RCC - Broadmark And Ready Capital: Quite The Deterioration In Q1-2023

2023-05-22 16:01:51 ET

Summary

- Broadmark Reality is being bought out by Ready Capital.

- Ready Capital looked like it was getting a slight deal, but it appears to be the opposite case.

- Distribution pressures will be front and center from the first quarter as a combined company.

- The senior securities look much safer here.

When the marriage of Ready Capital Corporation ( RC ) with Broadmark Realty Capital Inc. ( BRMK ) was announced, we took the opportunity to exit BRMK at $5.13. At the time, there were some question marks around the deal. Notable among them was why BRMK was agreeing to sell itself so far below tangible book value. We concluded that thought process with the following remarks.

Broadmark probably believed that this was the best deal they could get. That means that the 27% of borrowers that are currently in default will probably expand in the coming quarters. The loan to value of 60.6% would not offer them the cushion that number implies.

Source: Distribution Cut Likely To Be Big

We look at Q1-2023 results from both sides and show you why there has been a notable deterioration.

Broadmark

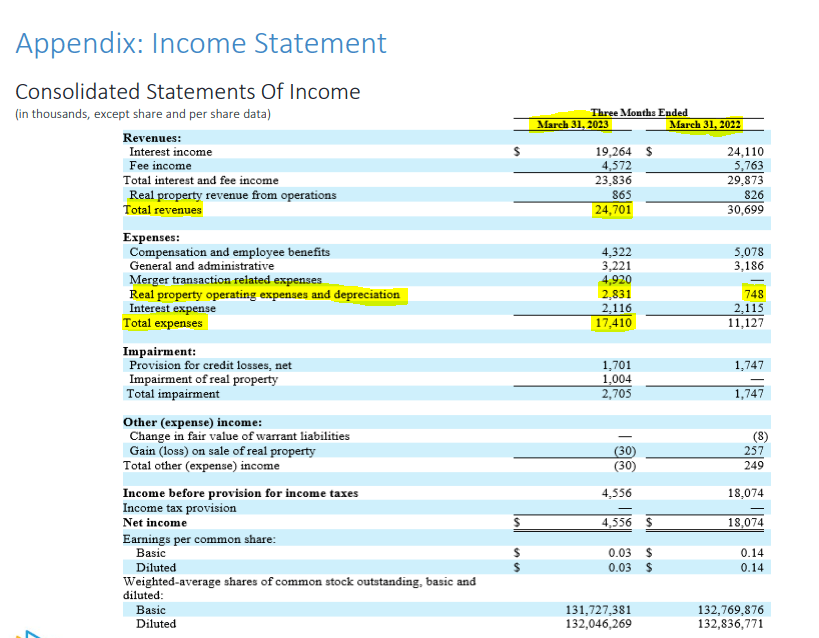

Earnings collapsed in Q1-2023 as interest income dried up, and merger-related expenses showed up.

{kind=link}

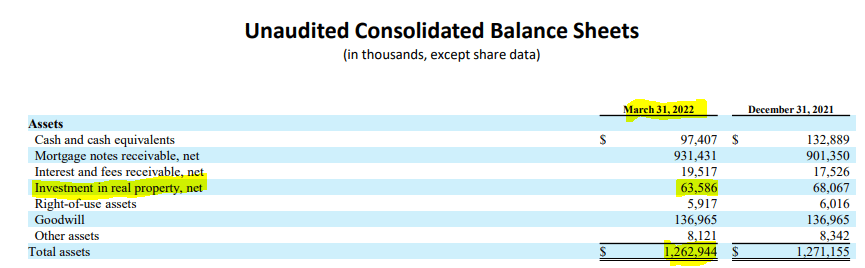

Interest income has dropped consistently over the past year as the company is keeping its portfolio in-run-off mode. But it is more interesting than just that. One year back, this was the composition of BRMK's balance sheet.

{kind=link}

$1.26 billion of total assets, and "investment in real property" was about 5% of that. These are the properties that BRMK had taken over as a result of defaults. The bulk of the total assets were the construction loans (mortgage notes receivable, net) at $931.4 million. Fast-forward to Q1-2023 and things look rather different. We now have two different lines here and they total $191.3 million. Both these represent defaults, with the only difference being whether BRMK plans to sell them right away or not.

{kind=link}

We will note that this is a stunning uplift, even from Q4-2022.

BRMK Q1-2023 Presentation

New loan origination has come to a standstill, and the company is whittling down the portfolio by about $20 million a month.

BRMK Q1-2023 Presentation

Interest earning principal is down to $664.6 million from $895.3 million a year ago and $716.3 million a quarter back.

Effective interest-earning principal of $664.6 million, representing principal balance outstanding of $827 million, plus the excess of minimum interest provisions of $3.5 million and less non-accrual principal of $165.8 million.

Source: BRMK Q1-2023 Presentation

Considering the near certainty of a recession ahead and the lag with which these loans get into trouble versus the economic climate, we think BRMK will ultimately have taken possession of at least 30-40% of the remaining assets. With close to $400 million tied down in these (probably by early 2024), cash flow generation will be extremely poor. You can extrapolate net income to probably go negative if you use proportionate interest expenses and boost real estate operating costs as more properties are managed.

{kind=link}

Yes, we reach that conclusion even taking out the one-time merger transaction-related expenses.

