RCA - Broadmark And Ready Capital: Distribution Cut Likely To Be Big

2023-03-28 03:28:48 ET

Summary

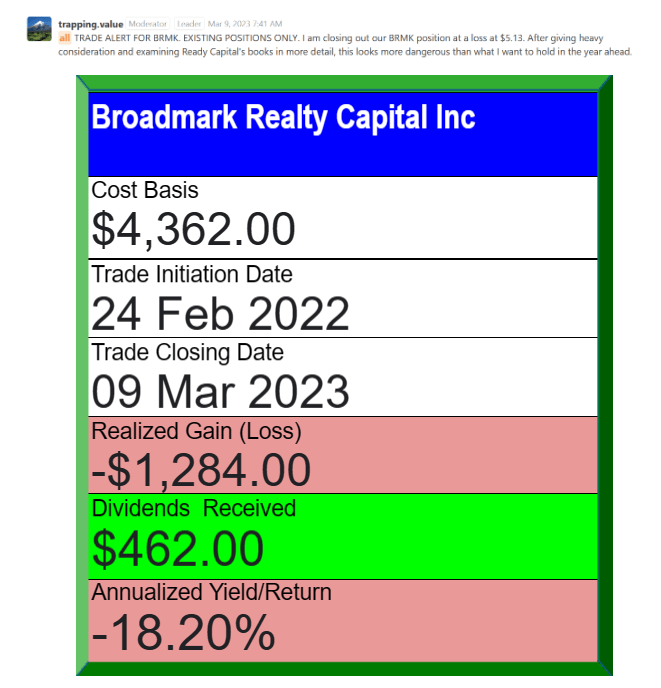

- Our call on Broadmark was horrible, and we were fortunate to get an exit at $5.13.

- We had no desire to own Ready Capital into the recession.

- Ready Capital's higher yield should prove temporary, and we see a high probability of a dividend cut within 12 months.

Sometimes you get the thesis wrong. Sometimes you get it really, really wrong. Broadmark Realty Capital Inc. ( BRMK ) falls in the latter category. We sung its praises when we last covered it and felt that we had three levels of protection and they would serve us well. The discount to NAV, the company's low leverage and our third tier of protection, cash secured puts. We believed that level of safety made our investment safe. Yes, we got that wrong and it was one of our worst calls. But things that hurt also instruct. Let's look at why we got this comically incorrect and how the margins of safety allowed us to still escape with a modest loss vs. what happened to the stock. We will then tell you why investors are about to get another dividend cut from Ready Capital Corporation ( RC ) which is buying Broadmark out.

The Broken Thesis

Broadmark's record as a private company was exemplary. Its public record was anything was quite the opposite. Yes it did have the unfortunate timing of listing near the start of COVID-19, but it also made obvious errors that we should have not excused. For example, it missed multiple opportunities to issue equity above tangible book value. It also delayed the required dividend cut long after it was obvious that it was needed. We should have taken an axe to the bullish view but we stuck with it. One reason was that we felt that our safety buffers would protect us. In a way they did.

Screenshot From Previous Article

In the timeframe shown, Broadmark had a total return of negative 34.25%.

When we hit the exits, on March 9, 2023, we did a bit better.

{kind=link}

That 16% of lower losses came from selling an out-of-the money put. But of course, when things go bad, premiums and buffers are not enough. In the case of Broadmark we had some faith left in the NAV and management's ability to get some value out of that... right until the Q4-2022 results came out. These were announced on the same day that Ready Capital announced the buyout. Ready Capital also released their results at the same time. So there was tremendous confusion.

Broadmark's numbers were horrid.

GAAP net loss of $153.0 million, or ($1.15) per diluted common share, inclusive of goodwill impairment of $137.0 million or ($1.03) per diluted common share and an increased provision for credit losses of $21.5 million or ($0.16) per diluted common share. The change in the allowance for credit losses was primarily due to heightened market volatility and an increase in loans that are expected to foreclose.

Distributable earnings prior to realized loss on investments, of $12.3 million, or $0.09 per diluted common share. Distributable earnings were impacted by increased interest receivable reserves of $3.3 million, or ($0.02) per diluted common share, resulting from interest receivable related to non-accrual loans being deemed not collectible.

