BATMF - British American Tobacco: 9% Yield For Income Investors

2023-11-17 09:00:00 ET

Summary

- British American Tobacco has experienced a significant decline, raising concerns about whether it is a value trap.

- BTI's financials show a strong balance sheet and impressive margins, indicating a solid company.

- The company's success in the New Categories segment and its ability to adapt to changing market dynamics make it a promising investment option.

- We added an additional strategy to increase your yield above 25% potentially.

- As such, we currently rate BTI as a buy.

Introduction

British American Tobacco ( BTI ) takes pride in its impressive collection of cigarette brands that even non-smokers often recognize, including iconic names like Camel, Newport, and Lucky Strike. These brands have left an indelible mark on the cigarette market, making them more than just products but symbols in their own right.

However, it's essential to bring a personal perspective to this recognition, especially in the face of the persistent long-term shift away from smoking. While BTI is diligently working to align with evolving consumer preferences, as individual investors, we must stay acutely aware of the potential risks associated with a declining cigarette business. It's not just about numbers; it's about making choices that resonate with our values and understanding the bigger picture of this industry's transformation.

BTI has experienced a significant decline and is now down 27.98% since its high. As such, one has to ask himself if this 9% yielding company isn't a value trap.

Furthermore, if it isn't a value trap, this might very well be a Buffett-style investment at the current price, with a strong yield to lock in for your retirement.

YCharts

In this article, we will review BTI's historical financial numbers, how it evolved, its most recent earnings, and analyst expectations in the coming years.

Financials

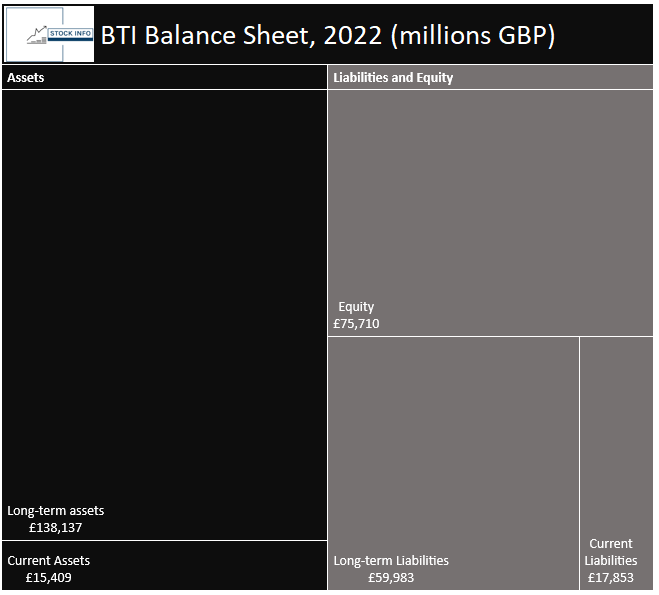

We would like to start by looking at BTI's Balance sheet as of the end of 2022, shown in the figure below. There are quite a few things to like about it. For instance, you will notice that their equity holdings are greater than their long-term debt at £75,710M and £59,983M, respectively.

In addition, BTI has many of its assets tied in the long term, which may not surprise a company as old as BTI. Interestingly, about £129,075M are tied up in intangible assets, with about £48B being goodwill. While having that much value tied up in goodwill and intangibles is not always beneficial, the amount is relatively stable from 2018-2022.

However, as we briefly mentioned in the introduction, BTI has many well-recognized brands under its umbrella, which is a point of attraction for the stock.

{kind=link}

In the table below, we calculated a few "checks" that help us evaluate BTI's balance sheet quality. First, BTI has had more current debt than cash since 2018. While companies don't need more cash than debt, it is usually a sign that great companies can generate cash without needing much debt. It should be noted that the discrepancy between the two has been shrinking overall and could turn positive by the end of 2023.

Finally, BTI's retained earnings have grown consistently from 2019 to 2021, with a dip in 2022. While we want consistent growth, a single year with a fall of -0.3% is not a cause for concern.

