MRTX - Bristol Myers Squibb: This Dividend Contender Is A Steal Right Now

2023-12-19 15:00:00 ET

Summary

- Bristol Meyers Squibb's stock is down nearly 15% over the past 3 years and currently trades at a price to earnings of less than 15x, indicating it is undervalued.

- BMY recently announced a deal worth $8.4 billion and another deal to acquire a biotech company, signaling their commitment to growth.

- BMY's dividend is well-covered, with a safe payout ratio of roughly 41%, and the company has increased its dividend by 5.3%. They also have a flexible share repurchase program.

- The pharmaceutical giant continues to face risks with upcoming drug expirations, but the company is well-positioned to mitigate these risks financially.

Introduction

If you've been invested in Bristol Myers Squibb Company ( BMY ) over the past few years you're probably not happy with your return. Pharmaceutical companies are considered controversial and can often lead to some big losses if you're not careful. But on the other hand, they can also lead to some large capital gains. Case in point: BMY's peer, Pfizer Inc. ( PFE ), whose stock soared during the pandemic but has declined more than 50% in the last year alone. Bristol Myers also saw their price increase during COVID but has not had near the price decline PFE saw during the same period, speaking to their quality.

One thing to consider with big pharmaceutical companies is that they tend to make large and frequent acquisitions to sustain growth over a long period. Shareholders are often worried that these companies overpay for such and this can lead to a huge drop in price. However, these significant price drops can often lead to great buying opportunities, especially if the stock is of high quality. In this article, my co-author and I, The Gaming Dividend, get into why BMY is currently a bargain and steal for long-term dividend investors.

This article was co-authored with The Gaming Dividend.

The Stock Is A Steal At The Current Price

Every once in a while a high-quality business goes on sale for whatever reason. As investors, we know these typically trade at premiums, some larger than others. Over the last 3 years the stock is down nearly 15% and currently trades at a price to earnings of less than 15x. We bring this up because the father of value investing, Benjamin Graham, stated you should never pay more than 15x earnings for a stock. BMY's forward P/E Non-GAAP of 6.88x is less than their 5-year average of 9.57x, signaling it's undervalued. If you use and believe in the dividend yield theory, then by that metric it signals the stock is also undervalued.

BMY recently announced a deal worth $8.4 billion with SystImmune, a U.S.-based enterprise company of Chinese drugmaker, Sichuan Biokin Pharmaceutical. Additionally, they announced a deal back in October to acquire Mirati Therapeutics, Inc. ( MRTX ), a biotech company developing therapies for cancer treatment. This is expected to close by the 1H of 2024. Since then the stock has declined further from a price of roughly $56 to its current of $50.60 at the time of writing.

The pharma giant reported its Q3 earnings on October 26th and although they beat analysts' estimates on EPS with revenue in-line, they cut their revenue forecast for next year from $3.9 billion to $3.2 billion. Furthermore, they reported their fifth consecutive loss in quarterly revenue due to the drug Revlimid experiencing a significant decline as it went generic earlier this year. They now expect $10 billion in 2026 vs the $10-$13 billion prior. As patents expire, this creates volatility in revenue for pharmaceutical companies. Fellow analyst Thomas Potter went into detail about the potential patent loss in his article on BMY published in November. But despite that, the quarter was solid for the company.

EPS of $2.00 beat estimates by $0.23 while revenue of $10.97 billion was in-line. EPS grew from $1.75 in Q2 but revenue declined slightly from $11.2 billion. Revenue was also down nearly 4% from $11.41 billion in Q4 of 2022. During the quarter, management increased the mid-point of their Non-GAAP EPS guidance and narrowed the range to $7.50 - $7.65. The problem with pharmaceutical companies is that sometimes adopted products take longer than expected.

Companies like BMY and their peers invest in these products for their long-term potential but for some, it takes time to be accretive. For example, this happens during drug development and trials. And sometimes products are unsuccessful, causing the business to pivot to continue growth. All these things combined could be considered negative and cause the stock's price to face downward pressures, sometimes for a prolonged period. But that's why we believe things like a safe payout ratio, a strong balance sheet, and a great management team are important.

Dividend Is Well-Covered

The good thing about investing in dividends is that although the stock may be down, a well-covered dividend ensures your (dividend) payment is sustainable for the long term. If the stock is down a hefty amount, you could still be at a loss, but collecting dividends does help alleviate the short-term pain somewhat. BMY recently announced a 5.3% increase raising their dividend to $0.60 a share. They also grew the cash from operations quarter-over-quarter and year-over-year by 153% & 30%, respectively, which in the current environment is impressive.

Seen in the chart below, BMY's cash from operations was in a steady decline before bouncing back by more than double this last quarter. This brings the total to $9.7 billion YTD. With a CAPEX of $879 million YTD and nearly $3.6 billion in dividends, this gives them a very safe payout ratio of roughly 41%, well below the 60% margin for pharmaceutical companies.

{kind=link}

Returning Capital To Shareholders

Bristol Myers initially announced a $2 billion share repurchase program but decided to increase this by an additional $3 billion. This decision further reflects the strength of the pharmaceutical giant's commitment to reward shareholders. What we like about the program is that it is flexible and the company can suspend it or discontinue it at a moment's notice.