Source: Broadmark Press Release

We don't care much about that Goodwill write-down, but the rest of those numbers were scary. Distributable earnings were exactly half of what they were in Q4-2021. We will stress two things here. The first being that the economy was still growing rather strongly in nominal terms in Q4-2022. These results will look far worse in a recession. The second being that Broadmark reduced its distributions by 50% and the new reduced distribution was not covered in Q4-2022. Broadmark paid at a rate of 10.5 cents in the quarter and distributable earnings were at 9 cents.

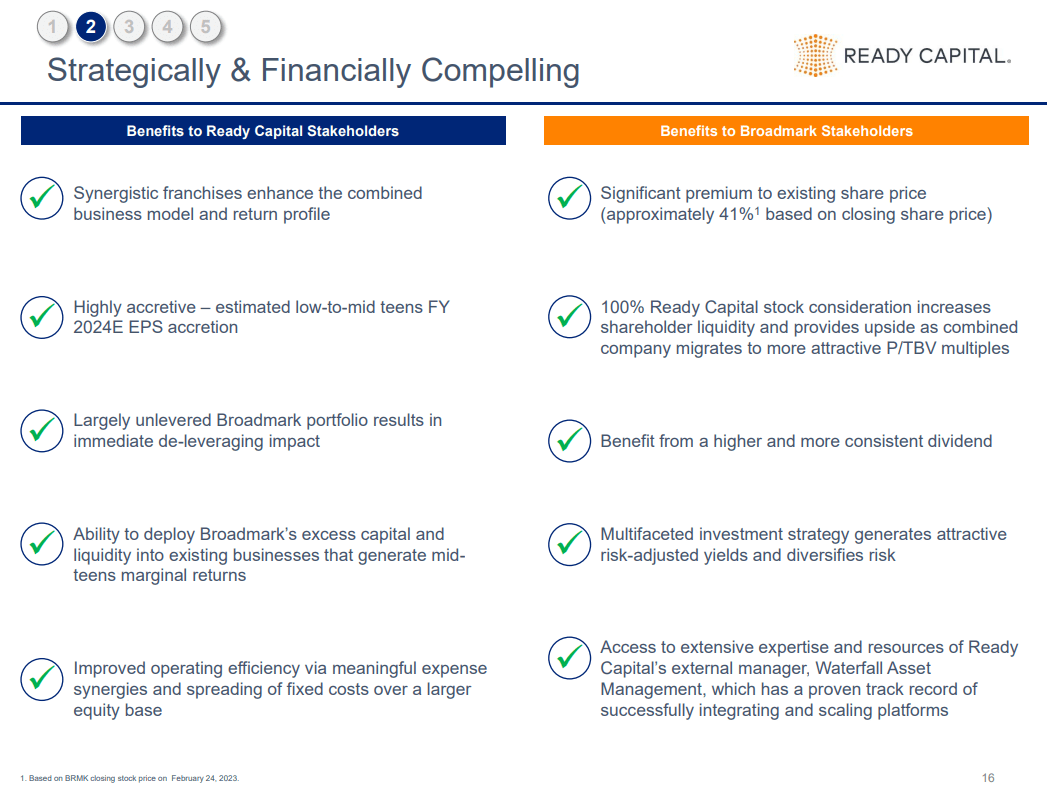

Ready Capital

Broadmark is being acquired at a discount to tangible book value per share. But Ready Capital is issuing its own shares, which are also discounted (though less so).

This nullifies a lot of the advantage. Nonetheless, Ready Capital marketed this as a strongly accretive deal.

{kind=link}

The idea was that the portfolio run-off would give Ready Capital tons of cash. Of course if this was so easy one wonders why Broadmark did not choose to realize this $7.08 in tangible book value. Even assuming this would take two years, and distributable earnings would remain about 9 cents a quarter, the total returns would be $7.68 vs. the exceptionally reduced immediate sale price.