Ready, But Not Steady

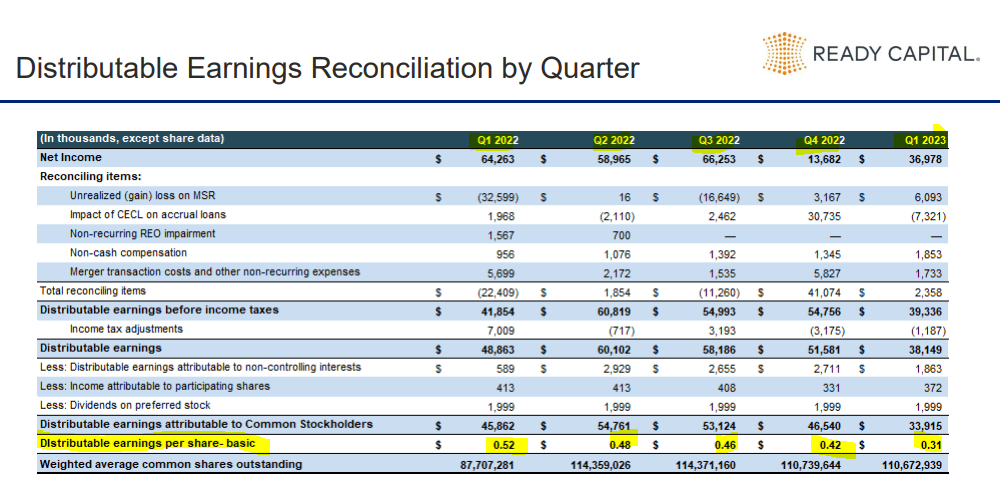

Ready Capital did not impress either on the earnings front. Distributable earnings (a metric shown by the company itself) came in at 30 cents a share versus the 40 cents of distributions.

{kind=link}

The company noted that the unrealized gains impacted it badly, and you can see it on this metric here.

{kind=link}

That is of course accurate, but another way to look at it is that the unrealized losses are still very small and likely to get far larger into a recession. Anyone who has not been star-struck by the distribution yield would have noticed just how rapidly the company's own coverage metric has been collapsing.

{kind=link}

That trend is consistent, if nothing else.

Valuation & Verdict

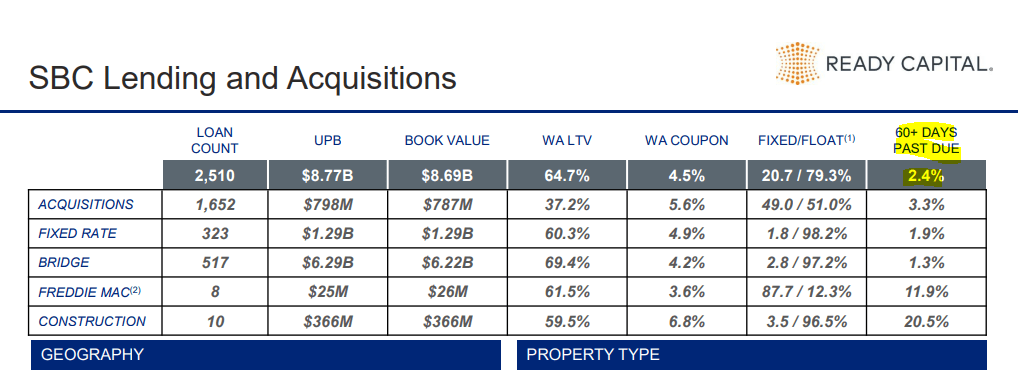

Ready Capital's loans 60 days past due were at 2.4% in June 2022 .

{kind=link}

That went to 3.2% in Q3-2022.

{kind=link}

At year-end 2022, we were at 3.9%.

Q1-2023 saw this go to 4.1%.

{kind=link}

The base run-rate for Ready Capital already looks like it cannot keep up with the distribution. We will add another 62 million shares on BRMK's closing, and that side of the equity will produce progressively less income over time. Sure, some loans will be paid off and can be reinvested, but we doubt Ready Capital will be levering up into the recession. Realistically, 25 cents a quarter is what is sustainable after the two companies merge. That does not mean that they need to cut right away. Overpayment can sometimes continue for a long time in the case of REITs before the reality is acknowledged. Investors will still claim they were "surprised" when it happens. Inovalis REIT ( INO.UN:CA) was a funny example of that, as it clearly showed a distribution coverage ratio of about 50% for five quarters before it finally cut the distribution. The stock still tanked 40% in the week after the cut was announced. One could argue that only the most naïve would believe anyone could sustain a 200% payout ratio indefinitely. But that was precisely what the holders believed until the rug was pulled.

Preferred Securities

There are still two ways to play Ready Capital that make sense here. One is of course the preferred shares. Ready Capital Corporation 6.50% CUM PFD E ( RC.PE ), a fixed rate preferred, looks delightfully juicy here with a 9% yield. The case for this is bolstered as the BRMK deal will lower overall leverage. Even before the deal, one must keep in mind that Ready Capital was running primarily non-recourse leverage.

{kind=link}

Sure, you are getting less yield here, but that is because the common shares distribution has not been realigned to what the company can generate. That is an opinion based on the above set of numbers, so you can deal with it as you see fit. RC.PE's 9% is much better than the 15% on RC.

Ready Capital Corporation 7% CN SR NT 2023 ( RCA ) is another way to play this, albeit for a very short while. These are convertible notes due on August 15, 2023. The price of Ready Capital common stock is nowhere near the required price for conversion.

The Notes will be convertible by holders into shares of the Company's common stock at an initial conversion rate of 1.4997 shares of common stock per $25 principal amount of Notes, which is equivalent to an initial conversion price of approximately $16.67 per share of common stock. Upon conversion, holders will receive, at the Company's discretion, cash, shares of the Company's common stock or a combination thereof.

Source: Quantum Online

So you can expect $25.00 plus one more distribution from a $24.85 entry price. So for a shorter term safe security, this is a great place to make decent returns over the next three months.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Broadmark And Ready Capital: Quite The Deterioration In Q1-2023