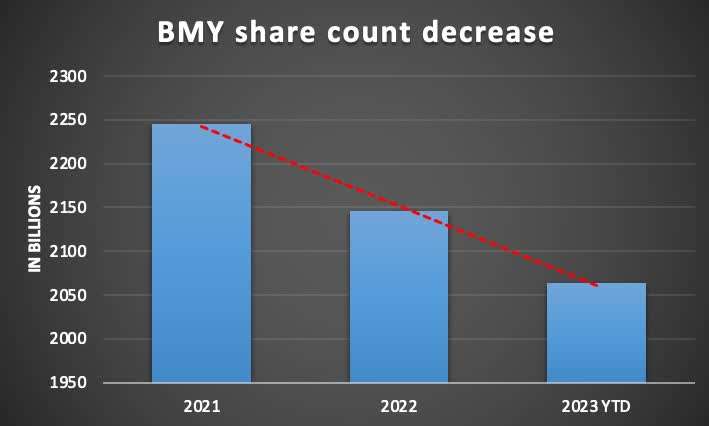

A lot of companies put out a time frame on their repurchase programs but this flexibility allows BMY to allocate capital carefully if say shares become too expensive or an attractive investment opportunity presents itself. Furthermore, the company has been buying back a good amount of shares over the last 2 years decreasing their share count from 2.245 billion in '21 to 2.064 billion YTD. And with the current cheap valuation, we expect management to continue this for the foreseeable future.

{kind=link}

Double-Digit Upside

As previously mentioned, every now and then a high-quality company goes on sale and opens the door for an attractive entry point. We've already mentioned that BMY's forward P/E Non-GAAP of 6.88x is less than their 5-year average of 9.57x, but we can also use another valuation method to confirm that these levels make for an attractive entry. We can also conclude that BMY is undervalued using a discounted cash flow model.

As stated previously, management has a projected EPS guidance of $7.50 to $7.65. Using a conservative outlook, we can use the lower end of this range for our model. Earnings are expected to grow at a slower rate, initially seeing a drop of 2% through 2024, but then a rise of 2.73% through 2025. To average this out, we will use an expected growth rate of 1%. Using these inputs, we see an estimated fair value of $75.75 a share. From the current price level, this would represent a potential upside of nearly 50% to fair value.

Moneychimp

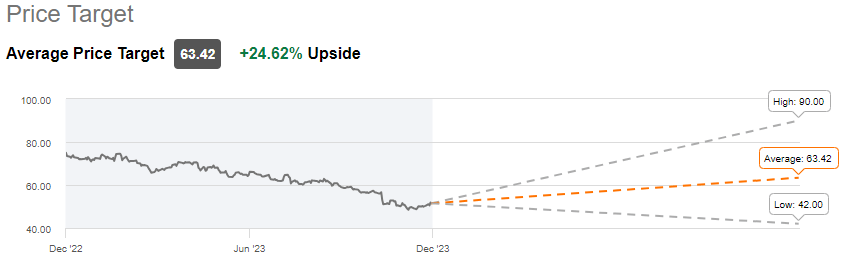

If you need more assurance, the sector median P/E Non-GAAP falls around 19x. For what it's worth, Wall Street's price target range is also optimistic. The highest price target sees BMY reaching $90 a share in the future and the average price target of $63.42 still represents a healthy upside of roughly 25%. This undervaluation, combined with a historically higher dividend yield of 4.7% reinforces that Bristol Myers presents an attractive buying opportunity.

{kind=link}

Risks

The main risk here is a story that we've just witnessed: drug expiry dates. Over the next few years, BMY will have to proactively maneuver into agreements to diversify its product portfolio and soften potential revenue losses resulting from patent expirations, as we've seen with the expiration of Revlimid. A comparable expiration challenge looms for Eliquis as well, a blood-thinning drug that is set to expire in 2026 with the generic version available for sale in April 2028. In 2028, this same challenge will take place once again with Opdivo, a cancer immunotherapy drug.

Currently, both of these products stand as significant contributors to BMY's revenue. Understanding the strategic moves BMY makes in response to these challenges provides valuable insights into how the company navigates uncertainties and prepares for the future. BMY's proactive measures to secure new agreements, explore innovative collaborations, and possibly invest in research and development can signify its commitment to maintaining a robust product portfolio despite patent expirations. This adaptability is crucial for sustaining revenue streams and ensuring the company remains competitive in the pharmaceutical landscape.

While the potential risks associated with patent expirations are significant, BMY's current financial position offers a degree of reassurance. The company's ample cash reserves of over $7 billion and resources provide a buffer, affording them time and flexibility to address upcoming challenges. This financial strength enhances BMY's ability to invest in new opportunities, research, and development initiatives, ultimately mitigating the impact of patent expirations on their overall financial performance.

Takeaway

Bristol Myers Squibb Company ((BMY)) emerges as an attractive buying opportunity with several factors pointing towards its potential as a solid long-term candidate. BMY is currently trading at an attractive valuation so investors with a long-term outlook get the potential for not only double-digit upside, but a safe, and growing dividend to help them sleep well at night. This undervaluation is further supported by a discounted cash flow model, suggesting a potential upside of 50% to fair value.

The challenges posed by impending drug patent expirations, as exemplified by Revlimid, Eliquis, and Opdivo, necessitate strategic maneuvering. However, deals with SystImmune and Mirati Therapeutics show the company's adaptability. This along with their ample cash reserves mitigates the risks associated with these expirations.

In light of the risks and opportunities, BMY presents a compelling case for investors seeking a high-quality and undervalued stock with a solid dividend yield. Furthermore, management recently increased their buyback program which not only shows their financial strength, but that they will continue to grow earnings while rewarding their shareholders. The company's proactive measures and growth potential make it a stock worth considering for those looking to capitalize on the pharmaceutical giant's long-term prospects.

The Dividend Collectuh and The Gaming Dividend are individual investors with a keen interest in dividend investing. Both have been published independently here on Seeking Alpha.

For further details see:

Bristol Myers Squibb: This Dividend Contender Is A Steal Right Now