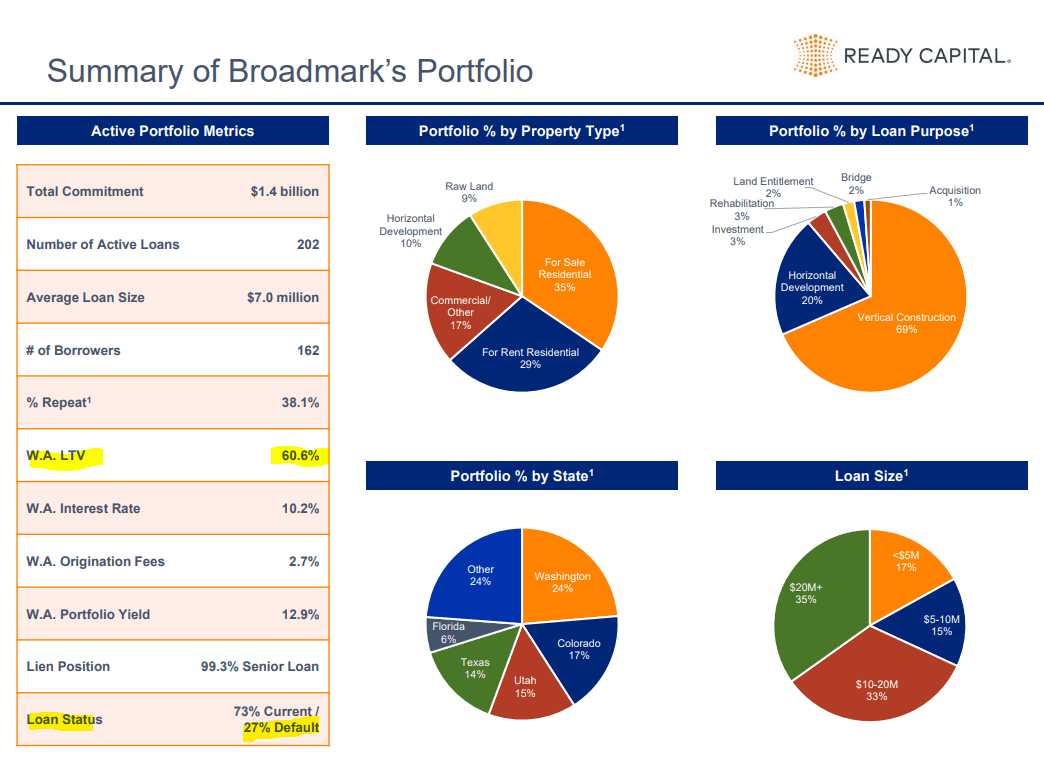

Broadmark probably believed that this was the best deal they could get. That means that the 27% of borrowers that are currently in default will probably expand in the coming quarters. The loan to value of 60.6% would not offer them the cushion that number implies.

{kind=link}

So Ready Capital's work will be cut out as well.

The Dividend Cut Coming Up

There might be some excitement in the Broadmark camp as the dividend yield will jump when Ready Capital shares replace those of Broadmark. Broadmark's yield is 9.4% as we type this and Ready Capital boasts of a 16.3% yield. But that bump will not last.