Stock Info

It's essential to remember that these calculations merely give an idea of their balance sheet. However, they can be instrumental as a quick overview. Plenty of caveats exist to the usefulness of these calculations.

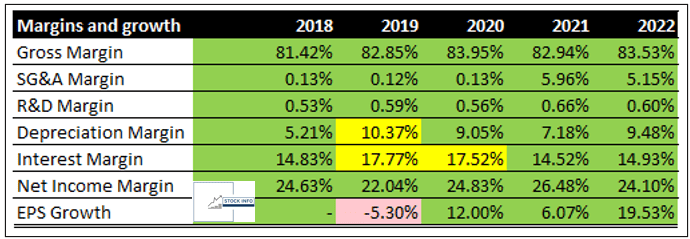

Regarding their income statement, we calculated different margins and color-coded them to show whether the margins were at satisfactory levels.

The first thing that stands out is BTI's gross margin, that's been well above 80% since 2018, indicating strong pricing power. In addition, they have also managed to keep their SG&A and R&D margins below 1%, except in 2021 and 2022. Still, anything under 20%, we are happy with.

BTI has been paying a significant amount of interest compared to its operating income. We prefer this to be around 15% or under, and therefore high 17% is still decent, and as we can see, they have kept it under 15% since 2021.

BTI also has an impressive net income margin, well above our 20% threshold that we want strong companies to have. In addition, they have had significant growth in their EPS, which is yet another sign of a solid company. Net income margin is a crucial metric for Buffett's Berkshire Hathaway when making investment decisions.

{kind=link}

Lastly, when evaluating their 5-year CAGRs on revenue, operating FCF, FCF, and dividends, it's pretty clear BTI is not growing their topline significantly. Neither is their free cash flow.

They make up for this by growing their paid dividends. An almost 2.5% CAGR on dividends paid is very robust when you are looking to allocate your wealth to a dividend-paying company.

Stock Info

As we look at the performance in the first half of 2023, BTI continues to face a decline in its total combustibles volume, which is down 4.9% compared to the previous year.

BTI Half-Year Report, 2023

What's particularly noteworthy is BTI's success in the New Categories segment. Revenues in this category have reached £1.65B, an overall 26% growth compared to the previous year. This impressive growth aligns with BTI's expected £5B target for this segment by 2025. These numbers underscore the company's exceptional performance under the guidance of its new CEO. In addition, it highlights their ability and willingness to pivot into new areas to keep their revenues flowing.

Given BTI's New Categories segment's substantial contribution to its overall revenue, there is no need for concern about its relatively slower growth rate than its competitors. BTI should be able to build upon this in the coming years quickly. The company's management has already guided that profitability in this segment will be achieved by 2024. This reinforces confidence in BTI's strategy and its ability to adapt to changing market dynamics.

