid that commanded double digit billion dollar sales at their peak. We could also add opdivo, and its >$8bn of annual sales, to that list, given the likely IRA pricing pressure and circa 2028 patent expiry.

BMY's deal for Mirati does not immediately seem to address that problem, given KRAZATI is unproven in the marketplace, earning <$20m of revenues last quarter, does not have a full approval, and is not approved at all in Europe.

BMY will believe however that it can make a KRAS targeting drug work. The fact that Mirati's and Amgen's data in relation to its KRAS inhibitors has been just about good enough to scrape approval in 2nd line NSCLC, but appears underwhelming in other indications, has allowed BMY to perhaps pay significantly less for Mirati's business than it would have had to pay 2 years ago, but now the onus is on BMY to unlock the value Mirati has been struggling to find.

There is no question that KRAS is a prized target and that KRAS mutation are expressed in a wide range of cancers. If BMY can somehow find ways to make KRAZATI work better in clinical studies as monotherapy and combo, there is an outside chance that Mirati's lead asset could win multiple approvals, and become another opdivo, eliquis or revlimid for BMY - a double digit billion dollar selling asset.

The Pharma has more resources to throw at KRAZATI than Mirati ever had. The additional early stage assets intrigue also - could MRTX1133 prove to be the drug candidate that the market once thought KRAZATI was? Ultimately, however, this deal is not without risk and the entire $5bn is at risk of being written off if KRAZATI cannot deliver in the clinic.

This feels a little like the type of deal BMY shareholders may have to start getting used to in the post-Celgene era - single-digit billions in value, somewhat speculative, and not bringing much in the way of near-term revenues. It is not ideal for shareholders, but if the gamble does pay off it could give BMY the edge in NSCLC and other solid tumor cancers for a decade or more in my view.

My perspective on the deal is that it is a good one for BMY, who can challenge itself to extract the maximum value from a drug candidate that once drove Mirati's valuation >$15bn, having paid just $58 per share, plus the CVR. For Mirati shareholders, it may feel like a disappointment, but it may also feel like an escape, given problems were mounting in the shape of rejection in Europe and struggles to make meaningful progress in the clinic.

KRAZATI, and Mirati's other assets have more chance of succeeding under the watchful eye of BMY's R&D division, and BMY can absorb losses better if it is unable to win the battle to succeed with a KRAS drug. Therefore, the deal makes sense, although Mirati shareholders may feel like they sold the family jewels before ever really discovering how valuable they may have been.

For further details see:

Bristol-Myers' Mirati Takeover: Pharma Is Either Buying Crown Jewels Or A Dud