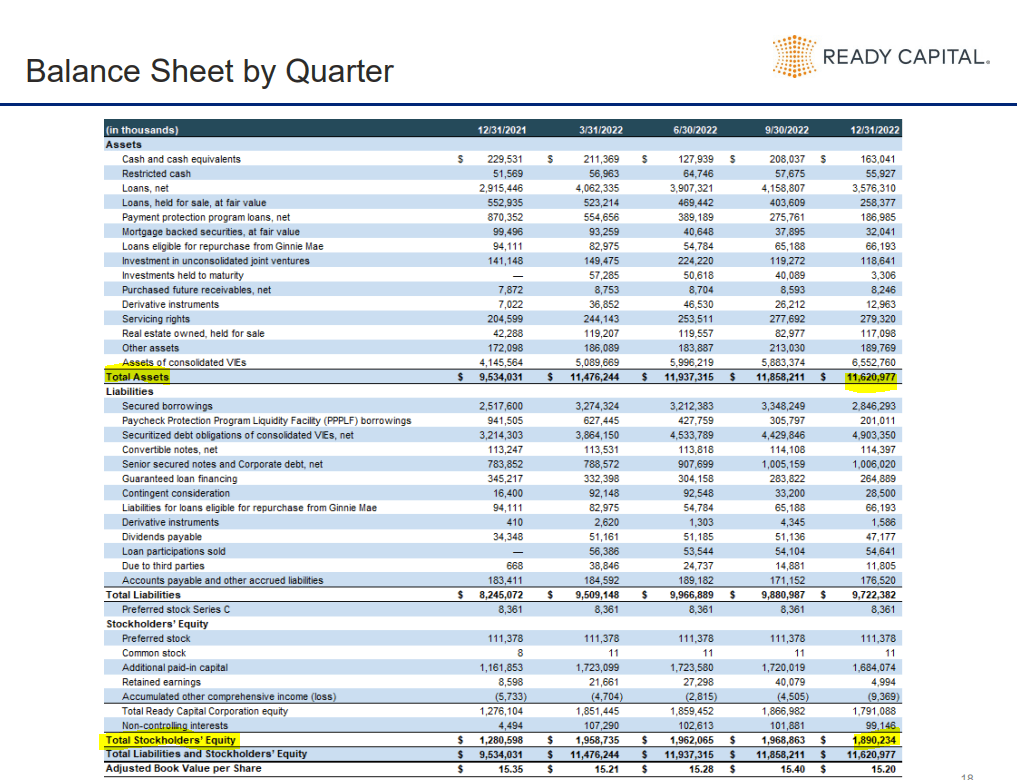

Ready Capital's distributable earnings barely covered the 40 cents of distribution in the Q4-2022 results. If we add Broadmark's numbers to Ready Capital, we are already at a huge shortfall. This can be seen by just adding up their returns on tangible book value. Ready Capital is generating about 11% of distributable earnings on tangible book value while Broadmark just delivered a 5% return in Q4-2022. Considering that Ready Capital's tangible equity is twice that of Broadmark, we can assume that the combined returns will be closer to 9%.

This of course refers to the distributable earnings as defined by Ready Capital. While Ready Capital has outperformed the other mortgage REITs such Annaly Capital Management Inc. ( NLY ) and AGNC Investment Corp. ( AGNC ) over the last decade, its own total return has been lackluster.

This holds whether or not dividends were reinvested.

Split History

2.18% a year without dividends reinvested during a huge bull market is quite weak. So we are fairly certain that even that 9% return on tangible book will not hold up in a recession. Ready Capital was running a 6X equity to assets ratio before the Broadmark acquisition.

{kind=link}

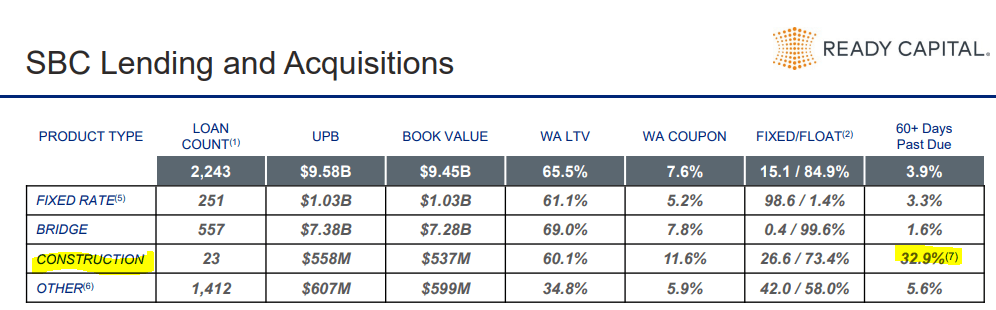

This is lower than the agency REIT average, but the company's assets are also subject to more risks. On its own construction loans (which it got as part of buying Mosaic), it has one-third that are already 60 days past due.

{kind=link}

With a huge amount of CRE exposure on its balance sheet, and an uncovered dividend to start off with, a cut looks inevitable to us. We think 25 cents a share per quarter, next year, looks extremely likely. That would bring the yield back down to Broadmark's current yield. Based on all the information we have looked at, Ready Capital has an "Extreme" level of danger of a dividend cut on our proprietary Kenny Loggins Scale.

Trapping Value

This rating signifies a 50-75% probability of a dividend cut in the next 12 months.

When we invested in Broadmark we were aiming for an unleveraged play on commercial real estate loans. That was obviously an error. We would like to not take that error and compound it by moving into a 6X leveraged commercial mortgage REIT. Hence we took the exit on March 9. We will add here that we actually do own a small position in Ready Capital Corporation 6.25 CNV PFD C ( RC.PC ). We think the deleveraging planned via Broadmark and the likely dividend cut (this should be a big amount), will further bolster the case for owning a security higher up in the capital chain.

For further details see:

Broadmark And Ready Capital: Distribution Cut Likely To Be Big