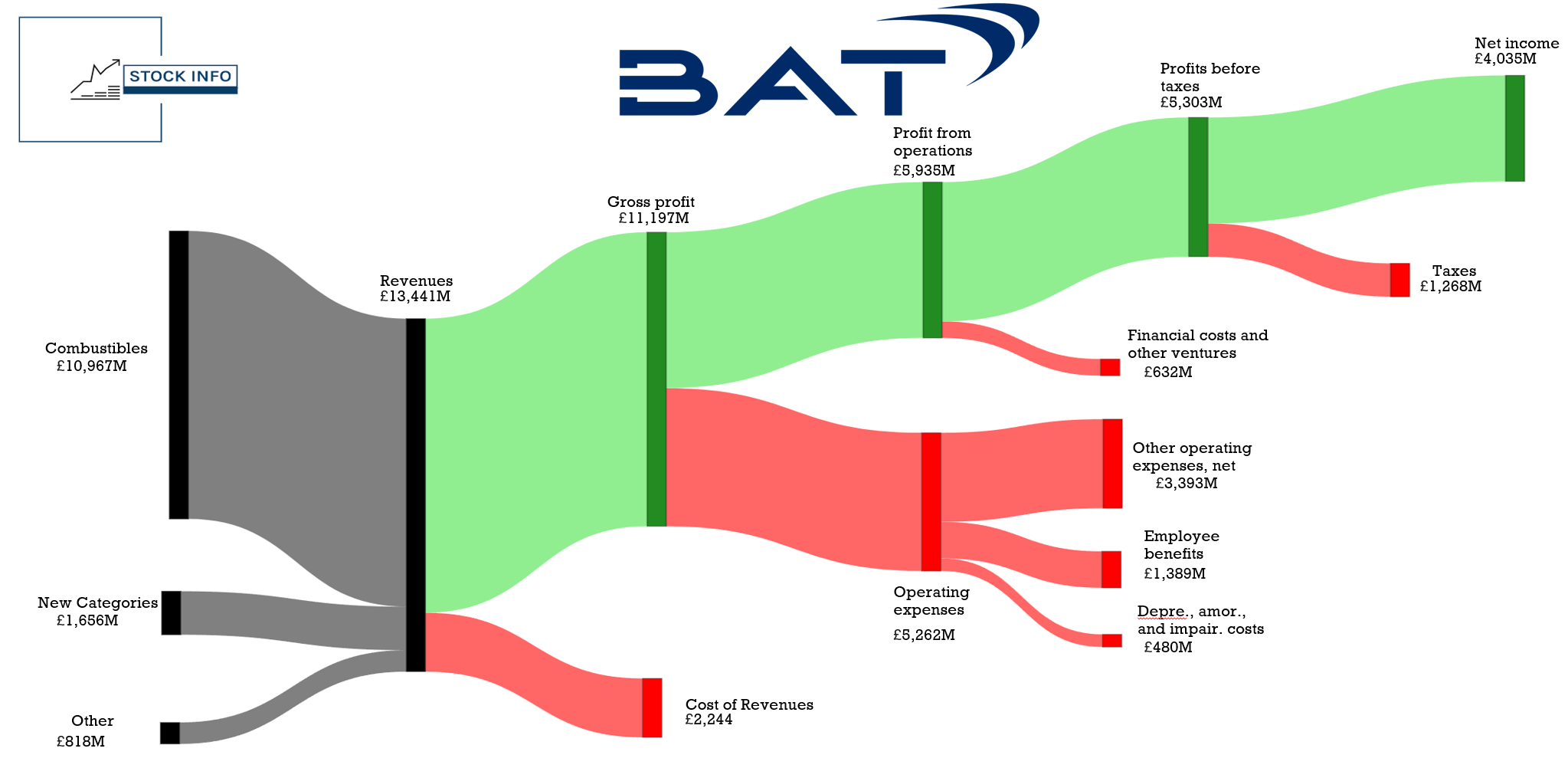

Below is a graph showing BTI's income statement and where its cost lies. It may not be surprising that most of their expenses are operating expenses.

{kind=link}

If we look forward to the end of 2023 and beyond, we first want to highlight BTI's rather extraordinary FCF and dividend yield based on the consensus estimates for 2023.

Stock Info

In terms of the consensus FCF, analysts expect $11B for the year, as per OpenBB, which at BTI's current market cap is a 19.21% FCF yield - a very handsome yield. In addition, BTI has a 10.20% dividend yield based on the expected dividend per share in 2023. These yields highlight the solid foundation for allocating some of your money to this company and earning a decent income from their dividends.

While the consensus forward estimates suggest that the tobacco company may only achieve an EPS of $5.91 in FY2026, the stock's long-term dividend yield remains very appealing. Analysts' expectations suggest a steady growth in the metrics we at Stock Info find the most useful.

Stock Info

When analyzing a company, one of the most important factors to consider is its ability to generate Free Cash Flow ((FCF)). BTI has shown impressive FCF generation in the year's second half, as evident from their past earnings reports .

In the last twelve months, their overall revenues amounted to £28.22 billion, showing a 7% sequential increase, and a Free Cash Flow of £8.09 billion, which is still a robust FCF margin of 28.6%, despite being 4.1% lower sequentially. Lastly, when evaluating their 5-year CAGRs on revenue, operating FCF, FCF, and dividends, it's pretty clear BTI is not growing their topline significantly. Neither is their free cash flow. It is important to remember that BTI is growing their New Categories segment very rapidly.

New Categories can possibly become the segment that carries the company in the future, as combustibles become less and less attractive for the younger generation . BTI has already established this segment quite well, and thus a potential transition to heavier production within the New Categories segment should be relatively easy for BTI.

BTI's management has guided for revenue growth of approximately 4% year-on-year, reaching £28.76 billion, and an adjusted EBITDA margin of 47.7%, a 1.5-point year-on-year increase. This means that the tobacco company may achieve an adjusted EBITDA of £13.71 billion, a 3.8% year-on-year increase. This information can be helpful for beginning dividend investors who are considering investing in BTI.

Overall, we believe the management's exceptional capital allocation strategy, prioritizing deleveraging the balance sheet, effectively navigates the challenges of an elevated interest rate environment.

Compounding on Steroids

As income investors, there is one thing we all enjoy, and that's the compounding effect when we reinvest those sweet dividends. What would you say if I told you that you can generate even more income by using options?

While I'm not typically a dividend investor myself due to unfavorable tax policies regarding dividends in my home country, I'm a big fan of generating capital while holding shares. Yes, most of you probably have heard of this before; in this part, we will discuss covered calls, but this isn't the only thing we will discuss here to generate extra income. In addition to the covered call, we will also discuss the cash-secured put. Held together, these two strategies are called a short strangle.

In general, a short strangle is a strategy used if one wants to capitalize from a stock trading in a specific range over a specific period. In this case, we will use this strategy so that you, the income-seeking investor, generate even more income while holding your shares.

Let's say you don't mind buying 100 shares of BTI at $30 per share on January 19th of '24. At the moment of writing, this cash-secured put gives you $0.95 or $95 in total, as each option contract in the US market has an underlying of 100 shares. This represents a ~16% return on a yearly basis at the moment of writing.

In addition to the cash secured put, we also write a covered call. Let's say we don't mind letting go of 100 BTI shares at $33 per share. If we take the same expiration date (January 19th, 2024), this would give us around $0.25 or $25, representing a 3.40% return on a yearly basis.

In total, this would mean we would have collected an additional $120 on top of the dividends we collected along the way. Keep in mind this is based on a 100-share example. If you want to use this strategy with 1000 shares, you would just sell 10 contracts of each, resulting in a premium collected of $1200.

Given you can do this options strategy a little over 5 times a year, this would generate an additional $600 in income per 100 shares each year. In total to the expected $2.82 dividend for this year, this would give a total of $8.82 per share or a yield of 28%.

Obviously, you can tweak this strategy as you see fit. For example, if you feel like the share price of BTI is getting a bit high, you can decide to sell more covered calls. If you feel like BTI shares are getting too cheap, you can decide to sell more cash-secured puts. For example, right now, the stock is at a relatively low price when compared to its historical price range.

Furthermore, you don't have to hold these contracts till expiration, you can take off one side as you see fit. You must manage this to make sure you roll the contracts in time if you don't feel like letting go of 100 shares or don't want to buy an additional 100 shares due to a change in the fundamentals. In addition, I wouldn't advise doing this on your full position, especially not the put side, due to the risk of a black swan event, for example, the COVID-19 crash. On the other hand, writing CCs too close to the current stock price could set you at the risk of losing your position for only a small gain in case of changing market sentiment.

Conclusion

British American Tobacco presents an intriguing opportunity amidst the evolving tobacco industry. Despite a decline in traditional segments, BTI's financials remain robust, showcasing adaptability in new categories with a remarkable 26% revenue growth.

The 9% yield prompts questions of value, but a detailed analysis suggests a potential Warren Buffett-style investment. Anticipated strong Free Cash Flow and an attractive dividend yield underscore BTI's resilience.

Considering the usage of option strategies like covered calls and cash-secured puts could provide a nice boost for income seekers.

In essence, BTI, with its historical strength and adaptive strategies, emerges as a viable option for stability and income in a transforming market.

For further details see:

British American Tobacco: 9% Yield For Income Investors